RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

3 hrs ago

Three tax changes announced on 12 May 2026 have effectively rewritten the after-tax return profile of almost every major asset class Australians invest in, and the direction of those changes is not the same for everyone. Treasurer Jim Chalmers delivered the 2026 Federal Budget with reforms to capital gains tax, negative gearing, and discretionary trust distributions that together represent the most significant reshaping of the investment tax landscape in decades. As of Budget night, none of these measures has passed Parliament, but the direction is clear enough for investors to begin thinking about what it means for their portfolios.

What follows is a map of which investments are set to lose their tax-efficiency edge, which are positioned to benefit, and how to think about repositioning without making reactive decisions before the legislative details are confirmed.

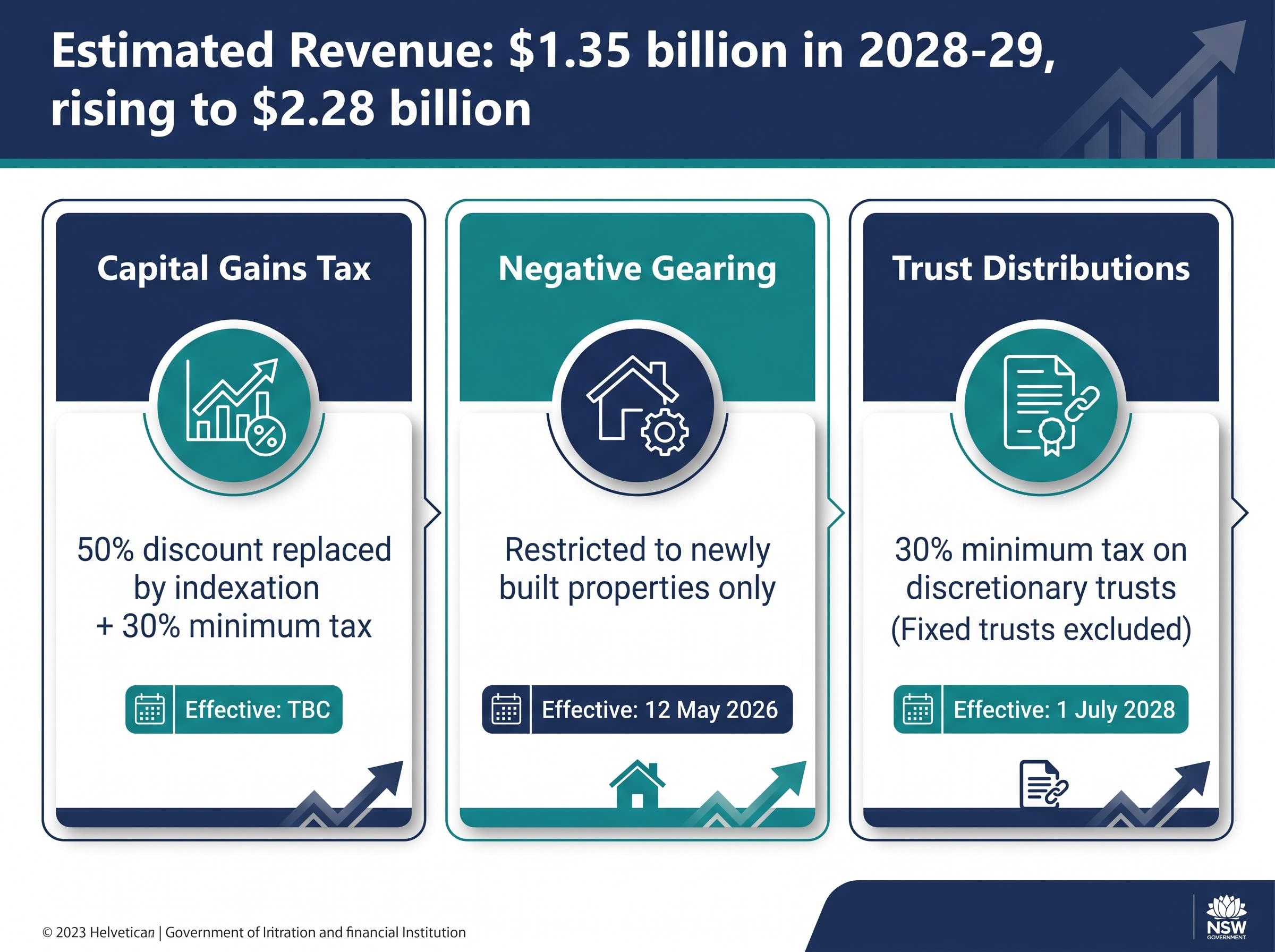

The Budget introduced three distinct changes. Each targets a different part of the investment tax architecture, and each operates on a different timeline.

