Woolworths: Strong Sales, Shrinking Profits, Slim Upside

2 hrs ago

CSL Limited was once the ASX’s closest thing to a guaranteed compounder. Today, the stock trades at roughly half the earnings multiple it commanded three years ago, after shedding more than 43% of its value since January 2026 alone. The sell-off is not a single-event story. It is the product of a sequence of earnings misses, a guidance downgrade, a US$5 billion impairment charge, and growing institutional doubt about whether the business model that made CSL a byword for quality still functions as advertised. For Australian investors, this raises a question that is simultaneously obvious and genuinely difficult: is this a once-in-a-decade buying opportunity in a world-class healthcare franchise, or a value trap wearing a familiar blue-chip label? What follows is a structured analytical framework covering what CSL’s three divisions actually do, how its financial metrics benchmark against blue-chip standards, what the valuation de-rating means in practice, and where the honest uncertainty lies for those considering an entry at current levels.

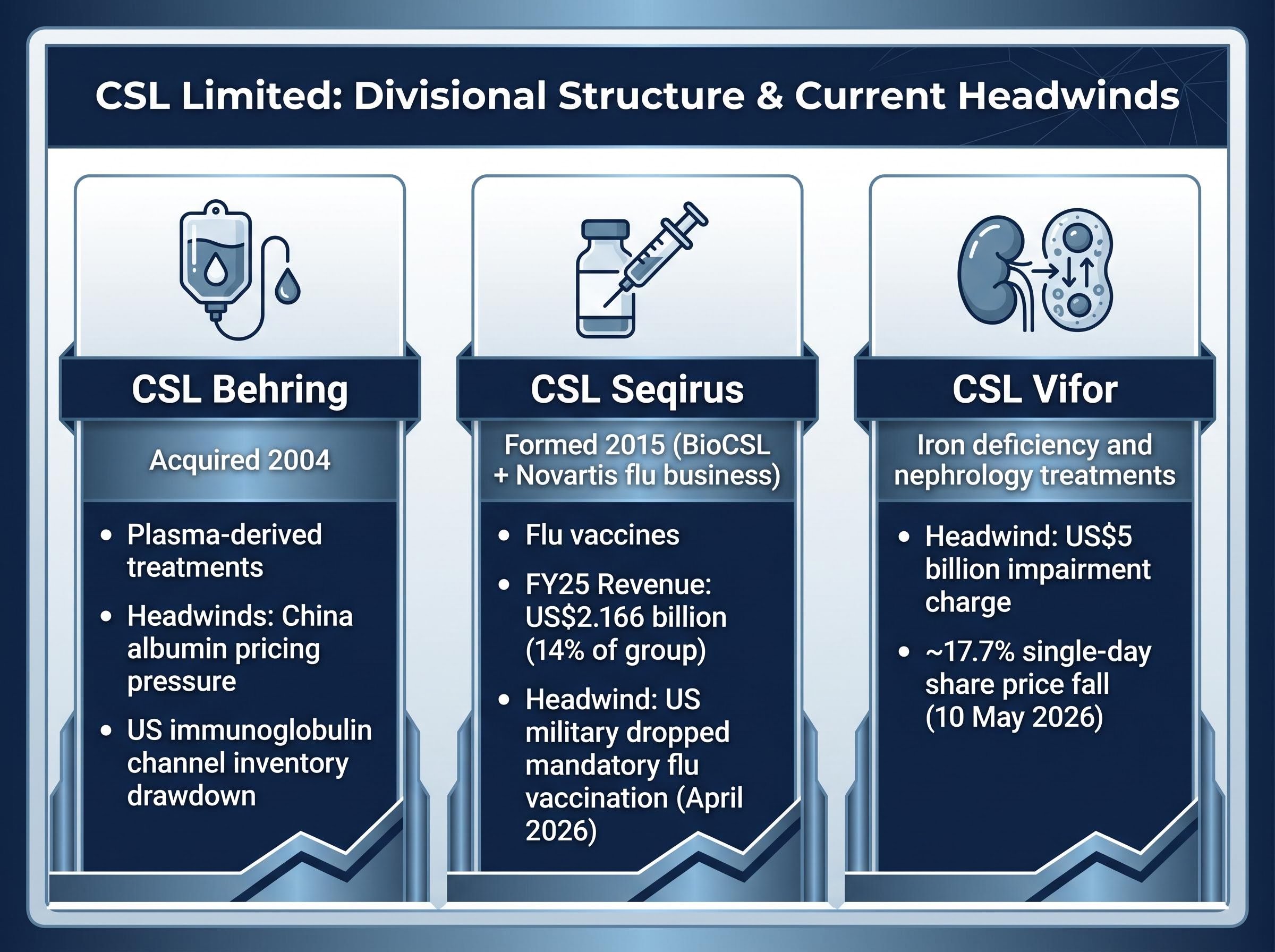

CSL operates through three distinct divisions, each with its own economics, competitive dynamics, and risk profile:

Australian investors who buy CSL are buying exposure to three distinct healthcare economics, not a single business. The risk profile of each is currently behaving very differently, and understanding that structure prevents misreading the headline sell-off as uniform.

