Nine of the ten largest contributors to US equity market returns between 30 March and 18 May 2026 were AI-linked stocks. Yet two of the most prominent names in that rally carry no economic moat rating whatsoever.

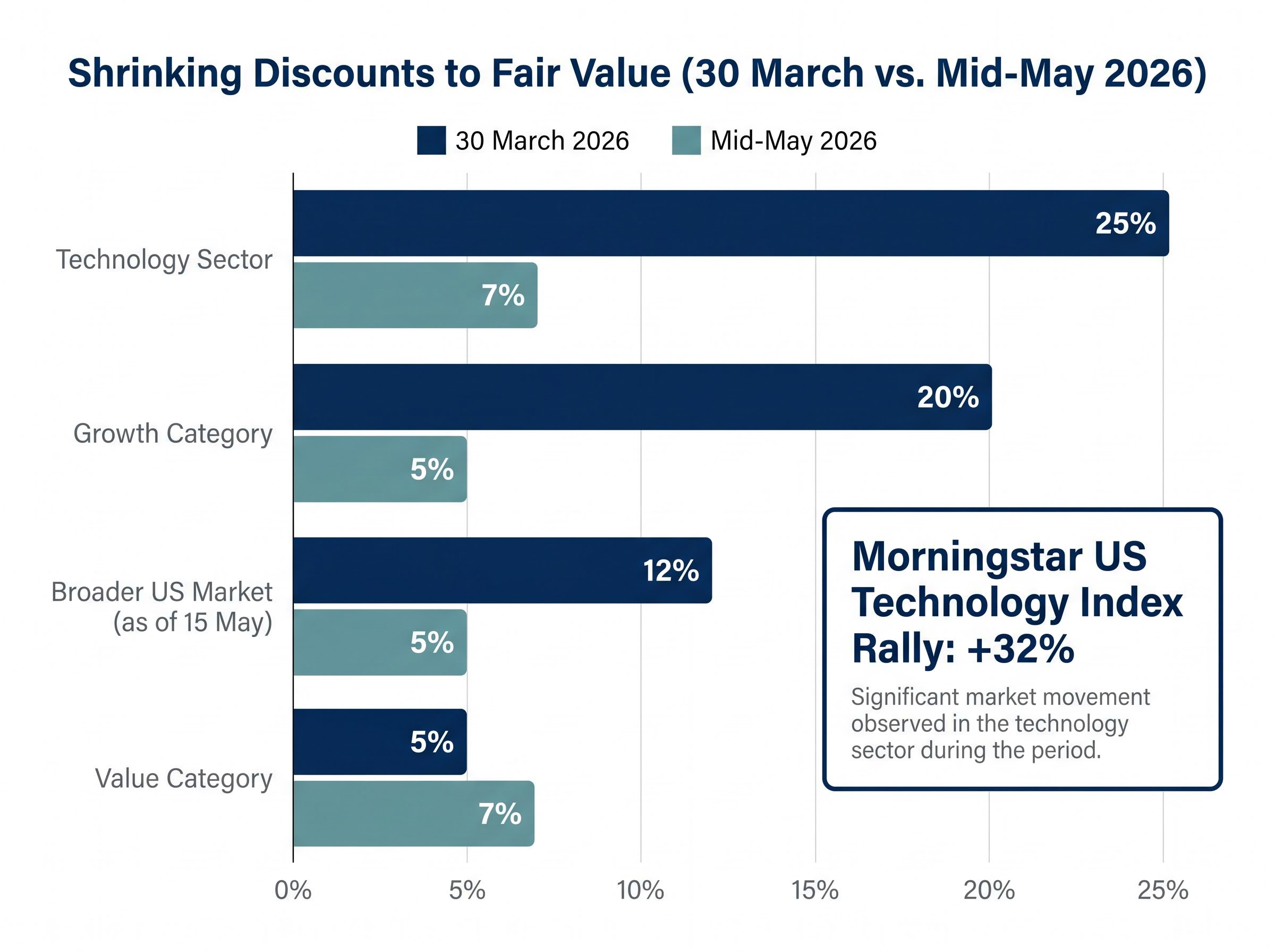

The Morningstar US Technology Index climbed 32% in roughly seven weeks, compressing what had been a 25% discount to fair value down to just 7%. That narrowing matters because it changes the risk calculus for investors still adding AI exposure at current prices. Not all of the appreciation was equally earned. Some of it reflected genuine structural advantage; some of it reflected a market willing to pay for narrative association with artificial intelligence. This analysis provides a framework-driven method for distinguishing between the two, drawing on specific stock-level assessments from Morningstar, Goldman Sachs, and Morgan Stanley across four named companies. The goal is a concrete evaluation lens investors can apply before allocating further capital to an AI investment strategy at mid-2026 valuations.

The 32% rally has changed the math for AI investors

The margin of safety that existed in late March has been largely spent. Between 30 March and 18 May 2026, the Morningstar US Technology Index appreciated 32%, and the valuation discount that underpinned the opportunity compressed sharply across every relevant category.

- Technology sector: discount to fair value narrowed from 25% to 7%

- Growth category: discount narrowed from 20% to 5%

- Broader US market: discount narrowed from 12% to 5% (as of 15 May 2026)

That compression changes the question. In late March, broad AI exposure carried a meaningful cushion. A diversified basket of technology names could absorb a moderate drawdown and still deliver reasonable forward returns. That cushion is now thin enough that selectivity, not sector allocation, becomes the primary driver of risk-adjusted performance.

David Sekera, Morningstar’s Chief US Market Strategist, has recommended shifting toward a balanced value/growth barbell as the prior discount advantage has diminished, enabling ongoing reallocation as relative valuations shift.

The question is no longer whether to own AI. It is which AI, and at what price.

When big ASX news breaks, our subscribers know first

