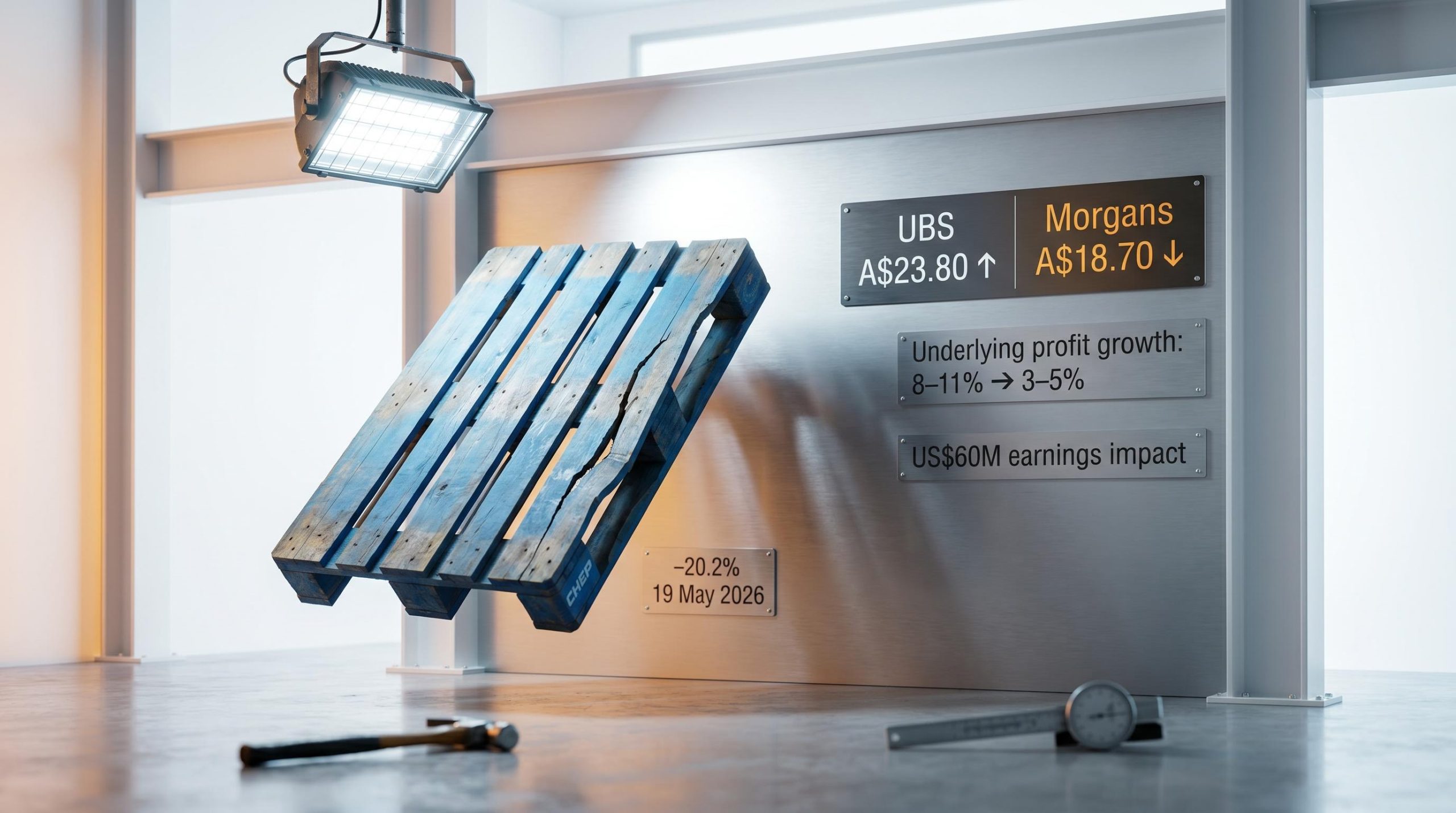

On 19 May 2026, Brambles shares opened 11.9% lower and never recovered. By the close, the stock had fallen 20.2%, erasing more than a fifth of the company’s market value in a single session. The trigger was a mid-year guidance cut that slashed underlying profit growth expectations from 8-11% to just 3-5%, more than halving the midpoint in one announcement.

