A single bank trimming half its South Korean position while simultaneously holding the other half captures the defining tension of 2026 investing: when is the right moment to take profits on a trade that keeps working? Citigroup published a note on 16 May 2026 partially closing its bullish KOSPI position, citing overheating signals and elevated global rate risks. The timing is striking. The KOSPI had surged approximately 74% year-to-date through that publication date, driven overwhelmingly by semiconductor and AI-linked technology stocks, and was approaching the psychologically significant 8,000 level before a 6.12% single-session decline on 15 May. What follows is a dissection of the anatomy of that decision: what is driving the rally, why Citigroup stopped short of a full exit, which risk signals are flashing most urgently, and what the episode reveals about disciplined position management when high-conviction trades become crowded.

How South Korean equities became 2026’s most spectacular trade

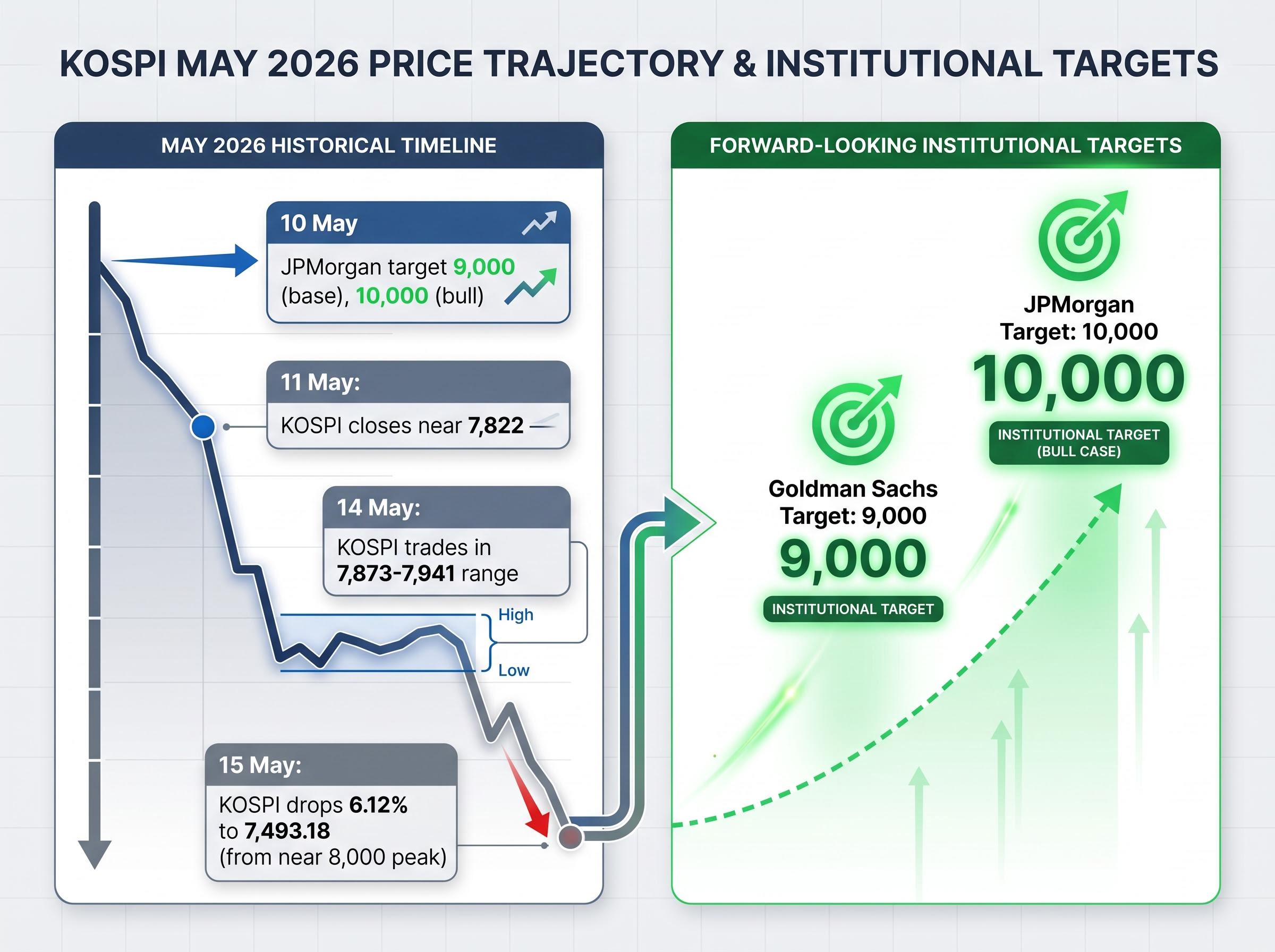

The 74% year-to-date figure cited in Citigroup’s note understates the full picture. By mid-May, the KOSPI had gained approximately 85% for the year, with the rally’s velocity accelerating sharply into the month. The index closed near 7,822 on 11 May, traded in the 7,873-7,941 range on 14 May, and reached record highs in the vicinity of 8,000 before the 15 May pullback brought it to 7,493.18.

Three structural forces explain why the move carried as far as it did:

- AI and semiconductor demand: Korean chipmakers, principally Samsung Electronics and SK Hynix, are the primary beneficiaries of the global AI hardware supercycle, and their earnings revisions have driven index-level returns disproportionately.

- Corporate governance reform: A multi-year programme aimed at reducing the long-standing “Korea Discount” has attracted institutional capital that was previously structurally underweight Korean equities.

- Earnings upgrades across the industrial and technology sectors: Broad-based revisions have supported valuation expansion beyond the semiconductor names alone.

The memory chip supply structure underpinning SK Hynix’s gains is unlike any previous DRAM upcycle: combined hyperscaler capex is projected at $725 billion in 2026, AI data centres now account for an estimated 70% of total memory shipments, and new manufacturing lines will not reach mass production before 2027, creating a near-term supply vacuum that reinforces rather than shortens the cycle’s duration.

JPMorgan raised its base-case KOSPI target to 9,000 and its bull-case target to 10,000 in a 10 May note, while Goldman Sachs independently raised its target to 9,000 in separate May commentary. The major institutional consensus remains firmly bullish.

