Why Your ETF Portfolio May Be Less Diversified Than You Think

52 mins ago

Australia’s proposed capital gains tax overhaul, announced in the 2026-27 Federal Budget on 12 May 2026, does not look dramatic at first glance. The 50% CGT discount gives way to an indexed cost base system with a 30% minimum effective tax floor, commencing 1 July 2027. Yet for an investor compounding a $100,000 portfolio at 8% annually over 30 years, the difference between the old effective rate and the new one is not a rounding error. It is a six-figure gap in terminal wealth. This guide sets out the compounding mathematics behind that gap, explains the mechanics of the new regime (including what remains unknown), and provides a specific portfolio construction playbook for preserving more after-tax wealth across the transition and beyond.

Capital gains tax drag does not function like a one-off fee. Each time a gain is realised and taxed, the investor compounds forward on a smaller base. That smaller base produces a smaller gain the following year, which is taxed again, producing a still-smaller base. The effect multiplies rather than adds. Over a decade, the difference between two effective tax rates feels modest. Over three decades, it reshapes retirement wealth.

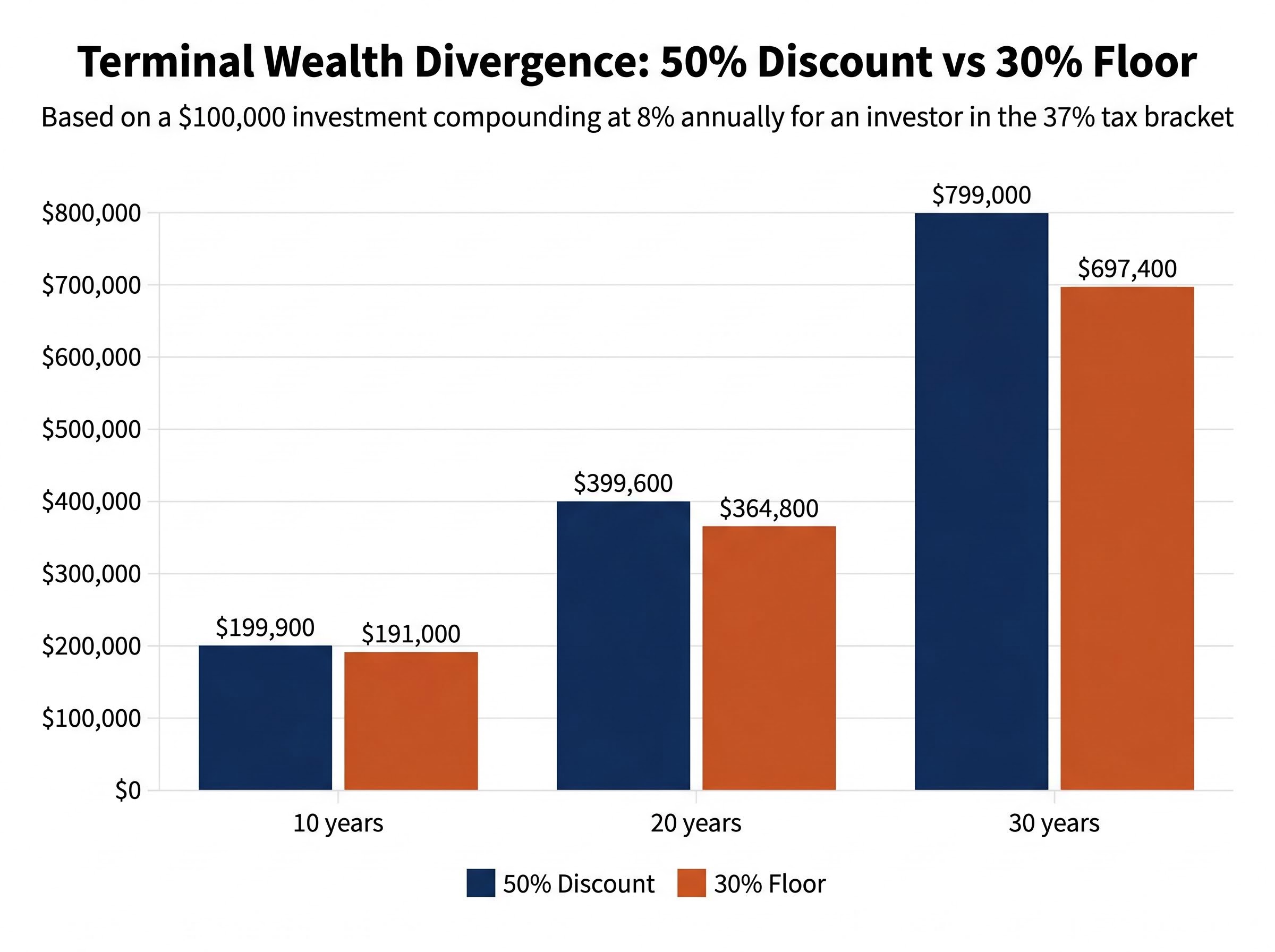

Consider an investor in the 37% marginal tax bracket, compounding $100,000 at 8% nominal growth with moderate annual turnover. Under the current 50% CGT discount, the effective rate on realised gains sits around 18.5%. Under the proposed 30% minimum floor, the effective rate rises to approximately 30% in most scenarios. That difference, roughly 0.5-1 percentage point of annual after-tax return, produces the following divergence in terminal wealth:

| Time Horizon | Terminal Wealth (50% Discount) | Terminal Wealth (30% Floor) |

|---|---|---|

| 10 years | $199,900 | $191,000 |

| 20 years | $399,600 | $364,800 |

| 30 years | $799,000 | $697,400 |

These are illustrative figures using simplified assumptions. No independent 30-year modelling incorporating the Budget-specific parameters has been published as of mid-May 2026. The Treasury and FSC fact sheets provide limited effective-tax-rate comparisons for 5-, 10-, and 20-year holding periods, which serve as the closest published benchmark.

At the 30-year mark, the gap between the two regimes exceeds $100,000 on a single $100,000 initial investment. For investors with 20-40 year horizons, particularly younger Australians, this is not a policy footnote. It is a structural reduction in lifetime wealth that demands a strategic response.

The reform replaces a simple mechanism with a two-part system. Understanding both parts, and how they interact, is the foundation for every planning decision that follows.

Under the current rules, an investor who holds an asset for more than 12 months receives a 50% discount on the nominal capital gain. The taxable gain is halved, then taxed at the investor’s marginal rate. Under the proposed regime, the cost base is instead indexed to inflation (so only the real gain is taxed), but a minimum effective tax rate of approximately 30% applies regardless of the investor’s marginal bracket. These are two separate elements operating together: indexation reduces the nominal gain, and the floor ensures the effective rate does not fall below 30%.

