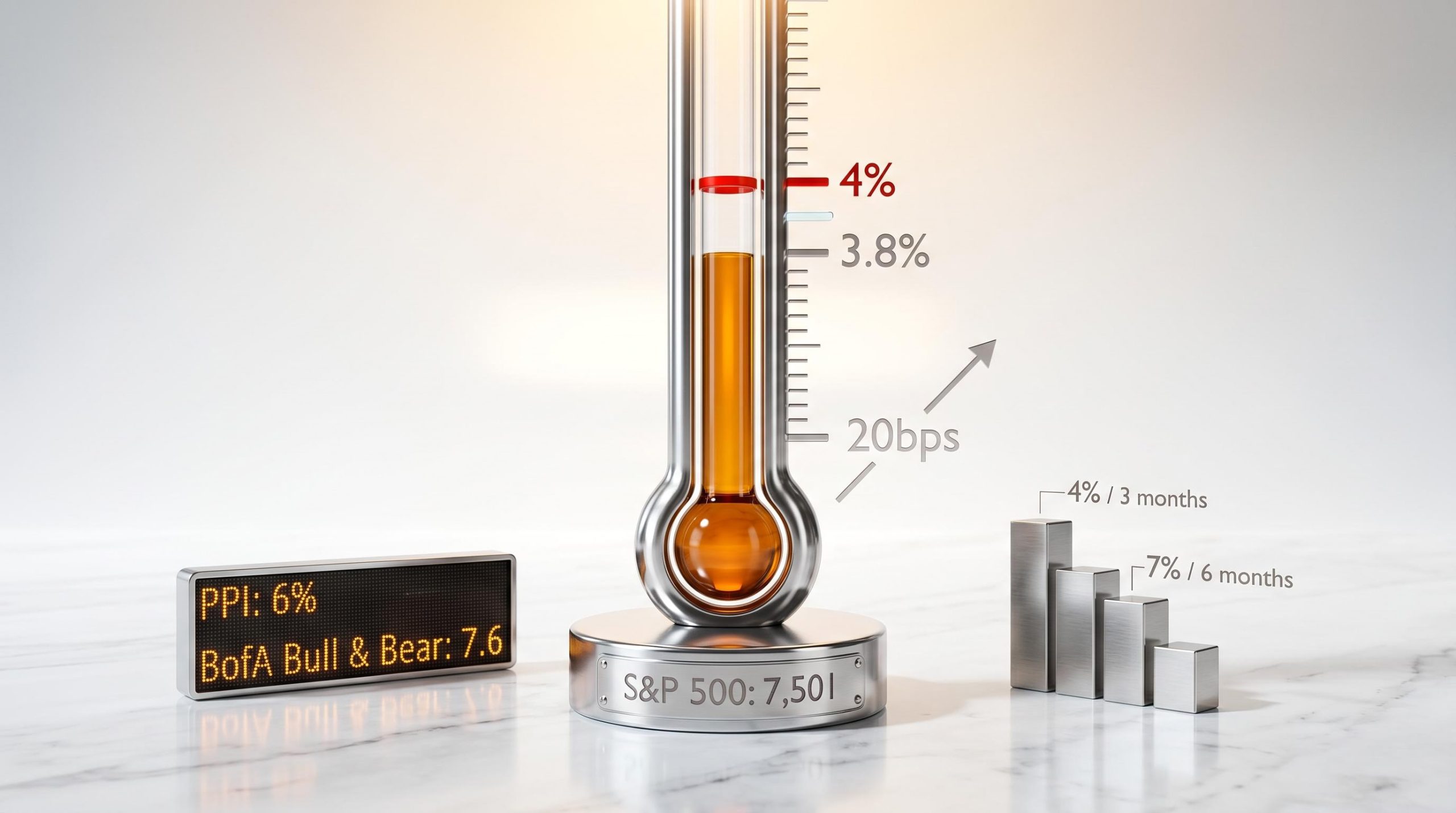

With headline CPI at 3.8% and the Philadelphia Semiconductor Index trading 62% above its 200-day moving average, the U.S. equity market is sitting at an unusual intersection: stretched valuations and inflation approaching the precise threshold where history says returns tend to deteriorate. Bank of America Chief Investment Strategist Michael Hartnett has flagged that if current monthly price pressures persist, CPI could breach 5% by the November 2026 midterm elections. Producer prices are already running at 6%. The Federal Reserve’s new chair, Kevin Warsh, confirmed on 13 May 2026, is inheriting a policy environment where the next CPI print could meaningfully shift market expectations. The S&P 500 stands at 7,501, up roughly 4% year-to-date, resilient but exposed. What follows lays out what the historical data actually shows about equity performance once CPI crosses 4%, explains the mechanical reasons inflation erodes stock valuations, and translates that into a practical framework for thinking about portfolio exposure as the threshold approaches.

