Goodman Group’s 18% Pullback: Decoding the Metrics That Matter

14 mins ago

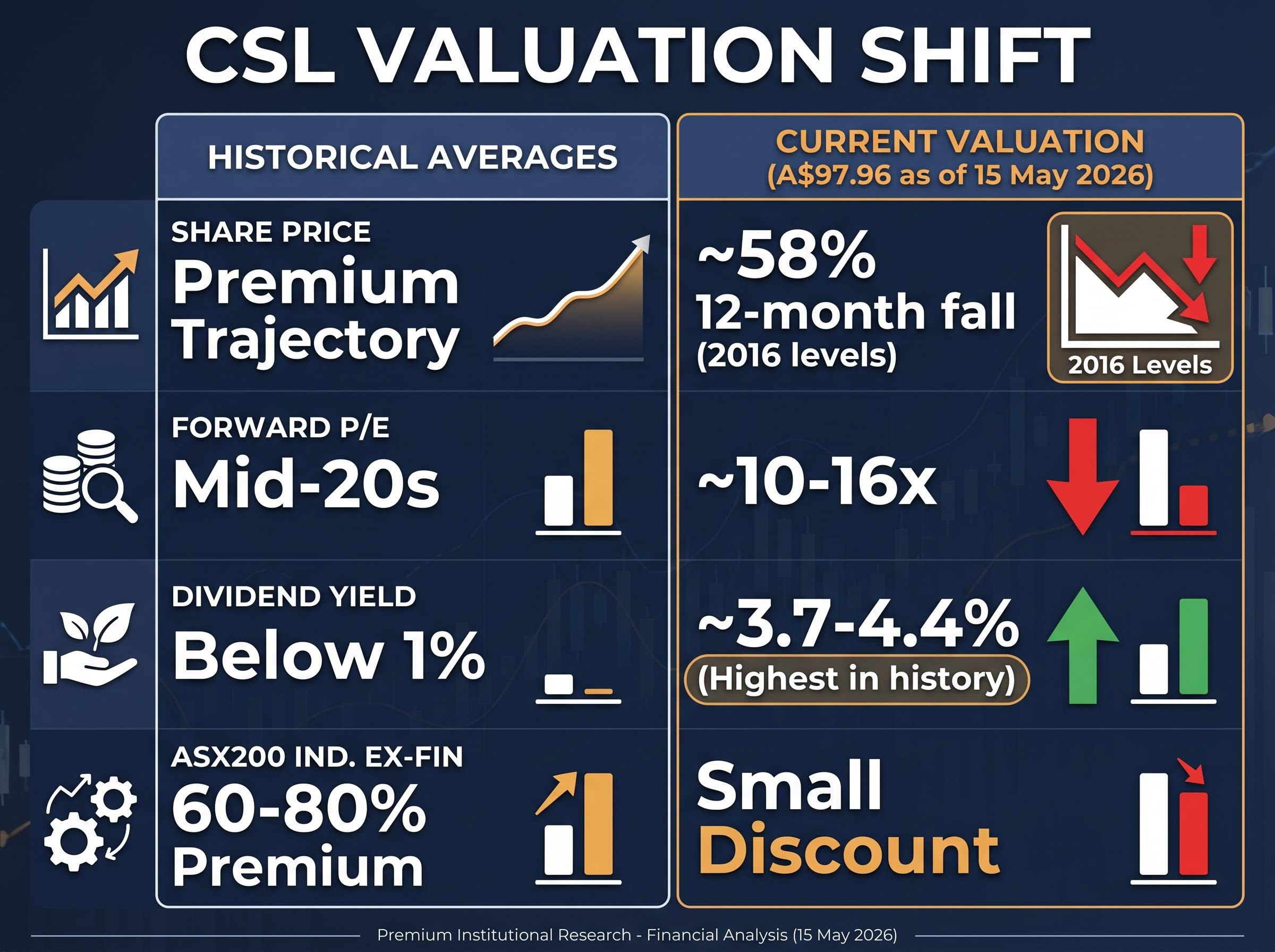

CSL Limited shares have fallen approximately 58% over the prior 12 months, returning the stock to levels last seen in 2016 and pushing its dividend yield to the highest point in the company’s history. For Australian investors, that combination forces an unavoidable question: is this a once-in-a-decade reset or the opening chapter of a structural decline?