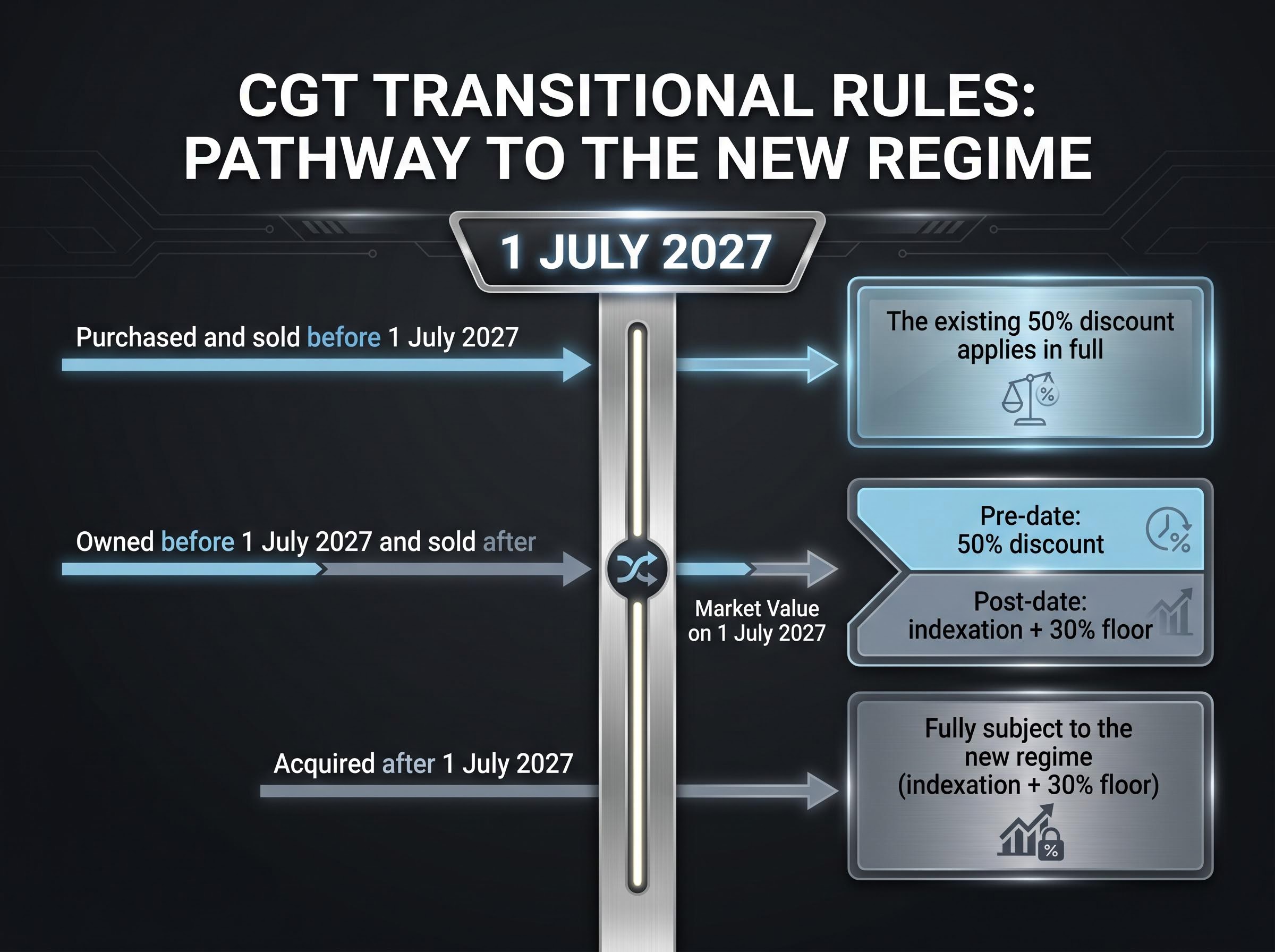

The transitional rules, set out in the Treasury fact sheet released with the Budget (budget.gov.au, accessed 16 May 2026), determine which regime applies depending on when an asset was acquired and sold:

The Treasury fact sheet on the CGT reform confirms the gain-splitting methodology for transitionally held assets, establishing that the pre-1 July 2027 portion retains the 50% discount while the post-commencement portion is subject to indexation and the 30% minimum floor.

Superannuation funds retain the existing one-third (33%) CGT discount under the new rules, a structural advantage that becomes more significant as personal-name effective rates rise.

No exposure draft, ATO Law Companion Ruling, or ATO FAQ page specific to this reform has been released as of mid-May 2026. Several material questions remain open.

The precise methodology for indexation, whether based on daily or annual CPI uplift, has not been confirmed. Whether any small-investor thresholds or asset-class carve-outs will apply is unknown. ATO worked examples demonstrating how the pre- and post-1 July 2027 gain apportionment will be calculated in practice have not been published. Platforms such as Stockspot have indicated they intend to update their tax engines and reporting systems once final implementation details are confirmed. Investors relying on manual calculations across multiple brokers face significant complexity in the transitional period until that clarity arrives.

The new regime’s effective tax cost is not incurred on unrealised gains sitting in a portfolio. It is incurred only at the point of realisation, the moment an asset is sold and a taxable event is triggered. This means the frequency with which an investor crystallises gains is the single most powerful variable they can control.

Index ETFs, by design, tend to trigger fewer taxable events than actively managed funds. An active manager buying and selling positions throughout the year generates a stream of realisation events that each attract CGT. A broad-market index ETF, by contrast, holds and tracks the index, realising gains primarily when index constituents change, a far less frequent occurrence. Industry research from the ASX, BetaShares, and Vanguard consistently demonstrates this lower-turnover characteristic, though no data updated for the 2026 CGT reform mechanics is yet available.

ETF portfolio turnover rates vary substantially even within the passive index category, with broad-market funds like VAS and VGS recording annual turnover of approximately 3-5% compared with 20-50% for actively managed funds, a gap that translates directly into fewer CGT realisation events and a structurally larger compounding base across 10-30 year holding periods under the new regime.

The distinction matters more under the new regime than it did under the old one. Each realisation event now attracts a higher effective tax rate at the margin. Early post-Budget commentary from Stockspot and Moore Australia confirms this directional assessment: low-turnover ETF strategies will become more valuable under the indexed regime.

Higher effective CGT rates under the new regime create a structural lock-in effect on portfolio rebalancing, discouraging asset sales even when the investment case for a position has weakened, which means investors who remain disciplined about not over-trading gain an advantage that goes beyond tax efficiency alone.

Consider the key differences through the lens of CGT drag specifically:

Each avoided taxable realisation is not simply a deferred cost. It is a compounding contribution to long-term after-tax wealth, because the unrealised gain remains in the portfolio, generating returns of its own.

No granular after-tax return comparison between ETFs and active funds under the new rules has been published as of mid-May 2026. However, the directional conclusion is clear: the reform amplifies the structural after-tax advantage of low-turnover investing at every holding period.

Understanding the problem is not enough. What follows are four specific tactics, each of which can be evaluated against an existing portfolio this week. None is new to tax-effective investing, but the 2026 reform increases the payoff from every one of them.

For investors who want to model the specific dollar difference that the widening CGT gap creates between superannuation and personal-name holdings, our full explainer on the super versus shares tax advantage works through a 25-year scenario where a 35-year-old investor accumulates approximately $230,000 more inside super than in a personal share portfolio, using after-tax return comparisons that now look even more conservative given the post-2027 minimum 30% floor on personal-name gains.

