Starbucks Builds AI Tools to Drop Microsoft, IBM and Oracle Apps

2 hrs ago

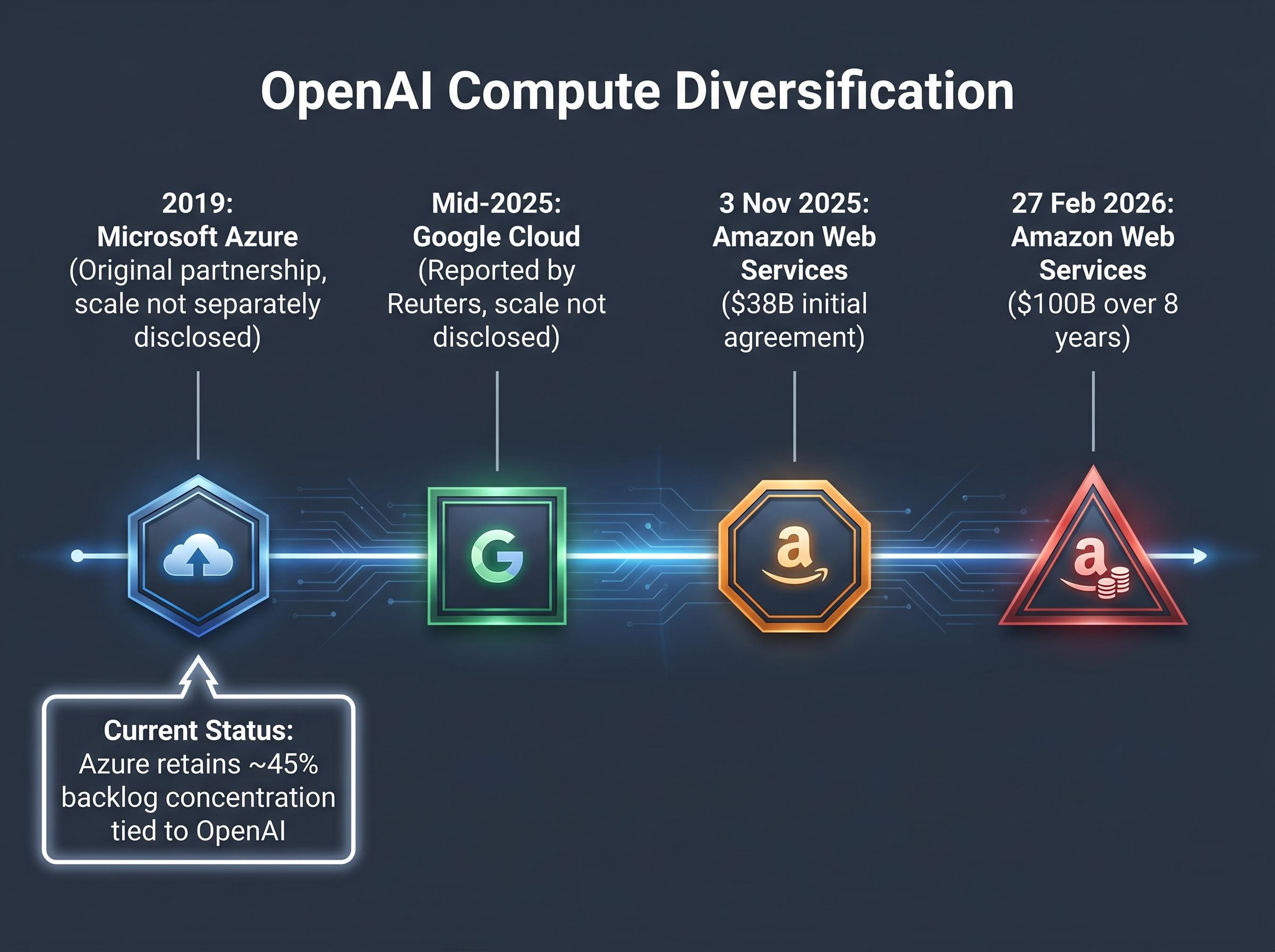

In early 2026, OpenAI signed a deal to bring Amazon Web Services into its compute infrastructure at a scale eventually worth $100 billion over eight years. Microsoft, which holds an estimated 45% concentration of its Azure backlog tied to OpenAI, disclosed this through earnings commentary without substantial pushback. That is the kind of fact that deserves a slower read.

