Alphabet has appreciated roughly 250% over five years, pushing its market capitalisation to approximately $4.8 trillion and its share price near $400. The stock analysis question at this price is not whether Alphabet is a great business. It is. The question is whether that quality is already reflected in the valuation, and whether two live Department of Justice (DOJ) antitrust proceedings plus AI-native search competition have been adequately discounted. What follows is a structured scenario framework, bull and bear cases included, designed to help investors evaluate whether current entry points make sense for their own risk tolerance rather than relying on headline ratings.

The $4.8 trillion problem: what the math requires for attractive returns

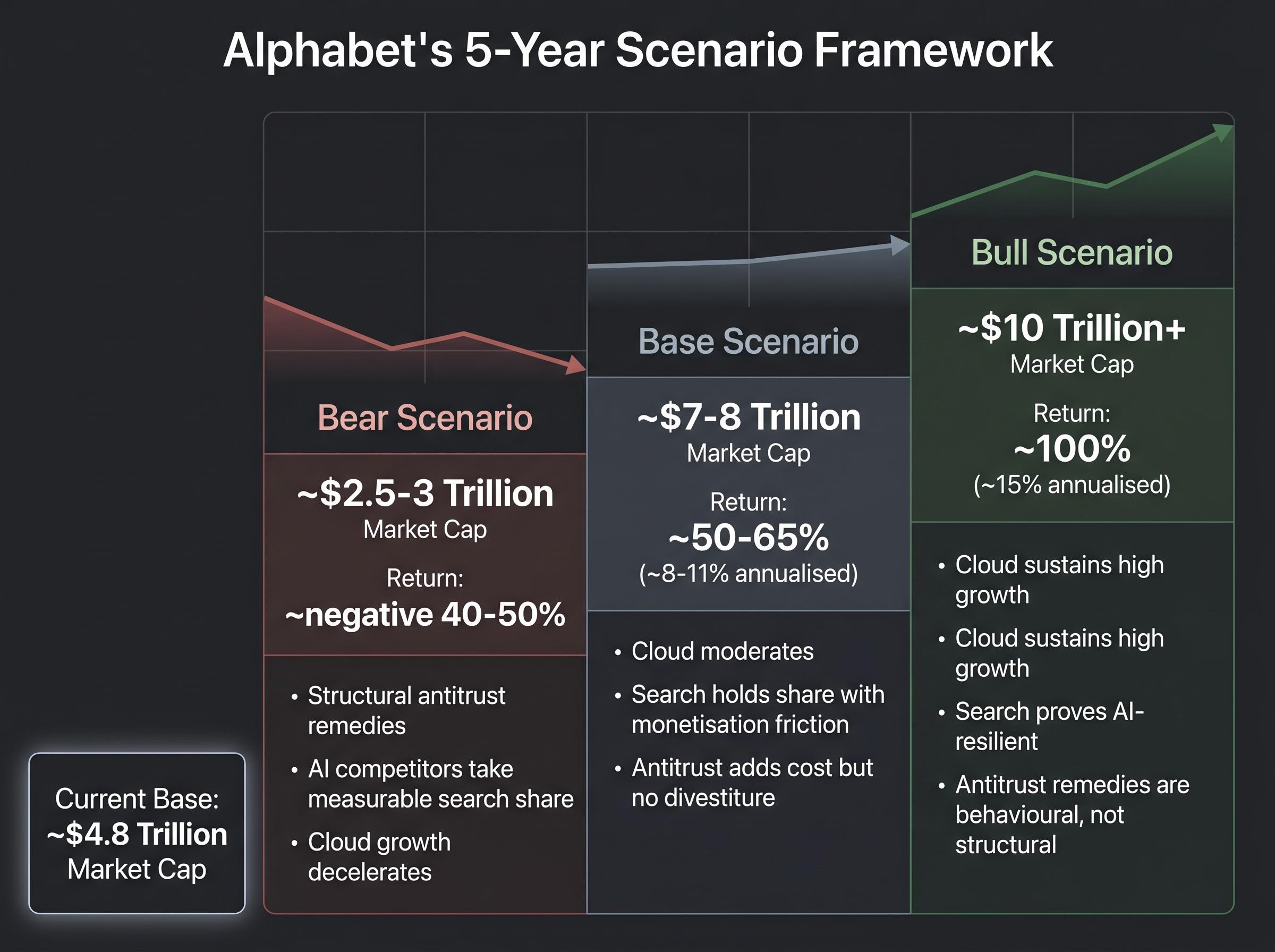

The starting point is arithmetic, not opinion. At approximately $4.8 trillion, Alphabet would need to reach roughly $10 trillion in market capitalisation over five years to deliver the kind of compounding that justifies buying at today’s price. That implies an annualised return of approximately 15-16%, a rate that exceeds historical large-cap equity averages by a wide margin.

The valuation multiples frame the constraint set. Alphabet trades at a forward price-to-earnings ratio of approximately 30x, a trailing P/E near 35x, and a price-to-sales ratio at its highest level over the past decade. None of these figures are red flags in isolation for a company growing revenue at this pace. But they do narrow the margin for error: the stock is priced for sustained excellence, not for a business that merely holds its ground.

The AI company framing matters for valuation because a business priced as a search incumbent and a business priced as a vertically integrated AI operator carry structurally different multiples, and Q1 2026 results, with EPS of $5.11 against a $2.64 consensus estimate, make the case that the second label is more accurate.

The $10 trillion threshold: For Alphabet to deliver attractive long-term returns from its current valuation, the company would need to roughly double its market capitalisation over five years, a target that requires exceptional execution across Search, Cloud, and subscriptions with no structural regulatory disruption.

The table below illustrates three return scenarios from the current base.

| Scenario | Implied 5-year market cap | Required annualised return |

