Life360 (ASX:360) delivered Q1 2026 revenue growth of 38% and pushed its global user base to nearly 98 million monthly active users. The profit line, however, grew at just 7%. That gap between top-line momentum and bottom-line delivery is the story of the quarter, and it is the gap that ASX investors need to read carefully before drawing conclusions. On 12 May 2026, shares edged higher following the release, but the modest reaction sits against a stock that has fallen more than 60% from its October 2025 peak. What follows is a breakdown of what the Q1 numbers actually show: where the growth is genuine, where the costs went, what management is promising for the second half of 2026, and what the Life360 share price context means for investors evaluating the stock today.

Life360 shares edge higher as Q1 results land on the ASX

The market’s response to Life360’s Q1 print was positive but measured. Shares opened at A$19.98 on 12 May 2026, touched an intraday high of A$20.15, and settled around A$20.11, a gain of approximately 1.9% from the previous close of A$19.30.

Key trading data from the session:

- Current price: A$20.11

- Intraday range: A$19.27 to A$20.15

- Volume: approximately 2.67 million shares

- Year-to-date return: -38.82%

- 90-day return: +20.5%

The year-to-date decline explains the restraint. A stock that has shed nearly 39% since January and more than 60% from its October 2025 peak does not rerate on a single quarter, regardless of how strong the headline numbers look.

The ASX Chapter 4 periodic disclosure rules require listed entities to release quarterly, half-year, and annual reports in a framework that supplements continuous disclosure obligations, meaning Life360’s Q1 revenue and cashflow figures carry formal reporting weight rather than functioning as voluntary investor updates.

Valuation context: SimpleWallSt’s analyst consensus fair value stands at A$35.29 (May 2026), implying an approximate 43% discount at current prices. Broker price target revisions following the Q1 release are pending.

That discount frames the opportunity and the scepticism simultaneously. The market is pricing Life360 as though the growth trajectory requires further proof before the valuation gap closes.

