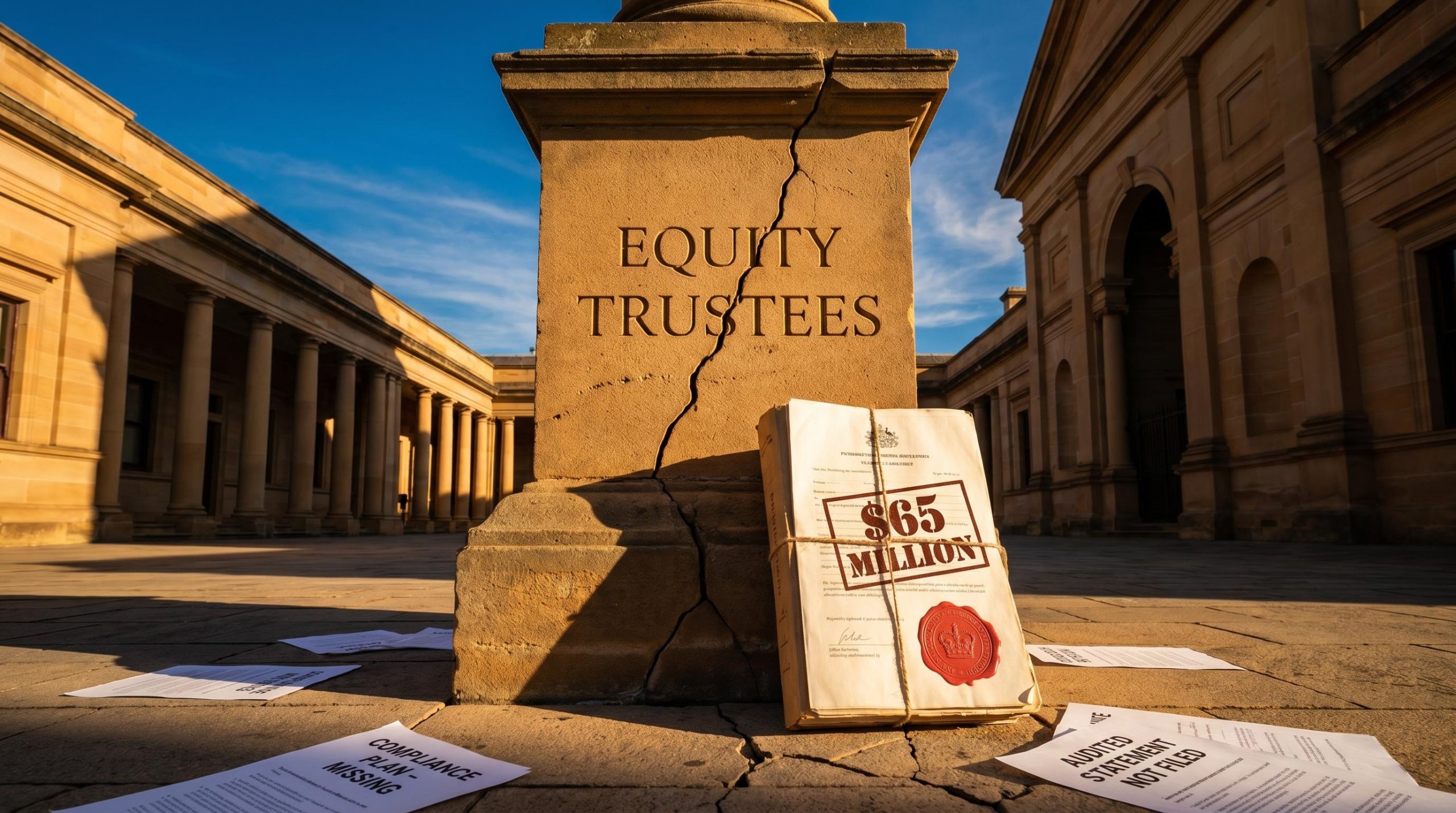

ASIC Sues Equity Trustees Over $65M Shield Master Fund Failures

1 hr ago

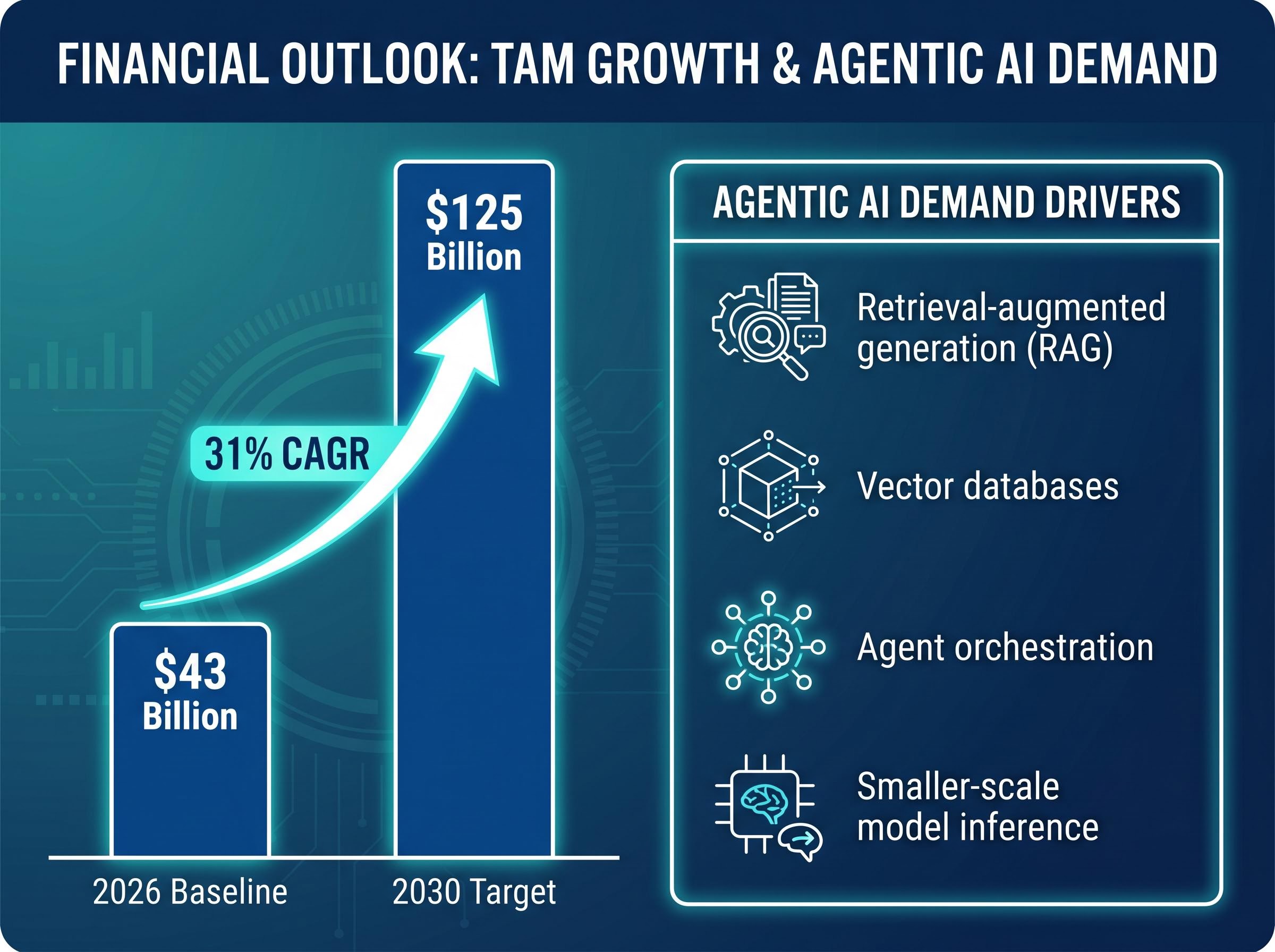

Bank of America just raised its server CPU total addressable market (TAM) estimate to as much as $125 billion by 2030, projecting a 31% compound annual growth rate, and named two specific stocks as the primary beneficiaries. The note, published 20 May 2026 by analyst Vivek Arya’s team, arrives as AMD is already posting record server CPU revenue and Nvidia is preparing to enter the CPU market directly with its Vera platform. For investors positioning around AI infrastructure spending, the distinction matters: this is about which semiconductor names are levered to CPU growth, not just GPU demand. What follows is a breakdown of BofA’s vendor-by-vendor share projections for 2030, the structural reason agentic AI is driving the CPU TAM revision upward, and the specific Buy-rated stocks with price targets that the bank sees as actionable today.

BofA raised its server CPU TAM estimate from a prior $110 billion to $125 billion by 2030, starting from an approximate $43 billion baseline in 2026. This is not a routine estimate tweak. The revision rests on a specific thesis about where AI infrastructure spend is heading next.