What a durable AI winner actually looks like: the moat test

An economic moat, in its simplest terms, is a structural advantage that allows a company to protect its profits from competitors over a sustained period. In the context of AI, this means more than building a good product. It means building something competitors cannot easily replicate: a software ecosystem with deep switching costs, a platform that locks in customers, or pricing power that persists even when rivals enter the market.

The economic moat framework, formalised by Morningstar into five distinct sources including switching costs, network effects, intangible assets, cost advantage, and efficient scale, is the analytical foundation that separates structurally durable businesses from companies that merely benefit from favourable cycle conditions.

Three institutional frameworks converge on the same core criteria for identifying these advantages. Morningstar evaluates moat rating, capital intensity, single-cycle dependency, and valuation against fair value. Goldman Sachs assesses stack position, revenue visibility, pricing power, and hyperscaler capex sensitivity. Morgan Stanley prioritises proprietary software or platform components, customer concentration risk, and stress-tested valuations against normalised growth.

The following table synthesises these frameworks into a single evaluation lens:

| Dimension | Durable Winner Characteristics | Narrative-Driven Risk Characteristics |

|---|---|---|

| Moat | Wide or narrow; software ecosystem, standards, lock-in | No moat; commodity product with price-taker dynamics |

| Stack Position | Core infrastructure; platform role | Peripheral supplier; single product category |

| Revenue Mix | Proven, recognised AI revenue; diversified end markets | Aspirational AI exposure; single-cycle dependency |

| Cyclicality | Structural secular growth; recurring revenue components | High capex-cycle exposure; boom-bust history |

| Valuation | Reasonable relative to fair value under higher discount rates | Stretched multiples; narrative-driven expansion |

Without a clear framework, investors risk confusing a company’s thematic association with AI for genuine pricing power. These criteria represent the institutional standard for making that distinction.

