Nvidia just guided to $91 billion in second-quarter revenue, authorised an $80 billion share buyback, and raised its dividend 25-fold. The stock fell anyway. The Q1 FY2027 earnings release, published after the close on 20 May 2026, represents one of the most consequential quarterly reports of the AI era, with Nvidia sitting at the centre of virtually every major data centre and artificial intelligence system worldwide. The paradox is stark: a record-setting quarter, a guidance beat that cleared consensus by more than $4 billion, and a capital return programme of historic scale, all met with a negative after-hours reaction. What follows breaks down exactly what Nvidia reported, what the forward outlook signals, and why investors sold the news on numbers that would be transformational for almost any other company.

Record quarter: what Nvidia actually reported for Q1 FY2027

The scale of the quarter is best understood through the numbers themselves.

- Total revenue: $81.6 billion, up 20% quarter-over-quarter from $68.1 billion in Q4 FY2026 and 85% year-over-year

- Data centre revenue: $75.2 billion, accounting for approximately 92% of total revenue

- Non-GAAP gross margin: 75.0%

- Non-GAAP EPS: $1.87, against analyst consensus of approximately $1.77-$1.78

Nvidia’s revenue grew 85% year-over-year, making Q1 FY2027 the largest quarterly haul in the company’s history and one of the largest single-quarter revenue prints ever recorded by a semiconductor firm.

Every major line item cleared expectations. The data centre segment, powered by demand for AI training and inference accelerators, now constitutes such a dominant share of the business that Nvidia’s overall trajectory is effectively a proxy for global AI infrastructure spending. The earnings-per-share beat of roughly $0.09-$0.10 above consensus confirmed that margin discipline held even as volumes scaled.

When big ASX news breaks, our subscribers know first

The $91 billion Q2 outlook and what the China carve-out reveals

The forward guidance extended the beat. Nvidia issued a Q2 FY2027 revenue outlook of $91.0 billion, plus or minus 2%, implying a range of approximately $89.1-$92.8 billion. That midpoint cleared the LSEG consensus of approximately $86.84 billion by more than $4 billion.

| Metric | Q2 FY2027 Guidance | Analyst Consensus | Variance |

|---|---|---|---|

| Revenue | $91.0 billion | ~$86.84 billion | +~$4.2 billion |

| Non-GAAP gross margin | ~75.0% | N/A | Stable |

Why the China exclusion matters to the guidance quality

Embedded in the $91 billion figure is a consequential assumption: zero China data centre compute revenue. U.S. export restrictions on advanced AI chips have effectively shut Nvidia out of one of the world’s largest potential markets for high-end accelerators. The zero-revenue assumption is conservative by design. It could represent upside if policy eases, or it could prove to be a structural ceiling if restrictions tighten further.

Nvidia’s China revenue collapsed from approximately $6 billion in FY2024 to near zero by Q1 FY2026, a structural reset rather than a cyclical dip, with domestic rivals led by Huawei Ascend now holding an estimated 70-80% of China’s AI accelerator market and institutional investors treating any China recovery as a call option on geopolitical resolution rather than a base-case input.

For analysts evaluating the quality of the guide, this distinction matters. A $91 billion quarter built entirely without China revenue signals extraordinary demand from the rest of the world. It also means the forward trajectory depends on whether non-China customers alone can sustain sequential growth at this pace.

Understanding “beat and raise” quarters and why stocks sometimes fall anyway

A “beat and raise” is the strongest possible earnings outcome: a company reports results above consensus and then guides the next quarter higher than analysts expected. Under normal conditions, this combination drives shares higher. For a stock trading at Nvidia’s valuation, the dynamic is different.

Three mechanisms explain why a strong quarter can still produce a negative price reaction:

Priced-in expectations are not unique to Nvidia: with 84% of S&P 500 companies beating EPS estimates in Q1 2026, well above the 10-year average of 76%, the market has broadly learned to anticipate beats, compressing the incremental share price gain that any single strong report can generate.

- Priced-in expectations. When a stock has risen substantially into an earnings event, the reported beat may already be reflected in the share price. The market’s reaction is not to the absolute quality of the numbers but to the gap between those numbers and what was already assumed.

- Whisper numbers. Published consensus is not the only bar. For high-profile names, institutional investors carry informal “whisper” estimates that sit above consensus. If the beat clears the published bar but falls short of the whisper, the stock can trade lower.

