Why Zscaler Stock Fell 30% on a Quarter It Actually Beat

1 hr ago

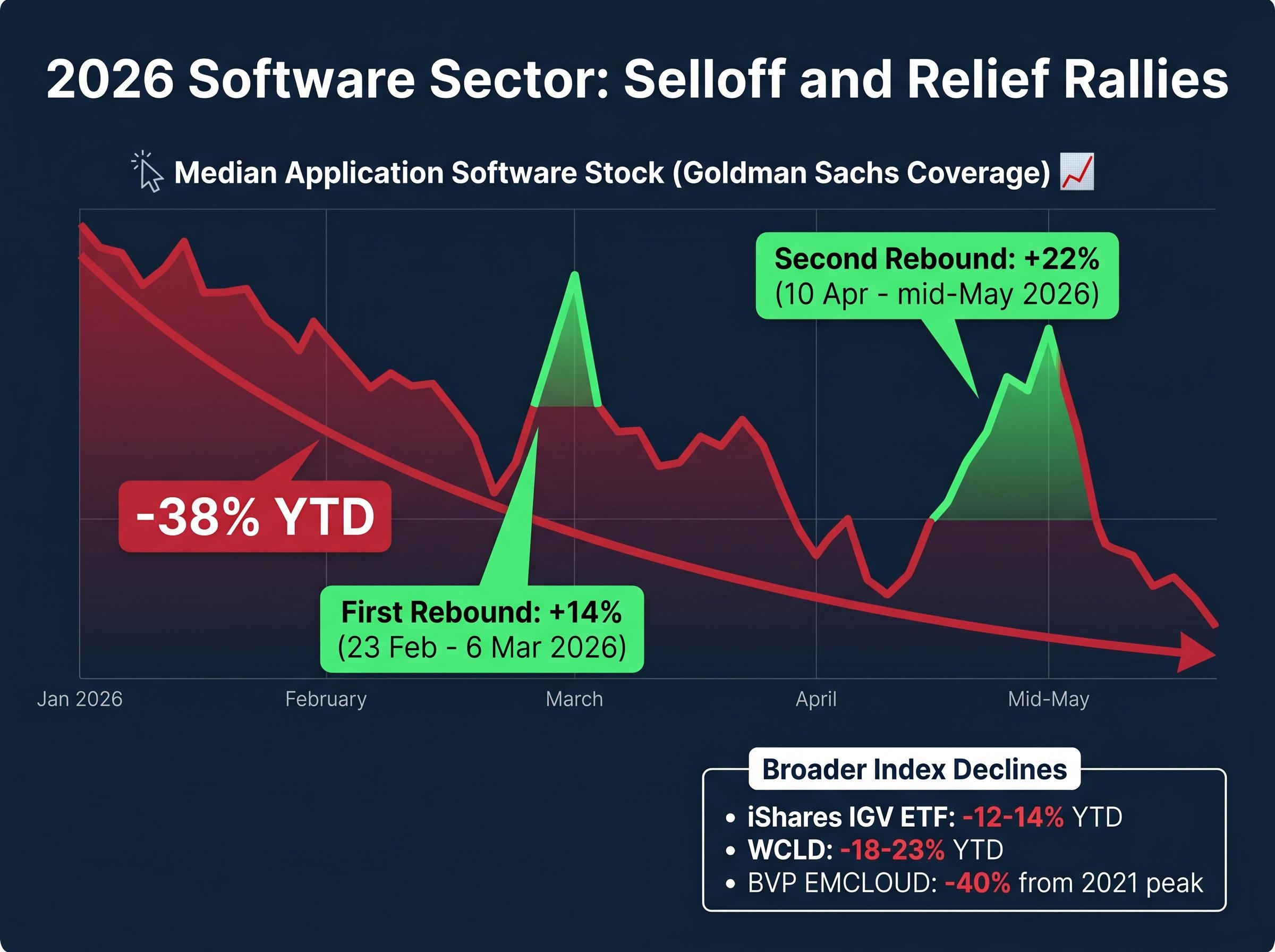

Goldman Sachs analyst Gabriela Borges delivered a stark assessment on 19 May 2026: the median application software stock in Goldman’s coverage universe has fallen roughly 38% year-to-date, bounced twice, and is likely to stay stuck. Two distinct rebounds, a 14% surge between 23 February and 6 March and a 22% rally from 10 April through mid-May, gave investors hope that the software selloff had found its floor. Both faded. With the iShares IGV ETF down approximately 12-14% year-to-date, the WCLD down roughly 18-23%, and the BVP EMCLOUD index still approximately 40% below its 2021 peak, the sector’s inability to sustain a recovery is now the central question for U.S. technology investors. What follows is a breakdown of Goldman’s diagnosis: why the software sector remains range-bound, what needs to change for a durable recovery, and which individual names Goldman views as exceptions worth watching.