|---|---|---|

| Bear | ~$3.5 trillion | Negative |

| Base | ~$7-8 trillion | Modest (8-11%) |

| Bull | ~$10 trillion+ | Attractive (15-16%) |

The question every subsequent section addresses is whether the specific evidence supports that bull case, or whether base and bear scenarios deserve more weight than current market pricing implies.

When big ASX news breaks, our subscribers know first

Google Services: the core profit engine’s enduring strength and growth

The bull case starts here. Google Services is Alphabet’s margin engine, and the most recent quarter showed that engine accelerating rather than decelerating. Operating margins expanded from approximately 42% to 45%, and Google Search revenue reached approximately $60 billion for the quarter, with growth accelerating from 17% to 19%.

Management’s argument is counterintuitive but increasingly supported by the numbers: AI integration is generating more search activity, not cannibalising it. Improved advertiser targeting through AI tools has created a self-reinforcing revenue cycle where higher relevance drives higher click-through rates, which attracts increased advertiser spend, which funds further AI investment.

The revenue base extends well beyond Search:

- Google Search: approximately $60 billion quarterly revenue, 19% growth

- YouTube advertising: approximately $10 billion quarterly revenue, 11% growth; ranked first in US streaming for three consecutive years with approximately 200 million hours of daily living room viewing

- Paid subscriptions: 350 million subscribers, up from 325 million at the end of the prior year, with segment growth of approximately 17-19%

The subscription flywheel Google rarely advertises

The 350 million paid subscriber base is often overlooked in the investment debate. Gmail, Google Docs, and the broader Workspace ecosystem provide a distribution channel for AI-powered premium upgrades that neither OpenAI nor Perplexity currently replicates at comparable scale.

This installed base gives Alphabet a structural advantage for monetising AI at the consumer level. The upsell opportunity, converting free users to paid tiers through AI-enhanced productivity features, operates across products that hundreds of millions of people already use daily. Subscriptions, platforms, and devices revenue growth of 17-19% suggests the conversion is already underway.

