Webjet Group shares fell as much as 15% on Wednesday after the company reported that underlying profit dropped 24% for the year, with the damage compounded by a simultaneous announcement that Virgin Australia will cut the commissions it pays the travel platform from 1 July 2026. The FY26 results land at a difficult moment: bookings through the online travel agency (OTA) are already running 12% below last year’s pace as of mid-May, consumer confidence remains weak, and the company is in the middle of a deliberate investment cycle in technology, people, and marketing that is suppressing near-term profit. What follows unpacks the headline numbers, explains why the statutory and underlying profit figures tell different stories, examines what each division actually delivered, and lays out what management says is coming in FY27.

Shares fall approximately 13% as results and Virgin Australia news land on the same morning

Webjet Group (ASX: WJL) shares dropped approximately 13% on 20 May 2026, falling from a previous close of $0.49 to around $0.425, with the stock touching intraday lows that exceeded 15% at points during the session. The day’s trading range ran from $0.400 to $0.435 on elevated volume.

The severity of the sell-off reflected the fact that two separate ASX announcements hit the market simultaneously:

- FY26 full-year financial results for the year ended 31 March 2026, reporting a 24% decline in underlying net profit after tax (NPAT).

- Change to commercial agreements with Virgin Australia, confirming revised commission terms that reduce payments on flight and ancillary sales from 1 July 2026.

Webjet Group shares fell approximately 13% to a post-demerger low, their weakest level since the company began trading as a standalone entity under the WJL ticker.

Either announcement in isolation could have prompted a moderate repricing. Their convergence gave the market two reasons to sell in the same session: weak earnings and a forward revenue headwind with a specific start date.

The severity of the sell-off is consistent with how the expectations gap works in practice: the market had already formed a view on Webjet’s trajectory, and the combination of a weak underlying result with a concurrent revenue headwind announcement meant the actual outcome landed below what was priced in, regardless of how the statutory headline read.

When big ASX news breaks, our subscribers know first

The headline numbers: revenue holds, but profit falls sharply

Revenue increased 1% to $136.4 million in FY26. That stability at the top line makes the profit decline that follows harder to explain as a demand problem.

Underlying earnings before interest, tax, depreciation, and amortisation (EBITDA) fell 20% to $28.1 million. Underlying NPAT fell 24% to $13.6 million. Total transaction value (TTV) declined 3% to $1.46 billion, while total bookings dropped 7% to 1.4 million.

The statutory NPAT figure moved in the opposite direction, rising 85% to $3.7 million, a divergence large enough to warrant its own explanation in the following section.

| Metric | FY26 | Change |

|---|---|---|

| Total transaction value (TTV) | $1.46 billion | -3% |

| Revenue | $136.4 million | +1% |

| Underlying EBITDA | $28.1 million | -20% |

| Underlying NPAT | $13.6 million | -24% |

| Statutory NPAT | $3.7 million | +85% |

Management attributed the margin compression to deliberate investment in personnel, technology, and marketing, with some offset from cost management measures and AI-driven efficiency initiatives. The question for investors is whether this spending is a temporary drag on an otherwise stable business or the beginning of a longer squeeze.

What statutory profit rising 85% while underlying profit fell 24% actually means

On paper, Webjet Group reported two profit figures that appear to contradict each other. Statutory NPAT rose 85% to $3.7 million. Underlying NPAT fell 24% to $13.6 million. Both numbers are accurate; they simply measure different things.

- Statutory NPAT is the profit figure calculated under accounting standards. It includes all items, whether recurring or one-off: restructuring credits, asset sale gains, impairment reversals, demerger-related adjustments, and any other non-recurring charges or benefits.

- Underlying NPAT strips out those one-off items to isolate the company’s recurring operating performance, the earnings the business generates from its day-to-day activities.

Underlying NPAT is the metric management and analysts typically use to assess a company’s repeatable earnings power, because it removes the noise of items that are unlikely to recur.

The gap between the two figures, approximately $9.9 million, represents the net effect of non-recurring items present in the statutory result. In the prior year, those items had been a larger drag, which is why the statutory figure improved so sharply in percentage terms even as the operating result deteriorated.

The distinction between GAAP and non-GAAP earnings is not unique to Webjet; it is a standard feature of how listed companies present results, and the gap between the two figures can grow substantially when restructuring credits, asset revaluations, or demerger adjustments are present in any given period.