Understanding these drivers is necessary before evaluating whether Citigroup’s caution is premature or overdue. An 85% rally looks like speculative excess in isolation; against the backdrop of an AI hardware supercycle, governance reform, and two of Wall Street’s largest banks targeting further 20-34% upside, the picture is more complex.

When big ASX news breaks, our subscribers know first

What the KOSPI actually is and why it moves differently from Western benchmarks

Index composition and sector weighting

The KOSPI (Korea Composite Stock Price Index) is the primary benchmark for South Korean equities, listed on the Korea Exchange. Its composition skews heavily toward large-cap technology and industrial conglomerates, with Samsung Electronics and SK Hynix serving as the dominant index heavyweights. Both are primary supply-chain beneficiaries of AI-driven hardware demand.

This concentration has a direct consequence: the KOSPI’s performance often diverges sharply from broader emerging market indices when global semiconductor demand accelerates or contracts. When chip cycles run hot, as they are in 2026, the index amplifies upside far beyond what a diversified EM benchmark would deliver. The same concentration amplifies downside when the cycle turns.

Key structural characteristics of the KOSPI include:

- Heavy technology and semiconductor sector weighting relative to other EM benchmarks

- Sensitivity to global chip demand cycles, making it a de facto semiconductor proxy for many portfolio managers

- A reform-driven structural catalyst distinct from cyclical earnings momentum

The Korea Discount and why it is narrowing

The “Korea Discount” refers to the persistent undervaluation of Korean equities relative to comparable Asian and Western peers. For years, complex cross-shareholding structures among conglomerates (chaebols), weak shareholder-return policies, and governance concerns suppressed valuations even when earnings justified higher multiples.

An ongoing reform programme targeting these structural issues has begun to narrow the discount, attracting long-term institutional allocations that were previously withheld on governance grounds. This discount-reduction narrative is a distinct, structural source of upside that operates independently of the semiconductor cycle, and it helps explain why capital has flowed into Korean equities even from investors who have no specific view on chip demand.

Why Citigroup pulled back, not out

The mechanics of the decision matter. Citigroup closed half its long KOSPI position while retaining the other half, explicitly framing the move as locking in partial gains while preserving upside exposure if the rally continues. This was not a reversal of its thesis on Korean equities; it was a recalibration of exposure to match shifting risk-reward.