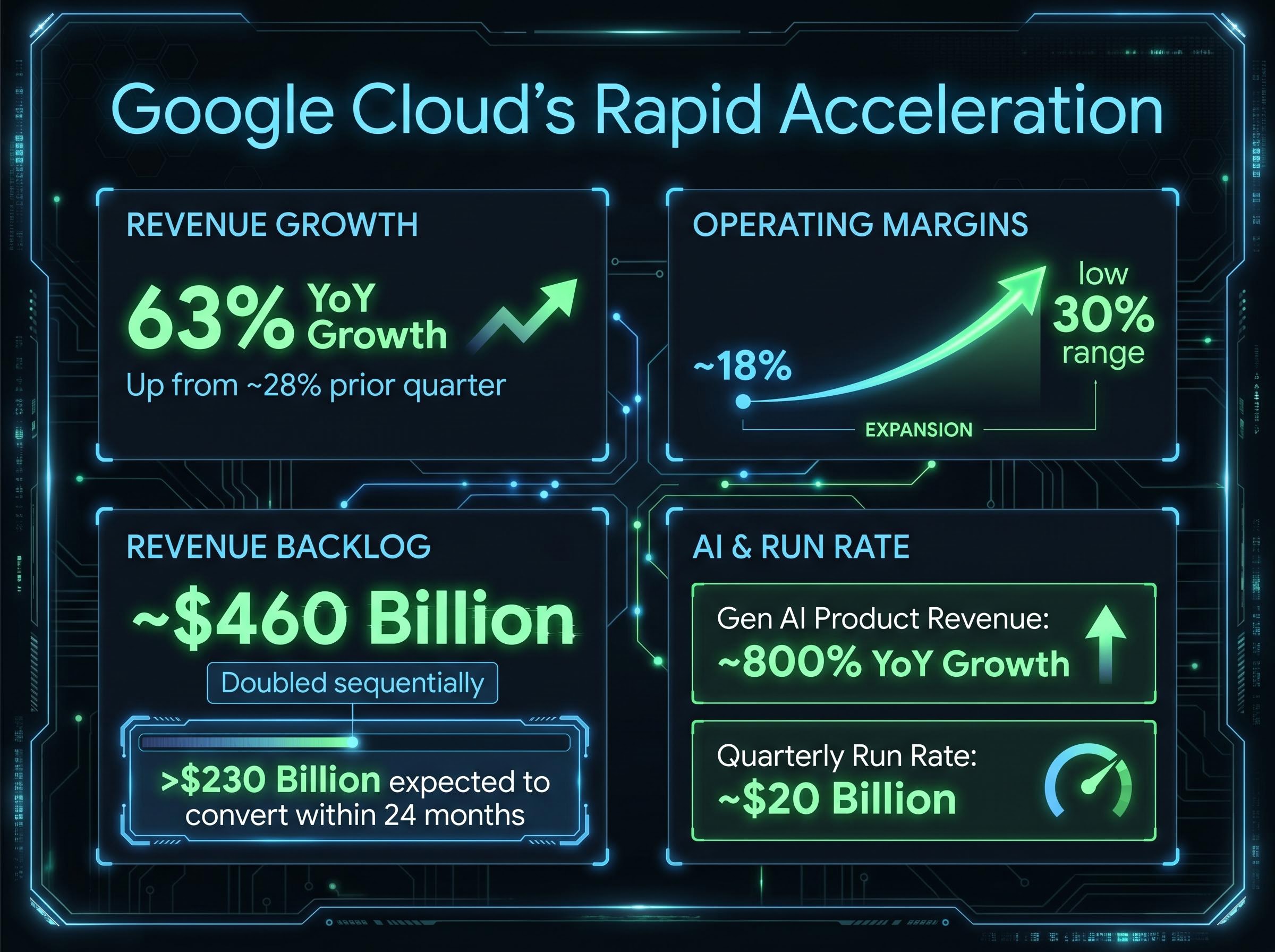

Google Cloud’s 63% quarter and what the backlog reveals

Google Cloud grew revenue 63% year over year in the most recent quarter, up from approximately 28% in the prior quarter. That acceleration is the single most significant near-term data point in the Alphabet bull case.

The backlog tells a forward-looking story. Cloud revenue backlog reached approximately $460 billion, roughly doubling sequentially, with more than $230 billion expected to convert to revenue within 24 months. Against a most recent quarterly run rate of approximately $20 billion, that backlog provides a degree of revenue visibility that partially de-risks the infrastructure investment.