The decline started early and accelerated through January. By mid-February, the median application software stock in Goldman’s coverage had lost more than a third of its value. Then came the first bounce.

The pattern is now unmistakable. Sell, bounce, sell again. Neither rally generated sufficient follow-through buying to shift the sector’s trajectory.

The February 2026 SaaS value destruction event, in which the US enterprise software sector shed over $1 trillion in market capitalisation as autonomous AI agents began dismantling per-seat licensing economics, set the conditions that Goldman’s range-bound diagnosis is now describing in mid-year terms.

Borges characterised the sector as “challenged,” with AI-driven outperformance framed as “more of a 2027 event” than a 2026 catalyst.

That framing matters. Goldman is not calling a bottom. The bank is diagnosing a sector caught between valuations that have normalised and fundamentals that have not improved enough to justify re-rating. The 38% drawdown is severe, but severity alone does not create a floor.

A sector is range-bound when neither sufficiently strong catalysts nor sufficiently poor fundamentals exist to break valuations decisively higher or lower. Software in 2026 sits precisely in that condition. Multiples have compressed from 2021 bubble extremes, but the stocks are not cheap enough to attract distressed capital. Growth is decelerating, but it is not collapsing.

The result is a holding pattern. Investors who bought the dip twice this year found that normalised valuations without improving fundamentals produce rallies that stall, not recoveries that compound.

Goldman’s range-bound view is not isolated. Across four major firms, the shared conclusion points in the same direction: wait for a catalyst, not buy the dip.

| Firm | Date | Key Valuation Observation | Sector Stance |

|---|---|---|---|

| Morgan Stanley | 6 March 2026 | Software stocks trading near historical averages on EV/revenue and EV/FCF | Selectively constructive |

| J.P. Morgan | 31 January 2026 | Quality growth names at 10-12x NTM revenue, down from 15-20x at 2021 peak | Range-bound absent IT spending re-acceleration |

| Bank of America | 22 January 2026 | Valuations compressed back toward 2018-2019 levels | Muted multiple expansion expected |

| Evercore ISI | 14 February 2026 | SaaS valuations “fair but not cheap” | Market-weight; overweight AI-levered platforms only |

The table tells the story. Four firms, four variations of the same conclusion: the sector is fairly valued on historical metrics, but fair is not a catalyst.

Within an otherwise cautious sector call, Borges identified Microsoft and ServiceNow as “idiosyncratic opportunities,” meaning their investment cases rest on company-specific catalysts rather than a broad sector re-rating. Goldman also noted incremental progress among other incumbents, including leadership transitions at Klaviyo, Workday, and Adobe, and early product refinements at ServiceNow and Salesforce, though these were characterised as signals of advancement rather than buy triggers.

Goldman’s implied criteria for an idiosyncratic opportunity in software follow a specific logic:

Record dispersion within the sector, where the spread between the top and bottom deciles of US technology stocks reached 133 percentage points, explains why Goldman’s selectivity framing around Microsoft and ServiceNow is not merely a preference but a structural requirement: buying the sector index captures both the platform consolidators and the names being cannibalised by them.

ServiceNow reported a roughly $600 million-plus AI ARR pipeline exiting Q1 2026, with CEO Bill McDermott framing AI as “stacked on top of existing platform subscriptions.” Microsoft confirmed on its Q3 FY26 call that AI services had added “several points” to Azure growth. Both companies present cases where AI spending appears to expand their revenue base rather than simply redirect it.

Goldman warned explicitly that attractive valuation alone is not sufficient justification without improving fundamentals, noting that a newer cohort of value-oriented software investors still requires positive fundamental evidence before turning constructive.

The distinction is clear. Goldman is not recommending software broadly; the bank is identifying names where the evidence already supports a differentiated thesis.

