Why Two Catalysts Are Converging on European Consumer Stocks Now

47 mins ago

Canada ranks last among G7 nations in investment in machinery, equipment, and intellectual property. Business investment per Canadian worker fell consistently from 2014 to 2025. The Canada Strong Fund, announced by Prime Minister Mark Carney on 27 April 2026 with CAD $25 billion in seed capital, was built in part as a response to that failure, with a promise that retail investors would be able to invest alongside institutional capital.

That retail product remains in design. Consultation outcomes and confirmed terms are still pending as of May 2026. But the commercial interest is real: investors want to know whether this product deserves a place in their portfolios before the window opens.

What follows is a layered analysis of what is structurally confirmed, what remains unknown, and how to evaluate the tradeoffs of liquidity, concentration, potential tax treatment, and the meaning of a government principal guarantee before making any capital commitment.

The productivity data is uncomfortable. Canada finished last among G7 nations in investment in machinery, equipment, and intellectual property, and business investment per worker declined over the decade from 2014 to 2025. That gap is made more striking by the country’s resource position: Canada holds the fourth-largest oil reserves globally and is a leading producer of both potash and uranium.

The fund’s stated investment mandate targets the sectors where that underinvestment is most visible:

The pipeline is already substantial. 15 projects have been referred to the Major Projects Office, with over CAD $125 billion in economy-wide investment under development.

The Major Projects Office provides a single point of contact for project approvals with a maximum 2-year regulatory review timeline, a direct response to the delays that have historically deterred private capital from large Canadian projects.

Whether the fund’s fiscal case holds depends substantially on whether this regulatory reform accelerates project timelines at both federal and provincial levels. The investment thesis and the policy reform are connected: one without the other weakens both.

The fund is structured as a Crown corporation with arm’s-length governance, an independently appointed CEO and board, and a mandate to operate on a fully commercial basis.

“Operating on a fully commercial basis alongside other investors.”

This is an equity-focused vehicle, not a lending programme. The fund takes ownership stakes in projects across energy, minerals, agriculture, and infrastructure. The initial CAD $25 billion will be seeded over three years, funded through government borrowing (debt issuance), with returns reinvested to grow the fund over time.

The relationship between government borrowing and asset inflation is not straightforward: debt-funded government investment programmes have historically concentrated gains among investors already holding equity and infrastructure assets, raising a structural question about whether retail participation in the Canada Strong Fund would meaningfully broaden wealth distribution or primarily benefit those with existing portfolio capacity.

The retail investment product has been confirmed in principle. Consultation on design terms is ongoing as of May 2026, with the Spring Economic Update 2026 (Department of Finance) the primary expected source for retail product specifications.

A distinction worth noting: the Canada Strong Fund is a separate vehicle from the Build Communities Strong Fund, which was announced earlier in April 2026 and serves a different purpose.

| Factor | Canada Strong Fund | Build Communities Strong Fund |

|---|---|---|

| Announcement date | 27 April 2026 | 7-9 April 2026 |

| Initial capital | CAD $25 billion (3 years) | CAD $51 billion (10 years) |

| Retail access | Planned; under consultation | Not structured for retail access |

The arm’s-length governance structure and commercial mandate are the fund’s credibility anchors. Whether those design features survive into final legislation is the single biggest structural question for long-term return quality.