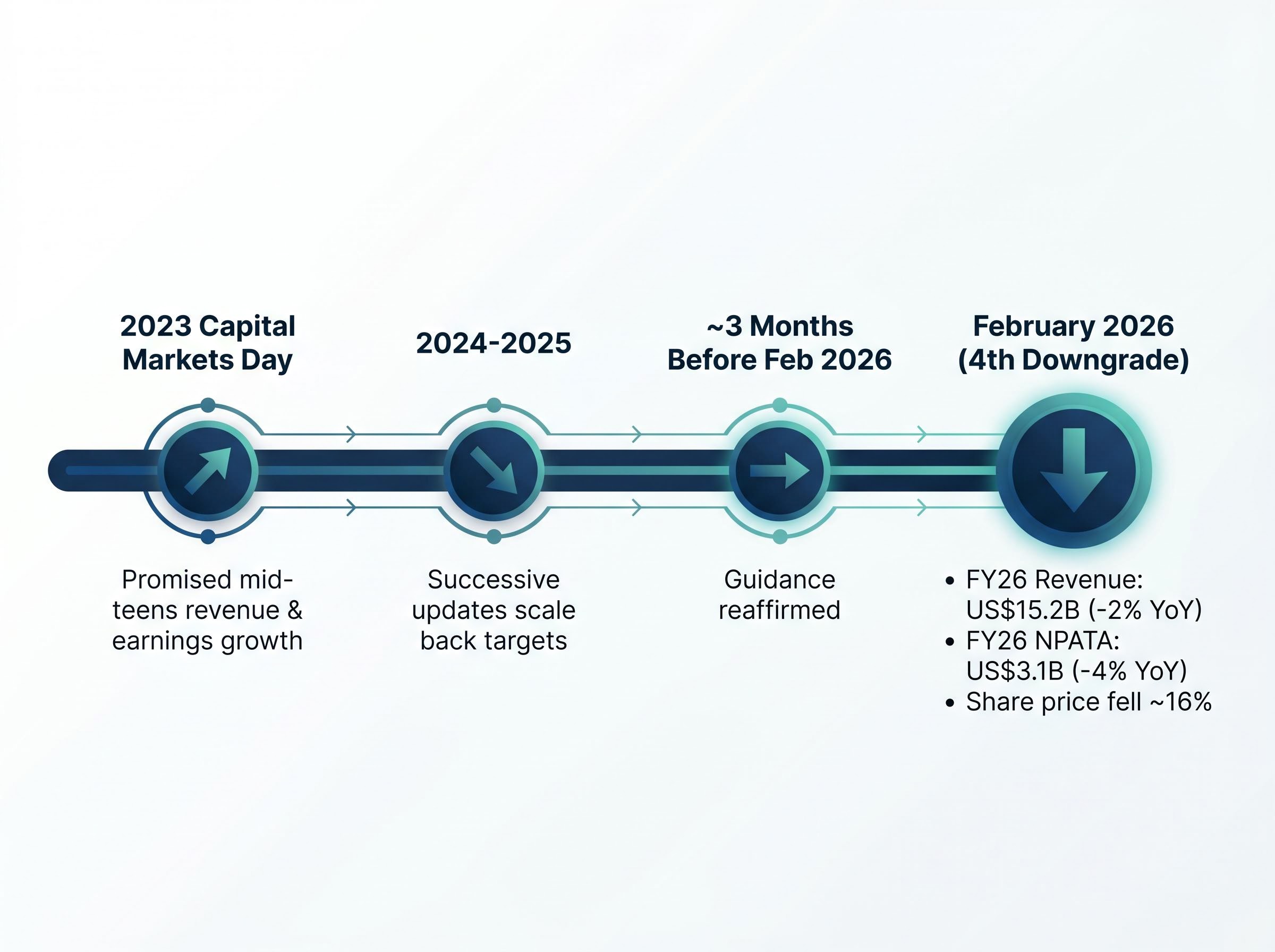

The February 2026 guidance revision was the fourth successive downgrade to CSL’s FY26 outlook since its 2023 Capital Markets Day, where management had promised mid-teens revenue and earnings growth. With a permanent CEO yet to be named and a major acquisition now carrying an impairment, the investment case has shifted from what the market spent a decade pricing in.

What follows is a structured walk through the scale of the earnings deterioration, the three drivers behind it, what the management void means for capital allocation credibility, and how the current valuation compares to CSL’s own history and global plasma peers. The aim is to give investors a framework for assessing whether the current price represents an entry point or a warning.

The deterioration did not arrive in a single event. It accumulated across a sequence that, read in order, explains why institutional trust in CSL’s forward numbers has broken down:

CSL’s May 2026 guidance downgrade erased A$9.48 billion in market capitalisation in a single session, with the stock closing at A$100.75 and the ASX healthcare sector index falling 6.47% on the same day, underscoring how heavily the broader index is weighted toward a single company’s execution.

“Kitchen sink” designation: Post-February 2026 broker consensus characterised the downgrade as “kitchen sink in nature,” meaning management recognised the bulk of near-term headwinds at once. The label matters because, if accurate, it implies the worst is now in the numbers rather than ahead.

The gap between the original mid-teens growth commitment and a year-on-year decline in both revenue and profit is not a rounding error. It is the distance between the business investors were pricing and the one they now own.

Not all of CSL’s problems carry the same weight or the same timeline. Separating them is what determines whether the investment case is recoverable or permanently impaired.

