Zip Co has grown revenue at an annualised rate above 75% over three years and delivered its strongest profit result on record in FY25, reporting net profit after tax of A$79.9 million. Yet the Zip Co share price is trading more than 50% below its 52-week high.

That kind of disconnect between operating performance and market pricing is either a significant opportunity or a warning that the market sees something in the earnings quality that headline numbers do not fully reveal. For Australian investors watching ASX-listed fintech stocks in mid-2026, Zip is one of the most contested valuation debates on the exchange. This analysis unpacks the business model, examines the FY25 earnings step-change in detail, explains the regulatory shift now in effect, and maps the risks and opportunities, giving readers a structured basis for forming their own view on whether the current price represents value or a value trap.

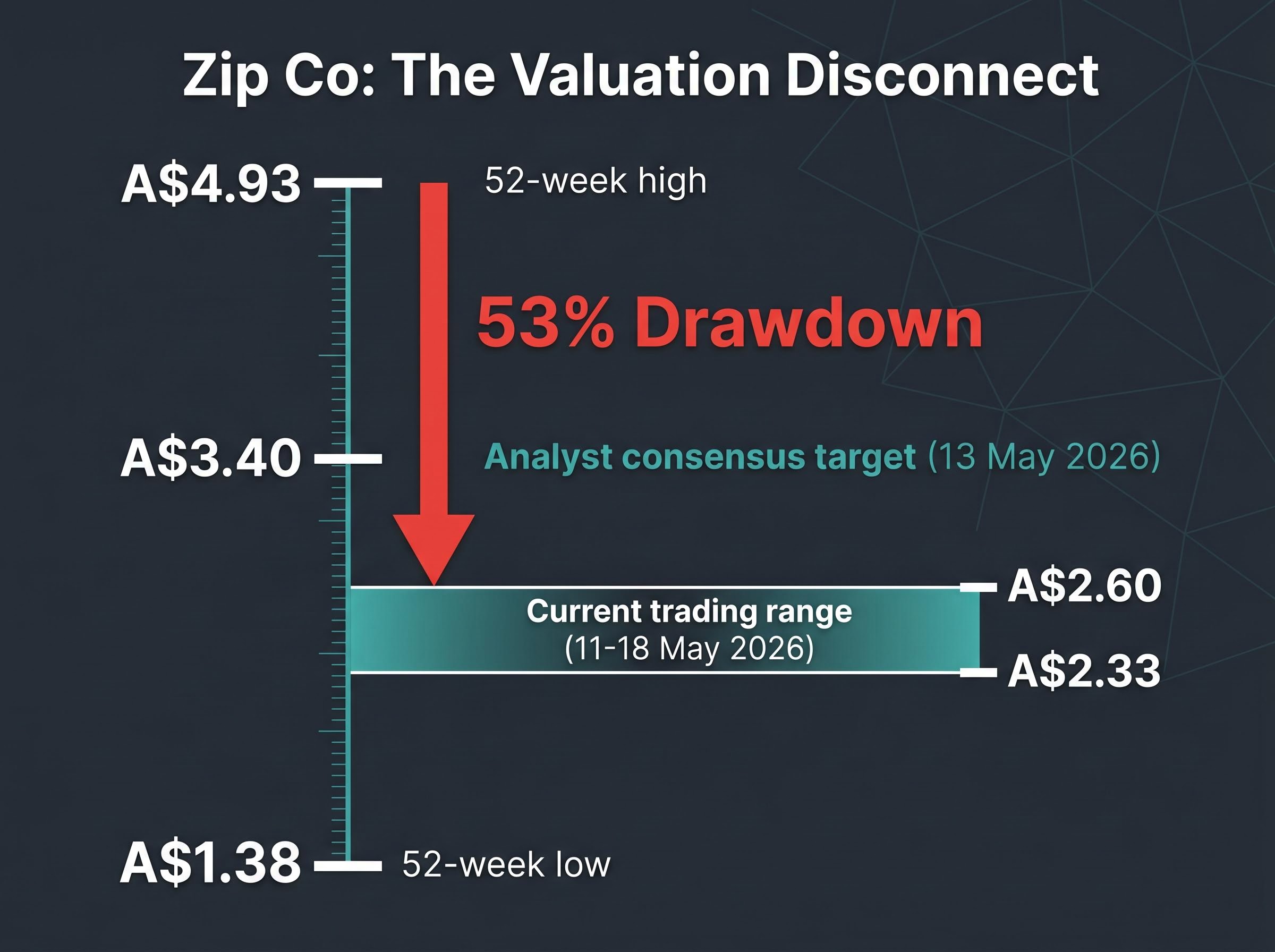

A 53% drawdown despite record earnings: what the price chart is actually signalling

Between 11 and 18 May 2026, Zip traded at approximately A$2.33-A$2.60 on the ASX. The 52-week high of A$4.93 was set earlier in the cycle. The 52-week low of A$1.38 marks the trough.

