The Senate confirmed Kevin Warsh as the next leader of the Federal Reserve on 13 May 2026, in a 54-45 vote that split almost entirely along party lines. Headlines treated the result as a inflection point for monetary policy. The more useful question is whether the institutional architecture of the Federal Open Market Committee (FOMC) allows it to be one. Warsh took office on 14 May, the day Jerome Powell’s term ended, inheriting a committee that held rates at 3.50-3.75% just two weeks earlier and is now navigating elevated inflation, Middle East energy uncertainty, and visible internal divisions. What follows is an examination of what a Fed chair transition actually changes, what it structurally cannot, and how to build a more durable framework for evaluating Fed-related market signals going forward.

What the Warsh confirmation actually means, beyond the vote count

The political texture of the vote was sharp. 54-45, with Senator John Fetterman (D-PA) as the sole Democratic crossover, made this one of the more partisan Federal Reserve confirmations in recent memory.

That partisanship, however, describes the Senate. It does not describe the Fed. A confirmation vote is a political event; the policy path that follows is determined by economic data, committee consensus, and institutional mandate. The two processes operate on different logics, and conflating them is one of the most common errors in Fed coverage.

- Senate vote: 54-45, 13 May 2026

- Democratic crossover: Senator John Fetterman (D-PA)

- Warsh took office: 14 May 2026, the day Powell’s term ended

- First FOMC meeting as chair: 16-17 June 2026 (includes Summary of Economic Projections and dot plot)

The article that follows is built on a single analytical tension: media coverage of leadership transitions routinely overstates the policy significance of who chairs the Fed. The institutional design exists precisely to prevent one person from redirecting monetary policy on the basis of personal preference.

When big ASX news breaks, our subscribers know first

How collective decision-making constrains any incoming chair

The FOMC makes rate decisions through a 12-voting-member committee, not through the chair alone. This is not a procedural footnote. It is the central architectural feature of American monetary policy, deliberately designed to distribute authority and constrain individual influence.

The FOMC voting structure and dual mandate, as defined by the Federal Reserve itself, establish that the committee rotates voting rights among Reserve Bank presidents while the Board of Governors members hold permanent votes, a design that ensures no single chair can dominate policy outcomes regardless of personal conviction.

Three institutional anchors limit what Warsh, or any chair, can unilaterally change:

Powell’s continued board presence through 2028, after stepping down as chair on 15 May 2026, introduces an unusual internal dynamic: a former chair retains a vote on the committee his successor now leads, a configuration without modern precedent that could affect policy cohesion during Warsh’s early months.

- Collective voting structure: Policy decisions require committee consensus. The chair sets the agenda and leads the press conference, but cannot outvote the committee.

- Codified 2% inflation target: Any chair who openly adopted a higher inflation tolerance would need full committee agreement to operationalise it. The target is not advisory; it is the committee’s stated policy framework.

- Established operating framework: The “ample reserves” operating framework remains broadly supported. A 2026 survey of Fed watchers found significant backing for maintaining it, signalling a preference for continuity regardless of who chairs the committee.

“Some surprises are the inevitable result of news about the policy outlook.” — San Francisco Fed Economic Letter, March 2026

That framing, from the Fed’s own research arm, acknowledges that even transparent communication produces market surprises. It also implies the inverse: the structure is designed to minimise surprises that stem from individual leadership rather than from genuine shifts in the economic outlook.

One additional finding from the 2026 Fed watcher survey deserves attention. Approximately one-third of respondents said Board members and Reserve Bank presidents should speak less frequently, reflecting concern that too much individual commentary fragments the committee’s message. Warsh inherits a communication environment where the volume of Fed voices is itself a source of noise.

