Goodman Group’s 18% Pullback: Decoding the Metrics That Matter

7 mins ago

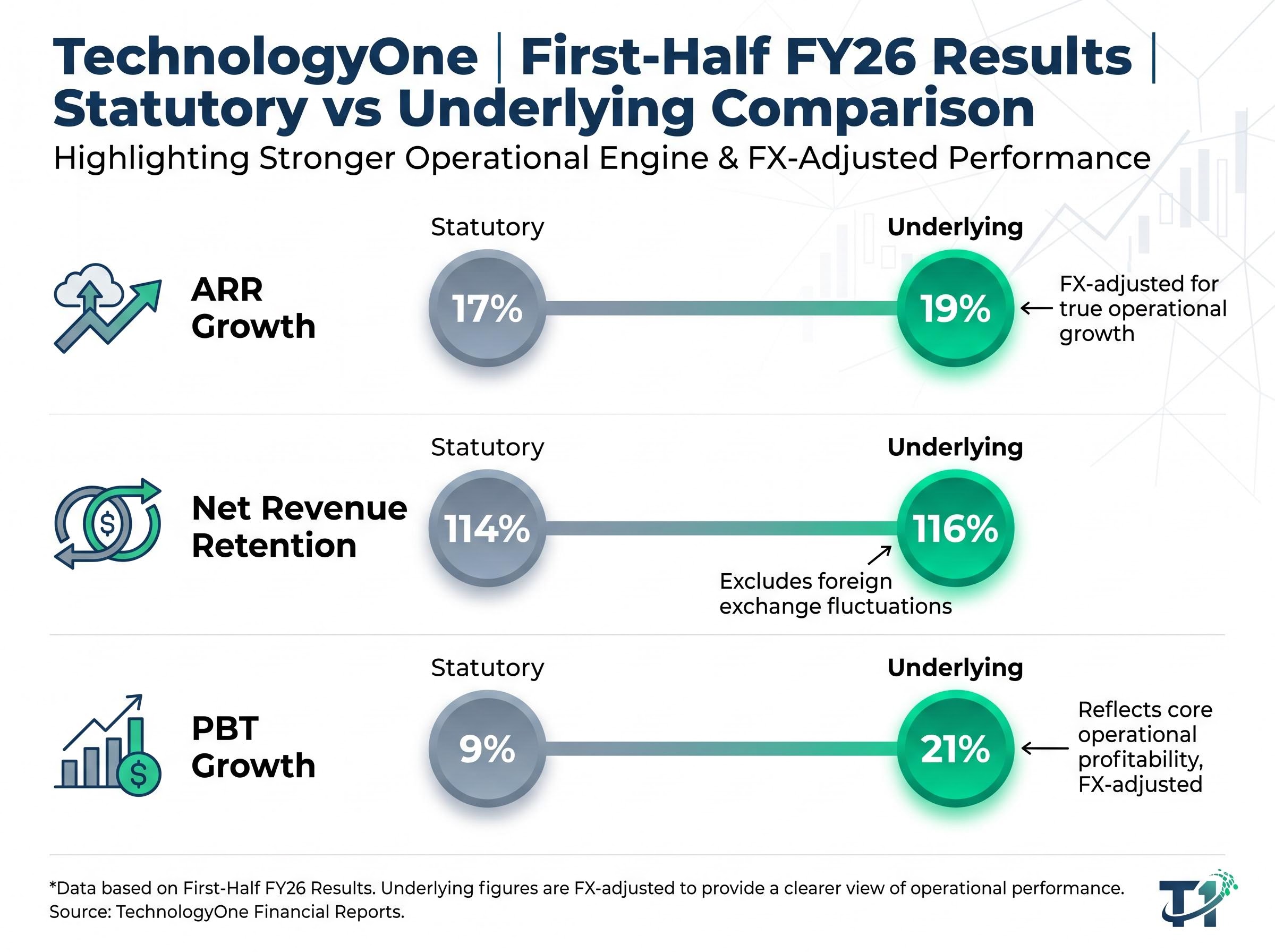

TechnologyOne delivered its first-half FY26 result on 19 May 2026, and the headline numbers tell a story that undersells the operating reality. Pre-tax profit rose 9%, free cashflow fell 15%, and revenue growth of 11% hardly screams momentum for a stock trading above 65x earnings. Yet strip out the currency drag from a strengthening Australian dollar and a one-off showcase investment, and the underlying business grew pre-tax profit by 21%, pushed annual recurring revenue (ARR) growth to 19%, and lifted the interim dividend by 21%. The gap between the statutory surface and the underlying engine is the single most important detail in this result. What follows breaks down what the headline numbers conceal, examines the UK growth story, assesses what a competitive win in Townsville signals about the company’s moat, and evaluates whether the upgraded 18-20% full-year profit guidance is credible for Australian investors weighing the TechnologyOne share price at approximately $28.27.