CSL’s sell-off did not occur in isolation: the ASX healthcare sector rout of the past 12 months reflects five compounding forces including RBA rate hikes, AUD appreciation, and corporate governance failures, with CSL’s approximately 45% weighting in the sector index meaning its own de-rating mechanically dragged the entire index to a six-year low.

| Division | Core Function | FY Contribution Note | Key Headwind Summary |

|---|---|---|---|

| CSL Behring | Plasma-derived therapies for serious and rare diseases | Largest revenue contributor (majority of group total) | China albumin pricing pressure; US immunoglobulin inventory normalisation |

| CSL Seqirus | Influenza vaccines and pandemic preparedness | FY25 revenue US$2.166b (~14% of group) | US military drops mandatory flu vaccination; post-COVID revenue volatility |

| CSL Vifor | Iron deficiency and nephrology treatments | Not separately broken out in accessible sources | Underperformance vs acquisition expectations; US$5b impairment |

Mature healthcare companies like CSL are best evaluated on return on equity (ROE), which measures how effectively a company turns shareholders’ capital into profit, alongside leverage and dividend yield, rather than the revenue-growth metrics applied to earlier-stage businesses. These are the metrics that separate enduring franchise value from momentum.

| Metric | CSL FY24 Figure | Blue-Chip Benchmark Context |

|---|---|---|

| Return on Equity | ~14.6% | Above the 10% threshold generally considered satisfactory for established companies |

| Debt-to-Equity | ~62.8% | Moderate leverage; equity exceeds total debt |

| Dividend Yield (5-yr avg) | 1.5% | Below ASX blue-chip averages, consistent with reinvestment-focused model |

| Forecast ROE FY28 | ~17.4% | Would represent a meaningful recovery from current levels (Simply Wall St, 13 May 2026) |

CSL’s FY24 ROE of approximately 14.6% clears the blue-chip threshold, even if it sits below the company’s own historical peak. Leverage remains moderate. The five-year average dividend yield of 1.5% is low by ASX income-stock standards, but consistent with a franchise that has historically reinvested aggressively.

The post-impairment balance sheet picture is materially different from the pre-announcement figures: the US$5 billion Vifor write-down will compress reported equity and make the pre-impairment debt-to-equity ratio of 62.8% understated once the post-impairment balance sheet is formally disclosed, a consideration that changes leverage calculations for those using current figures.

The critical nuance is this: FY26 guidance represents a real step down in underlying earnings, not purely an accounting event. Management’s own NPATA guidance of approximately US$3.1 billion compares to FY25 actuals of approximately US$3.3 billion.

The FY26 statutory loss of approximately US$648 million is a reported figure incorporating non-recurring impairment costs. NPATA guidance of approximately US$3.1 billion reflects actual operating performance. The distinction between accounting impairment and operating deterioration is one of the most practically significant calls an investor needs to make here.

Consensus forecasts ROE recovering toward approximately 17.4% by FY28, according to Simply Wall St data updated 13 May 2026. Whether that recovery materialises depends on the divisional headwinds examined below.

CSL Behring faces a dual squeeze. In China, albumin pricing has compressed, directly impacting the division’s margin profile in one of its largest growth markets. In the United States, immunoglobulin channel inventory normalisation is suppressing near-term revenue. Channel inventory normalisation means distributors are drawing down existing stock rather than ordering new product, so even if end-patient demand remains stable, reported revenue falls until the excess inventory clears. Management explicitly cited both pressures when announcing the FY26 guidance downgrade.

CSL Seqirus took a specific hit in April 2026, when the US military dropped its mandatory flu vaccination policy. For a division generating US$2.166 billion in FY25 revenue (approximately 14% of group total), the loss of a large institutional buyer compounds a broader concern: vaccine revenue has proved more volatile post-COVID than the market previously assumed.

The US military’s decision to end mandatory flu vaccination, confirmed in AP News reporting on the Pentagon policy change, removed a significant institutional buyer from the influenza vaccine market at a moment when Seqirus could least absorb the revenue shortfall.

| Division | Primary Headwind | Nature of Headwind |

|---|---|---|

| CSL Behring | China albumin pricing; US IG channel inventory drawdown | Cyclical / Uncertain |

| CSL Seqirus | US military drops mandatory flu vaccination (April 2026) | Structural (policy-driven) |

| CSL Vifor | US$5b impairment; underperformance vs acquisition expectations | Structural / Uncertain |

| Group-level | FY26 guidance cut; management credibility erosion | Reputational / Ongoing |

Vifor’s problems sit in a different category. The US$5 billion impairment charge, which triggered an approximately 17.7% single-day share price fall on 10 May 2026, is not purely an operational concern. It raises direct questions about management’s acquisition judgement. The iron deficiency and nephrology pipeline has not delivered the growth re-rating that justified the acquisition premium, and the impairment has damaged market credibility beyond the dollar value of the write-down itself.