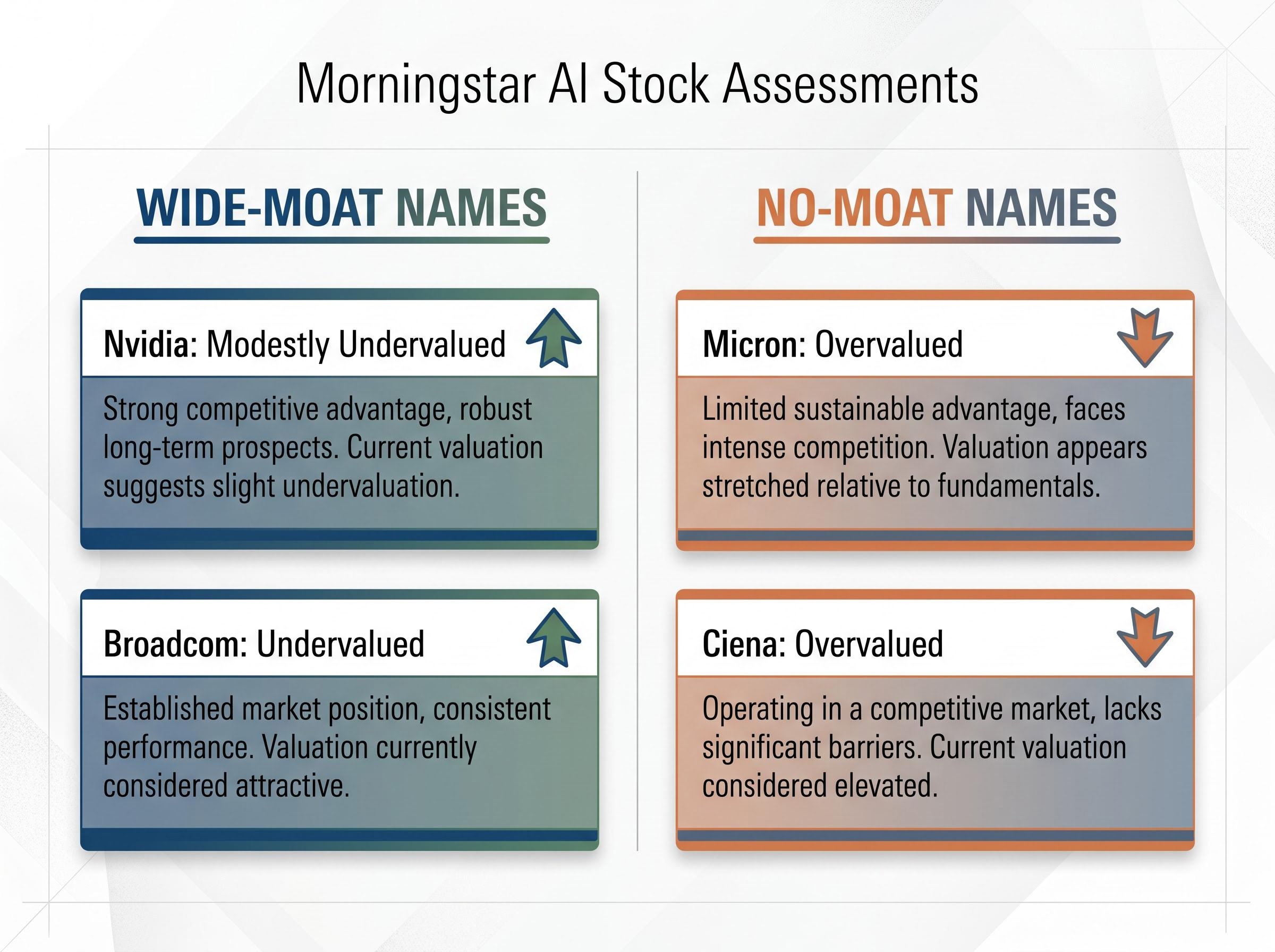

Nvidia and Broadcom: why wide-moat AI names still warrant attention

Nvidia: the software moat hardware competitors cannot easily copy

Nvidia’s wide economic moat, as rated by Morningstar, does not rest on its chips alone. It rests on CUDA, the proprietary software ecosystem that developers, researchers, and cloud providers have built around over more than a decade.