31% projected CAGR from BofA’s 2026 baseline to its 2030 server CPU TAM target of $125 billion.

The driving force, according to BofA, is agentic AI. Unlike the GPU-dominated training phase of AI development, agentic workloads are CPU-intensive in ways that shift the infrastructure spending mix. The four workload categories BofA cites as demand drivers:

BofA frames this CPU expansion as additive to, not a replacement of, GPU demand. AI accelerators are still projected to account for roughly $1.2 trillion of an overall $1.7 trillion AI data centre market by 2030. Server CPUs, even at $125 billion, would represent only approximately 5-6% of total data centre systems expenditure. The significance lies in the growth rate, not the absolute share of spend.

Hyperscaler AI capex commitments provide the demand foundation beneath BofA’s TAM projections: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion on AI infrastructure in Q1 2026 alone, with full-year 2026 combined guidance reaching approximately $725 billion, a spending rate that structurally validates multi-year CPU procurement growth independent of any single analyst model.

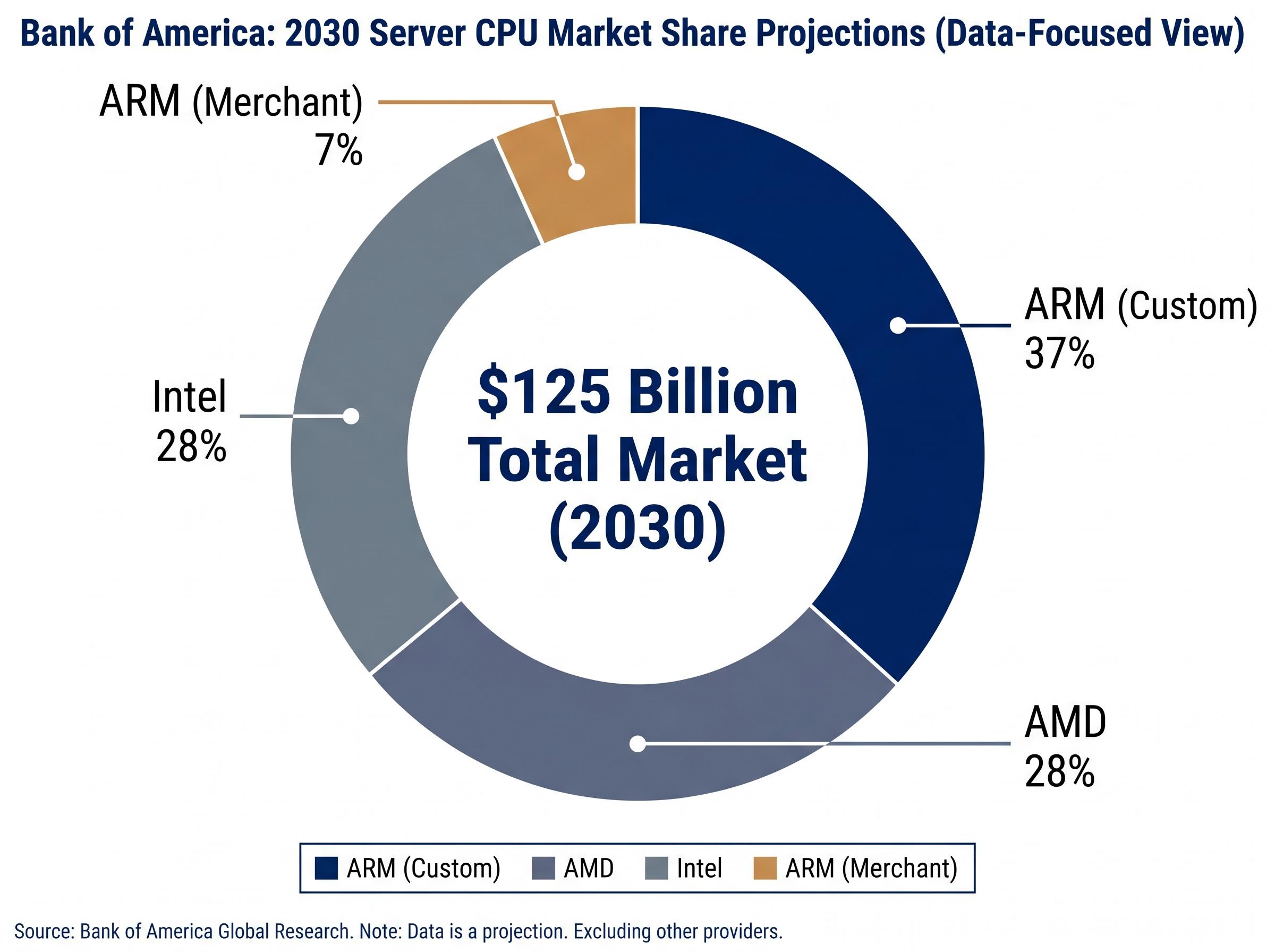

ARM-based custom silicon currently holds an estimated 15% of server CPU market value. BofA projects that figure reaching approximately 37% by 2030, with an additional 7% coming from ARM-based merchant CPUs (those sold commercially rather than designed in-house by hyperscalers).

The projection rests on three specific hyperscaler programmes that are already deployed at scale.

| Vendor | Product Name | Architecture Basis | Key Performance Claim |

|---|---|---|---|

| AWS | Graviton4 | ARM (custom) | Up to 30% faster than Graviton3; up to 40% better price-performance vs x86 |

| Google Cloud | Axion | ARM Neoverse V2 | Improved performance and energy efficiency vs x86 instances |

| Microsoft Azure | Cobalt 100 | ARM (custom) | Performance-per-watt emphasis vs prior-generation x86 instances |

All three major cloud providers have committed multi-year engineering investments to their custom ARM chip programmes. AWS Graviton4 delivers up to 75% more memory bandwidth than its predecessor. Google announced Axion in April 2024 on the ARM Neoverse V2 architecture. Microsoft has deployed Cobalt 100 across Azure services with an emphasis on performance-per-watt improvements.

The price-performance advantages are recurring, not one-time. Each new generation compounds the gap versus equivalent x86 instances, making reversion to x86 procurement unlikely at scale. For investors, the ARM trajectory represents the primary structural force reshaping server CPU economics ahead of BofA’s Intel assessment.