The cause, according to management, was not a demand collapse. It was a capacity bottleneck in the company’s US subcontracted repair network, a distinction that matters because it frames the problem as operational rather than structural. Whether the market agrees with that framing is another question entirely.

What follows is a breakdown of the guidance revision mechanics, the operational bottleneck behind them, the split broker response from UBS and Morgans, and a framework for evaluating whether the post-selloff price represents a buying opportunity or a warning. The answer depends on information Brambles has not yet provided.

What Brambles actually cut, and by how much

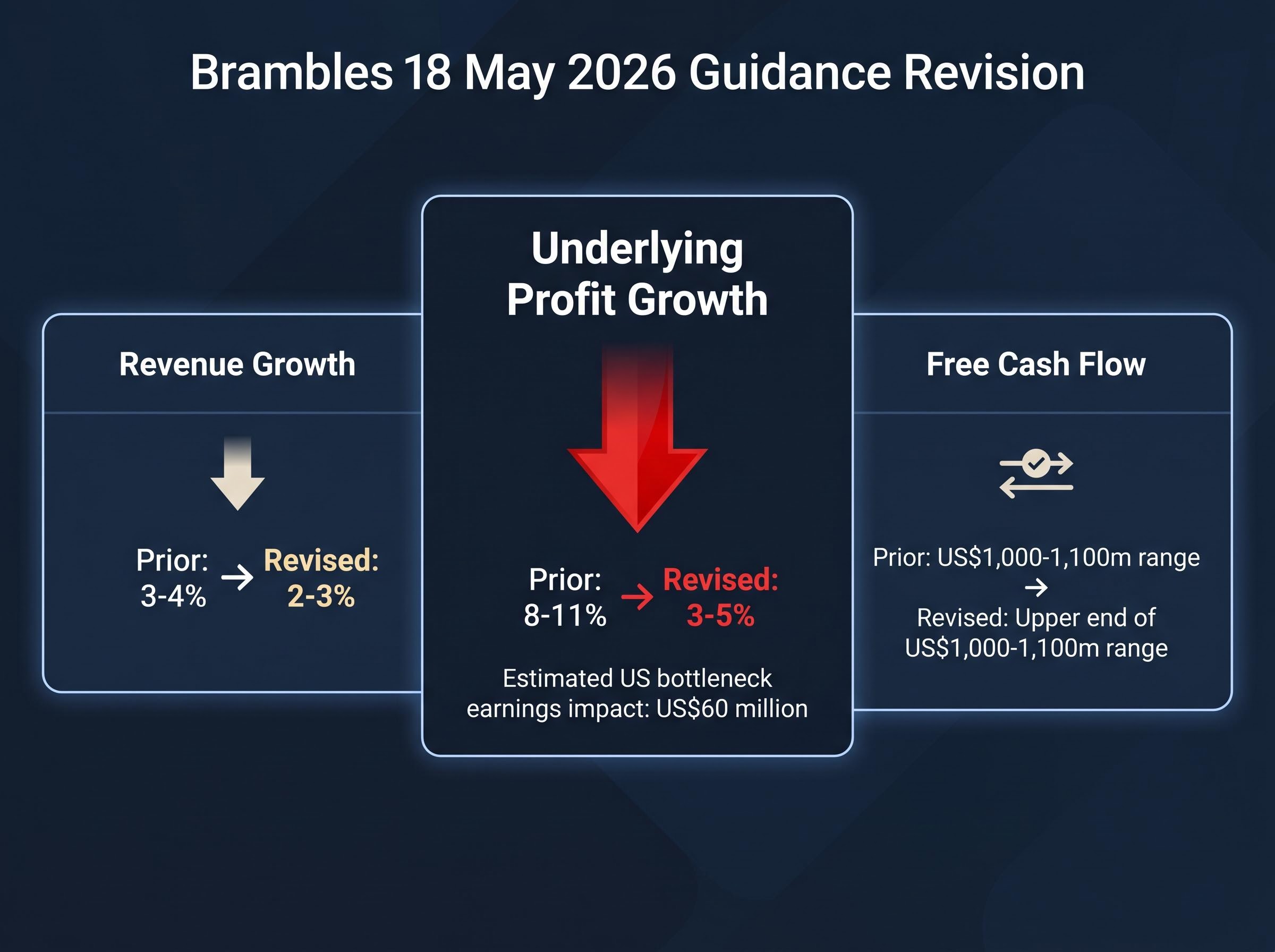

The 18 May 2026 ASX trading update revised all three headline guidance metrics, but not equally. Revenue growth guidance came down from 3-4% to 2-3%. Underlying profit growth, the figure that drove the selloff, was cut from 8-11% to 3-5%. Free cash flow guidance, however, held firm at the upper end of the US$1,000-1,100 million range.

ASX Listing Rule 3.1 continuous disclosure obligations require listed companies to immediately notify the market of any information a reasonable person would expect to have a material effect on the price or value of their securities, which is precisely the regulatory trigger that compelled Brambles to release the 18 May trading update rather than hold the guidance revision until its scheduled results.

| Metric | Prior guidance | Revised guidance |

|---|---|---|

| Revenue growth | 3-4% | 2-3% |

| Underlying profit growth | 8-11% | 3-5% |

| Free cash flow | US$1,000-1,100m range | Upper end of US$1,000-1,100m range |

The estimated earnings impact of the US bottleneck: US$60 million.

At the midpoint, the revenue guidance moved approximately 1 percentage point lower. The profit guidance moved roughly 5 percentage points lower. That asymmetry is where the real story sits, and it reflects the cost-base leverage inherent in Brambles’ business model.

The free cash flow guidance holding firm is not a minor detail. It signals that the business is still generating cash at the levels previously expected, even as profit growth compresses. For investors evaluating whether this is a deteriorating business or a temporarily constrained one, that distinction is the starting point.