The primary trigger was comparative: the KOSPI displayed more pronounced overbought characteristics than the S&P 500 at the time of assessment, making relative over-extension the deciding signal. A secondary concern was harder to quantify but no less significant: excessive South Korean retail investor enthusiasm, which Citigroup flagged as a warning beyond standard valuation metrics.

The data behind that retail warning is stark.

| Signal | Value | Risk Implication |

|---|---|---|

| KOSPI YTD gain | ~85% | Pace of rally historically unsustainable without consolidation |

| Single-session retail net buying (13 May) | 6.7 trillion won | Euphoric retail participation near a psychologically significant level |

| Margin loan balance | 35.7-36.1 trillion won (record) | Record leverage amplifies forced-selling risk in any pullback |

| Margin loan YTD change | +20% | Leverage growth accelerating into the rally’s later stages |

| Investor deposits (brokerage dry powder) | 136.98 trillion won (record) | Large potential inflows could extend the rally or cushion a decline |

The 6.12% single-session decline on 15 May provided a live illustration of what leverage-driven volatility looks like in practice. The KOSPI fell from near 8,000 to 7,493.18 in a single day, a move whose speed reflects the margin debt embedded in the market’s structure.

The half-exit decision is the most instructive element of this story. It demonstrates how professional risk managers respond to overbought signals without abandoning a thesis, and the retail leverage data quantifies exactly why the downside risk has become asymmetric.

The KOSPI margin loan balance data published in late April 2026 recorded a combined KOSPI and KOSDAQ margin balance of approximately 34.26 trillion won at that point, a figure that has since climbed further to the 35.7-36.1 trillion won range cited in Citigroup’s note, indicating that leverage continued to build rapidly into the rally’s later stages.

The macro forces Citigroup is watching beyond Korea

The KOSPI rally has not occurred in a vacuum, and the deeper tension in Citigroup’s note concerns the divergence between Korean equity performance and a tightening global financial environment.

Citigroup identified long-end yield breakouts across multiple sovereign curves as a genuinely global phenomenon. This is not a U.S.-specific rate story.

| Instrument | Yield / Price | Context |

|---|---|---|

| U.S. 10-year Treasury | 4.59-4.60% | Elevated; constrains Fed rate-cut expectations |

| UK 10-year gilt | 5.18% | Reflects persistent UK inflation concerns |

| Japanese 10-year JGB | 2.71% | Near a 29-year high; signals unwinding of global carry dynamics |

| Brent crude | $109.26/barrel | Middle East tensions drove sharp May escalation |

| WTI crude | ~$101-102/barrel | Back above $100; reignites inflation expectations |

The oil price dimension is particularly relevant for South Korea as a major energy importer. Citigroup noted that persistently elevated crude prices could steepen yield curves, with the U.S. particularly exposed. The March-April spike tied to U.S.-Israel-Iran tensions was the specific catalyst that pushed Brent above $100.

The interaction between oil price and rate expectations creates a compounding headwind for Korean equities specifically: sustained Brent above $100 adds approximately one percentage point to CPI readings, which reduces the probability of Fed rate cuts, sustains dollar strength, and simultaneously raises Korea’s energy import costs, tightening financial conditions through three separate channels at once.

Three channels transmit these tightening conditions to Korean equity risk:

- Dollar strength and capital flows: Higher U.S. yields sustain dollar strength, raising the opportunity cost of holding emerging market assets and pressuring foreign capital flows into Korea.

- Oil import costs: Korea’s status as a major energy importer means $100+ oil increases input costs, pressures the current account, and adds to domestic inflation.

- Global risk-off sentiment: Simultaneous yield breakouts across the U.S., UK, and Japan compress the global appetite for high-beta equity exposure, and an 85% YTD rally makes the KOSPI one of the highest-beta positions available.

Citigroup’s overall assessment was cautiously watchful rather than bearish: financial conditions have not tightened sufficiently to terminate the bull market, but a moderate pullback in risk assets was assessed as plausible near-term.

What Citigroup’s partial exit reveals about position management in momentum markets

The half-in, half-out structure is a deliberate hedge against outcome uncertainty. It is not a prediction that the rally ends at 8,000; it is an acknowledgement that the risk-reward ratio has shifted enough to warrant reducing exposure while the trade remains profitable.