ARM supply constraints represent a near-term complication for the custom silicon trajectory BofA models: Arm’s AGI CPU attracted more than $2 billion in forward hyperscaler demand against confirmed supply covering only roughly half that figure, with TSMC 3nm and 2nm capacity acting as the primary bottleneck through FY2027-FY2028.

BofA projects Intel holding approximately 28% of server CPU market value by 2030, losing share in both cloud and enterprise segments simultaneously. The arithmetic is straightforward.

28% of $125 billion implies approximately $35 billion in server CPU revenue for Intel by 2030, in a market it once controlled near-exclusively.

Intel held a near-monopoly position in server CPUs as recently as a few years ago. The projected 28% share represents a permanent structural ceding of the market, not a cyclical dip awaiting recovery.

The pressure comes from two directions at once:

UBS corroborated this trajectory in May 2026, confirming that AMD and ARM-based solutions continued gaining server CPU share at Intel’s expense during Q1 2026. BofA’s 28% projection is the base case under continued share erosion, not a floor.

Citi’s server CPU forecast, published two days before BofA’s note, projects an even larger market of $131.5 billion by 2030 and introduces a separately defined agentic CPU segment growing at a 185% CAGR, though Citi’s vendor share projections diverge sharply from BofA’s, assigning Intel 47% and AMD 34% rather than the 28%-each split BofA models.

AMD reported record server CPU revenue in Q1 2026, with growth exceeding 50% year-over-year. Mercury Research data pinned AMD’s x86 server CPU revenue share at 46.2% and unit share at 33.2%.

Mercury Research data on AMD’s x86 share also captures AMD’s data center revenue reaching $5.8 billion in Q1 2026, providing the granular segment-level figures behind the headline share gains that BofA cites in its vendor projections.

Those figures coexist with BofA’s 28% projected share because they measure different markets. AMD’s 46.2% is x86-only market share. BofA’s 28% is AMD’s projected share of the total server CPU market including ARM. The distinction is the key to reading the Buy thesis correctly: AMD is already winning the x86 battle while BofA models ARM capturing 37% of the broader market.

BofA maintains a Buy rating on AMD with a $500 price target. AMD closed at $414.05 on 19 May 2026, implying approximately 21% upside to target.

| Metric | Current (Q1 2026, x86 only) | BofA 2030 Projection (total market incl. ARM) |

|---|---|---|

| AMD Revenue Share | 46.2% | ~28% |

| AMD Unit Share | 33.2% | Not separately specified |

BofA designated AMD as the “preferred x86 name” and modestly raised financial estimates while keeping the $500 price target unchanged. AMD’s own updated TAM outlook of greater than $120 billion by 2030 is broadly consistent with BofA’s estimate, reinforcing the alignment between company guidance and independent analyst modelling.