The 4% line: what BofA’s historical data actually shows

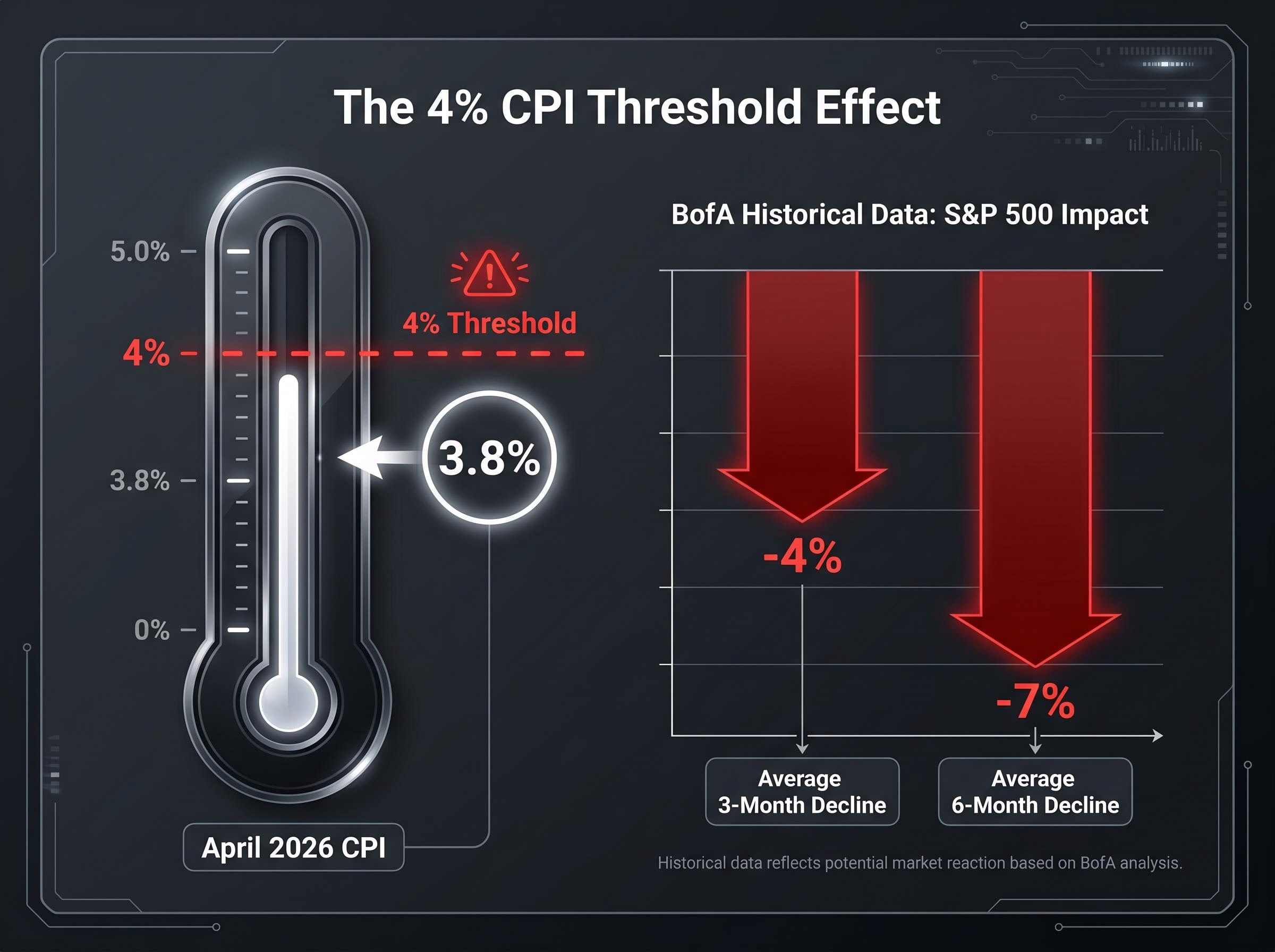

The finding is straightforward, and that is what makes it uncomfortable. According to Bank of America research led by Hartnett, once U.S. headline CPI has crossed 4%, the S&P 500 has historically declined an average of 4% over the subsequent three months and 7% over the following six months.

Historically, once U.S. CPI surpasses 4%, the S&P 500 has declined an average of 4% over the subsequent three months and 7% over the following six months.

These are not worst-case scenarios. They are averages, the baseline outcome across multiple inflationary episodes. The drawdowns encompass periods where earnings held up and periods where they did not, periods of Fed tightening and periods of policy uncertainty.

The April 2026 CPI release from the Bureau of Labor Statistics on 12 May 2026 put headline inflation at 3.8%. Producer prices, often a leading indicator of where consumer prices head next, are running at 6%. The 4% threshold is not a distant hypothetical. It is 20 basis points away.

The April CPI print, which came in at double the consensus monthly forecast of +0.3%, showed broad-based price acceleration across shelter, core services, goods, food, and energy simultaneously, removing the possibility of characterising the upside surprise as isolated to a single category.

| CPI Threshold | Subsequent 3-Month S&P 500 Return | Subsequent 6-Month S&P 500 Return |

|---|---|---|

| Above 4% | -4% (average) | -7% (average) |

When big ASX news breaks, our subscribers know first

Why inflation erodes stock valuations: the mechanics behind the numbers

Most investors understand that stocks tend to fall when inflation rises. Fewer can trace the causal chain that explains why.