Capital gains tax: The longstanding 50% CGT discount for assets held longer than 12 months is replaced by an inflation-indexation-based discount plus a 30% minimum tax floor on capital gains. The effective date for the new regime has not yet been confirmed in the Budget papers.

Negative gearing: From Budget night itself (12 May 2026), negative gearing deductions on interest expenses are restricted to newly built properties only. Any purchase of existing residential property after that date is not eligible for deductions against other income.

Trust distributions: A 30% minimum tax applies to discretionary trust distributions from 1 July 2028. Fixed trusts are excluded.

The combined revenue estimate from the Budget papers is approximately $1.35 billion in 2028-29, rising to approximately $2.28 billion in subsequent years.

Budget Paper No. 1 Statement 4, published by the Australian Treasury on Budget night, sets out the full legislative rationale for the three reforms, framing them as measures to make the tax system fairer and more sustainable while redirecting capital toward more productive economic uses.

| Change | Effective date | Who is affected | Key uncertainty |

|---|---|---|---|

| CGT discount replaced with indexation + 30% minimum tax | TBC (no date confirmed in Budget papers) | All investors holding CGT assets | Transitional and grandfathering rules for existing assets not yet released |

| Negative gearing restricted to new builds | 12 May 2026 (Budget night) | Investors acquiring existing residential property | Precise definition of “new build” and treatment of existing loans pending |

| 30% minimum tax on discretionary trust distributions | 1 July 2028 | Discretionary trust beneficiaries | Trust structure scope and interaction with Division 7A unconfirmed |

Several details will determine precisely how these changes land in practice, and none has been released as of Budget night:

Treasury exposure drafts and ATO guidance are the primary sources to monitor. Investors making significant decisions should wait for those releases rather than acting on the announcements alone.