- Morningstar assigns a wide-moat rating, grounded in the CUDA stack and dominant market share in AI data centre accelerators

- Goldman Sachs characterises Nvidia as “the core enabler of AI infrastructure,” citing the combination of hardware performance and software depth that competitors have not matched

- Morgan Stanley highlights deep integration with major hyperscalers (AWS, Google Cloud, Microsoft Azure) and a consistent architecture update cadence from Hopper to Blackwell

- Morningstar views the stock as modestly undervalued following its early May 2026 pullback

The structural thesis is that CUDA’s switching costs make competitive displacement substantially harder than in a commodity hardware market. The risks remain real: China revenue constraints under the export control regime, hyperscaler customer concentration, and semiconductor cycle volatility. These introduce near-term volatility rather than undermining the long-term positioning.

Broadcom: custom silicon and networking as structural rather than cyclical advantages

Broadcom’s wide moat is built differently but carries the same institutional conviction.

- Morningstar assigns a wide-moat rating, citing leading positions in networking chips and custom ASICs with high switching costs for hyperscale customers

- Goldman Sachs names Broadcom among its core AI infrastructure beneficiaries for Ethernet switching chips and custom silicon designed for large cloud providers

- Morgan Stanley holds an Overweight rating, highlighting structural growth in AI-driven networking demand and strong free-cash-flow conversion as a buffer against rate volatility

- Morningstar characterises the stock as undervalued relative to its AI-driven growth prospects

The software segment provides diversification against hardware cyclicality. The primary risk is customer concentration: a small number of hyperscale cloud customers account for a significant share of revenue, and any shift in their spending priorities would be felt directly.

Micron and Ciena: valuation disconnects where fundamentals lag the hype

Micron and Ciena both participated in the AI rally. Neither carries an economic moat.

Morningstar rates Micron as having no moat and considers it overvalued. DRAM and NAND remain commoditised products where pricing discipline depends on industry-wide supply restraint rather than company-specific advantage. Micron’s fiscal Q2 2026 results beat revenue expectations on strong high-bandwidth memory (HBM) demand, and at least one brokerage raised near-term estimates. The same brokerage maintained a neutral rating, citing the memory sector’s cyclical history as a constraint on the structural thesis.

Short-term earnings strength and long-term structural risk can coexist. If supply capacity ramps faster than demand, DRAM pricing vulnerability remains the primary downside catalyst.

Ciena tells a different story. Morningstar rates it as having no moat and considers it overvalued. Fiscal Q1 2026 delivered soft orders from telecom carriers, a full-year guidance cut, and at least one analyst downgrade.

One analyst characterised the situation as the “AI narrative running ahead of reality” for Ciena, with the timing and magnitude of AI-driven optical orders remaining uncertain.

The underlying issue is that much of Ciena’s business remains tied to carrier capital expenditure cycles rather than hyperscale AI cluster buildouts. The stock had “ridden the AI networking trade” without the underlying order flow to sustain its multiple expansion.

- Micron’s key risk: DRAM pricing cycle; commodity dynamics limit sustainable pricing power

- Ciena’s key risk: carrier capex dependency; AI optical demand has not yet arrived at sufficient scale

Both names illustrate a recurring pattern in technology cycles: companies that benefit from thematic tailwinds can attract valuations that assume the tailwind will become a structural advantage. When that assumption is tested, the correction can be severe.

Rate environment and geopolitical risk: the macro tests sentiment-driven valuations first

Why the 10-year yield matters more for narrative names than for moat names

The 10-year Treasury yield closed at approximately 4.61% on 18 May 2026 and traded near 4.67% intraday on 19 May 2026, according to FRED data. This rate environment is a material constraint on high-multiple growth valuations.

The mechanism is straightforward: higher discount rates reduce the present value of cash flows weighted toward future years, disproportionately compressing valuations for long-duration, high-multiple stocks. Goldman Sachs research distinguishes between high-multiple software and unprofitable tech (most adversely affected) and AI infrastructure names with strong, visible cash generation (relatively more resilient).