The sequence begins with the consumer price index itself. When CPI moves above the Federal Reserve’s 2% target and stays there, the central bank faces pressure to keep real interest rates elevated, meaning rates that are meaningfully above the inflation rate. The Fed’s current stance under newly confirmed Chair Kevin Warsh remains data-dependent, with rates held steady pending inflation’s trajectory.

Higher real rates feed directly into how the market values future corporate earnings. Every share price reflects a discounted stream of expected profits. When the discount rate rises, the present value of those future profits falls, and price-to-earnings multiples compress. Goldman Sachs Asset Management has noted that equity valuations are most vulnerable when inflation is above 3-4% and the Fed keeps policy rates restrictive for longer.

The transmission mechanism works in three steps:

- CPI rises and remains persistently above the Fed’s target

- The Fed holds or raises real interest rates to contain price pressures

- Higher discount rates compress P/E multiples across the equity market

BlackRock Investment Institute frames the exposure similarly: when inflation is persistently above target, equity risk premia compress and rate-sensitive, highly leveraged parts of the market face the most pressure.

The pricing power divide

The discount rate mechanism hits all equities, but not equally. Companies with durable pricing power, those with strong brands, provision of services with inelastic demand, or control of unique inputs, can pass rising costs through to customers. Their margins hold. Their earnings estimates remain intact even as the discount rate rises.

Companies without that power face a compounding problem. Input costs climb faster than revenues, squeezing earnings at exactly the moment the market is applying a higher discount rate to whatever earnings remain. Goldman Sachs Asset Management distinguishes between profitable mega-cap growth with strong cash flows, which can remain resilient, and unprofitable growth or long-duration names, which sit at the sharp end of both the earnings squeeze and valuation compression.