Investors entered 2026 expecting AI to lift software broadly. Goldman’s Borges framed the reality differently: AI-driven outperformance across the sector is a 2027 event, not a 2026 one. The distinction between additive AI revenue (which expands a company’s total growth) and substitutive AI revenue (which merely redirects existing budget) is what determines investor reception, and in 2026, the evidence favours the latter for most names.

Multiple companies have indicated that 12-18 months beyond current AI product launches is a more realistic timeline for material revenue contribution. AI capabilities remain embedded in existing SKUs at most vendors rather than breaking out as discrete growth drivers.

According to Evercore ISI analysis from 22 April 2026: “For the mid-tier of application software, AI spend looks more redistributive than additive in 2026.”

The dynamic is structurally asymmetric. Microsoft, ServiceNow, and Salesforce have each confirmed, in varying degrees of directness, that AI capabilities are helping them absorb functionality that smaller vendors previously owned. A Morgan Stanley CIO survey published 1 May 2026 found roughly half of CIOs planned to fund AI software spend by “reallocating from other software categories” rather than expanding budgets. IDC described 2026 as “a transition year where AI spending is more about prioritisation than expansion.”

For large platform vendors, this consolidation trend is positive. For mid-tier and niche application software names, it represents genuine cannibalism of existing wallet share, even as the sector narrative frames AI as uniformly bullish.

The hardware versus software divergence, a spread of more than 70 percentage points between the Morningstar Global Semiconductor Equipment index and the Software Applications index year-to-date, reflects the same budget reallocation dynamic Goldman identifies: enterprise AI capital is flowing into infrastructure spend first, and the software revenue inflection that follows remains deferred.

Goldman identified two primary conditions for a sustained software recovery, and they are sequenced, not simultaneous. The second cannot arrive without the first.

Goldman’s framing positions AI-driven outperformance as a 2027 event rather than a 2026 catalyst, a timeline that reflects structural sequencing rather than pessimism.

The logic is straightforward. Budget expansion must precede revenue inflection, and revenue inflection must become visible in earnings before multiples re-rate. In 2026, the first condition remains unfulfilled. The second is still forming. The third is, at best, emerging at a handful of individual names.

Goldman’s verdict is clear: the software sector is challenged, both 2026 bounces were relief rallies rather than the beginning of sustained recoveries, and the conditions for a durable re-rating remain absent in the near term. The 38% year-to-date decline in Goldman’s median application software coverage has created pockets of value, but value without a catalyst is a range, not a recovery.

For investors with a medium-term horizon, the second half of 2026 offers several specific data points worth monitoring:

The software sector’s path out of its current range depends on these signals arriving in sequence. Until they do, Goldman’s diagnosis holds: challenged, range-bound, and selectively opportunistic at best.

Investors wanting a concrete company-level case study of how the additive versus substitutive AI revenue distinction plays out in practice will find our full explainer on Xero’s AI monetisation strategy, which examines the three-pronged pricing model (bundled, standalone add-on, and usage-based), the adoption gap between feature availability and paying subscribers, and the structural moat arguments management is making to justify a late FY27 revenue ramp.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding AI monetisation timelines and sector recovery conditions are subject to change based on market developments and company performance.

Goldman Sachs characterised the software sector as challenged and range-bound in 2026, noting the median application software stock in its coverage universe had fallen roughly 38% year-to-date, with two failed relief rallies and no durable recovery catalyst yet in place.

Both the 14% rebound in February-March and the 22% rally in April-May 2026 faded because normalised valuations alone are not sufficient without improving fundamentals; enterprise IT budgets have not re-accelerated and AI revenue remains largely substitutive rather than additive for most vendors.

Goldman identified two sequenced conditions: first, enterprise IT budget stabilisation and re-acceleration above mid-single-digit growth; and second, visible AI-driven revenue expansion at the sector level that represents net-new budget growth rather than internal reallocation.

Goldman Sachs identified Microsoft and ServiceNow as idiosyncratic opportunities, noting that Microsoft confirmed AI services added several points to Azure growth and ServiceNow cited a roughly $600 million-plus AI ARR pipeline, with both companies showing AI revenue that appears additive to total growth.

Additive AI revenue expands a company's total addressable growth by attracting net-new enterprise budget, while substitutive AI revenue simply redirects spending that already existed within software categories; Goldman's analysis suggests most of 2026 AI spending falls into the substitutive bucket for mid-tier vendors.