- Current trading range: A$2.33-A$2.60 (11-18 May 2026)

- 52-week high: A$4.93

- 52-week low: A$1.38

- Analyst consensus target: approximately A$3.40 (13 May 2026), with seven buy-rated analysts

At the mid-range of recent trading, the stock sits roughly 53% below its 52-week peak. A court loss in May 2026 added a near-term sentiment drag, drawing coverage as a specific risk event. The analyst consensus target of approximately A$3.40 implies 38-40% upside from current levels, a gap wide enough to demand explanation.

The May 2026 court loss that contributed to the sentiment drag is the Australian rebrand ruling from the High Court, which ordered Zip to cease using its trade mark in Australia within 28 days; because the US business generates approximately 80% of divisional cash earnings, the financial impact of the ruling is structurally contained even as it introduces near-term operational uncertainty.

Zip’s share price is approximately 53% below its 52-week high as of mid-May 2026, despite reporting record revenue and a net profit of A$79.9 million in FY25.

The fundamentals have not deteriorated. Revenue is at record levels. Profit is at record levels. The drawdown is not telling a story of decline; it is telling a story of unresolved doubt. The rest of this analysis examines what, specifically, the market is uncertain about.

When big ASX news breaks, our subscribers know first

How Zip actually makes money: the line-of-credit model most investors misread

Many retail investors treat Zip as interchangeable with a pay-in-4 instalment provider. It is not. Zip operates a revolving line-of-credit model, closer in structure to a credit card than to a simple instalment product. A customer is approved for a credit limit, makes purchases across participating merchants, and repays over time with flexibility on repayment amounts and timing.

This distinction matters because it changes the revenue mix and the risk profile entirely. Zip generates income from three sources:

- Merchant fees: charged to retailers when a customer completes a transaction using Zip

- Account fees: recurring charges to customers for maintaining their credit line

- Interest and late payment charges: income earned when customers carry balances or miss scheduled payments