Plasma margin pressure is a unit economics problem, not a volume problem. Donor fees, labour costs, and centre overheads rose faster than the lagged price adjustments for plasma-derived therapies. Collection volumes themselves remained solid, above pre-COVID levels at the FY25 result. The miss came from what it cost to collect each litre, not how many litres were collected. The margin recovery timeline was pushed back and reset at the February 2026 update.

Currency translation is a reporting-layer headwind. Morgan Stanley cited FX translation as a contributor to the FY26 downgrade, with a stronger USD compressing reported earnings relative to constant-currency guidance. This is arithmetic, not operations, but it makes the headline numbers look worse than the underlying business.

| Fault line | Cyclical or structural | Estimated recovery timeline | Primary analyst view |

|---|---|---|---|

| Plasma margin pressure | Cyclical (cost timing) | 2-3 years (tied to Rika rollout) | Recoverable, but slower than guided |

| Vifor/dialysis impairment | Structural (one-time reset) | Complete (write-off taken FY25) | Contained misstep; lowers long-term Vifor contribution |

| Currency translation | Cyclical (FX arithmetic) | Variable (exchange rate dependent) | Reporting noise, not operational |

CSL’s FY25 result (August 2025) disclosed a large impairment of dialysis-related assets within the Vifor business. Structurally weaker dialysis market dynamics, slower therapy uptake, and pricing pressures drove the write-down. Brokers including UBS and Citi characterised it as a one-off reset rather than an ongoing earnings drag, with AFR commentary describing it as a “rare but costly misstep” for an otherwise disciplined capital allocator.

The question for investors is whether the impairment signals an isolated misjudgement on nephrology market dynamics or something broader. Most brokers are treating it as contained, but tracking whether CSL pursues further large acquisitions before organic margins stabilise will be a useful discipline.