At the group level, FY26 revenue guidance of approximately US$15.2 billion compares to FY25 actual revenue of approximately US$15.6 billion. The cumulative weight is what matters: three divisions, each under distinct pressure, with no single catalyst visible to resolve all three simultaneously.

CSL currently trades at approximately 14.2x forward earnings, based on consensus FY27 EPS forecasts and a share price near A$97. For most of the 2010s and into the early 2020s, CSL commanded a forward price-to-earnings ratio (P/E), the share price divided by expected earnings per share, of 25-30x or higher. The stock has broadly halved its valuation multiple.

That compression is large enough to attract value-oriented capital on its own. It is also large enough to reflect a genuine reassessment of the business rather than pure sentiment.

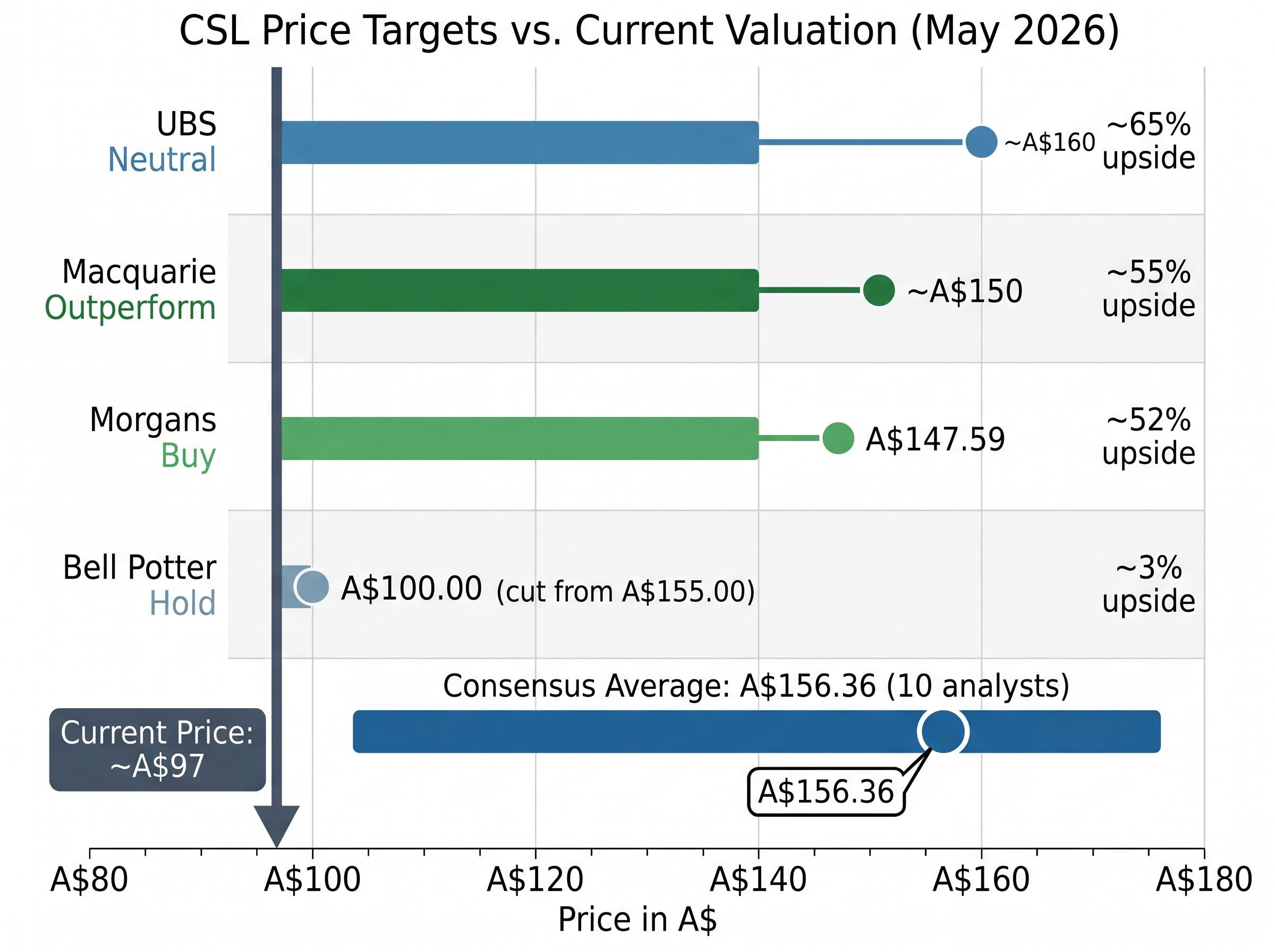

| Broker | Rating | Price Target (A$) | Implied Upside from ~A$97 |

|---|---|---|---|

| Morgans | Buy | $147.59 | ~52% |

| UBS | Neutral | ~$160 | ~65% |

| Macquarie | Outperform | ~$150 | ~55% |

| Bell Potter | Hold | $100.00 | ~3% |

The consensus average price target across 10 analysts sits at approximately A$156.36, according to TipRanks data from May 2026. Morgans characterises the operational problems as “primarily executional rather than structural,” retaining a Buy rating with approximately 50% implied upside. Bell Potter sees it differently.

“We think a discount is warranted for CSL considering the declining underlying earnings outlook across FY26-27, the lack of stable management, and series of credibility hits following several disappointing results/trading updates,” Bell Potter stated, cutting its price target from A$155.00 to A$100.00.

The gap between A$100 and A$160 is not noise. It reflects a genuine analytical dispute about whether CSL’s problems are temporary execution failures or durable structural shifts. At 14.2x forward earnings, CSL now trades broadly in line with global plasma and healthcare peers such as Grifols and Takeda, rather than at the clear premium it maintained for the better part of a decade.

The bull-versus-bear tension on CSL can be reduced to two specific questions. The first is about earnings trajectory. The second is about trust.

The bull case rests on recovery:

One material positive not captured in the bearish consensus narrative is the plasma therapy tariff exemption granted under the US Section 232 pharmaceutical proclamation, which protects CSL Behring’s highest-value US revenue stream from import duties effective September 2026 and directly reduces one tail risk that had been priced into the stock.

The bear case rests on structural damage:

A fallen blue chip becomes a value trap when the multiple compression is permanent: when the earnings power that justified the old valuation does not return, and a lower price alone cannot compensate for lower future returns. Multiple compression is not reversed by price falling alone. It requires demonstrated earnings recovery and restored market trust.