Morningstar’s market strategists have noted that AI stocks accounted for a disproportionately large share of US equity gains from late March through mid-May, signalling narrow market leadership at a time when rates remain elevated. That concentration raises vulnerability if macro expectations shift.

Export controls as a structural constraint, not a one-off event

US export controls on advanced AI chips to China, originally established under rules developed in 2023-2024, remain in place and have been tightened. The practical effect has forced companies such as Nvidia to design lower-performance chip variants for the Chinese market, creating a structural revenue and market-access constraint.

The structural durability of export controls matters here because the controls are grounded in national-security law with bipartisan Congressional backing, placing them outside the jurisdiction of trade negotiators and making periodic diplomatic summits an unreliable signal for investors pricing China revenue recovery into semiconductor valuations.

The BIS export control rules on advanced computing, updated across October 2023, April 2024, and December 2024, specifically target China’s capacity to develop AI and semiconductor manufacturing capabilities, establishing the regulatory framework that forces companies such as Nvidia to engineer lower-performance chip variants for that market.

- Rate environment: elevated yields compress long-duration, high-multiple valuations first

- Export controls and China exposure: ongoing restrictions limit revenue and market access for AI hardware names with significant China sales

- US-China trade tensions: the Trump administration’s May 2026 tariffs on Chinese imports (covering EVs, batteries, and technology-related products) reinforce the geopolitical risk environment and elevate the probability of further semiconductor restrictions

Goldman Sachs has noted that some institutional investors are tilting toward AI-exposed semiconductor names with lower China revenue concentration. Names without a moat and without pricing power have the least buffer when these macro stress tests arrive.

Staying in AI without overpaying: a practical allocation lens for mid-2026

The institutional frameworks converge on five questions investors can apply to any AI-exposed stock:

- Does the company have a wide or narrow economic moat?

- What is its position in the AI stack (core infrastructure vs. peripheral supplier)?

- How much of its revenue is proven and recurring vs. aspirational?

- How exposed is it to memory or hardware commodity cycles?

- What is its China revenue concentration under the current export control regime?

A “yes” on the first three and a “low” on the last two describes a name worth holding through macro volatility. The inverse describes a name where the margin of safety depends almost entirely on sentiment persistence.

David Sekera of Morningstar recommends splitting evenly between value and growth, enabling ongoing reallocation as relative valuations shift. The growth category sits at a 5% discount to fair value, down from 20% on 30 March. The value category sits at a 7% discount, marginally wider than the 5% discount recorded on 30 March.

The entry-point advantage in growth has been largely spent. The barbell approach provides a structural hedge: maintain AI exposure through moat-backed names while rebalancing toward value where the discount has widened.

For investors wanting to translate the moat and stack-position criteria into a structured portfolio, our dedicated guide to AI infrastructure stock allocation walks through a three-layer hardware, cloud, and software framework with specific position-sizing ranges, Goldman Sachs capex projections by layer, and valuation benchmarks for each category as of mid-2026.

The AI trade is not over, but the easy money was in the margin of safety

The long-term thesis for AI infrastructure investment remains intact. What has changed is the price of admission. The 25% discount that technology carried in late March compressed to 7% in seven weeks, and the margin of error for new capital deployed into the sector has narrowed accordingly.

Nvidia and Broadcom remain wide-moat, structurally positioned names where institutional frameworks consistently identify durable advantages. Micron and Ciena carry no moat, face identifiable fundamental vulnerabilities, and trade at valuations that reflect narrative enthusiasm more than sustainable earnings power.

Investors who apply the moat and stack-position framework consistently will be better positioned to hold through rate volatility and geopolitical disruption without being caught in drawdowns among commodity-oriented AI names where the narrative, not the business, was doing the heavy lifting.

Passive index exposure to AI is larger than most investors realise: the Magnificent Seven now represent approximately 34-35% of the S&P 500, matching dot-com era concentration levels, which means a broadly diversified equity allocation still carries substantial single-theme sensitivity to the same macro and valuation pressures discussed here.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—