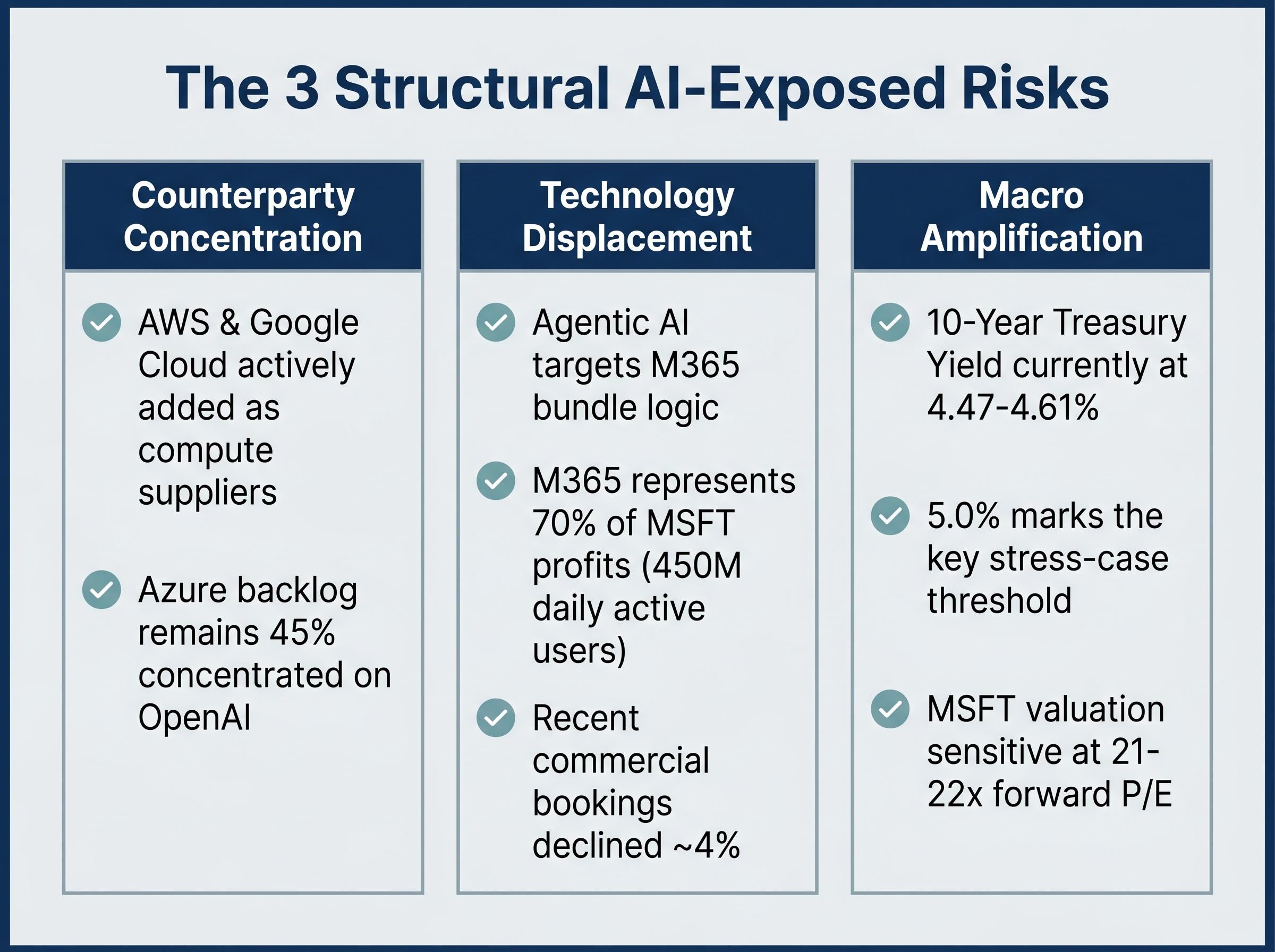

Microsoft’s headline financials remain strong: 15-18% revenue growth, 46% operating margins, and earnings per share expanding above 20% annually. Beneath the growth story, three structural pressures are building simultaneously. None of them show up clearly in a single quarter’s results. All of them matter to investors who hold or are evaluating large-cap AI-exposed technology stocks right now, in May 2026.

This article is not a buy-or-sell recommendation on Microsoft. It is a risk-architecture walkthrough aimed at investors who want to understand the systemic forces that could reprice the entire large-cap AI trade, using Microsoft as the clearest available case study.

The assumption most investors carry is straightforward: Microsoft’s 2019-era OpenAI partnership gave Azure a structural lock on OpenAI’s compute demand. That assumption is no longer accurate.

Two confirmed departures from exclusivity have reshaped the relationship. On 3 November 2025, OpenAI announced a $38 billion multi-year agreement with AWS, providing hundreds of thousands of NVIDIA GPUs including GB200s and GB300s. On 27 February 2026, a separate expansion added $100 billion over eight years. Reuters reported in mid-2025 that OpenAI was also adding Google Cloud as an additional compute supplier.

The hyperscaler capital expenditure trajectory provides the scale context for why OpenAI’s compute diversification matters: with the four largest hyperscalers collectively spending $130 billion in Q1 2026 alone and issuing $121 billion in debt in 2025 to fund buildout, the AI infrastructure race has moved to a scale where single-counterparty compute relationships are increasingly untenable from OpenAI’s operational risk perspective.

Azure Backlog Concentration Microsoft earnings commentary disclosed that approximately 45% of Azure’s reported backlog is attributed to OpenAI, a figure that measures single-counterparty dependency rather than competitive strength.

The three confirmed OpenAI compute relationships now stand as follows:

| Partner | Announcement Date | Disclosed Scale | Status |

|---|---|---|---|

| Microsoft Azure | 2019 (original partnership) | Not separately disclosed | Confirmed |

| Amazon Web Services | 3 November 2025 / 27 February 2026 | $38B initial; $100B over 8 years | Confirmed |

| Google Cloud | Mid-2025 (Reuters) | Not publicly disclosed | Reported |

This is not an OpenAI breakup story. It is a concentration erosion story, where the question shifts from “how much OpenAI revenue does Azure get?” to “what share of OpenAI’s growing infrastructure spend does Azure retain as the pie expands?” That distinction matters because the diversification is happening on terms OpenAI controls.

Microsoft 365’s dominance rests on bundle logic. Per-seat licensing of integrated applications, where compliance, security, and workflow are interdependent, makes the suite genuinely difficult to replace. An enterprise running 450 million daily active users through M365 does not swap that out because a single application is not best-in-class.

M365 accounts for approximately 70% of Microsoft’s profits. Institutional trust and broad adoption across global markets reinforce retention even during periods of product stagnation. The moat is real. The question is whether it is permanent.

The threat is not a competitor product. It is a structural shift in how enterprise software gets used.

If AI agents can execute drafting, scheduling, search, and workflow orchestration across any available tool, including free or open alternatives, the rationale for paying for the full integrated suite weakens. The specific workflow categories at risk include:

Bain & Company published research in 2025, including “Will Agentic AI Disrupt SaaS?” and “Building the Foundation for Agentic AI” (23 September 2025), framing this as an emerging structural risk to seat-based enterprise software. Gartner’s 2025 research on “digital labour” reinforced the thesis, arguing that enterprise software value may migrate from bundled seats to orchestration and agent layers.