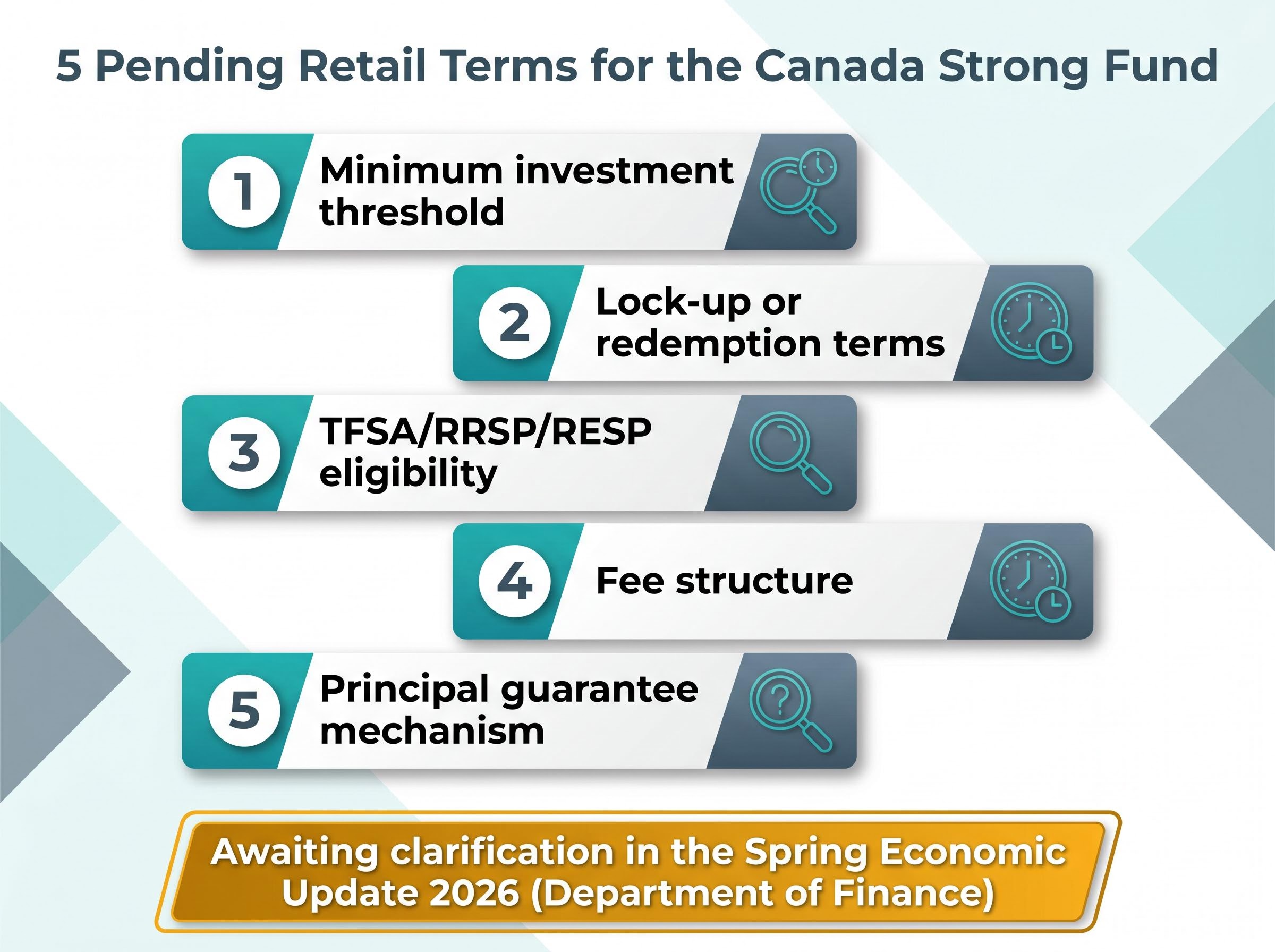

The structural picture is clear enough. The problem is what sits behind it: five material unknowns that any investor would need answered before committing capital.

These are not minor administrative details. Each one materially affects the product’s risk-adjusted attractiveness. The absence of confirmed terms is itself an investment constraint.

The U.S. experience with retail-accessible private market funds offers a cautionary reference: some products experienced withdrawal restrictions under redemption pressure, leaving investors locked in during periods of stress.

Consultation is ongoing as of May 2026. The Spring Economic Update 2026 from the Department of Finance is the primary expected source for retail product specifications. The Canada Strong Fund Transition Office is responsible for finalising governance structure, investment mandate, and retail terms.

The Spring Economic Update 2026 from the Department of Finance Canada formally establishes the fund’s CAD $25 billion seed capital commitment and confirms the retail investment product in principle, making it the primary disclosure document investors should consult for any updates to product specifications as consultation concludes.

Waiting for those disclosures is a rational choice, not a missed opportunity.

Each of these risks is manageable in isolation. The problem is what happens when they layer together.

Many Canadian investors already hold a disproportionate share of their portfolios in Canadian assets. The fund adds concentrated domestic equity exposure in precisely the sectors that already dominate the TSX: energy, materials, and infrastructure. For an investor already overweight Canadian equities, this product compounds an existing concentration rather than diversifying it.

TSX concentration and portfolio risk are closely linked for Canadian investors: the index is heavily weighted toward energy, financials, and materials, meaning that adding a fund with identical sector exposure compounds rather than diversifies the structural risk already embedded in a standard Canadian equity allocation.