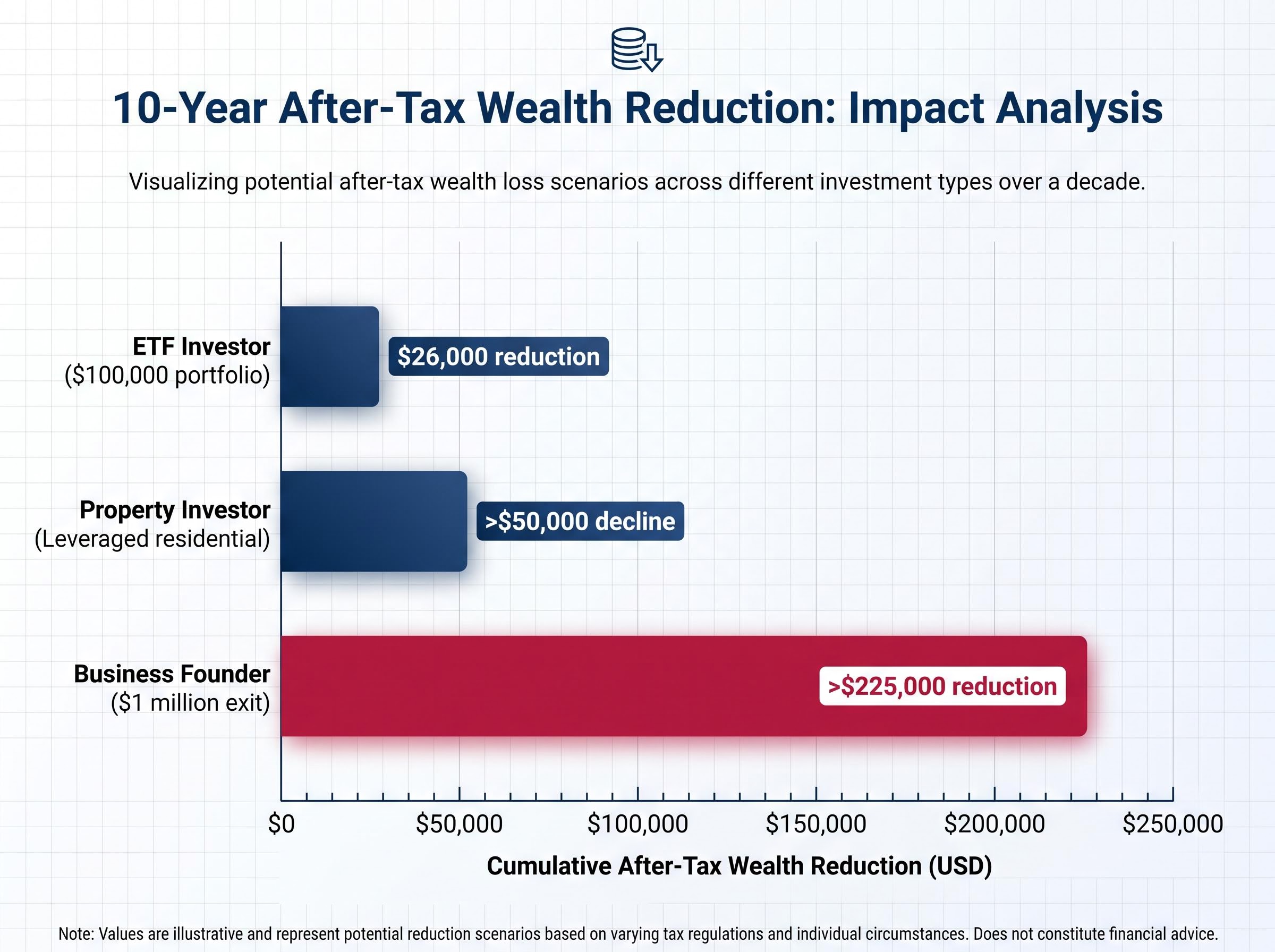

A few percentage points of additional tax drag may appear modest in any single year. Compounded over a typical investment horizon, those percentage points translate into wealth differences measured in tens of thousands of dollars.

The impact is not uniform. Three illustrative 10-year scenarios show how differently the new rules bite depending on asset type and investor profile:

The business founder scenario is the starkest illustration of the new regime’s impact. A $225,000+ reduction in after-tax proceeds on a $1 million exit fundamentally alters the risk-reward calculation for entrepreneurial investment in Australia.

These projections show that the tax changes are not marginal. The revised framework effectively raises how much Australians must save to reach identical financial outcomes, and younger investors accumulating wealth outside superannuation are disproportionately exposed compared with older investors drawing on established super balances.

Not every asset class is equally affected. The losses concentrate where the investment case relied on specific tax advantages that the Budget has now diminished or removed.

A less visible consequence sits underneath the asset-specific analysis. Investors facing a larger CGT bill on disposal may hold underperforming or misallocated assets longer than is financially optimal, simply to defer the tax event.

This creates a tension between tax minimisation and sound investment decision-making. A portfolio frozen by tax-deferral logic can underperform a portfolio that accepts the tax cost and redeploys capital more effectively. The lock-in effect reduces capital mobility across the economy and, at the individual level, may quietly erode returns in ways that are harder to measure than the tax bill itself.

The same changes that diminish certain tax advantages create relative tailwinds elsewhere. The winning side of the ledger is specific and structural.

| Asset class | Why it benefits | Key consideration or limitation |

|---|---|---|

| Passive ETFs (e.g., VAS) | Low portfolio turnover generates fewer realised capital gains distributed to investors, reducing exposure to the 30% minimum tax floor | Underlying index rebalancing still creates some taxable events |

| Dividend-paying blue-chip equities | A higher proportion of total return arrives as franked income rather than capital gain, with franking credits offsetting personal tax | Dividend income still taxed at marginal rates; benefit depends on individual tax position |

| Inflation-linked bond ETFs (e.g., ILB on ASX) | Returns are income-dominated, and CPI-linked CGT indexation creates a natural portfolio hedge | Lower total return potential compared with equities |

| ASX-listed REITs | Provide property-sector exposure without the negative gearing restriction that applies to direct residential holdings | REIT distributions can include capital gains components; structure varies by trust |

| Superannuation | Concessional tax environment retained; accelerating contributions is widely recommended | Contribution caps apply; capital locked until preservation age |

| Owner-occupied housing | CGT exemption unchanged; relative advantage increases as other asset classes lose tax efficiency | Illiquid, concentrated, and not an investment strategy for all profiles |