When big ASX news breaks, our subscribers know first

Revenue surged 38%, and the user growth numbers are hard to argue with

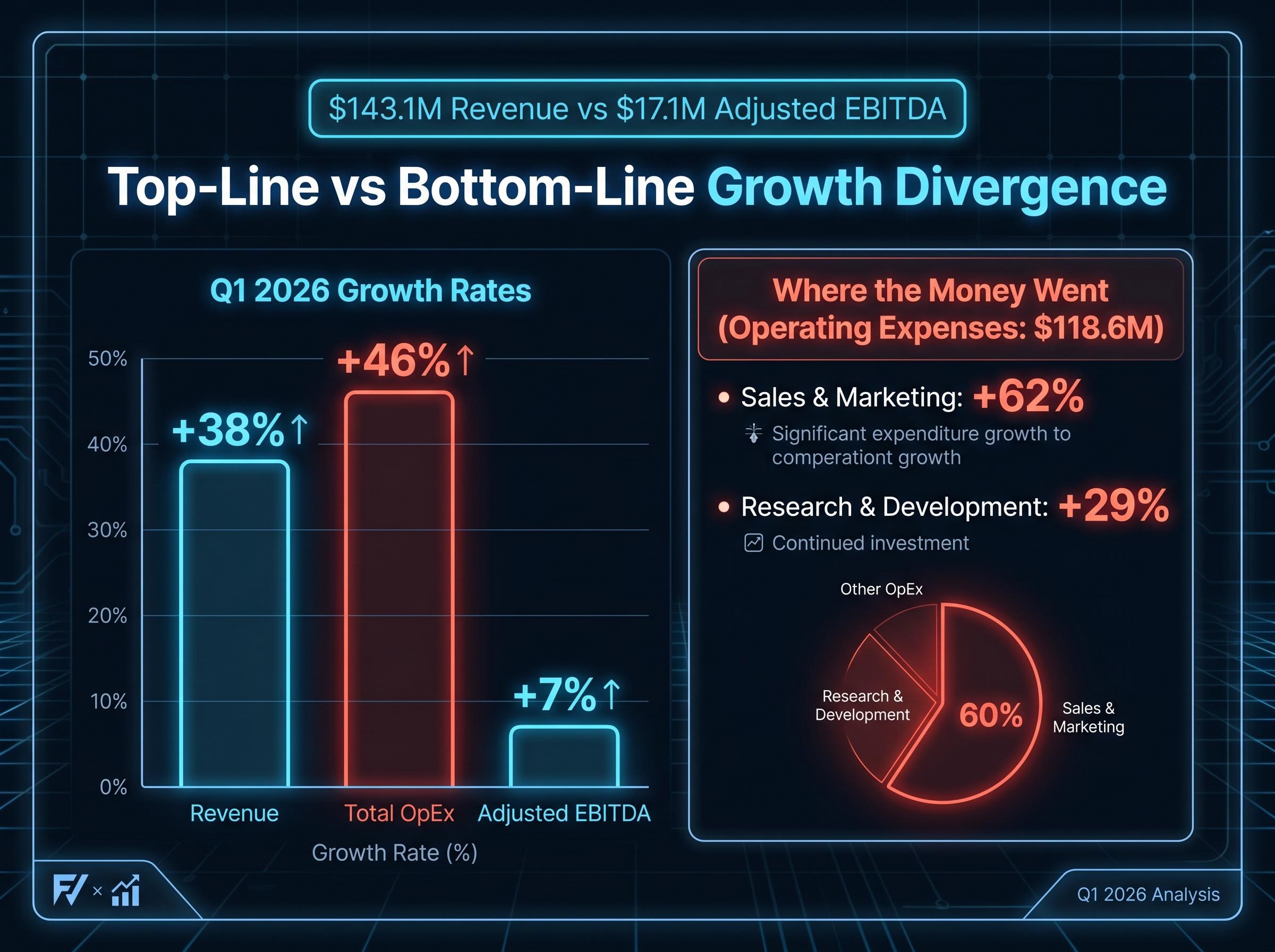

Life360 reported Q1 2026 total revenue of $143.1 million, up 38% year-over-year. Annualised monthly revenue reached $517.9 million, up 32%. Both figures exceeded Bell Potter’s forecast of $137.5 million for the quarter.

The Q1 trajectory becomes clearer when read against Life360’s Q4 2025 milestone, when the company reported its first full-year profit in company history alongside a 105% surge in adjusted EBITDA, marking a structural shift from loss-making growth stock to a business beginning to monetise its scale.

Subscription revenue accounted for $108.2 million of the total, a 32% increase. The advertising line, disclosed as a separate item for the first time, contributed $19 million, up year-over-year, signalling a structural shift in the company’s revenue composition.

| Metric | Q1 2025 | Q1 2026 | Year-on-Year Change |

|---|---|---|---|

| Total Revenue | $103.7M | $143.1M | +38% |

| Global MAU | 83.6M | 97.8M | +17% |

| Paying Circles | 2.36M | 3.0M | +27% |

| ARPPC | All-time high prior | New all-time high | +7% |

| Advertising Revenue | N/A | $19M | N/A |

User and subscriber growth reinforced the revenue story:

- Global monthly active users: 97.8 million, up 17%; net Q1 additions of 1.9 million

- Paying circles: 3 million, up 27%; net additions of 1.9 million, described by management as a record

- Average revenue per paying circle (ARPPC): up 7% to an all-time high

The combination of accelerating advertising revenue, record subscriber additions, and rising revenue per user indicates that Life360’s monetisation flywheel is gaining traction rather than simply adding users at lower value.

Why the profit line grew at just 7% when revenue grew at 38%

Revenue grew 38%. Adjusted EBITDA grew 7%. The gap is stark, and it is worth understanding rather than reacting to.

The headline contrast: $143.1 million in Q1 revenue (up 38%) produced $17.1 million in adjusted EBITDA (up 7%, on a 12% margin). Bell Potter had forecast approximately 10.5% margins on lower revenue, so the result technically exceeded expectations, but the revenue-to-profit divergence raises a fair question about where the money went.

Total operating expenses reached $118.6 million, up 46% year-over-year. Three line items absorbed the bulk of the increase:

- Sales and marketing: up 62%, driven by growth media spend and App Store commissions tied to accelerating subscriber acquisition

- Research and development: up 29%, reflecting headcount additions from the Nativo acquisition and ongoing AI-related investment

- General integration costs: concentrated in H1 as part of the Nativo integration and brand-building cycle

The cost growth is real. It is also, according to management, deliberate. Life360 is spending into its growth phase while user acquisition economics remain favourable and the advertising business scales.