Retail investors who look only at the statutory headline could form a misleading impression of operating health. The underlying number provides the clearer read on whether the business is earning more or less from its core operations, and in FY26 the answer was decisively less.

Divisions compared: OTA under pressure, cars resilient, business travel burning cash

The consolidated result obscures three distinct stories playing out inside Webjet Group.

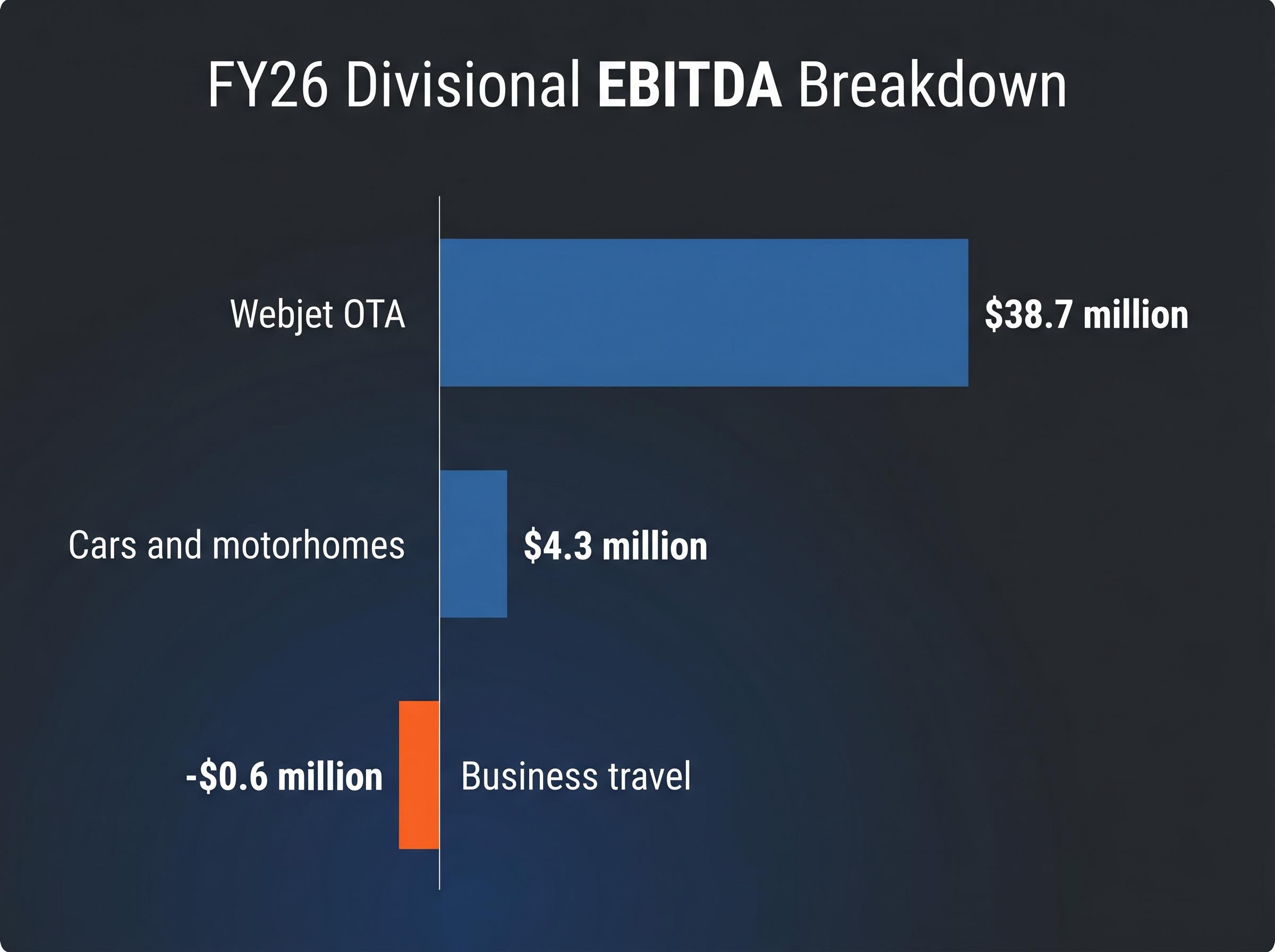

The Webjet OTA division reported EBITDA of $38.7 million in FY26, a result that reflects cost-of-living headwinds, weaker domestic leisure demand, and a shift in the international booking mix toward lower-value short-haul Asian routes. This is the largest segment and the one most exposed to discretionary consumer spending.