Morgan Stanley noted record hedge-fund buying in Korean equities as of May 2026, adding an institutional crowding dimension to the retail leverage already discussed. When both hedge-fund positioning and retail margin debt sit at record levels simultaneously, the difficulty of exiting a popular trade at scale increases materially. Early, partial profit-taking becomes strategically rational precisely because late, forced exits become more costly.

The coexistence of opposing forces complicates any binary view:

- Bull case (remaining upside): Record investor deposits of 136.98 trillion won in brokerage accounts represent a pool of potential inflows; JPMorgan and Goldman Sachs targets of 9,000-10,000 imply 20-34% further upside from post-pullback levels; the governance reform catalyst continues to operate independently of cyclical conditions.

- Bear case (mounting risk): Record margin debt of 35.7-36.1 trillion won amplifies forced-selling risk; record hedge-fund positioning creates correlation risk; global yields and oil prices tighten the macro backdrop in ways that make 85% YTD gains difficult to sustain on fundamentals alone.

Citigroup explicitly framed its move as a precautionary measure to lock in partial gains, not a full reversal of its conviction on Korean equities. The distinction matters: the thesis has not changed, but the cost of being wrong has risen.

The rally that still has room to run, with less margin for error

The structural bull case remains

The durable fundamental drivers behind the KOSPI’s rally have not been invalidated by the 15 May pullback. The semiconductor supercycle remains intact. AI hardware demand continues to accelerate. Corporate governance reform is a multi-year programme with further milestones ahead. JPMorgan’s base-case target of 9,000 and bull-case target of 10,000, published on 10 May, imply meaningful upside from the approximately 7,500 post-pullback level. Goldman Sachs’ independent 9,000 target reinforces the institutional conviction.

The semiconductor supercycle debate carries direct weight for KOSPI investors because Samsung Electronics and SK Hynix together represent a significant portion of the index, meaning the question of whether the $3.8 trillion added across the PHLX Semiconductor Index since early 2026 reflects durable earnings or speculative excess is also a question about whether the KOSPI’s 85% year-to-date move has fundamental support.

The risk triggers to watch

What would change the picture is identifiable and monitorable. Investors holding Korean equity exposure, whether through direct positions, ETFs, or emerging market funds with Korea weighting, should track these specific conditions:

- U.S. 10-year yield trajectory: A sustained move materially above 4.6% would tighten financial conditions further and pressure EM capital flows.

- Brent crude price: Sustained levels above $110/barrel increase Korea’s import costs and reignite inflation expectations globally.

- KOSPI margin debt (weekly change): Any sharp acceleration beyond the current 35.7-36.1 trillion won record would signal further leverage build-up into an already stretched market.

- Foreign investor flow data: The domestic-buying-versus-foreign-selling dynamic has supported the rally so far; a reversal in that pattern would remove a key structural pillar.

- South Korean corporate earnings revisions: As long as upgrades continue, the fundamental case holds. A downward revision cycle, particularly in semiconductors, would undermine the rally’s foundation.

The 15 May single-day 6.12% drop came from near 8,000. Whether the index recovers that level or declines further is the near-term test of retail leverage sustainability.

Citigroup’s half-step is the whole lesson

An 85% year-to-date rally in a major index, record retail leverage, record hedge-fund crowding, and tightening global macro conditions do not make the trade wrong. They make it more expensive to be wrong.

Citigroup’s partial exit preserves optionality in both directions. If JPMorgan’s 9,000-10,000 target proves correct, the remaining half of the position captures the upside. If the 15 May pullback deepens into something more sustained, gains have already been banked on the half that was closed. The decision is less a sell signal than a marker of where disciplined risk management draws a partial line.

The conditions that would turn a partial trim into a full exit are the same ones identified above: accelerating global yield tightening, oil sustaining above $110, forced-selling cascades from margin calls, or a reversal in the earnings upgrade cycle that underpins the semiconductor thesis. Each is monitorable. None has triggered yet.

Brazil’s emerging market outperformance in 2026, with the Ibovespa up roughly 23% year-to-date against the KOSPI’s 85%, illustrates how the same $100-plus oil environment that tightens Korea’s macro backdrop acts as a structural tailwind for net energy exporters, a divergence that portfolio managers running broad EM allocations must weigh when deciding how much of their Korean overweight to preserve.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.