Where Hartnett’s 5% scenario comes from and why it matters

Hartnett’s projection that CPI could exceed 5% by November 2026 is not a consensus forecast. It is a conditional risk scenario, and understanding its internal logic is what makes it useful.

The argument rests on trajectory. If monthly CPI gains continue at their recent pace without meaningful deceleration, the cumulative path points to 5% or above by the midterm elections. The 6% PPI reading as of May 2026 strengthens the case: producer prices running well ahead of consumer prices historically signals upstream cost pressure that eventually feeds through to the retail level.

Upstream cost pressures have been building since the Strait of Hormuz closure removed roughly 20% of global oil supply, with Bank of America estimating a 1.0 percentage point addition to headline CPI from the prolonged disruption alone, a figure that sits independently of the domestic services and shelter inflation already embedded in the index.

CPI could exceed 5% by the November 2026 midterm elections if recent monthly inflation trends do not slow significantly.

The scenario’s value lies not in its certainty but in its interaction with current market positioning. Three signals are converging:

- PPI at 6%, indicating persistent upstream cost pressure

- BofA Bull and Bear indicator at 7.6, approaching the 8.0 sell signal threshold

- SOX index trading approximately 62% above its 200-day moving average, reflecting stretched sentiment in the semiconductor space

This combination leaves little margin for upside inflation surprises. The risk asymmetry is unfavourable: if Hartnett is wrong and inflation moderates, markets have already priced in much of the optimism. If he is right and CPI breaches 4% or reaches 5%, the historical data suggests a drawdown that current positioning is poorly hedged against.

How different equity sectors respond when inflation re-accelerates

Inflation does not hurt all equities equally. The historical pattern is well documented, and April 2026 data is already confirming it in real time.

Energy, materials, and financials tend to outperform in high-inflation regimes. Energy revenues are directly tied to commodity prices, which rise with inflation. Financials benefit from higher interest rates through wider net interest margins. Materials companies see the value of their inventories and output rise with producer prices.

Long-duration growth and unprofitable technology sit at the other end. The discount rate mechanism outlined above hits these names hardest, as their valuations are weighted toward distant future earnings that shrink in present-value terms when rates rise.

J.P. Morgan Asset Management’s April 2026 review provides a live illustration: commodities gained 4.2%, energy gained 7.7%, and industrial metals gained 5.0%. In the same month, rising yields pressured government bonds and weighed on rate-sensitive segments. Infrastructure funds recorded a record $1.5 billion in weekly inflows for the week ending 15 May 2026, reflecting rotation into real-asset-linked positions.

| Sector | Inflation Sensitivity | April 2026 Performance | Positioning Implication |

|---|---|---|---|

| Energy | Positive: revenues tied to commodity prices | +7.7% | Overweight as inflation hedge |

| Materials / Industrials | Positive: input and output prices rise | +5.0% (industrial metals) | Overweight for real-asset exposure |

| Financials | Positive: higher rates widen margins | Beneficiary of rising yields | Selective overweight |

| Technology / Growth | Negative: discount rate compression | Under pressure from rising yields | Distinguish profitable from unprofitable |

The technology tension

Technology sector funds still took in $5.4 billion in weekly inflows (the largest since February 2026), driven primarily by AI-related earnings momentum. This creates a visible tension: money is flowing into the sector most mechanically exposed to inflation risk.

The distinction matters. BlackRock and Goldman Sachs Asset Management both flag profitable mega-cap technology with strong free cash flow as a partial exception to the standard inflation-hurts-growth pattern. These companies generate enough near-term cash to withstand discount rate pressure. Unprofitable or long-duration names, where the entire valuation rests on earnings years into the future, do not share that resilience.