ACCC domestic airline competition monitoring through late 2025 documented continued capacity constraints and fare dynamics across Australian routes, conditions that shape the booking volumes and average transaction values flowing through OTA platforms like Webjet.

The cars and motorhomes segment delivered EBITDA of $4.3 million, described by management as a materially improved result and the strongest divisional outcome across the group. The improvement is notable given the broader environment, though the segment remains small relative to the OTA business.

The business travel division contributed $1.2 million in revenue during its initial operating period but recorded an EBITDA loss of $0.6 million. Management has framed this as a deliberate investment-phase outcome. Higher-value business travel bookings partially offset the OTA volume decline in the second half of FY26, helping to narrow the gap between the 3% TTV decline and the 7% drop in total bookings.

| Segment | Key metric | FY26 result | Status |

|---|---|---|---|

| Webjet OTA | EBITDA | $38.7 million | Under pressure |

| Cars and motorhomes | EBITDA | $4.3 million | Improved |

| Business travel | EBITDA | -$0.6 million | Investment phase |

The Virgin Australia commission cut and what FY27 trading data already shows

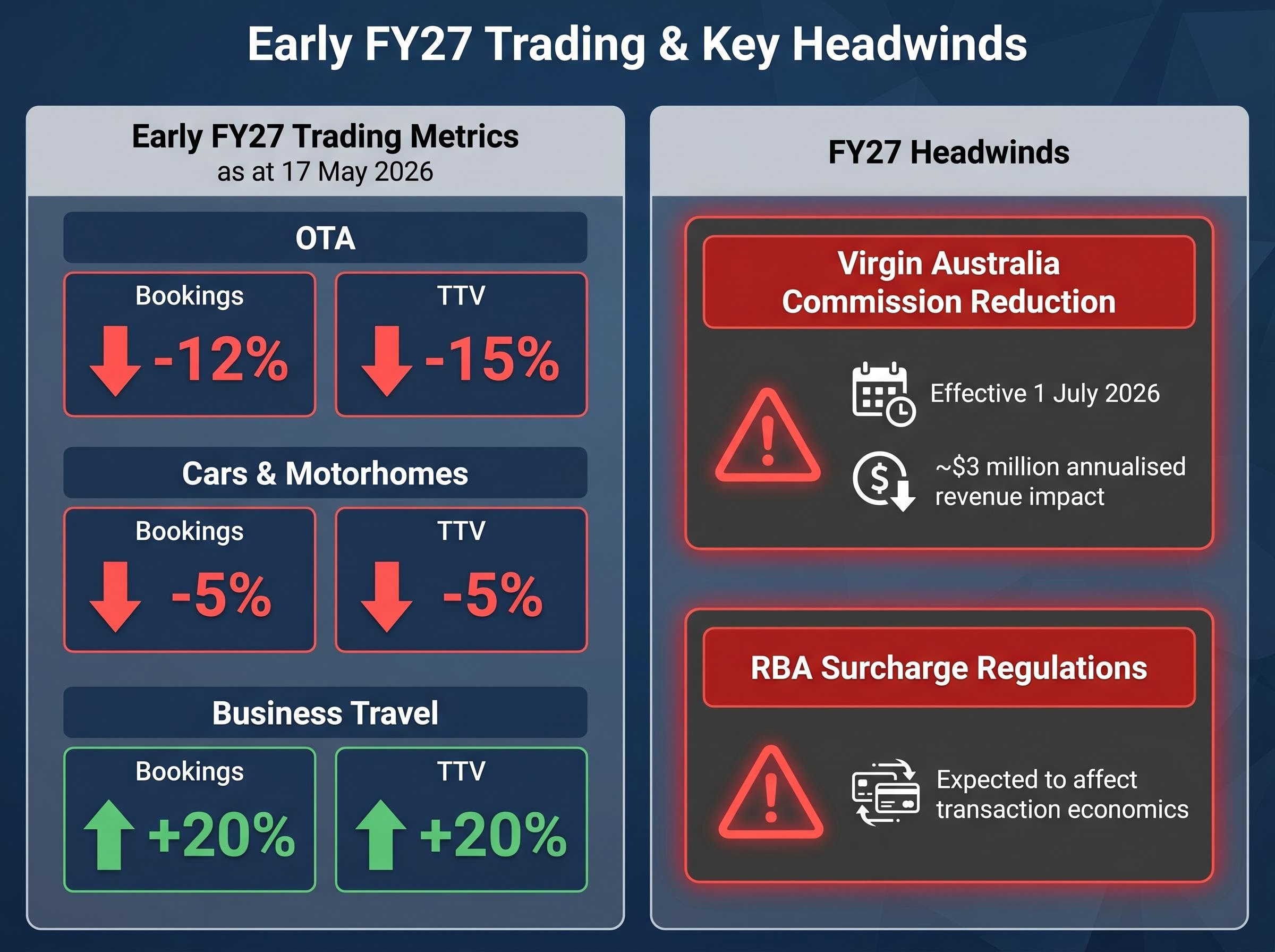

The Virgin Australia commission change is not a speculative risk. The revised terms take effect from 1 July 2026, reducing commission payments on flight and ancillary sales. Had the new terms applied during FY26, revenue would have been approximately $3 million lower, providing a concrete measure of the forward drag.

The Virgin Australia commission changes were disclosed in a separate ASX announcement on 19 May 2026, the day before the full-year results, providing the first quantified estimate of the FY27 revenue headwind before the broader financial picture was released.

Early FY27 trading data confirms that the macro headwinds management described are already showing up in the numbers:

As at 17 May 2026, OTA bookings were down 12% and OTA TTV was down 15% year-on-year, signalling continued volume softness heading into the new financial year.

Cars and motorhomes bookings and TTV were down approximately 5% in constant currency terms over the same period. Business travel direct-to-business bookings and TTV were up approximately 20%, though management noted that momentum is easing.

Three named headwinds are expected to weigh on FY27 earnings:

- Virgin Australia commission reduction, effective 1 July 2026, with an estimated annualised revenue impact of approximately $3 million.

- Reserve Bank of Australia surcharge regulations, which are expected to affect transaction economics.

- Lower variable revenue items, reflecting the weaker booking environment.

Management characterised operating conditions as fluid and challenging, citing Middle East instability, inflationary pressures, and subdued consumer confidence as contributing factors.