The policy baseline Warsh inherits, and why it is not a blank slate

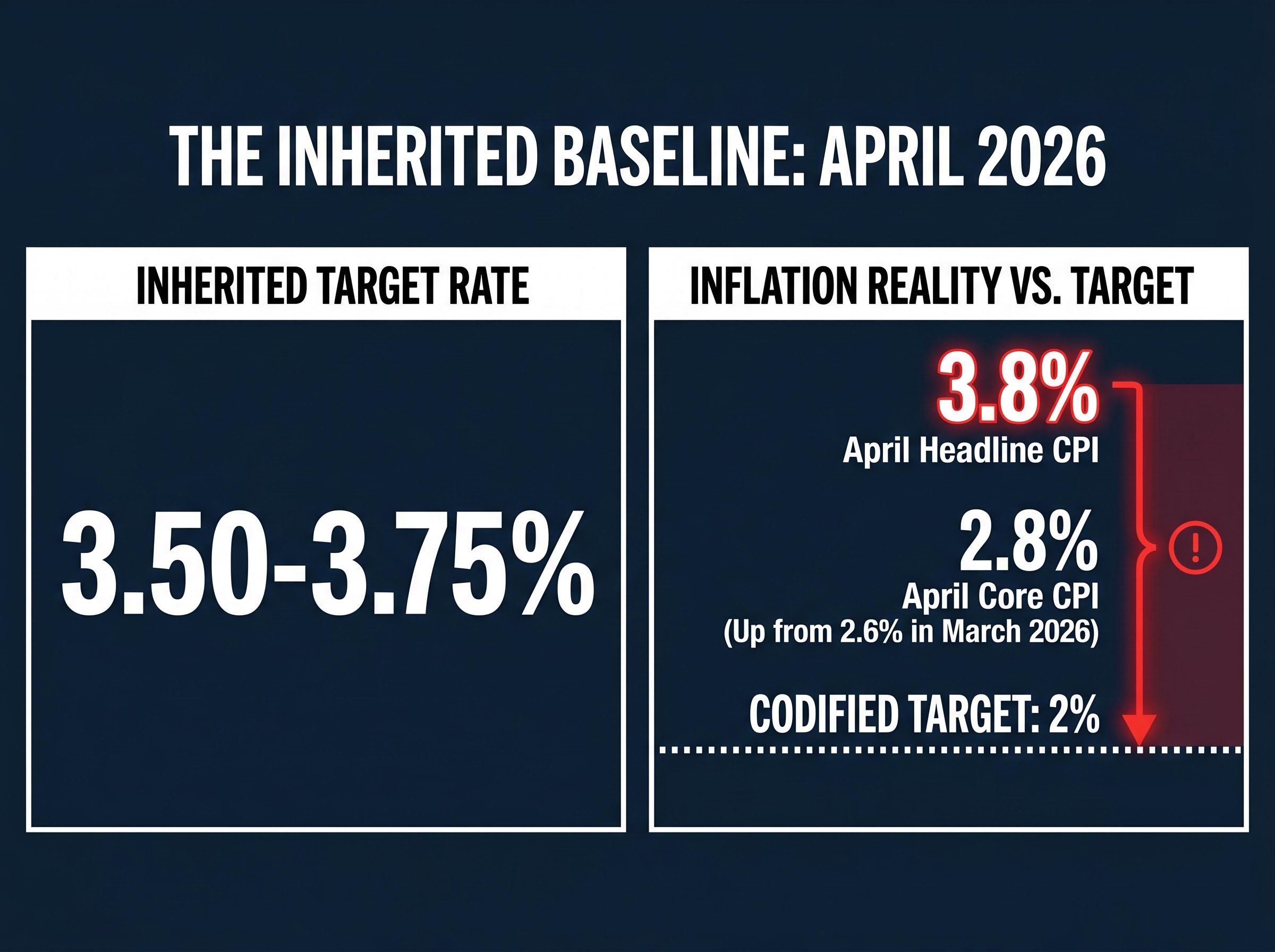

The real policy handoff document is not the Senate vote. It is the 29 April 2026 FOMC statement, which set the conditions Warsh walks into on his first day.

The April 29 FOMC decision to hold at 3.50-3.75% was itself a product of a committee already fracturing under dual-mandate pressure, with PCE inflation at 3.5% and unemployment rising to 4.3% simultaneously pulling in opposite directions, a conflict that rate tools are structurally unable to resolve without trade-offs.

That statement held the federal funds target range at 3.50-3.75%, characterised the economy as “expanding at a solid pace,” and acknowledged that “inflation is elevated, in part reflecting the recent increase in global energy prices.” The committee maintained an easing bias in its forward guidance, signalling that the next move, when it comes, is more likely to be a cut than a hike.

The inflation data complicates that bias. April headline CPI came in at 3.8% year-over-year, the highest reading since May 2023. Core CPI rose to 2.8%, up from 2.6% in March 2026. The gap between a 2% target and a 3.8% headline print is the kind of tension that shapes meetings more than any chair’s personal disposition.

