RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

1 hr ago

At 7:30 PM AEST on Tuesday 12 May 2026, the Chalmers government announced the most significant overhaul of Australian investment taxation in nearly three decades. The 2026-27 Federal Budget moves simultaneously on two of the most heavily used tax structures in Australian property and equity investing: the 50% capital gains tax discount is being replaced, and negative gearing on established residential properties is being restricted to new builds. The CGT changes take effect from 1 July 2027, while the negative gearing cutoff applied from budget night itself, meaning the clock has already started for some investors. What follows is a precise breakdown of each reform, which investors are affected and from when, which structures remain protected, and what the market has already priced in as of today.

The 50% CGT discount for assets held longer than 12 months has been a cornerstone of Australian investment tax planning since the Howard government introduced it in 1999. That discount is now being abolished, effective for gains realised after 1 July 2027, and replaced with a cost base indexation model where the purchase price is adjusted for inflation before the gain is calculated.

The indexation model alone might resemble the pre-1999 framework. It does not stop there. A minimum 30% tax on net capital gains above $20,000 for individuals (and $40,000 for couples) has been introduced alongside the indexation change. This floor tax is what makes the reform structurally different from a simple reversion to the old model.

One underappreciated dynamic is the limited indexation protection in a low-inflation environment: with the RBA’s target band sitting at 2-3%, the annual cost base uplift from inflation adjustment will be modest, making the 30% minimum floor the operative constraint for most long-term holders rather than a backstop that rarely activates.

The ATO’s CGT calculation framework confirms that the 50% discount has applied to individuals holding assets for 12 months or more, and that complying super funds receive a 33.33% discount applied against the 15% statutory rate, which is the basis for the 10% effective rate that SMSFs retain under the new regime.

For new build investments, a choice mechanism between the two models is expected to apply, though ATO guidance on its operation had not been published as of 13 May 2026.

The three components of the new framework:

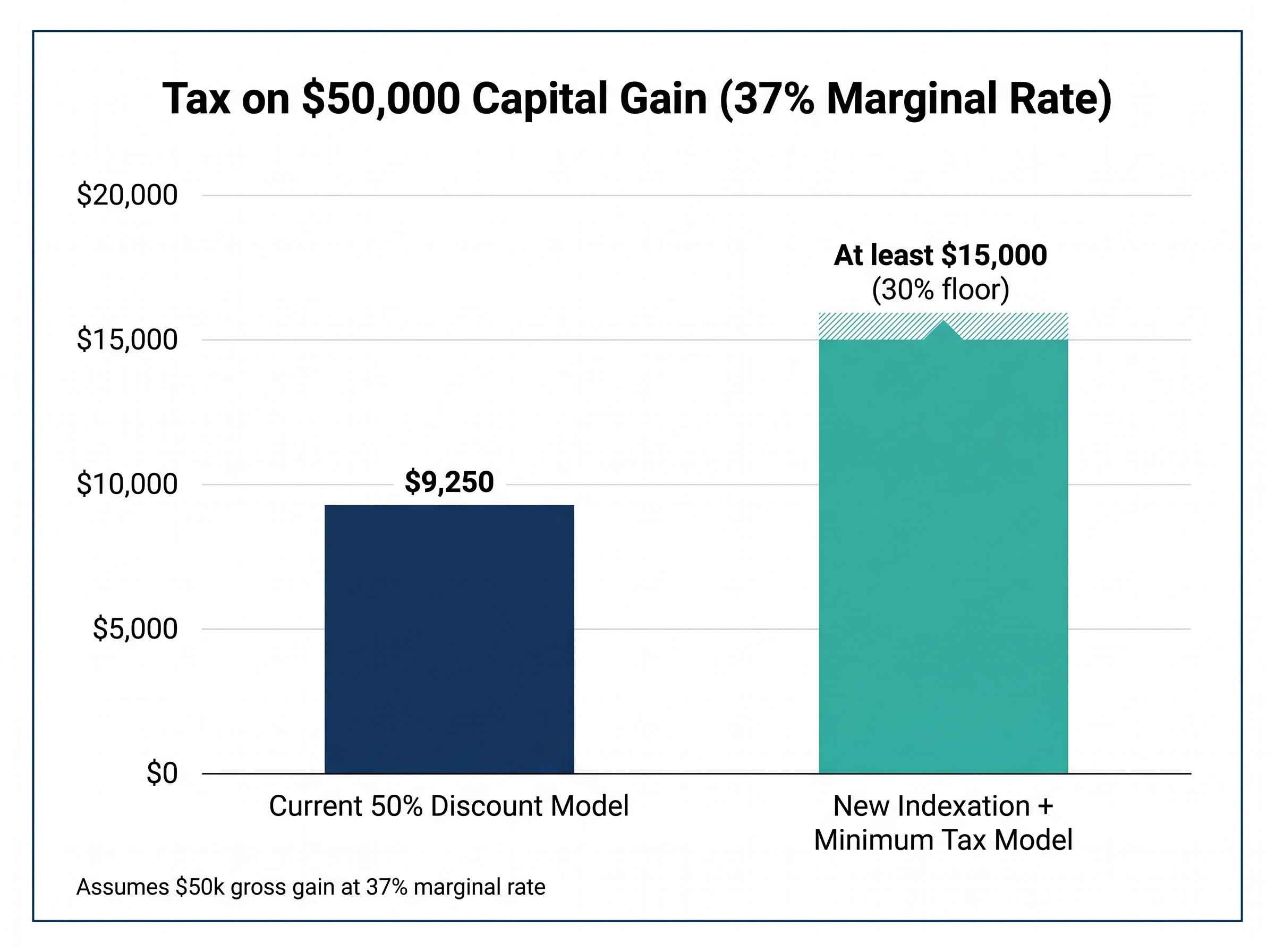

The table below illustrates the difference on a $50,000 net capital gain for an individual on a 37% marginal rate.

| Component | Current 50% discount model | New indexation + minimum tax model |

|---|---|---|

| Gross capital gain | $50,000 | $50,000 |

| Discount / indexation adjustment | 50% discount: taxable gain $25,000 | Inflation-adjusted cost base reduces gain (varies by holding period) |

| Tax rate applied | Marginal rate: 37% | Minimum 30% floor (or marginal rate if higher) |

| Tax on $25,000 taxable gain | $9,250 | At least $15,000 (30% of $50,000 pre-indexation gain, subject to indexation offset) |