Bain’s agentic AI research, published in September 2025, frames the shift from seat-based to outcome-based pricing not as a gradual product evolution but as a structural break, one where the unit of enterprise software value migrates from licensed access to orchestrated task completion, a distinction that carries direct implications for M365’s per-seat revenue model.

Hard evidence of broad M365 seat erosion is not yet visible in Microsoft’s public financials. Commercial bookings declined approximately 4% in the most recent quarter, partly attributed to the transition from seat-based to token-based pricing. That transition is a related but distinct signal: Microsoft itself is hedging against seat-based model pressure. The pricing model shift is worth watching precisely because it suggests management sees the same structural risk that Bain and Gartner have described.

For readers wanting to understand how slowly the enterprise AI deployment curve is actually moving, our full explainer on enterprise AI adoption rates examines why 70-80% of enterprise AI pilots fail or stall, why only 12-20% of enterprises achieve meaningful operational AI embedding, and what that failure rate means for the timeline over which agentic AI could realistically displace seat-based software models.

Most investors track earnings beats and misses as their primary risk signal. Duration risk operates on a different frequency entirely; it is invisible in earnings reports and only becomes apparent when the macro environment shifts.

The concept works in three steps:

“5.0% has emerged as the key stress-case threshold for the 10-year, with 5.25-5.5% representing the tail-risk extension.”

That 5.0-5.5% range is a tail-risk stress case, not a base case as of May 2026. But the mechanism does not require extreme scenarios to matter. A 100-150 basis point yield increase from current levels could materially compress forward price-to-earnings (P/E) and enterprise-value-to-earnings-before-interest-and-tax (EV/EBIT) multiples for large-cap technology names, even without an earnings recession.

Treasury yield mechanics have shifted materially since this analysis was framed: by 18 May 2026, Brent crude above $110 per barrel and an 80% market-implied probability of a Fed rate hike pushed the 10-year to a 15-month high, compressing the distance between current yield levels and the 5.0% stress threshold identified in this article’s duration-risk section.

Microsoft trading at 21-22 times forward earnings, near its 10-year low forward multiple, is still pricing in substantial future growth. A material rise in the discount rate reprices that growth downward even if business fundamentals hold. This is a valuation mechanism, not an earnings shock, and that distinction is what makes it easy to miss until it arrives.

Analysed individually, each of the three risks described above is manageable. Analysed together, the picture changes.

A rising yield environment that pressures tech multiples is also likely to coincide with competitive market shifts that accelerate enterprise cost scrutiny. That is exactly the condition under which agentic AI adoption accelerates, as enterprises look for efficiency gains. It is also the condition under which OpenAI has stronger incentive to diversify away from premium-priced Azure toward lower-cost alternatives. Macro tightening environments have historically coincided with enterprise cost pressure, which tends to accelerate adoption of efficiency-driven technology shifts.

| Risk Factor | Current Status | Trigger Condition | Potential Impact |

|---|---|---|---|

| OpenAI compute diversification | Active; AWS and Google Cloud confirmed | Further Azure backlog concentration decline | Azure revenue growth deceleration |

| Agentic AI bundle erosion | Theoretical; early pricing model transition signals | M365 seat count deceleration in earnings | Margin compression on 70% profit contributor |

| Treasury yield repricing | 10-year at 4.47-4.61%; below stress threshold | 10-year yield sustained above 5.0% | Forward P/E compression across large-cap tech |

Microsoft at 21-22x forward earnings looks inexpensive relative to its own history. But that multiple still embeds specific assumptions: stable Azure concentration with OpenAI, M365 seat retention, and a discount rate environment not materially worse than today. Revenue grew 15% on a constant-currency basis (18% reported) in the most recent quarter. Free cash flow, however, declined approximately 22% year-over-year (from approximately $20 billion to approximately $16 billion) as capital expenditures approximately doubled.