A divided committee before Warsh chaired a single meeting

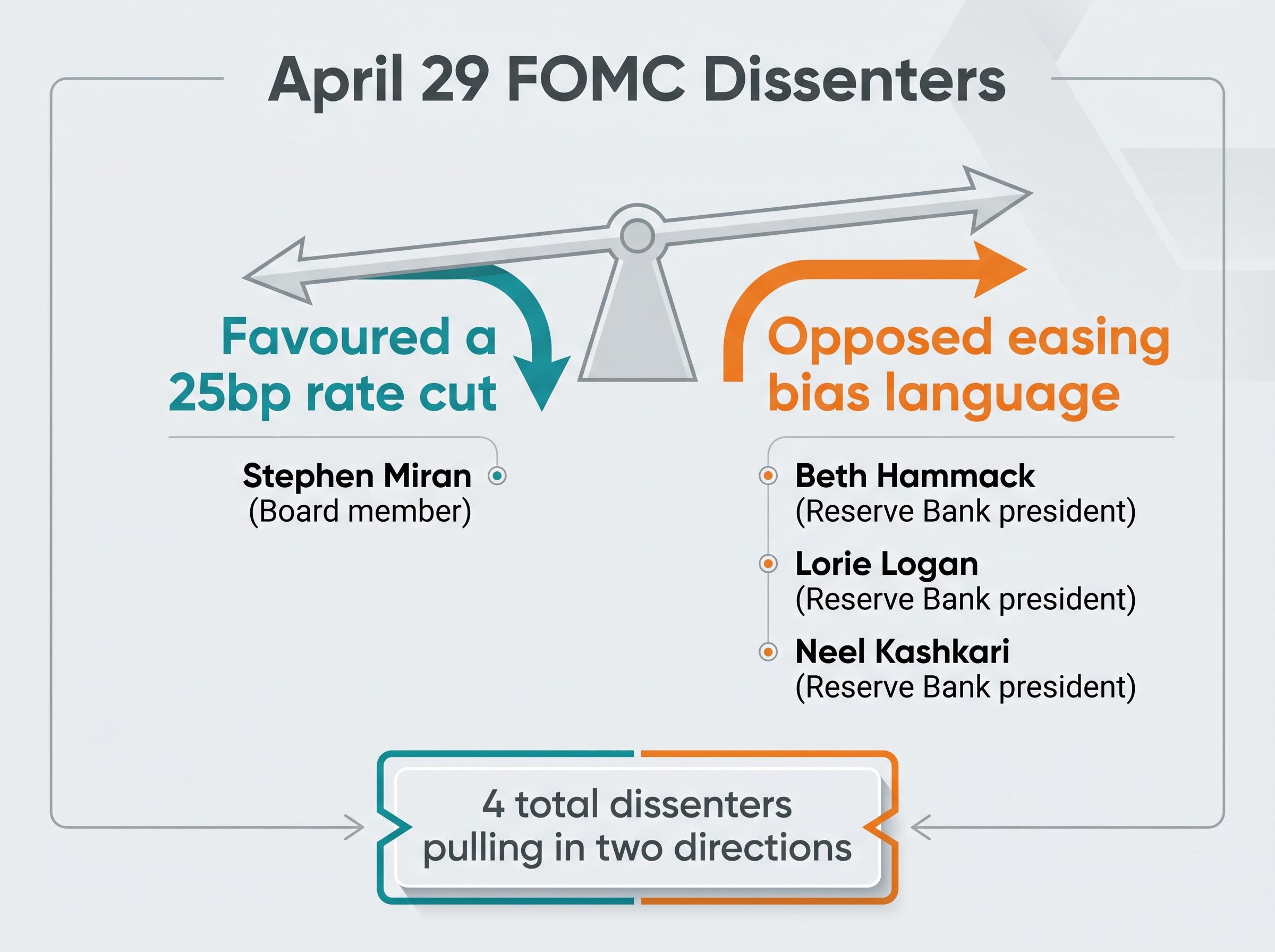

The 29 April decision produced four dissenters, an unusually large bloc that reveals the committee fractures Warsh must manage from day one.

| Dissenter | Role | Position |

|---|---|---|

| Stephen Miran | Board member | Favoured a 25bp rate cut |

| Beth Hammack | Reserve Bank president | Opposed easing bias language |

| Lorie Logan | Reserve Bank president | Opposed easing bias language |

| Neel Kashkari | Reserve Bank president | Opposed easing bias language |

These are not dissents in the same direction. Miran wanted to cut. Hammack, Logan, and Kashkari wanted to remove the language suggesting a cut was coming. Warsh inherits a committee pulling in two directions simultaneously, which constrains his early degrees of freedom considerably. The 16-17 June meeting, his first as chair, will be the first moment where any shift in tone or reaction function becomes visible, making the dot plot and press conference the confirmation hearing that actually matters for markets.

What pre-appointment positioning fails to predict about actual policy

What a Fed chair nominee says before confirmation is a weak predictor of what they do in the role. This is not a speculative claim; it is a documented pattern.