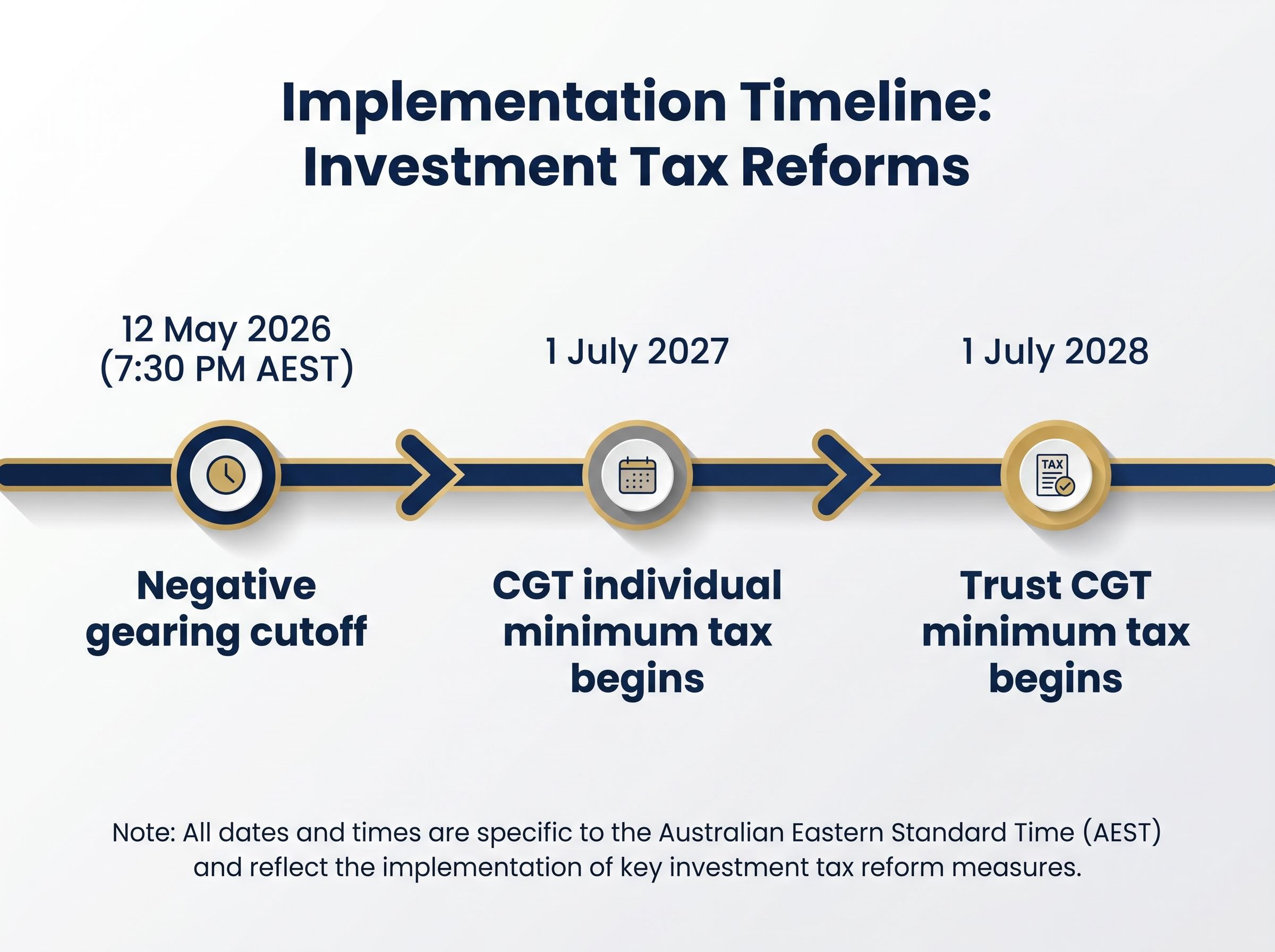

The grandfathering cutoff was 7:30 PM AEST on 12 May 2026. Investors who signed contracts on established residential properties after that moment are already outside the protected class. The door closed during the Treasurer’s speech.

The restriction does not eliminate negative gearing. It quarantines it. Losses on established properties acquired after the cutoff are ring-fenced: they can only be deducted against residential property income rather than against general income such as wages or salary. Carry-forward of quarantined losses is permitted. Negative gearing on new builds remains fully intact, a measure the government has framed as a housing supply incentive. The Housing Industry Association (HIA) broadly welcomed this framing in its initial response.

Quarantining rule: Losses on established residential properties acquired after 7:30 PM AEST, 12 May 2026 are deductible only against residential property income, not against wages, salary, or other general income. Carry-forward is permitted. Implementation takes effect 1 July 2027.

The three scenarios investors now fall into:

Both the CGT and negative gearing reforms are grandfathered. Existing holdings and contracts entered before the cutoff retain their current tax treatment for as long as those assets are held. Gains accrued prior to 1 July 2027 are also grandfathered.

The most significant carve-out applies to Self-Managed Superannuation Funds. SMSFs are excluded from the new CGT framework entirely. The effective CGT rate on long-held assets within SMSFs remains at 10%, unchanged. For investors weighing where to hold appreciating assets, the gap between a 10% effective rate inside super and a 30% minimum floor outside it has widened overnight.

The SMSF tax advantage over personal investment was already material before this budget, with accumulation-phase earnings taxed at 15% and long-held assets subject to a 10% effective CGT rate, but the reform widens that gap by approximately 20 percentage points on exit for high-income individual investors moving outside super.

Trusts face the 30% minimum CGT tax, but not until 1 July 2028, providing a one-year buffer relative to individual investors. Some exceptions also apply, though detailed guidance on the scope of those exceptions had not been published as of 13 May 2026. Pre-1985 assets carry specific transitional rules under the new framework, according to Alvarez & Marsal’s budget analysis.

| Entity type | CGT treatment from reform date | Effective date |

|---|---|---|

| Individual | Indexation model + 30% minimum tax on gains above $20,000 | 1 July 2027 |

| SMSF | Exempt from changes; 10% effective rate maintained | N/A |

| Trust | 30% minimum tax (with some exceptions) | 1 July 2028 |

These two reforms operate on different mechanisms, but their combined effect is greater than either in isolation. Understanding how they interact is the difference between making portfolio decisions under the old tax architecture and correctly pricing the new after-tax return profile.