When big ASX news breaks, our subscribers know first

The US repair network bottleneck: operational problem or structural warning sign?

What management said

The 18 May trading update attributed the downgrade to “repair capacity constraints in parts of Brambles’ US subcontracted service centre network.” Volume shortfalls and customer mix issues in the United States were identified as the direct consequences. Management framed the problem as operational: a bottleneck in the repair and redeployment cycle, not a loss of customer demand or competitive displacement.

This framing matters. An operational bottleneck implies a fixable, time-bound problem. A structural demand issue implies something more lasting. Management is clearly signalling the former.

What the announcement left unanswered

The trading update did not, however, provide the detail required to independently verify that framing.

What the announcement confirmed:

- The problem is located in the US subcontracted service centre network

- The earnings impact is estimated at US$60 million

- Customer mix effects are contributing alongside volume shortfalls

What remains undisclosed:

- No named facilities, cities, or states affected

- No quantified capacity utilisation figures

- No formal remediation timetable with milestones

- No specific interim measures (outsourcing contracts, capex acceleration) announced

The absence of a remediation timeline is itself a material data point. Brambles’ FY24 results (released 20 August 2024) had already discussed ongoing US network automation and service-centre upgrades, meaning this is not the first time the US repair network has required investment. That the same network is now the source of a guidance downgrade raises a fair question about whether the capital deployed to date has been sufficient.

Until management provides plant-level detail and a dated recovery plan, investors are pricing a recovery event they cannot time. That uncertainty is what separates a measured dip-buy from a speculative one.