Before the margin problem, there is the franchise itself. CSL holds an oligopolistic position in plasma-derived therapies, a market with high barriers to entry, long collection supply chains, and limited global competitors. That structural foundation is what makes the “not broken” argument defensible, even as the near-term economics remain under pressure.

Morningstar’s wide economic moat designation, reaffirmed in May 2026 despite the share price collapse, rests on the oligopolistic structure of the plasma-derived therapy market: high collection infrastructure barriers, a limited global competitor set, and the multi-year lead time required to replicate CSL’s donor network at scale.

The volume-versus-cost distinction: CSL’s plasma collection volumes were above pre-COVID levels as of the FY25 results. The business is not losing market share or facing demand erosion. The problem is that each unit collected costs more than management anticipated, and the price adjustments for finished therapies have lagged behind input cost inflation.

The primary lever for margin restoration is the Rika plasma collection device, now rolling out across CSL’s centre network:

Approximately 98% of CSL’s revenue is generated outside Australia, meaning the business is largely insulated from domestic economic conditions but fully exposed to global plasma cost dynamics. For an investor trying to time re-entry, the Rika rollout is the most tangible operational signal to watch, even if it moves slowly.

Management’s historical optimism on the margin recovery timeline is precisely what makes the Rika-driven recovery case harder to accept at face value. The device may well deliver, but the timeline has already been revised once.

Gordon Naylor was appointed interim CEO in late 2025 following the departure of the previous chief executive. The board engaged an international executive search firm, with the November 2025 ASX announcement noting the process would “take several months.” No hard deadline or shortlist has been confirmed.

In post-February 2026 commentary, Naylor described the search as “well progressed” without disclosing a timeline. Reported internal contenders include the heads of CSL Behring and CSL Seqirus. Some investor commentary has pushed for an external hire with fresh perspective on capital allocation.

Institutional investors have stated explicitly that the CEO appointment is a key catalyst for sentiment repair. The vacancy matters not because the interim arrangement is operationally dysfunctional, but because the next permanent appointment is the mechanism through which the market will decide whether the “kitchen sink” reset is believable or whether more surprises remain.

The board itself set the strategic direction that led to the Vifor acquisition and the guidance sequence. The CEO hire will signal whether the board is seeking continuity or genuine reset.

An internal appointment signals operational continuity and confidence in the existing strategy. An external hire signals the board acknowledges a need for fresh perspective on capital allocation and guidance credibility. For investors, this choice is likely the single most consequential near-term binary for CSL’s re-rating trajectory.

Two forces have collided in CSL’s price. The first is a genuine maturation of the growth profile, which justified some derating. The second is a possible over-correction driven by repeated guidance failures and broken institutional trust. The investment question is which force dominates at A$97.

CSL closed at approximately A$97.96 on 15 May 2026. The forward P/E sits in the range of approximately 10-16x depending on estimate source, versus a 10-year historical average in the mid-20s. Morgan Stanley noted CSL now trades at a small discount to the ASX200 Industrials ex-Financials on a 12-month forward P/E, versus a 60-80% premium historically.

The dividend yield of approximately 3.7-4.4% is the highest in CSL’s history, a stock that historically yielded below 1%.

| Company | Forward P/E | Dividend yield | Consensus rating | Key thesis |

|---|---|---|---|---|

| CSL | ~10-16x | ~3.7-4.4% | Majority Buy/Overweight | Kitchen sink priced; mature compounder |

| Baxter | ~14-15x | N/A | Mixed | Restructuring; portfolio simplification |

| Grifols | ~9-10x | N/A | Mixed | Higher leverage; governance concerns |

CSL’s historic premium to both peers has collapsed. UBS argued the premium should persist, citing a stronger balance sheet and higher return on invested capital, but conceded it should now be modest. Morgan Stanley maintained an Overweight rating, framing CSL as a business where most bad news is reflected. UBS kept a Buy, stating the derating “prices in a permanent impairment to returns we believe is too harsh.”