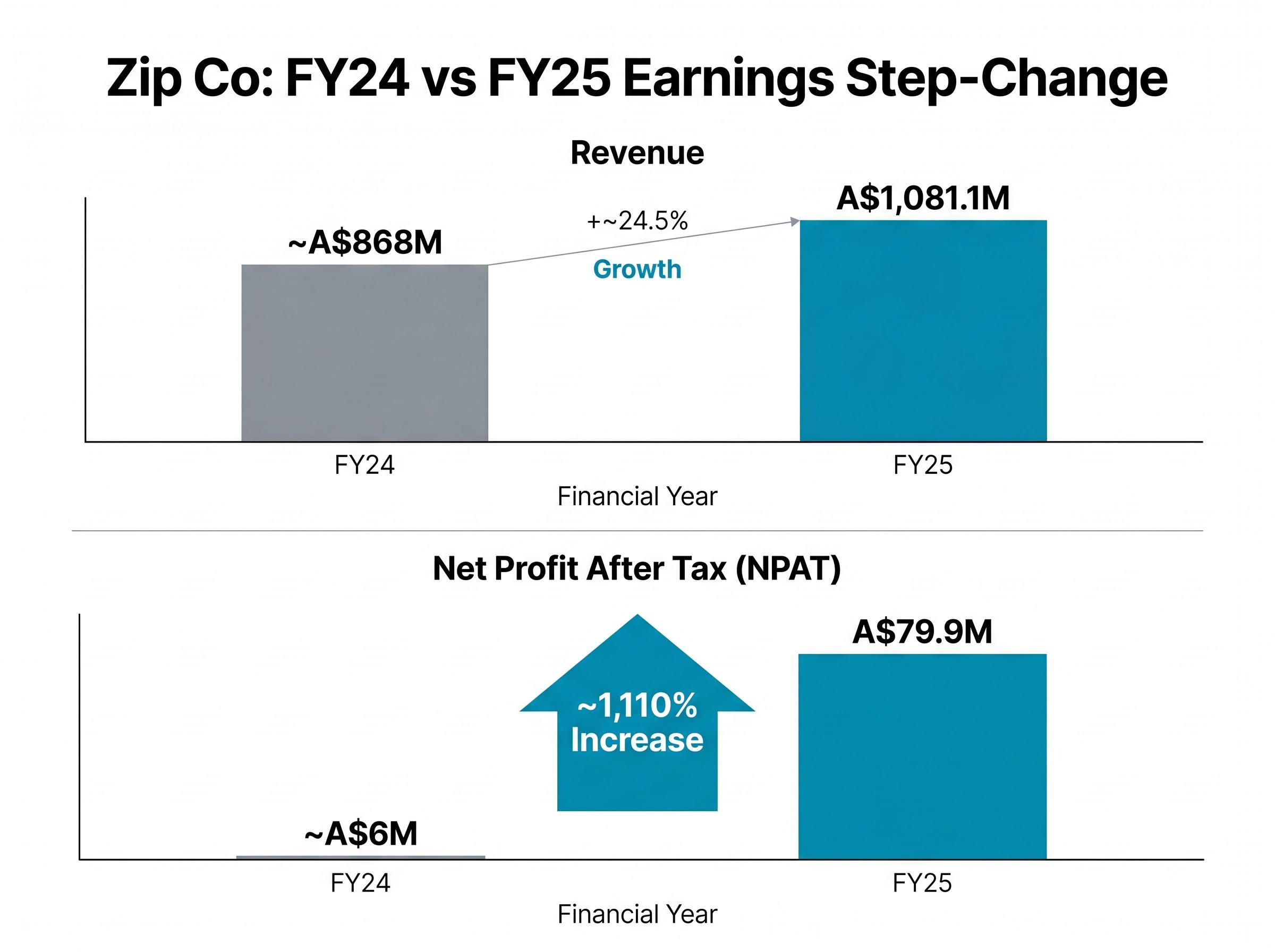

That third category is what makes Zip structurally different. Interest income places the company closer to a credit provider than a payments processor. In FY25, total revenue reached A$1,081.1 million, a scale that reflects the breadth of this model across millions of active accounts.

Why the model’s risks are different

Because Zip extends credit, it carries exposure to bad debts, arrears sensitivity, and funding cost fluctuations that a pure pay-in-4 product does not. Zip was already subject to more regulated credit-like treatment than many BNPL peers even before formal regulation arrived in June 2025. Understanding this distinction is the foundation for assessing both the earnings quality and the risk profile in the sections that follow.

The FY25 earnings step-change: genuine turnaround or one-year anomaly?

The scale of improvement from FY24 to FY25 is not marginal. It is a structural shift.

| Metric | FY24 | FY25 | Change |

|---|---|---|---|

| Revenue | ~A$868M | A$1,081.1M | ~23.5-25% increase |

| NPAT | ~A$6M | A$79.9M | ~1,110% increase |

| EBITDA | N/A | A$170.3M | N/A |

| US cash earnings | N/A | >US$100M | N/A |

Net profit after tax grew approximately 1,110% year-on-year in FY25, reaching A$79.9 million.

FY24 itself was a milestone, the first year Zip returned to profitability after a net loss of A$678 million accumulated over prior years. But A$6 million in net profit was a proof of concept, not a scaled result. FY25 converted that proof into a materially different earnings base.

The US segment was the engine. Revenue from US operations reached approximately US$657.9 million, with cash earnings exceeding US$100 million and total transaction value (TTV) of US$9.345 billion. A business that many analysts had expected Zip to exit or wind down became the single largest profit contributor.

The operational decisions behind the improvement were deliberate. Between 2022 and 2024, Zip exited a range of loss-making international markets, concentrating capital in its core ANZ and US operations. The FY25 result is a product of that rationalisation, not a cyclical uplift. The question the market is now debating is whether this new earnings level is sustainable or whether it represents a high-water mark tied to favourable credit conditions.

BNPL regulation is now live: what the new rules mean for Zip and its competitors

The Australian regulatory environment for buy now, pay later providers moved from proposal to law during 2024-2025. The Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Act 2024 classified BNPL products as low-cost credit contracts, and the operational requirements took effect on 10 June 2025.

The framework imposes three core obligations on providers:

- Credit licensing: BNPL operators must hold an Australian credit licence

- Modified responsible lending obligations: providers must conduct affordability and suitability assessments before extending credit

- ASIC Regulatory Guide 281 (RG 281) compliance: published in May 2025 (announced via ASIC media release 25-069MR on 8 May 2025), this guide sets detailed expectations for how providers meet their obligations

These are not future requirements. They are current operating conditions.

ASIC Regulatory Guide 281 sets out the detailed compliance expectations for low-cost credit contract providers, covering how modified responsible lending obligations must be applied in practice, including the affordability and suitability assessment processes that all licensed BNPL operators are now required to implement.

What the new rules mean specifically for Zip’s competitive position

Zip’s existing credit infrastructure and experience operating under regulated-credit frameworks give it a relative cost advantage. Smaller pay-in-4 startups that never built affordability assessment systems face a steeper compliance build. The regulation is expected to thin the provider field, with undercapitalised or unprofitable operators likely to exit or consolidate.