For the six months to 31 March 2026, TechnologyOne reported total revenue up 11% to $322.7 million, pre-tax profit (PBT) up 9% to $89.1 million, and net profit after tax (NPAT) up 6% to $66.8 million. Free cashflow came in at $20.3 million, down 15% on the prior corresponding period.

On face value, the free cashflow decline and single-digit profit growth look underwhelming for a company priced for high-teens earnings expansion. ARR reached $598 million, up 17%, a stronger signal, but even that number carries a currency distortion.

Two factors suppressed the statutory result. The Australian dollar strengthened materially against the British pound during the half, compressing the reported AUD value of UK-sourced revenues. Separately, a one-off showcase investment added costs that will not recur at the same level.

Adjust for both, and the underlying picture sharpens considerably.

| Metric | Statutory | Underlying (FX-adjusted) |

|---|---|---|

| ARR growth | 17% | 19% |

| Net revenue retention (NRR) | 114% | 116% |

| PBT growth | 9% | 21% |

| Interim dividend per share | $0.08 (up 21%) | |

The 21% dividend increase is itself a signal. Management teams do not lift dividends at that rate unless they view the underlying earnings trajectory as durable.

For investors more accustomed to reading NPAT as the bottom line, TechnologyOne’s result requires a different lens. The company operates a software-as-a-service (SaaS) model, which means the metrics that matter most are not the ones that matter most for, say, a retailer or a bank.

Three terms frame the entire investment case:

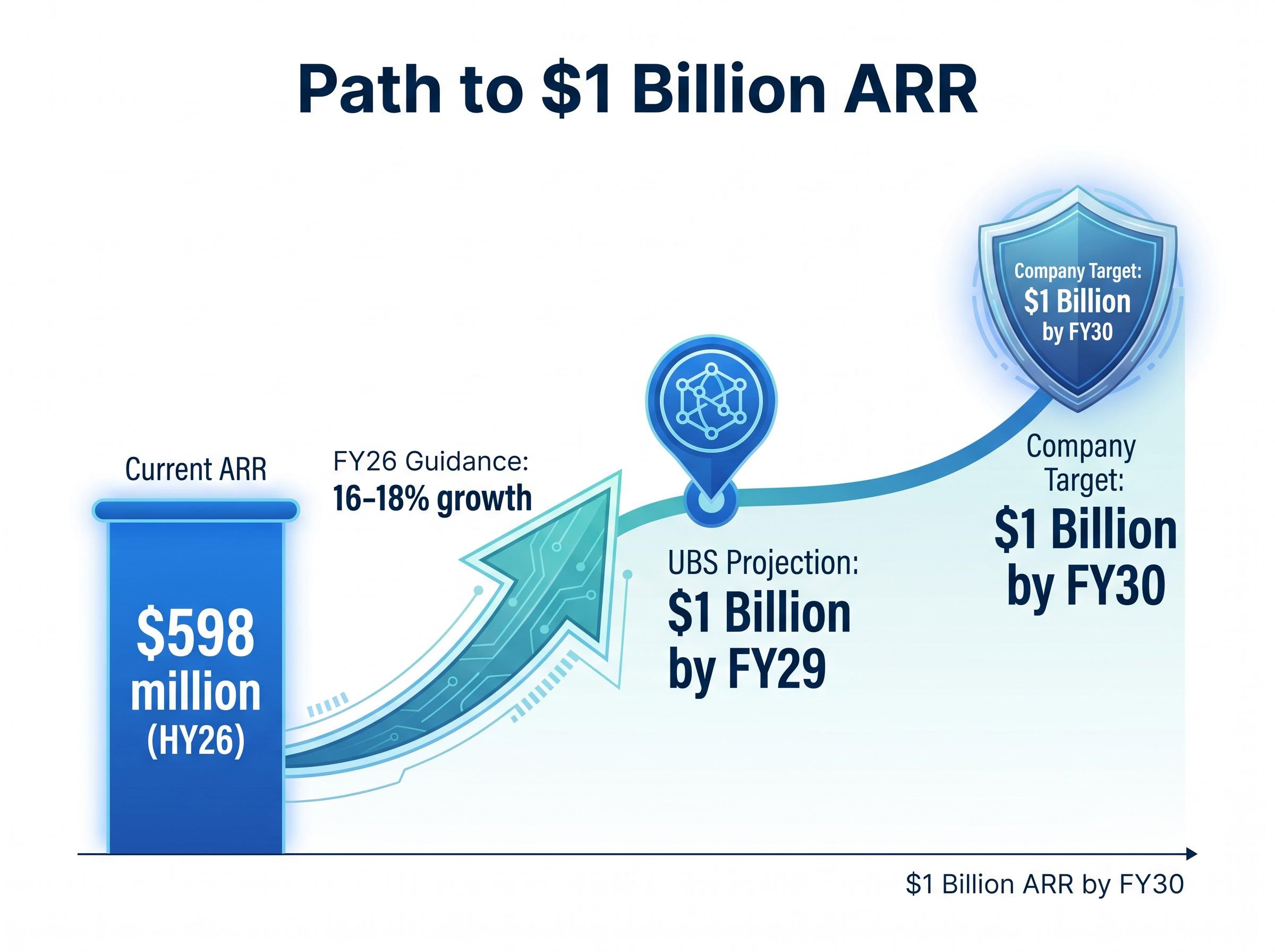

At $598 million in ARR (up 17%, or 19% underlying), with NRR of 114% (underlying 116%), TechnologyOne’s existing customer base is expanding faster than it is contracting. That compounding dynamic is why the company’s target of at least $1 billion in ARR by FY30 is structurally credible rather than aspirational.

UBS projects TechnologyOne will reach $1 billion in ARR by FY29, one year ahead of the company’s own target.

For Australian investors evaluating the stock at any reporting period, ARR growth and NRR carry more interpretive weight than a single half’s NPAT figure.

UK ARR reached $53 million in the half, up 23%, a rate that materially outpaces the company-wide 17% statutory growth (and even the 19% underlying figure).

The problem is that Australian investors reading the statutory result in AUD do not see that outperformance clearly. The currency translation mechanism works in three steps:

The UK business targets public-sector organisations, particularly local government. Anticipated council consolidation across England, creating larger and more economically viable councils, represents a structural demand catalyst for enterprise resource planning (ERP) systems of the kind TechnologyOne provides.

The UK local government reorganisation policy published by the Ministry of Housing, Communities and Local Government outlines a program to replace two-tier county and district councils with single-tier unitary authorities, a structural shift that materially expands the pool of organisations requiring new or upgraded enterprise resource planning systems.

The UK segment remains small relative to the ANZ core. But its growth rate and its structural tailwinds suggest investors anchoring solely to the current revenue split may be underweighting its long-run contribution.

The City of Townsville left TechnologyOne for a rival ERP provider. The rival could not meet the council’s requirements. Townsville returned.

The council signed a 10-year agreement at a higher contract value than its prior deal, a rare example of a customer defecting and then returning on improved terms.

That sequence matters more than any single contract’s dollar value. In enterprise software, switching costs are the primary mechanism through which providers retain customers. Government and education organisations build years of workflows, data structures, and staff training around a single ERP platform. Leaving is expensive. Returning after leaving is an even stronger signal: it suggests the alternative was not merely different but materially worse.

Switching costs as a moat source operate differently from brand or scale advantages: they are embedded in the customer’s own workflows, data structures, and staff training rather than in the vendor’s product alone, which is why a government council returning to a prior ERP provider after a failed defection is a stronger competitive signal than a new customer win at an equivalent contract value.

A second data point reinforces the competitive picture. TechnologyOne secured a new contract with James Cook University, which includes the company’s Plus agentic AI platform. The Plus platform, which had 22 subscriptions as of approximately February 2026, is designed to drive both new customer acquisition and higher spend from existing clients.

Combined with NRR of 114% (underlying 116%), these wins reduce the probability of the competitive displacement scenario that would most threaten the investment case.