The structural reasons are straightforward:

- The data environment shifts after confirmation. A nominee testifies based on the economic conditions visible during the nomination process. By the time they chair their first meeting, the data may have moved.

- Committee dynamics reshape individual stances. A chair who arrives with strong personal views on inflation tolerance or rate trajectory encounters 11 other voting members with their own assessments, staff forecasts, and regional economic data.

- Mandate obligations override personal preferences. The dual mandate, maximum employment and 2% inflation, is not optional. It constrains every chair regardless of pre-appointment rhetoric.

Powell himself illustrates the point. Originally nominated by President Trump in 2017, his tenure spanned aggressive rate hike cycles, emergency cuts to near zero, and a complete reversal of balance sheet policy. One chair’s actual decisions can span the full policy spectrum when the data demands it.

Warsh’s preference for a rules-based policy framework, favouring Taylor Rule-style rate decisions over the discretionary, forward-guidance-heavy approach that characterised the Powell era, represents a procedural departure that may matter more for committee dynamics than any single rate decision.

“The Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” — FOMC Statement, 29 April 2026

That language is the operating principle Warsh inherits. It is also the principle that renders pre-confirmation positioning secondary to the data environment a chair encounters once seated.

What to actually watch in the months ahead

The earlier sections dismantled the wrong framework. This section constructs the right one.

Three specific signals will reveal more about Warsh’s chairmanship than the confirmation vote or any pre-appointment commentary:

- Warsh’s 16-17 June press conference tone on inflation tolerance. The first press conference is not a binary hawkish or dovish verdict. It is a baseline. How Warsh characterises the 3.8% headline CPI reading, whether he frames it as transitory energy pass-through or as a more persistent concern, will establish his reaction function for the meetings that follow.

- The dot plot distribution relative to the April 29 inherited baseline. The June Summary of Economic Projections will be the first dot plot under new leadership. Shifts in the median dot, and especially in the dispersion of individual projections, will signal whether the committee’s rate expectations are converging or diverging under Warsh’s early tenure.

- Whether the dissent coalition expands or contracts. Four dissenters in April is an elevated number. If the June decision produces fewer dissents, it would suggest Warsh is building consensus. If the bloc holds or grows, the committee remains fractured regardless of who chairs it.

The San Francisco Fed’s own research found that transparent, predictable communication “reduces unnecessary volatility.” That finding is the benchmark against which Warsh’s communication style will be assessed, not by markets alone, but by the Fed’s own institutional standards.

Rate-sensitive asset classes, including long-duration Treasuries, REITs, and utilities, face the sharpest repricing risk when forward guidance loses its market-calming authority, and a committee this fractured produces forward guidance that markets discount more heavily than usual.

How economic fundamentals absorb the distraction of a chair transition

The Warsh confirmation arrived on the same day as the Trump-Xi Beijing summit (13-14 May 2026), which covered tariffs, semiconductors, rare earths, Taiwan, and artificial intelligence. April CPI had already printed at 3.8%. The FOMC’s own characterisation of the economy as “expanding at a solid pace” remained the baseline.

The chair transition, in other words, was one variable among several that markets were simultaneously pricing:

- Trump-Xi summit covering trade, technology, and geopolitical flashpoints

- April CPI at 3.8% headline and 2.8% core, both above the Fed’s 2% target

- Ongoing Middle East energy price dynamics feeding through to inflation readings

Markets have historically climbed what is sometimes described as a “wall of worry,” where recurring anxieties, including Fed leadership transitions, inflation fears, and central bank independence concerns, feature as persistent background noise rather than reliable signals of reversal.

The analytical principle at work is straightforward. Real economic outcomes relative to investor expectations, not inflation readings or Fed chair identity in isolation, are the primary driver of equity market direction. Sound economic fundamentals do more structural work in determining where markets go than any single personnel change at the central bank.

Reading Fed transitions through a data-first lens

The FOMC’s collective design, codified targets, and data-dependent mandate mean that chair transitions produce far less policy discontinuity than media coverage implies. This has been the pattern across multiple transitions, and there is no structural reason to expect the Warsh era to break it.

His first real test is 16-17 June 2026. The signals worth watching are the press conference tone, the dot plot distribution, and the committee dissent pattern. The inherited conditions are specific: a 3.50-3.75% target range, 3.8% headline inflation against a 2% codified target, and a four-member dissent bloc that predates his chairmanship.

The reusable principle is simple. Evaluate Fed developments by what the data environment is doing and how the full committee is responding, not by who is chairing the press conference. The institution is designed to outlast any individual occupant. The analytical framework should be, too.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—