The trade-off is real, however. Stricter approval processes may reduce approval rates, creating a near-term volume headwind even as the competitive landscape thins. For Zip, the question is whether the consolidation benefit outweighs the friction cost over the next two to three years.

The risks that explain why the market is not rushing back in

The gap between analyst targets and the share price is not a simple inefficiency. It reflects specific, unresolved concerns.

- Credit and arrears risk: Zip’s profitability is highly sensitive to credit loss rates. The trade-off between volume growth and underwriting discipline is a central management challenge; loosening approval criteria can drive transaction volumes but raises loss ratios. Elevated interest rates and cost-of-living pressure on lower-income consumers make this risk persistent.

- Funding cost risk: Zip’s line-of-credit model requires ongoing debt capital. The elevated interest rate environment increases the cost of that funding and compresses net interest margins, directly affecting profitability even if transaction volumes grow.

- Earnings durability and return on equity: The FY24 return on equity (ROE) was 1.8%, reflecting modest returns on capital even after the return to profitability. The market is asking whether FY25 represents a durable new earnings level or a peak-cycle result, and until ROE expands materially, that question remains open.

- Competitive pressure: Afterpay (Block), Klarna, Affirm, and bank-offered instalment products all compete for the same consumer. Large digital wallets including Apple Pay and PayPal continue expanding into instalment credit. Zip has survived this competition and remained profitable, but the intensity of the field constrains pricing power.

Zip’s return on equity was 1.8% in FY24, reflecting that the company is still generating modest returns on capital even after its return to profitability.

The May 2026 court loss added a specific near-term risk event to these structural concerns. Collectively, these factors explain why seven buy-rated analysts and a 38-40% implied upside have not yet been enough to bring capital back into the stock.

The risk-reward picture in mid-2026: what the numbers require investors to believe

At A$2.33-A$2.60, Zip is priced for doubt. At the analyst consensus of approximately A$3.40, it is priced for resolution. The gap between those two numbers is a bet on earnings durability.

What the bull case requires

Investors buying at current levels are implicitly underwriting three beliefs: that FY25’s A$79.9 million in net profit is a sustainable baseline rather than a one-off; that ROE will expand materially from the FY24 level of 1.8% as the earnings base scales; and that the US business, which generated more than US$100 million in cash earnings, will continue growing. Add regulatory consolidation tailwinds and a three-year revenue compound annual growth rate of 75.7% to FY24, and the constructive case is credible if those conditions hold.

What the bear case rests on

The market’s reluctance to reprice rests on equally specific concerns: that the credit cycle could turn, rapidly eroding profitability in a high-arrears environment; that funding costs will compress margins further if rates remain elevated; and that FY25 may prove to be the earnings peak rather than the earnings base. Until reported data resolves these tensions, the discount is unlikely to close on sentiment alone.

For investors wanting to stress-test the consensus A$3.40 target against the full range of analyst views, our deep-dive into the analyst price target debate maps the spread from A$2.63 to A$5.53, examines the 85.6% cash earnings growth figure that separates Zip from BNPL operators that did not survive the rate cycle, and assesses what the RBA rate environment means for the investment case.

Three forward indicators will serve as empirical tests:

With US credit losses tracking below target at 1.75% of transaction volume through Q4 FY26 and US transaction volume growing above 40% year-on-year in April 2026, the early FY26 data points are running in the direction of the bull case rather than the bear case, though a single quarter does not resolve a multi-year durability question.

- Arrears rates: any sustained deterioration would validate the bear case directly

- ROE trajectory: expansion above the FY24 baseline would signal durable improvement in capital efficiency

- US TTV growth: continued growth in transaction volumes would confirm the US segment’s profit contribution is structural

Zip’s story is improving, but the market is asking for proof, not promises

The 53% drawdown from Zip’s 52-week high is not explained by deteriorating fundamentals. Revenue is at record levels. Net profit grew more than tenfold. The US business is profitable at scale. The drawdown reflects unresolved market scepticism about whether the quality of those earnings can persist through a credit cycle.

Three developments would shift that view: sustained arrears discipline demonstrating underwriting quality holds under pressure, ROE expansion above the FY24 baseline proving that profit translates into adequate returns on capital, and continued US cash earnings generation confirming the largest profit driver is structural rather than cyclical.

Zip is a stock suited to investors with a higher risk tolerance, a multi-year horizon, and the discipline to monitor the specific credit and return metrics that will determine the outcome. The data, not the narrative, will settle this debate.

Earnings quality and rate sensitivity have emerged as the dominant sorting variables across ASX technology and fintech stocks during the 2025-2026 drawdown cycle, with companies demonstrating positive cash flow before the trough recovering materially faster than high-growth peers whose profitability remained theoretical, a pattern directly relevant to how investors should interpret Zip’s FY25 NPAT step-change.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.