The concept at the centre of this shift is asset location strategy: choosing which entity or structure holds a given asset based on the tax treatment each structure receives. The differential between an SMSF’s 10% effective CGT rate and an individual’s new 30% minimum floor makes that choice more consequential than it was 48 hours ago. ATO guidance on the precise inflation calculation methodology for the indexation model had not been published as of 13 May 2026, meaning exact modelling is not yet possible.

The S&P/ASX 200 A-REIT index closed at 1,741.30 on 13 May 2026, down from an open of 1,762.60, a decline of approximately 1.2% on the first full trading day after the budget announcement.

The A-REIT decline offers the most direct market signal on how property-exposed equities are absorbing the budget, but the picture is not clean. The same session saw the ASX absorbing above-forecast US inflation data, with the US Consumer Price Index printing at 3.8% annual for April 2026, the highest since May 2023. The REIT move reflects a combination of domestic policy repricing and global rate pressure rather than the budget alone.

The repricing pressure visible in the A-REIT index reflects the inverse of what is happening to structurally better-positioned asset classes, including passive ETFs, dividend-paying blue-chip equities, and superannuation-held assets, where the new tax settings create a relative advantage that did not exist under the old framework.

What remains outstanding matters more than what has been priced so far. The following are still pending as of today:

The HIA’s initial response was broadly positive, framing the housing elements of the budget as productivity-oriented. KPMG and Alvarez & Marsal had published initial analyses confirming the core mechanics, but full legislative detail is weeks away.

Two separate timelines are now running. The negative gearing cutoff has already passed. The CGT changes apply to gains realised from 1 July 2027. Trusts face the minimum CGT tax from 1 July 2028. These are not a single deadline; they are a staggered sequence, and the decisions that lock in exposure are being made now.

The absence of ATO guidance and draft legislation as of today means financial advisers and investors cannot yet model precise outcomes under the indexation methodology. Seeking professional tax advice before making structural decisions is appropriate given this level of uncertainty.

Monitoring resources for ongoing updates:

Three structural realities are now in place. Negative gearing on established properties is restricted for post-cutoff purchases, with losses quarantined to residential income. The 50% CGT discount is replaced from July 2027 with a cost base indexation model and a minimum 30% tax floor. SMSFs remain the most tax-advantaged structure for long-term asset holding, with an effective 10% CGT rate unchanged.

What remains unknown: the precise inflation methodology for CGT indexation, the full scope of trust exceptions, and detailed ATO guidance on the choice mechanism for new builds. These details will determine the exact after-tax outcomes that investors and advisers need to model.

The most immediate step is understanding which category existing holdings and any pending contracts fall into, and deferring structural portfolio changes until ATO guidance is available.

For investors who have concluded that super is now the optimal structure for long-term asset holding and want to act on that before year-end, our comprehensive walkthrough of superannuation contribution strategies for 2026 covers the carry-forward rules, the rising concessional cap of $32,500 from 1 July 2026, and the FY2020-21 unused cap amounts that expire permanently on 30 June 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding tax implementation and market outcomes are subject to change based on legislative drafting, ATO guidance, and market conditions.

From 1 July 2027, the 50% CGT discount for assets held more than 12 months is replaced by a cost base indexation model, where the purchase price is adjusted for inflation before the gain is calculated, alongside a minimum 30% tax on net capital gains above $20,000 for individuals.

Quarantining means that losses on established residential properties acquired after 7:30 PM AEST on 12 May 2026 can only be deducted against residential property income, not against wages, salary, or other general income, though carry-forward of those losses is still permitted.

No. Self-Managed Superannuation Funds are fully exempt from the new CGT framework, and the effective 10% CGT rate on long-held assets inside SMSFs remains unchanged, widening the tax advantage gap between super and individual investing by approximately 20 percentage points.

The cutoff was 7:30 PM AEST on 12 May 2026. Investors who held existing properties or signed contracts on established residential properties before that moment retain full negative gearing treatment for as long as those assets are held.

Trusts face the 30% minimum CGT tax from 1 July 2028, one year later than the 1 July 2027 start date that applies to individual investors, with some exceptions whose full scope had not been published as of 13 May 2026.