- Sell-the-news positioning. Traders who bought ahead of earnings to capture the anticipated beat may take profits on the release itself, regardless of what the numbers show.

Analysts have framed the reaction as evidence that Nvidia must “continually exceed a very high bar” to move the stock materially higher from current levels.

Nvidia’s after-hours decline was approximately 0.56%, with shares falling to roughly $222.21 from a regular session close of $223.47. Some early reports characterised the move as greater than 2%; the actual decline was considerably more modest. The valuation asymmetry remains the core issue: strong execution maintains the stock roughly where it is, while any deceleration signal can produce outsized downside.

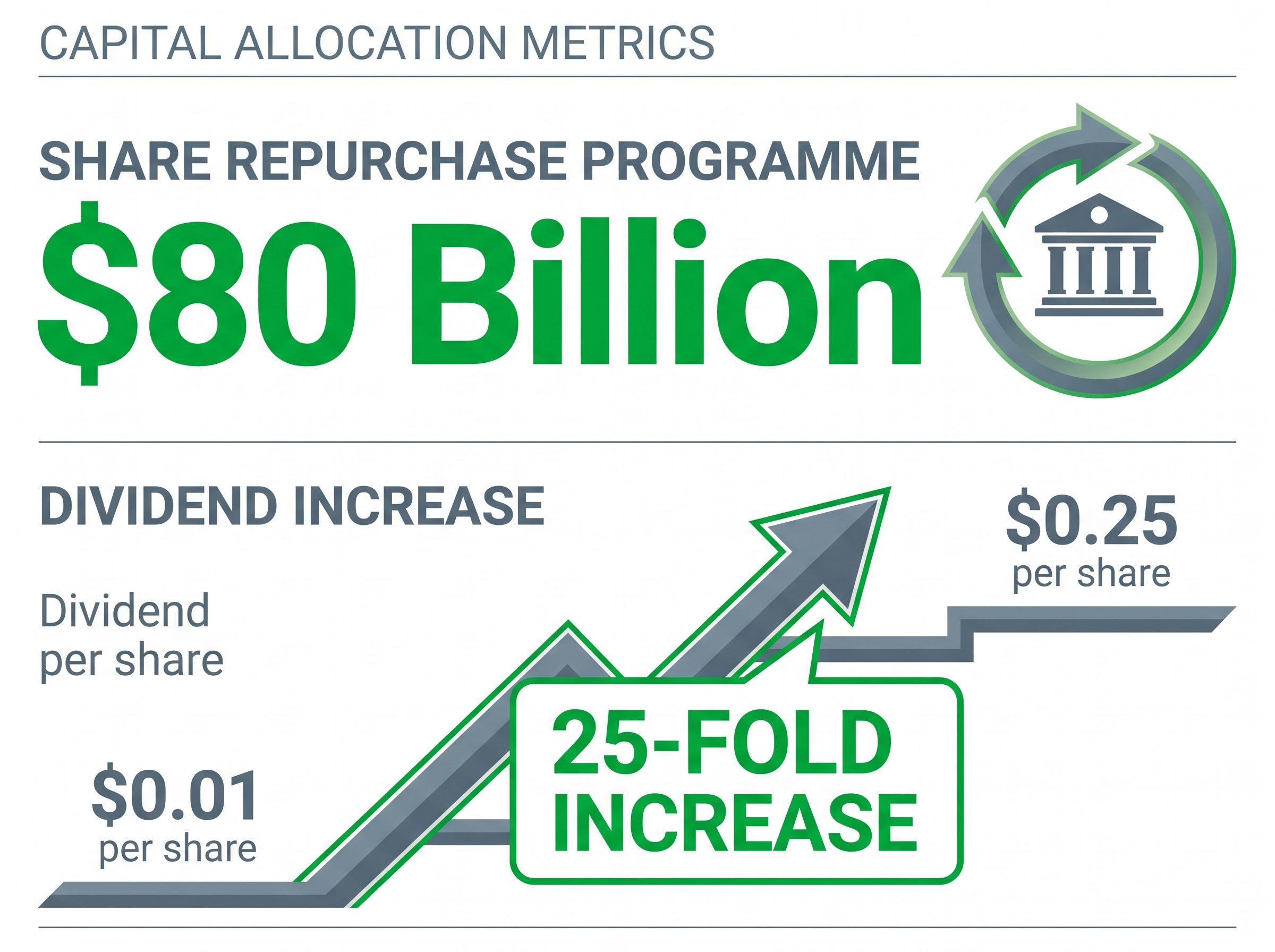

The $80 billion buyback and 25-fold dividend increase: confidence signal or maturity signal?