Westpac-Melbourne Institute Consumer Sentiment data from May 2026 shows that while the index edged higher from April, consumers remain deeply pessimistic, a backdrop that constrains discretionary spending categories like leisure travel and reinforces the OTA demand softness Webjet is recording in early FY27.

A company investing through a downturn, or a company with a structural problem?

The results leave investors with a question the data alone cannot answer: is the margin compression temporary or permanent?

What management says

The investment thesis from management is straightforward. Deliberate spending on people, technology, and marketing is compressing near-term profit in service of medium-term strategic objectives. AI-driven efficiency initiatives are cited as a partial offset. The business travel division, though currently loss-making, is intended to diversify revenue toward higher-value bookings. Management has stated the company continues to pursue its medium-term strategic objectives.

What the market appears to be pricing in

The market’s response suggests a less sanguine reading:

- The Virgin Australia commission loss is structural and not reversible; it has a start date and a dollar estimate.

- Early FY27 trading data is already negative across the OTA and cars segments.

- The share price has fallen to a post-demerger low, suggesting the market is pricing in deterioration beyond a single weak year.

- Underlying EBITDA fell 20% to $28.1 million despite only a 1% revenue change, illustrating how sharply margins compressed under the investment programme.

The post-demerger low reached on 20 May 2026 represents a significant de-rating from the levels at which the stock was trading during the acquisition talks and buyback resumption in February 2026, when Helloworld and BGH Capital had both submitted indicative proposals and the company held over $133 million in cash.

Business travel bookings and TTV are growing approximately 20%, but momentum is easing. Whether that growth can scale fast enough to offset the OTA headwinds is the open question.

What these results mean for investors watching WJL

Revenue held, but profit fell sharply. A concurrent supplier agreement change added a forward revenue headwind with a specific start date, and early FY27 data points to continued volume softness. The stock’s fall to a post-demerger low reflects a market that is, at minimum, demanding evidence that the investment cycle will produce returns.

The following data points and milestones will provide the next meaningful read on whether the strategy is working:

- OTA booking trend: whether the 12% year-on-year decline stabilises or deepens through the September quarter.

- Business travel revenue trajectory: whether the 20% growth rate holds or continues to ease.

- H1 FY27 EBITDA: the first full reporting period under the new Virgin Australia commission terms.

- Broker price target updates: analyst research notes tied to the FY26 results had not yet been published as of 20 May 2026, with updated coverage expected in the coming days.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements are subject to market conditions and various risk factors.