How pallet pooling works and why a service centre bottleneck hits earnings so hard

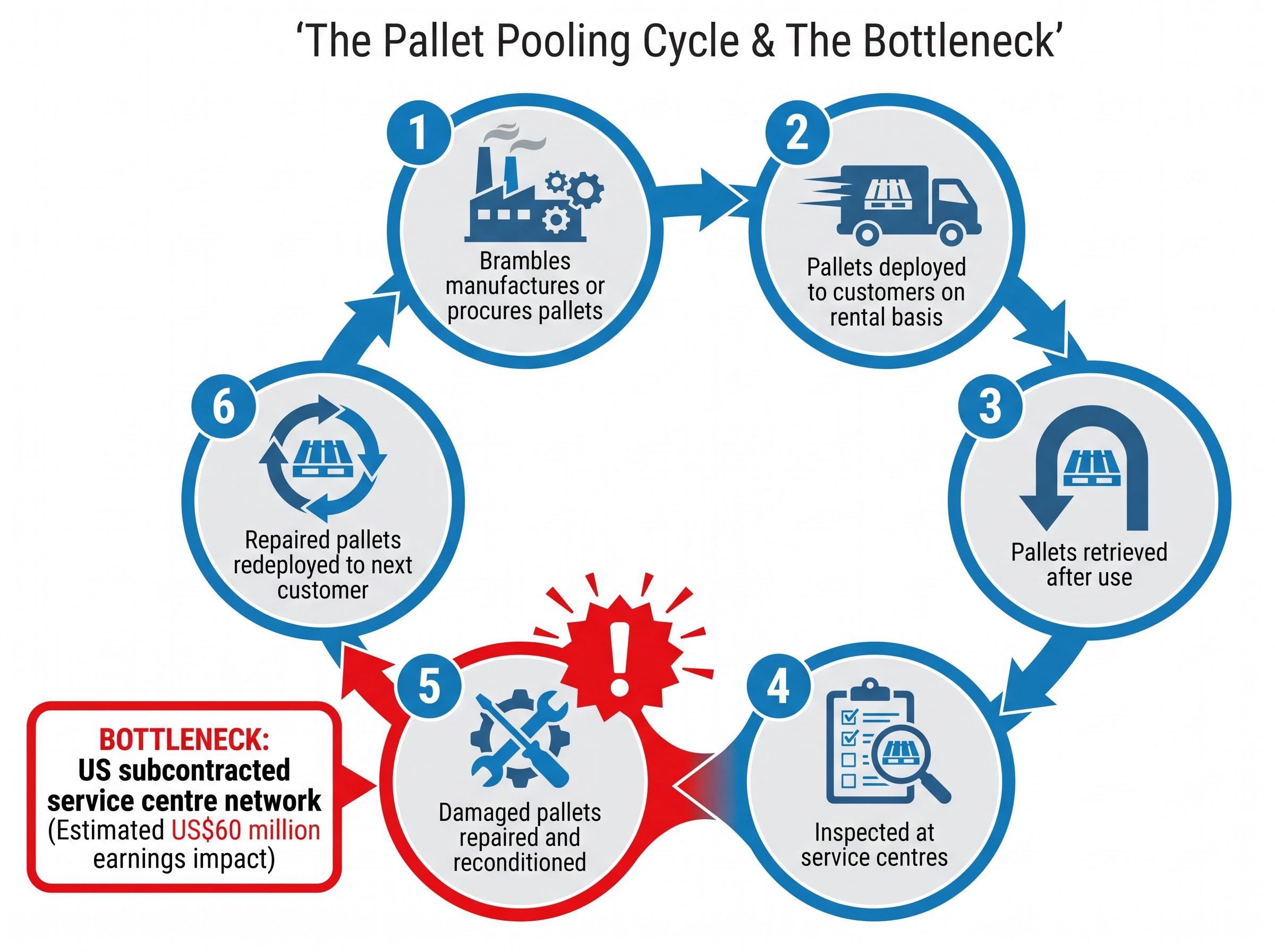

Brambles operates the CHEP pallet pooling network, the largest in the world, across the Americas, EMEA, and Asia-Pacific. The US is its single largest market. Understanding why a repair bottleneck translates directly into an outsized earnings hit requires understanding how the pooling cycle works.

The pallet pooling model operates as a continuous loop:

- Brambles manufactures or procures pallets

- Pallets are deployed to customers on a rental basis

- Pallets are retrieved after use

- Retrieved pallets are inspected at service centres

- Damaged pallets are repaired and reconditioned

- Repaired pallets are redeployed to the next customer

The bottleneck sits at step five. When repair capacity is constrained, pallets that cannot be reconditioned cannot re-enter the rental pool. Every pallet stuck in the repair queue is a pallet not generating revenue.