Cloud backlog conversion is the mechanism that links the $460 billion committed figure to actual recognised revenue, with Goldman Sachs characterising the tripling of cloud operating income as a game-changer for Alphabet’s multiple expansion potential.

Three milestones capture Cloud’s trajectory:

- Operating margins expanded from approximately 18% to the low 30% range, demonstrating improving unit economics at scale

- The backlog doubled sequentially to $460 billion, the clearest measure of enterprise demand for Alphabet’s AI infrastructure

- Generative AI product revenue within Cloud grew approximately 800% year over year, indicating that the AI workload thesis is converting to billable contracts

$460 billion in Cloud backlog: This figure, roughly doubled from the prior quarter, represents Alphabet’s most concrete evidence that enterprise customers are committing long-term capital to its AI infrastructure.

The cost side complicates the enthusiasm. Capital expenditures approximately doubled year over year, and free cash flow declined approximately 50%. Investors are being asked to trust that infrastructure spending converts to durable earnings. The backlog and margin expansion suggest it may; the FCF compression is the price of that bet today.

How real is the AI search disruption threat?

OpenAI, Perplexity, and Apple are consistently framed across 2025 and 2026 coverage as strategic threats to Google’s search dominance. The competitive evidence, however, is qualitative rather than quantitative.

- OpenAI (ChatGPT): Positioned as an answer-engine alternative to traditional search, with web-browsing integration that directly addresses informational queries. The most direct threat to Search’s query volume, though no post-January 2025 institutional report provides a numeric estimate of Google’s query share loss attributable to ChatGPT.

- Perplexity AI: Explicitly built as an AI-native search replacement, with growing venture backing and user adoption. Competitive framing remains strategic rather than numerically documented in public sources.

- Apple: Reported to be developing more sophisticated in-house search capabilities, with long-term potential to reduce its dependence on Google as Safari’s default engine. No accessible source confirms the launch of a full-scale Apple web search product.

The structural mechanism of disruption is clear in principle. AI answer engines resolve queries directly, reducing click-through behaviour to traditional search results. That compresses the monetisable surface area of search advertising. Google’s Network segment, at approximately $7 billion in revenue, provides a partial proxy for third-party ad ecosystem health, but does not isolate AI-driven effects.

AI query share data from First Page Sage, published in April 2026 and drawing on StatCounter, Similarweb, and Alphabet earnings disclosures, estimates that ChatGPT accounts for approximately 17% of all global digital queries, a figure that contextualises the scale of volume now routing outside traditional search interfaces.

Google’s own AI integration as defence and risk

Alphabet’s primary competitive response is AI Overviews, formerly the Search Generative Experience, which integrates AI-generated answer summaries directly into Google Search results. The intent is to retain query volume within Google’s ecosystem rather than ceding it to standalone AI tools.

The financial effect remains an open empirical question. AI Overviews may protect query volume while simultaneously compressing advertising revenue per query if users receive answers without clicking through to advertiser-linked results. Alternatively, improved query understanding could increase ad relevance and revenue per query. Neither outcome has been documented with publicly quantified data. This ambiguity is itself a reason investors cannot fully price the disruption risk in either direction.

The antitrust cases every Alphabet investor must understand

Two DOJ proceedings are live, and neither has produced a final remedy order as of mid-May 2026. The range of potential outcomes is unusually wide, spanning from operational restrictions to forced structural divestitures.

| Case | Current status | Worst-case remedy |

|---|---|---|

| Search distribution monopoly | Liability ruling (Judge Amit Mehta, August 2024); remedy phase ongoing | Forced termination of default search agreements (Apple arrangement at risk); potential divestiture of Chrome or Android |

| Ad tech stack | DOJ targeting divestiture of ad server and ad exchange; no final order | Structural divestiture of advertising technology assets |

The search distribution case is the more immediate concern. Judge Mehta’s August 2024 liability ruling found that Google unlawfully maintained monopolies in general search and search text advertising. The remedy phase is examining whether to restrict or eliminate default search distribution agreements, the arrangement with Apple chief among them, or to pursue structural relief including data sharing with competitors.