The tax changes do not eliminate sound investment options for Australians. They shift relative advantages, and knowing which assets now carry a structural tax tailwind is the starting point for a coherent portfolio review.

Superannuation’s resilience under the 2026 Budget is not incidental: super’s tax wrapper advantage over identically invested portfolios held outside the system is projected to create a $230,000 wealth gap over 25 years for mid-career investors, a structural edge the Budget has left entirely intact.

The instinct after a Budget of this magnitude is to act quickly. That instinct should be resisted selectively, not entirely. Some actions are already sensible given confirmed changes. Others should wait for legislative detail that does not yet exist.

A sequenced approach:

Salary sacrifice mechanics illustrate the immediate tax saving available before the broader legislative changes take effect: at the $120,000 income level, directing $15,000 into concessional contributions generates an estimated $4,800 tax saving in the current financial year, with the benefit scaling further at higher marginal rates.

Holding an asset purely to defer a CGT bill can be a more expensive mistake than paying the tax and redeploying capital more effectively. Optimising for tax alone, without regard to the underlying investment case, is its own financial risk.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The government’s rationale for the package rests on a specific economic argument. Whether that argument holds is genuinely contested.

The government’s case:

The critics’ case:

The tension at the centre of this reform is genuine: simultaneously promoting innovation and entrepreneurship while materially increasing the tax burden on the upside that incentivises such risk-taking is a contradiction the legislative process will need to resolve.

The investors best positioned under these reforms are those who understand the full policy logic, not just the immediate changes, because the reform trajectory and the political uncertainty around it are themselves portfolio risks to monitor.

The 2026 Budget has created three distinct categories for investors to track: changes already in effect (the negative gearing restriction from Budget night), changes pending legislative confirmation (the CGT overhaul and the trust distribution minimum tax from 1 July 2028), and asset classes that now sit on different sides of the tax-efficiency ledger.

The winners-and-losers framework in this article is a starting point for a structured conversation with a financial adviser, not a basis for immediate portfolio decisions. Much depends on transitional rules, grandfathering provisions, and legislative detail that has not yet been released.

The legislative process from June 2026 onward, Treasury exposure drafts, and independent modelling from bodies such as the Parliamentary Budget Office and the Grattan Institute will provide the clarity investors need. Those are the sources worth monitoring, rather than reacting to coverage alone.

—

The 2026 Federal Budget introduced three key changes: the 50% CGT discount is replaced by an inflation-indexation-based discount plus a 30% minimum tax floor, negative gearing deductions on interest expenses are restricted to newly built properties from 12 May 2026, and a 30% minimum tax applies to discretionary trust distributions from 1 July 2028.

From 12 May 2026, investors who purchase existing residential properties can no longer claim negative gearing deductions on interest expenses against their other income. The restriction applies only to new acquisitions of existing stock; newly built properties remain eligible for negative gearing.

Passive ETFs with low portfolio turnover, dividend-paying blue-chip equities with franking credits, ASX-listed REITs, inflation-linked bond ETFs, superannuation, and owner-occupied housing are all positioned to benefit, as they either avoid the new CGT and trust tax floors or retain existing tax advantages.

The 30% minimum tax on discretionary trust distributions takes effect from 1 July 2028, giving investors approximately two years to review their trust structures with a financial adviser before the rules apply. Fixed trusts are excluded from the measure.

Investors should review their superannuation contribution capacity immediately, evaluate any planned existing-property purchases under the new negative gearing rules, flag discretionary trust structures for adviser review ahead of 2028, and wait for Treasury exposure drafts before making major asset disposal decisions, as transitional CGT rules have not yet been released.