The revenue guidance was cut by approximately 1 percentage point at the midpoint. The profit guidance was cut by approximately 5 percentage points. That asymmetry reflects cost-base leverage: fixed costs remain while volume and revenue compress.

The margin impact is disproportionate because Brambles’ cost base does not scale down proportionally when throughput falls. Service centres still carry labour, lease, and overhead costs whether they process 90% or 70% of capacity. Fewer pallets through the system means each unit carries a higher cost burden, compressing margins well beyond the revenue shortfall.

This mechanism prevents investors from treating the downgrade as trivial. A bottleneck that persists compounds: unrepaired pallets accumulate, customer service levels deteriorate, and mix effects worsen as higher-margin contracts become harder to fulfil on time.

UBS upgrades, Morgans downgrades: what the analyst split tells investors

Within hours of the selloff, two brokers moved in opposite directions. UBS upgraded Brambles, viewing the 20.2% fall as an excessive market reaction that had substantially priced in the earnings risk. Morgans downgraded to Hold from Accumulate, treating the guidance cut as a more serious signal requiring caution.

The price targets tell the real story.

| Broker | Previous target | Revised target | Rating change | Implied upside from ~A$17.63-17.72 |

|---|---|---|---|---|

| UBS | A$25.40 | A$23.80 | Upgraded | ~34-35% |

| Morgans | A$25.50 | A$18.70 | Downgraded to Hold | ~5-6% |

UBS views the earnings risk as “substantially reflected” in the post-selloff share price, implying the market has overshot.

The gap between A$18.70 and A$23.80 is not a rounding difference. It reflects two fundamentally different assessments. UBS is answering the question: “Has the market already priced in the worst case?” Morgans is answering a different question: “Is there enough visibility on the recovery to justify buying here?”

For retail investors, the framework for interpreting this split is straightforward. When two credentialled brokers disagree by more than 25% on a revised price target within the same trading session, the disagreement itself is informative. It means genuine uncertainty exists about whether FY26 represents a floor or the beginning of a more persistent earnings reset. Neither broker is necessarily wrong; they are pricing different confidence levels in the remediation timeline.

BXB share price valuation involves at least three distinct layers of uncertainty after the May guidance cut: the earnings miss itself, the unresolved class action damages quantum, and the AUD/USD translation drag on US-dollar-denominated cash flows, and collapsing these into a single price target, as both UBS and Morgans have done, necessarily requires assumptions that reasonable investors will weight differently.

A framework for evaluating post-selloff entry: what investors should be weighing

Risk factors to monitor

Three unknowns will determine whether the selloff is a buying opportunity or an early warning.

The first is the remediation timeline. Management has not provided a dated plan for resolving the US repair capacity constraint. Without that timeline, investors cannot model when earnings normalise.

The second is customer mix persistence. The 18 May announcement identified mix effects alongside volume shortfalls. If higher-margin contracts have been disrupted, the margin impact could extend into FY27 even if volume recovers.

The third is further broker consensus adjustments. Only UBS and Morgans have published revised targets. As Macquarie, Citi, and other brokers update their models in coming days, additional downgrades could reset market expectations lower.

Conditions that would support a recovery thesis

Several factors provide a counterweight to the risk.

- The free cash flow guidance held at the upper end of US$1,000-1,100 million, meaning the business is still generating cash at previously expected levels

- Management’s framing is explicitly operational, not structural; no loss of customer demand or competitive displacement has been identified

- UBS sees ~34-35% upside to its revised target, implying substantial value at the current price if remediation proceeds

- A formal remediation announcement with milestones would materially narrow the uncertainty premium currently embedded in the share price

The risk asymmetry is worth noting. The cash generation floor limits the downside scenario (this is not a business burning cash), but the absence of a recovery timetable means investors are being asked to price a turnaround they cannot date. The difference between a value trap and a recoverable earnings miss typically comes down to whether the underlying demand is intact. Nothing in the 18 May announcement suggests it is not.