Sector divergence during inflationary episodes is not purely mechanical; the AI infrastructure buildout by Amazon, Alphabet, Meta, and Microsoft has created a semiconductor supercycle that partially insulates profitable mega-cap technology from the discount rate pressure that hits unprofitable long-duration names in the same sector classification.

Building a portfolio framework for a world where CPI hits 4% or higher

The analytical framework built across this piece points toward a specific set of portfolio responses, and the consensus among major asset managers reinforces them.

BlackRock, J.P. Morgan Asset Management, and Goldman Sachs Asset Management converge on a multi-asset framework: quality large caps, Treasury Inflation-Protected Securities (TIPS, which are U.S. government bonds whose principal adjusts with CPI), shorter-duration bonds, and real-asset exposure form the core response to inflation above 4%.

TIPS are particularly relevant at this juncture. With CPI at 3.8%, inflation protection remains relatively affordable compared to what it would cost after a breach of 4%. Gold attracted $2.0 billion in weekly inflows for the week ending 15 May 2026, signalling that institutional capital is already positioning for further inflation risk.

Investors wanting to translate this framework into specific position sizing and asset class weights will find our dedicated guide to inflation tactical allocation, which maps TIPS, REITs, physical gold, and quality equity screens into a structured portfolio response to the current macro crosscurrents, including the disinflationary counterweight that AI productivity gains may provide over a longer horizon.

Goldman Sachs Asset Management frames the equity side as a barbell:

- One side: Profitable mega-cap growth with pricing power and strong cash flows

- Other side: Value and real assets with commodity linkage (energy, materials, infrastructure)

| Asset Class | Positioning Rationale |

|---|---|

| Quality equities | Strong margins and pricing power protect earnings through inflation |

| Value and cyclicals | Outperform when inflation is high but growth remains solid |

| TIPS | Direct CPI-linked protection; more affordable before threshold breach |

| Short-duration bonds | Limit price losses as yields rise on inflation expectations |

| Commodities and resource equities | Revenues rise with the same prices driving CPI higher |

| Infrastructure and select REITs | CPI-linked cash flows provide structural inflation protection |

| Avoid / underweight | Unprofitable growth, long-duration story stocks, highly levered small caps |

The 3.8% moment: what investors should be watching right now

The S&P 500 closed at 7,501.24 on 14 May 2026, up approximately 4% year-to-date. The BofA Bull and Bear indicator sits at 7.6, within striking distance of the 8.0 level that has historically triggered sell signals. Core CPI at 2.8% offers some distinction from the more elevated headline figure, but the gap between headline and core is narrowing.

Genuine uncertainty remains. The 5% scenario is a risk projection, not a certainty. Warsh’s Fed may respond differently to inflation than its predecessor. Strong earnings, particularly in AI-linked technology, are providing a real counterweight to inflation pressure.

Four forward-looking signals deserve close attention in the weeks ahead:

- Monthly CPI and PPI releases, which will determine whether the 4% threshold is breached

- FOMC meeting outcomes under Warsh, for signals on the “higher for longer” policy path

- The BofA Bull and Bear indicator relative to the 8.0 sell signal

- Sector rotation signals, particularly whether capital continues flowing from growth into energy and real assets

The distance between 3.8% and 4% may appear small. The historical evidence suggests it is not. Acting before the threshold is crossed gives investors more options than acting after.

At 3.8% and rising, the historical playbook is already in play

The 4% CPI threshold is not an arbitrary level flagged for attention. It is a historically documented inflection point where average S&P 500 returns turn negative over both three-month and six-month horizons. At 3.8%, the current reading places investors within a single report of that line.

The rotation that historical data would predict is already visible. April 2026 sector returns and weekly fund flows show capital moving toward energy, commodities, and infrastructure while small caps and speculative growth face pressure. The market is beginning to price the inflation scenario without having fully reckoned with it.

Whether CPI reaches 4%, 5%, or moderates from here, the analytical framework for evaluating inflation risk against equity exposure remains the same: quality over leverage, real assets over duration, pricing power over hope. That framework is best applied before the threshold is crossed, not after.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.