The ad tech case targets a different layer of the business. The DOJ has argued that Google should divest parts of its advertising technology stack, potentially separating the ad server from the ad exchange. A forced divestiture here would directly affect the infrastructure through which Alphabet processes digital advertising transactions.

Neither case has produced a final remedy order as of mid-May 2026. The uncertainty is real and ongoing, not a resolved legacy overhang. Investors face a spectrum of outcomes from behavioural restrictions to structural divestitures, and cannot collapse that range into a single probability-adjusted discount.

With Google Services operating at approximately 45% margins, the financial stake in preserving the current search distribution model is significant. Any remedy that meaningfully restricts default search placement or forces asset separation would directly affect the company’s highest-margin business.

For investors wanting to map the full legal landscape in detail, our dedicated guide to Alphabet’s antitrust proceedings covers the December 2025 search distribution remedies order, the mechanics of the annual auction mechanism starting Q1 2027, and analyst estimates of how the Apple deal restructuring affects revenue, alongside the ad-tech case judge’s signals on divestiture.

Bull, base, and bear: structuring your own Alphabet decision

The prior sections provide the inputs. This section provides the framework for weighting them.

| Scenario | Key drivers | Implied 5-year market cap | Estimated return |

|---|---|---|---|

| Bull | Cloud sustains high growth; Search proves AI-resilient; antitrust remedies are behavioural, not structural | ~$10 trillion+ | ~100% (approx. 15% annualised) |

| Base | Cloud moderates; Search holds share with monetisation friction; antitrust adds cost but no divestiture | ~$7-8 trillion | ~50-65% (approx. 8-11% annualised) |

| Bear | Structural antitrust remedies; AI competitors take measurable search share; Cloud growth decelerates | ~$2.5-3 trillion | ~negative 40-50% |

Evercore ISI’s Mark Mahaney has characterised the risk-reward as attractive, framing Alphabet as a top large-cap AI beneficiary. Wedbush’s Dan Ives has repeatedly described the company as a “core AI winner” with meaningful upside from AI-driven monetisation. That bullish institutional consensus anchors on the Services margin of approximately 45% as the earnings quality floor and the $460 billion Cloud backlog as the growth visibility anchor.

Two variables determine which scenario materialises:

- The antitrust remedy outcome: Behavioural restrictions preserve the current business model with added cost. Structural divestitures (Chrome, Android, ad tech assets) would fundamentally alter the company’s competitive position and margin profile.

- The rate of measurable query share loss to AI competitors: If public data emerges showing material query volume migration from Google to AI answer engines, the bear case gains quantitative support it currently lacks.

Investors who cannot tolerate the antitrust tail risk should size their position accordingly. Investors with a five-year-plus horizon may treat the Cloud backlog visibility and Services margin durability as partial insurance against the bear scenario. The framework is the tool; the probability weighting is the investor’s own.

Alphabet’s path to $10 trillion: a complex equation

Alphabet’s business fundamentals, 63% Cloud growth, 45% Services margins, 350 million paid subscribers, are exceptional by any measure. The valuation requires sustained exceptional performance over five-plus years with no structural regulatory disruption. That is a high bar, even for a company executing at this level.

The two unresolvable uncertainties, the antitrust remedy outcomes and the magnitude of AI search disruption, are the honest reason this remains a difficult allocation decision rather than an obvious buy or an obvious avoid. Neither variable has produced publicly quantified data that would allow investors to assign confident probabilities.

Waymo optionality, with the autonomous vehicle unit targeting 1 million weekly paid trips by end of 2026 and operations across 12 cities, represents a mid-decade revenue vector that current earnings multiples do not capture and that neither the Cloud backlog nor the Services margin analysis surfaces directly.

Great businesses and great investments are not always the same thing at any given price. At $4.8 trillion, Alphabet is priced for a future where nearly everything goes right. The scenario framework above is the appropriate tool for this decision: assign probabilities to the bull and bear cases based on a personal assessment of those two variables, rather than anchoring to any single analyst rating.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.