Classifying selloffs as irrational overreactions, temporary setbacks, or structural disruptions before looking at a price-to-earnings multiple is the sequencing discipline that separates investors who act on data from those who act on price movement alone, and the Brambles situation maps most closely to the temporary setback category: real near-term damage, intact competitive moat.

Before entering a position, investors may benefit from answering several specific questions:

- What is my confidence level in the remediation timeline, given no formal plan has been disclosed?

- What is my exit thesis if FY27 guidance also disappoints?

- How much weight do I place on the free cash flow floor as downside protection?

- Am I comfortable holding through the information gap between now and the 1H26 results?

For investors already holding BXB who need to decide whether to hold through the information gap, trim exposure, or wait for the 1H26 results before acting, our dedicated guide to post-earnings decision frameworks examines the structured approach of writing conditional decision rules before an earnings release, including specific guidance-cut thresholds that trigger a trim, and covers how analyst revision timing affects the probability that post-selloff drift continues in either direction.

What a 20% single-day fall on a blue chip ASX stock actually means for long-term holders

A 20.2% single-session decline on a major ASX industrial is genuinely unusual. This is not a speculative small-cap; Brambles is one of the largest industrial companies on the exchange. The magnitude of the fall warrants serious analysis rather than a reflexive response in either direction.

Shares opened 11.9% lower at the bell, then continued to sell off through the session, closing down 20.2%. The sequential nature of the decline, gap down followed by a further leg lower, suggests sustained selling pressure rather than a single block trade.

No prior Brambles guidance downgrade of comparable severity has been documented in publicly accessible sources across the FY22-FY25 period. The company generally upgraded or reaffirmed guidance during those years, benefiting from pricing power and strong demand across CHEP Americas and EMEA. There is no clean historical recovery roadmap to reference.

The BXB class action judgment delivered in April 2026 dismissed the majority of shareholder claims while upholding liability for a narrow two-month window in late 2016, leaving the total financial impact unquantified pending damages proceedings and any appeal, a layer of legal overhang that sat above the stock even before the May guidance cut.

Even Morgans, which downgraded to Hold, set its revised target at A$18.70, implying limited further downside from the post-selloff close. UBS cut its target from A$25.40 to A$23.80, a 6.3% reduction, confirming that even the most constructive broker is not dismissing the downgrade as trivial. Long-term holders benefit from separating the legitimate concern, a US$60 million earnings miss with an unclear resolution timeline, from the mechanics of post-shock price discovery, which routinely overshoots fundamental revisions on high-volume days.

The repair job ahead: what Brambles needs to show investors to reclaim lost ground

The entire analytical arc of this downgrade converges on a single forward question: what evidence would shift the risk-reward calculus?

Evidence that would support upgrading conviction:

- A formal US remediation timetable with specific milestones and a completion target

- 1H26 results showing volume recovery in the affected US service centres

- Confirmation that customer mix effects are contained to FY26 and not persisting into FY27

- Updated guidance that narrows or lifts the current 3-5% underlying profit growth range

Evidence that would confirm caution:

- A further guidance cut at the 1H26 results

- Disclosure that repair capacity constraints have spread beyond the initially affected centres

- Loss of contract volume to competitors as a consequence of service-level disruption

- Additional broker downgrades that compress the consensus target toward or below the Morgans A$18.70 level

The next information catalyst is the 1H26 results and accompanying investor presentations. No specific date has been announced as of 19 May 2026. The spread between the UBS target (A$23.80) and the Morgans target (A$18.70) quantifies the range of expert disagreement. The free cash flow guidance maintenance remains the most concrete positive data point available. And the US$60 million earnings impact quantifies precisely what the remediation programme needs to claw back to restore prior expectations.

The current information environment requires investors to hold genuine uncertainty rather than force false precision. That is itself a valid reason some will wait for the 1H26 results before acting. UBS believes the selloff has more than priced in the risk. Morgans believes it offers little margin of safety. The resolution of that tension depends on operational evidence that does not yet exist.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.