Nvidia authorised an $80 billion share repurchase programme and raised its quarterly dividend from $0.01 to $0.25 per share, a 25-fold increase.

The bull and bear cases for a capital return programme of this scale split along a single question: what it says about the company’s internal reinvestment opportunity.

- Bull case: Management is signalling confidence that cash generation from AI demand is durable and growing. The buyback offsets stock-based compensation dilution, supports earnings-per-share growth, and the higher dividend broadens the shareholder base to include income-oriented investors.

- Bear case: A high-growth company returning $80 billion to shareholders could indicate that the marginal return on internal reinvestment, whether in R&D, foundry partnerships, or acquisitions, is becoming harder to justify relative to buybacks.

Nvidia carries significant ongoing commitments across new chip architectures, networking, and software. Whether this programme represents surplus confidence or a subtle shift in capital allocation philosophy is a question the market has not yet resolved.

Nvidia’s capital return strategy has drawn specific analyst attention since Bank of America’s Vivek Arya argued that raising the dividend yield to 0.5%-1.0% could expand the institutional buyer base and catalyse a multiple re-rating independent of the AI demand case, a thesis that predates the $80 billion buyback authorisation but gains new analytical force in light of it.

The next major ASX story will hit our subscribers first

The competitive threat taking shape around Nvidia’s core business

Combined AI-related capital expenditure from major U.S. technology firms is projected to surpass $700 billion in 2026, up from roughly $400 billion in 2025. That spending trajectory is the tailwind underpinning Nvidia’s growth. The question is how much of the incremental spend continues to flow through Nvidia versus alternatives now under active development.