For CSL specifically, the stock needs NPATA to bottom, predictability to return, and capital allocation discipline to be re-established, not merely a lower entry price. If plasma and vaccine economics have shifted structurally and management credibility cannot be rebuilt, the 14x forward P/E may not be cheap relative to the underlying earnings power of the business going forward.

At current levels, an investor is buying a franchise with genuine long-term value, trading at a historically low multiple, with elevated near-term earnings uncertainty and unresolved management credibility questions. That is a different proposition from buying CSL at 30x forward earnings with a predictable growth trajectory.

The distinction between the stock being objectively cheaper and being objectively a good investment is one that individual risk tolerance and time horizon must resolve. There is no universal verdict here.

For those monitoring the recovery thesis, three operational metrics matter most over the next 12-24 months: Behring’s margin trajectory as channel inventory normalises, Vifor’s pipeline progress against acquisition expectations, and whether management stability can be restored after a period of senior turnover and repeated earnings disappointments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

NPATA stands for Net Profit After Tax and Amortisation, and it strips out non-cash amortisation charges to reflect a company's underlying operating performance. For CSL investors, NPATA matters because the FY26 statutory loss of approximately US$648 million is distorted by a one-off impairment charge, while NPATA guidance of approximately US$3.1 billion better represents actual business performance.

CSL's share price fell approximately 17.7% in a single day on 10 May 2026 after the company announced a US$5 billion impairment charge on its CSL Vifor division, which it acquired to target iron deficiency and nephrology markets but which failed to deliver the growth expected at acquisition. The fall compounded an already significant 43% decline since January 2026 driven by earnings misses, a guidance downgrade, and divisional headwinds across all three business units.

CSL operates through CSL Behring (plasma-derived therapies, facing China albumin pricing pressure and US inventory normalisation), CSL Seqirus (influenza vaccines, impacted by the US military dropping mandatory flu vaccination in April 2026), and CSL Vifor (iron deficiency and nephrology, carrying a US$5 billion impairment charge and underperformance against acquisition expectations).

CSL currently trades at approximately 14.2x forward earnings, compared to the 25-30x or higher forward price-to-earnings ratio it commanded for most of the 2010s and early 2020s. This broadly halving of the valuation multiple has brought CSL in line with global plasma and healthcare peers such as Grifols and Takeda, rather than at the premium it maintained for most of the past decade.

The article identifies three metrics as most important over the next 12-24 months: CSL Behring's margin trajectory as US immunoglobulin channel inventory normalises, CSL Vifor's pipeline progress relative to the expectations that justified its acquisition price, and whether management stability can be restored after a period of senior turnover and repeated earnings disappointments.