No published adviser playbook specific to these tactics under the new indexed CGT rules exists as of mid-May 2026. The strategies above represent author-synthesised guidance building on confirmed reform mechanics.

The table below illustrates how personal-name and superannuation CGT treatment diverge under the new regime:

| Structure | Current CGT Discount | Post-1 July 2027 Treatment |

|---|---|---|

| Personal name | 50% discount on nominal gain | Indexed cost base + 30% minimum effective floor |

| Superannuation fund | 33% (one-third) discount | 33% discount retained (unchanged) |

The period between now and 1 July 2027 is a distinct planning window. After that date, the new regime becomes the default, and the specific opportunity associated with the transitional split closes permanently for most investors.

Three actions warrant consideration before the window closes:

Two variables determine whether selling before 1 July 2027 is advantageous. The first is the size of the unrealised gain relative to the investor’s marginal tax rate. A large gain crystallised at the 50% discount may still produce a substantial tax bill, and the cash paid in tax is cash that no longer compounds.

The second variable is the likely inflation environment over the remaining holding period. In high-inflation scenarios, the indexed cost base under the new regime may reduce the taxable gain enough to make the new rules comparable, or even favourable, for some long-hold positions. Early realisation is not automatically the right answer.

The FSC fact sheet (released 15 May 2026) provides limited effective-tax-rate comparisons that can assist in evaluating specific scenarios. However, a final assessment for most investors requires waiting for exposure draft legislation to confirm the indexation methodology. Premature mass crystallisation of gains to “lock in” the old discount, without running the numbers, risks triggering a larger tax liability than the new regime would have imposed.

After several sections of mechanics and calibrated urgency, it is worth returning to first principles. The structural case for long-term, diversified, low-turnover investing is strengthened by this reform, not undermined by it. The new regime specifically rewards patience: holding assets longer allows more of the gain to be sheltered by indexation, while unnecessary realisations attract the 30% floor with less offsetting benefit.

The reform also reshapes the relative attractiveness of different ASX equity categories, with the removal of the CGT discount raising the after-tax value of fully franked dividend income compared with capital gains, driving an expected sectoral rotation toward franked dividend income in banks, telcos, utilities, and infrastructure stocks as investors recalibrate yield preferences under the new regime.

The reform remains a Budget proposal, not enacted law. No exposure draft or ATO guidance has been released as of mid-May 2026, and exposure drafts are expected before year-end. Investors should monitor the legislative process and avoid irreversible decisions until implementation details are confirmed. Chris Brycki, Founder and CEO of Stockspot, has reflected the broader industry position that remaining invested and diversified is likely to remain more important for most investors than reacting to short-term political or tax developments.

The Grattan Institute research on CGT discount reform provides an independent economic assessment of how the existing 50% discount shapes investment behaviour and wealth distribution, offering policy context that underpins the structural case for why the 2026 Budget changes were proposed and what long-term outcomes the new indexed regime is designed to achieve.

For complex situations, including business sales, trust structures, and transitional calculations involving large pre-1 July 2027 gains, professional advice is warranted. For the broader investor population, the foundational portfolio principles outlined in this guide apply.

Tax-efficient investing and sound long-term investing are, under the new regime, more aligned than they have ever been. The investors best positioned to preserve wealth are those who were already doing the right things: diversifying, minimising turnover, and letting compounding do its work.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The illustrative compounding models above use simplified assumptions and do not constitute projections of future returns. Past performance does not guarantee future results. The CGT reform discussed is a Budget proposal as of May 2026, not enacted legislation, and final rules may differ from the announced design.

From 1 July 2027, Australia's proposed CGT reform replaces the existing 50% discount on nominal gains with an indexed cost base system, meaning only real (inflation-adjusted) gains are taxed, but a minimum effective tax rate of approximately 30% applies regardless of the investor's marginal bracket.

Key strategies include using buy-only rebalancing to avoid triggering taxable realisation events, holding higher-growth assets inside superannuation (which retains its one-third CGT discount), harvesting tax losses to offset gains, and using low-turnover index ETFs that crystallise fewer taxable events each year.

No. Superannuation funds retain the existing one-third (33%) CGT discount under the proposed new regime, meaning the gap between personal-name and superannuation CGT treatment widens after 1 July 2027, making super a more valuable structure for holding growth assets.

For assets purchased before 1 July 2027 and sold after that date, the gain is split at the market value on 1 July 2027: the portion of the gain accrued before that date retains the 50% discount, while the portion accrued after is subject to the new indexation plus 30% floor.

Under the proposed rules, each time a gain is realised it attracts a higher effective tax rate, so investors who trade frequently will shrink their compounding base more often; low-turnover index ETFs, which trigger far fewer taxable events than actively managed funds, provide a structurally larger after-tax compounding base over 10-30 year holding periods.