The pattern of strong revenue growth paired with investor scepticism about cost acceleration is not unique to Life360: across Q1 2026 earnings season, AI capex commitments from the largest US tech companies produced the same revenue-versus-margin tension, with markets repeatedly punishing spending acceleration even where top-line beats were delivered.

What the operating cashflow figure adds to the picture

Adjusted EBITDA captures one view of profitability. Operating cashflow provides another, and the two told different stories in Q1.

Positive operating cashflow came in at $17.2 million, up 42% year-over-year. That growth rate is six times the EBITDA growth rate, suggesting that non-cash charges and timing differences within the EBITDA calculation compressed the headline profit figure more than the underlying cash generation.

Cash on hand at the end of Q1 stood at $459 million, compared to $288.6 million at the same point in 2025. The balance sheet is not under pressure. Whether the investment cycle delivers returns is a separate question, but the runway to sustain it is not in doubt.

Management raises full-year guidance and explains the investment logic

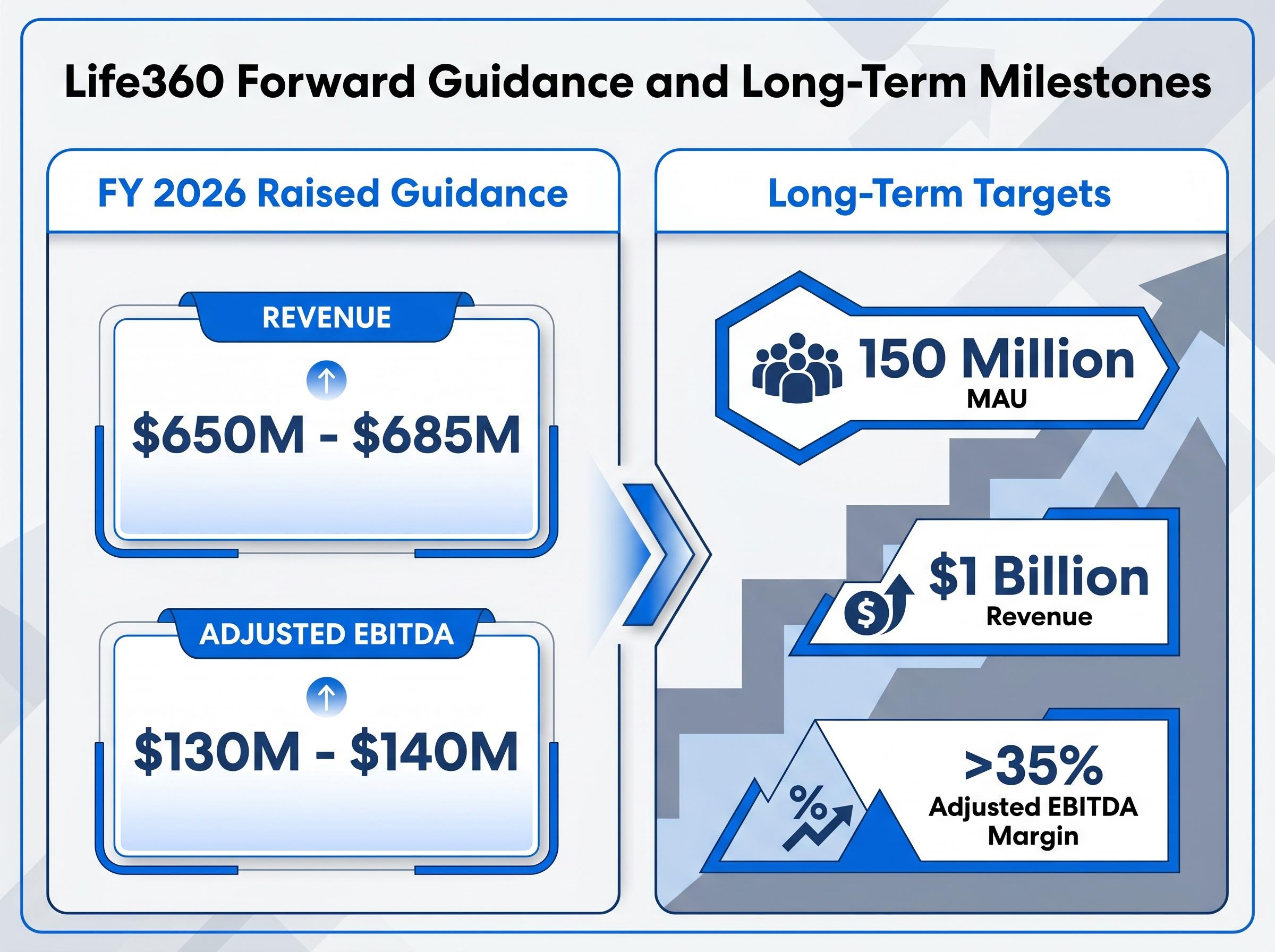

The clearest signal that Life360’s leadership views the Q1 cost pattern as temporary came in the form of a guidance raise. Full-year 2026 revenue guidance was lifted to $650 million to $685 million, with adjusted EBITDA guidance raised to $130 million to $140 million.

Raised full-year 2026 revenue guidance: $650 million to $685 million

Management framed the first-half cost concentration as a deliberate front-loading of investment, with advertising revenue seasonality and subscriber compounding expected to benefit the second half. Integration costs from the Nativo acquisition are largely an H1 event, and the organic portion of advertising revenue (approximately 50% of the Q1 total) is expected to scale as the platform matures.

The long-term targets were reaffirmed:

- 150 million monthly active users

- $1 billion in revenue

- Greater than 35% adjusted EBITDA margins

On the operational side, management disclosed that AI-driven developer productivity has increased more than 50% year-over-year, though earnings call analysts questioned the real-world impact of this claim. Monthly active user growth was temporarily held back by Android registration funnel technical issues, which management expects to resolve by Q3 2026.

The guidance raise shifts the conversation. Rather than asking investors to trust the strategy on faith, management has committed to specific numbers against which the second half will be measured.

What Life360’s Q1 result means for ASX investors watching the stock

The Q1 result validates the growth thesis. It does not yet resolve the profitability debate.

Rask Media analysts have described Life360 as an ASX growth share worth monitoring, noting that its competitive moat appears stronger than current market pricing implies. The caveat is straightforward: sustained profit growth is the re-rating catalyst the market is waiting for. A 3-year total shareholder return of approximately 3.4 times provides long-term context, but the year-to-date decline signals that patience has limits.