Investors who think of Nvidia purely as a GPU company need to reassess. The Vera Rubin platform, announced 16 March 2026 with H2 2026 planned availability, represents Nvidia’s entry into the server CPU market through a fundamentally different approach than AMD or Intel.

The platform integrates three layers into a rack-scale system:

A complete Vera Rubin pod approaches a roughly 1:1 CPU-to-GPU ratio, illustrating that CPU capacity is a first-class design consideration in Nvidia’s architecture, not an afterthought.

BofA’s framing positions Nvidia as a server CPU TAM beneficiary not as an x86 vendor competing chip-for-chip, but as a full-stack provider that embeds CPUs within integrated systems. BofA maintains a Buy rating on Nvidia. The competitive implication is that Nvidia is packaging the CPU as part of a system-level approach, expanding the definition of who benefits from server CPU TAM growth beyond traditional CPU vendor rankings.

For investors wanting to extend the Nvidia analysis beyond its CPU market entry, our full explainer on Nvidia’s five investor debates covers gross margin sustainability near 75%, Vera Rubin architecture design win signals, and BofA’s $320 price target rationale, all of which connect directly to Nvidia’s positioning as a full-stack AI systems vendor rather than a discrete CPU competitor.

BofA’s 2030 share framework, viewed in one place, clarifies the competitive landscape: ARM at 37%, AMD at 28%, and Intel at 28%. AMD holds x86 share parity with Intel while ARM captures the growth delta from hyperscaler custom silicon.

The two Buy-rated picks carry distinct investment theses:

| Stock | Rating | Price Target | Key Thesis | 2030 Role in CPU Market |

|---|---|---|---|---|

| AMD | Buy | $500 | Preferred x86 name; share gain trajectory | ~28% total market share; x86 leader |

| Nvidia | Buy | Not specified in this note | Full-stack rack-scale CPU integration | TAM beneficiary via Vera Rubin platform |

BofA’s Vivek Arya team published the note on 20 May 2026, providing a vendor-level roadmap into a market still early in its growth curve.

BofA’s TAM revision reflects a structural shift in AI infrastructure spending toward CPUs as agentic workloads scale. The share projections (ARM at 37%, AMD and Intel each at 28%) are directional theses backed by already-observable Q1 2026 data, not speculative targets detached from current performance.

All major CPU vendors could potentially post double-digit annual sales growth within this market through 2030, but BofA’s Buy ratings concentrate conviction in AMD and Nvidia specifically.

For investors evaluating semiconductor positioning in mid-2026, the framework is specific, dated, and analyst-backed. AMD offers the x86 consolidation thesis with a named price target and demonstrated share momentum. Nvidia offers the system-level integration thesis through a platform shipping later this year. The server CPU opportunity is broader than traditional vendor rankings suggest, and BofA’s note provides a usable structure for thinking about which names carry the most direct exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The server CPU total addressable market (TAM) is the total revenue opportunity across all server processor sales globally. Bank of America estimates it will reach $125 billion by 2030, growing at a 31% CAGR from a roughly $43 billion baseline in 2026, making it a significant growth segment for semiconductor investors.

Agentic AI workloads such as retrieval-augmented generation, vector databases, agent orchestration, and smaller-scale model inference are CPU-intensive, shifting some AI infrastructure spend away from GPU-dominated training toward CPU-heavy deployment, which Bank of America identifies as the structural driver behind its upgraded TAM estimate.

AMD held 46.2% of x86 server CPU revenue share in Q1 2026 according to Mercury Research, but Bank of America projects AMD will hold approximately 28% of the total server CPU market by 2030, a figure that includes ARM-based custom silicon capturing an estimated 37% of the broader market.

Nvidia's Vera Rubin platform, announced in March 2026 with planned H2 2026 availability, integrates Vera CPUs co-designed for agentic AI workloads with Rubin next-generation GPU accelerators into a rack-scale system, positioning Nvidia as a full-stack server CPU TAM beneficiary rather than a traditional discrete CPU vendor.

Bank of America maintains a Buy rating on AMD with a $500 price target, which implied approximately 21% upside from AMD's closing price of $414.05 on 19 May 2026, the day before the note was published.