Macquarie, which downgraded to Neutral from Outperform, captured the conditional nature of the bull case most precisely: CSL has entered a “show-me phase.”

Investors wanting a complete picture of the three simultaneous divisional pressures will find our full explainer on CSL’s divisional headwinds and tariff exposure, which details the US military flu vaccination reversal affecting Seqirus, the China albumin pricing dynamics in Behring, and the plasma therapy tariff exemption under the US Section 232 pharmaceutical proclamation effective September 2026 that removes one significant tail risk the market had been pricing.

The CSL that traded at a mid-20s P/E was a high-growth compounder delivering mid-teens earnings growth. The CSL at A$97 is a mature, high-single-digit growth healthcare business. AFR’s Chanticleer column described this transition in March 2026 as CSL “graduating from market darling to mature compounder.”

Some of the derating is rational; the growth profile no longer justifies the historic premium. Whether the market has over-corrected beyond that rational adjustment is the open question.

For Australian investors specifically, the franking credit dimension matters. With approximately 98% of revenue generated offshore, dividend franking credits are minimal to nonexistent. The 3.7-4.4% yield, while the highest in company history, delivers less after tax for Australian retirees and SMSF holders than a comparable fully franked yield from a domestic earner.

The balance sheet remains serviceable: total debt of approximately US$11.5 billion against a debt-to-EBITDA ratio of approximately 2x. One large-cap growth fund manager, quoted in Livewire Markets in March 2026, called CSL at current valuations “the most attractive risk-reward we’ve seen in a decade.”

The Seqirus demerger timeline, which brokers expect to be resolved by June 2026, represents one of four near-term checkpoints that could materially shift sentiment before the permanent CEO is named, alongside H2 FY26 Behring revenue recovery, US immunoglobulin channel normalisation, and management’s next guidance communication.

The multiple compression is real. The business is structurally intact. The earnings recovery is real but slow, and dependent on variables, Rika execution, CEO appointment, plasma cost normalisation, that are not yet confirmed.

The “kitchen sink” framing only proves accurate in retrospect. The prior guidance reaffirmations before subsequent cuts are the single most important data point for calibrating how much trust to extend to that claim now. The majority of analyst ratings sit at Buy or Overweight on reduced targets, with a minority at Neutral and very few explicit Sell calls.

Before making a position decision, an investor should be able to answer three questions:

Both outcomes remain plausible: a once-in-a-decade entry point and a value trap with further to fall. The honest conclusion is that the answer depends on which version of CSL’s recovery timeline an investor believes, and the evidence to confirm either view has not yet arrived.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The 'kitchen sink' label means brokers believe management recognised the bulk of near-term headwinds in a single downgrade, implying the worst is now reflected in the numbers rather than still ahead. If accurate, it suggests further earnings surprises are less likely, though prior reaffirmations before cuts have damaged confidence in that framing.

CSL's dividend yield has risen to approximately 3.7-4.4%, the highest in the company's history, because the share price has fallen roughly 58% over the prior 12 months while dividend payments have continued. Investors should note that with approximately 98% of revenue generated offshore, CSL dividends carry minimal to no franking credits.

Rika is a new plasma collection device being rolled out across CSL's centre network, designed to improve collection efficiency and reduce the per-unit cost of plasma. It is the primary operational lever management is relying on to restore plasma margins, though the rollout is gradual and the timeline has already been revised once.

CSL's forward P/E has fallen to approximately 10-16x depending on the estimate source, compared to a 10-year historical average in the mid-20s. Morgan Stanley noted CSL now trades at a small discount to the ASX200 Industrials ex-Financials on a 12-month forward basis, versus a 60-80% premium it historically commanded.

The four key catalysts are: the permanent CEO appointment and whether it signals continuity or strategic reset; the first reporting period showing plasma EBIT margin expansion; Rika rollout reaching a meaningful portion of the network with quantified efficiency data; and guidance language that is stable or conservative rather than requiring further revision.