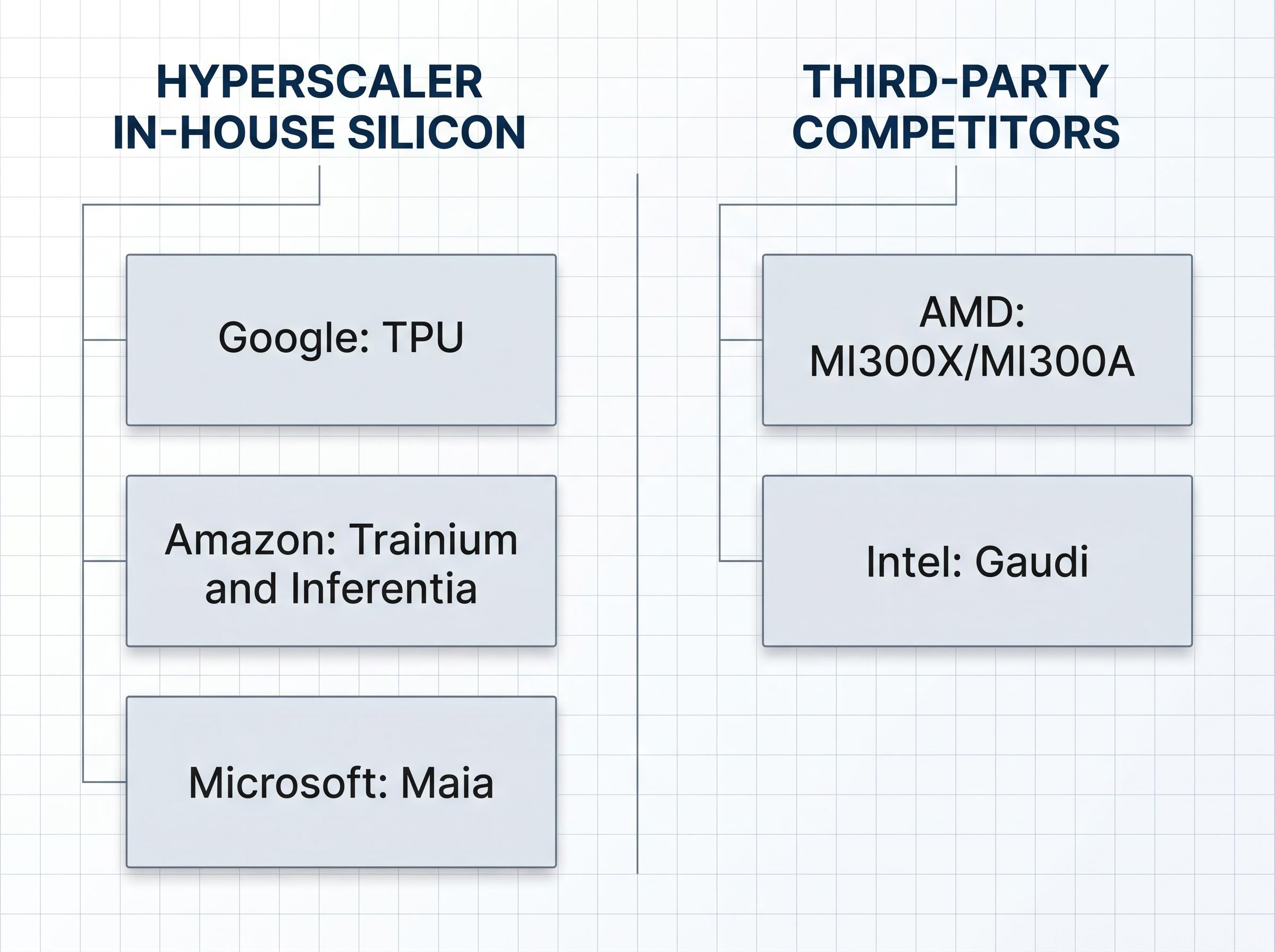

Hyperscaler in-house silicon: building away from Nvidia

The largest cloud providers are investing in proprietary chips designed to reduce their dependence on Nvidia, particularly for inference workloads where total cost of ownership matters as much as peak performance.

- Google TPU: multiple generations deployed for both training and inference across Google Cloud and internal workloads

- Amazon Trainium and Inferentia: purpose-built for training and inference respectively, with pricing structured to undercut Nvidia on cost per inference

- Microsoft Maia: the newest entrant, designed to serve Azure AI workloads and give Microsoft direct control over its accelerator roadmap

AMD, Intel, and the inference battleground

Beyond in-house silicon, two third-party competitors are gaining traction in the cost-sensitive inference segment.

- AMD MI300X/MI300A: confirmed deployments at Microsoft Azure and positioning as a direct alternative to Nvidia’s high-end accelerators, with growing analyst attention on inference share gains

- Intel Gaudi: differentiated through an open software stack and marketed as a lower-cost training and inference option, adopted by select cloud providers and OEMs

Nvidia’s March 2026 partnership with Groq on a new CPU and AI inference system suggested a defensive awareness of the inference battleground’s importance. The collective weight of these alternatives does not threaten Nvidia’s near-term dominance, but it feeds a narrative that incremental AI spending may gradually diversify away from a single supplier.

Bloomberg Intelligence projects AI accelerator market growth to $604 billion by 2033, with the custom ASIC segment expanding at a 27% compound annual rate, a trajectory that frames why hyperscalers are accelerating in-house silicon development even as Nvidia continues to dominate near-term shipment volumes.

What Nvidia’s numbers say about the AI investment cycle right now

Taken together, the $81.6 billion in Q1 actuals and the $91 billion Q2 guide tell a sequential growth story that points in one direction: enterprise and hyperscaler AI infrastructure investment remains in full acceleration, not moderation. The $700 billion-plus projected AI capex for 2026 provides the macro context.

The macro context behind these numbers is significant: hyperscaler AI capex commitments reached $130 billion in Q1 2026 alone across Amazon, Microsoft, Alphabet, and Meta, pushing full-year 2026 combined projections to $725 billion and placing the industry on a trajectory toward $1 trillion in annual spend by 2027.

The sustainability question is not whether AI demand exists. It is whether the current growth rate is episodic, whether spending may normalise after the initial build-out cycle, and whether Nvidia’s share of incremental capex compresses as custom silicon and competing architectures mature.

The core tension the market is pricing is this: Nvidia’s execution has been extraordinary, but the valuation leaves no room for anything less. A record quarter can confirm the thesis without expanding the multiple, which is why the stock slipped approximately 0.56% after hours on the strongest results the company has ever reported.

That tension is unlikely to resolve in a single quarter. For investors, the signal from 20 May 2026 is that the AI infrastructure cycle is intact, but the bar for Nvidia to move materially higher from here is set by the market’s own expectations, not by the company’s ability to deliver.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.