Bill Ackman established a position in Microsoft during Q1, citing long-term valuation attractiveness at approximately 21-22x forward earnings. Jim Cramer reduced exposure over the same period. Genuinely opposing risk reads on the same data set is itself informative about the current uncertainty level. If any two of the embedded assumptions are tested simultaneously, the compression potential for a $3 trillion market capitalisation company is meaningful.

The bull case components that remain intact are real and should not be dismissed:

Named-Investor Data Point Bill Ackman established a large stake at approximately 21-22x forward earnings, near Microsoft’s 10-year historical multiple low. Microsoft’s share price sat at approximately $424 at the time of analysis, having declined 12% to nearly 30% at peak year-to-date loss at the time of his purchases.

Risk awareness without a monitoring framework is not actionable. Three specific signals would confirm or contradict the risk thesis:

These are the review triggers that allow position sizing decisions to be tied to observable conditions rather than quarterly headlines.

AI exposure creates a specific risk profile that combines three categories, applicable to any large-cap AI-exposed stock:

The three risks identified in this article each map cleanly onto one of these categories, which is why Microsoft is an unusually instructive case study rather than a company-specific story. Azure is growing at approximately 40%. The broader Nasdaq 100 faces the same yield sensitivity dynamic; this is a sector-wide condition, not a Microsoft-specific one.

The analytical framing from available commentary describes the current setup as “acceptable rather than exceptional,” with potentially superior opportunities available elsewhere at present valuations. Investors evaluating any large-cap AI stock in 2026 should ask which of these three risk categories applies, at what intensity, and whether those risks are currently priced.

Index-level concentration risk compounds the duration sensitivity problem: Goldman Sachs’ May 2026 assessment found that the top five companies controlling roughly 30% of total US market capitalisation means passive investors may be carrying more AI-thematic duration exposure than their index allocation suggests, with individual winners and losers cancelling each other out at the index level while single-stock volatility remains elevated.

The three risks examined in this article are each invisible in Microsoft’s current headline financials, which show revenue up 15-18%, margins at 46%, and EPS growing above 20%. That invisibility is precisely the risk.

This analysis is not a reason to exit. It is a reason to define monitoring conditions, understand position sizing relative to identified risks, and avoid the error of assuming current fundamentals describe future fundamental stability. The investor debate itself, with Ackman building a position and others reducing exposure, signals that this risk-awareness window is live right now, not a retrospective exercise.

The monitoring signals identified above (M365 seat trends, Azure-OpenAI concentration, the 10-year yield threshold) are the practical takeaway. Structural risks compound quietly before they surface in earnings. The analytical work is recognising them while the headline numbers still look strong.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Duration risk refers to the sensitivity of a stock's valuation to changes in interest rates; because Microsoft's valuation embeds substantial future earnings growth, even a modest rise in the 10-year Treasury yield mechanically compresses its forward price-to-earnings multiple without any change in underlying business fundamentals.

Microsoft disclosed through earnings commentary that approximately 45% of Azure's reported backlog is attributed to OpenAI, making it a significant single-counterparty dependency rather than a straightforward indicator of competitive strength.

OpenAI signed a $38 billion multi-year agreement with AWS in November 2025, later expanded to $100 billion over eight years in February 2026, and Reuters reported in mid-2025 that Google Cloud was also added as an additional compute supplier, confirming that OpenAI has actively diversified away from exclusive reliance on Azure.

If AI agents can execute drafting, scheduling, search, and workflow orchestration across any available tool, the rationale for paying for Microsoft 365's fully integrated per-seat bundle weakens; Microsoft's own shift toward token-based pricing models is an early signal that management recognises this structural pressure.

Three key monitoring signals are: deceleration in M365 commercial seat counts disclosed through earnings, any further reduction in the 45% Azure-OpenAI backlog concentration figure, and whether the 10-year Treasury yield sustains a move above 5.0%, the threshold identified as triggering duration-risk repricing across large-cap technology names.