A 3-year total shareholder return of approximately 3.4 times demonstrates that long-term investing frameworks, applied to high-growth ASX technology positions, can produce materially different outcomes than the year-to-date return figure alone suggests, though the gap between peak pricing and current levels is a reminder that entry timing and holding conviction interact in ways that simple compounding tables do not capture.

The near-miss on the 100 million MAU milestone (actual: 97.8 million) and the Android funnel issue are worth noting as a technical setback rather than a structural growth problem. Management’s timeline for a fix by Q3 2026 is specific enough to be testable.

Three checkpoints for investors watching the stock through H2 2026:

- MAU recovery: Does the Android fix restore the growth trajectory toward 100 million and beyond?

- EBITDA margin expansion: Does the second half deliver the margin improvement the front-loaded cost thesis promises?

- Advertising revenue growth: Does the Nativo-powered advertising line continue scaling at triple-digit rates?

With the stock trading more than 60% below its October 2025 peak and 43% below consensus fair value, investors face a genuine evaluation decision. H2 2026 results will determine whether the current price represents a recovery opportunity or whether the market’s scepticism is justified.

The verdict is half-delivered: Life360’s growth engine is running, but the profit proof is still coming

Life360 reported record revenue, record subscriber additions, and a raised full-year guidance range. The growth engine is performing. The profit engine is not yet matching its pace, and the market is pricing the stock accordingly.

The Q1 result is a pass, not a verdict. Management has committed to $130 million to $140 million in adjusted EBITDA for 2026 and reaffirmed long-term margins above 35%. Those commitments will be tested in the second half, when the front-loaded investment cycle is supposed to ease and advertising seasonality is expected to contribute.

The next quarterly update is the checkpoint. If H2 numbers show margin expansion alongside continued revenue growth, the re-rating case strengthens materially. If they do not, the 43% discount to consensus fair value may prove to be the market pricing the stock correctly rather than undervaluing it.

Investors evaluating whether to hold Life360 as a direct ASX position or as part of a broader growth allocation will find our dedicated guide to the best ASX growth ETFs useful, covering how NDQ, FANG, HYGG, RBTZ, and ATEC perform under the current RBA rate environment, with risk-adjusted return comparisons across the five leading funds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including management guidance and long-term targets, are subject to change based on market developments and company performance.