TechnologyOne upgraded its FY26 PBT growth guidance to 18-20%, up from a prior range of 13-17%. ARR growth guidance sits at 16-18% for the full year, with a long-term pre-tax profit margin target of at least 35%.

With ARR at $598 million at the half and growth typically weighted toward H2, the 16-18% full-year ARR target appears achievable on the current trajectory. The PBT upgrade, from a range that topped out at 17% to one that starts at 18%, reflects management’s confidence that the underlying momentum, not the statutory headline, is the truer signal.

The guidance upgrade from February 2026, which lifted the PBT growth floor from 13% to 18%, established a baseline of management confidence before the HY26 result was even reported; the May 2026 reaffirmation at the top end of that range is therefore not a standalone data point but a continuation of a trajectory management signalled months earlier.

Brokers are split on what the stock is worth from here.

| Broker | Rating | Price target | Key assumption | Implied upside from $28.36 |

|---|---|---|---|---|

| Bell Potter | Buy | $32.25 | ARR growth could outperform expectations | ~14% |

| Morgans | Hold | $31.20 | Valuation above 65x PE limits upside | ~10% |

| UBS | N/A | N/A | 18.4% profit growth; $1B ARR by FY29 | N/A |

The bull case requires three conditions to hold:

Morgans’ Mitch Belichovski has flagged the valuation risk directly, noting the stock was trading on a price-earnings ratio above 65x. The 24 April 2026 downgrade to Hold was not driven by deteriorating fundamentals but by the price itself.

What HY26 confirmed:

What remains to watch:

The H2 FY26 result and any formal broker target revisions following the 19 May 2026 release represent the next meaningful data points. The Morgans downgrade was price-driven, not fundamentals-driven, and the stock is re-rating on growth expectations that demand sustained execution through FY27.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The statutory numbers understate the operating reality. Underlying pre-tax profit grew 21%, ARR is compounding at 19%, the UK is outpacing the core business at 23% growth, and a customer defection reversal in Townsville reinforces the competitive position in ways that NRR alone cannot capture.

The $1 billion ARR target by FY30 has credible support, with UBS projecting achievement a year early. But the stock’s valuation, above 65x earnings per Morgans’ assessment, prices in a growth trajectory that leaves little room for disappointment.

The variable most likely to determine whether TechnologyOne re-rates higher or consolidates at current levels is Plus. With 22 subscriptions and James Cook University as a named enterprise adopter, the agentic AI platform is the bridge between a strong SaaS compounder and the next phase of the growth story. Whether that bridge holds weight is a question H2 FY26 will begin to answer.

Enterprise AI adoption rates tell a sobering story for vendors counting on rapid platform uptake: with an estimated 70-80% of enterprise AI pilots failing or stalling as of early 2026, and only 17% of enterprises having meaningfully deployed agentic AI, the 22-subscription starting point for TechnologyOne’s Plus platform sits within the realistic early-adopter range rather than signalling slow commercial traction.

Forward-looking statements regarding guidance, ARR targets, and growth projections are subject to change based on market developments and company performance. Past performance does not guarantee future results.

Annual recurring revenue (ARR) is the total annualised value of all active subscription contracts, measuring the size and growth rate of predictable, repeating income. For TechnologyOne, ARR is a more meaningful performance indicator than a single half's profit figure because the company operates a SaaS model where compounding subscription revenue drives long-term value.

TechnologyOne reported statutory revenue up 11% to $322.7 million, pre-tax profit up 9% to $89.1 million, and ARR of $598 million, up 17%. After adjusting for currency headwinds and a one-off showcase investment, underlying pre-tax profit grew 21% and underlying ARR growth reached 19%.

Free cashflow fell 15% to $20.3 million in the six months to 31 March 2026, partly due to a one-off showcase investment that added costs not expected to recur at the same level, along with the impact of a strengthening Australian dollar on UK-sourced revenues.

TechnologyOne targets at least $1 billion in ARR by FY30, and UBS projects the company will reach that milestone by FY29, one year ahead of schedule. With ARR at $598 million and growing at 19% on an underlying basis, the trajectory is considered structurally credible rather than aspirational.

Townsville left TechnologyOne for a rival ERP provider, but returned after the rival could not meet its requirements, signing a 10-year agreement at a higher contract value than its prior deal. In enterprise software, a customer defecting and then returning on improved terms is a stronger signal of competitive moat than a new customer win at an equivalent value.