Infrastructure illiquidity adds a second layer. Major projects can require more than a decade to generate returns, and selling equity stakes prior to maturity may itself require years of negotiation. This is a fundamentally different liquidity profile from anything currently available in a standard retail portfolio.

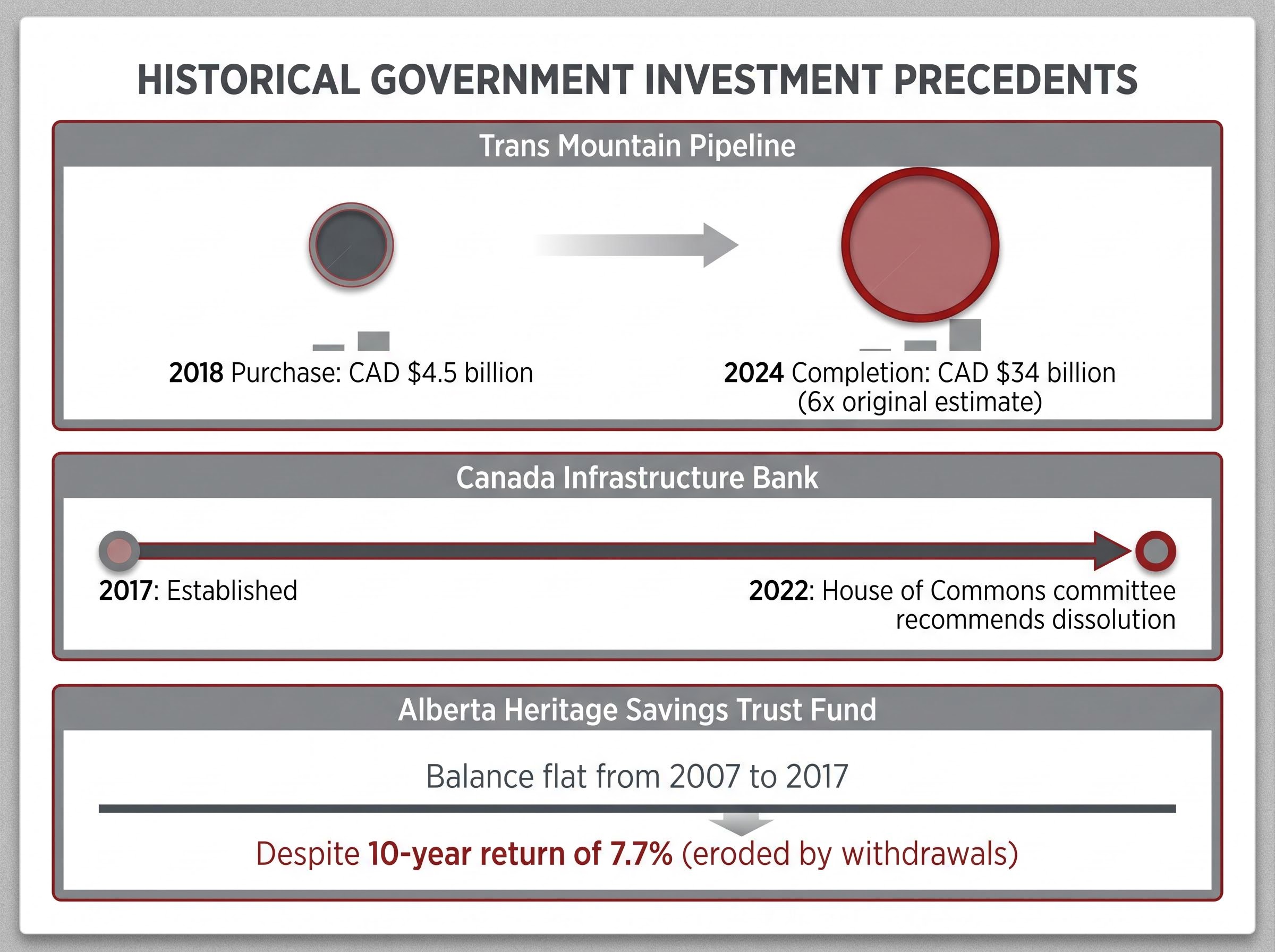

The Alberta Heritage Savings Trust Fund balance remained flat from 2007 to 2017 despite a 10-year return of 7.7%, due to government withdrawals. Political interference can erode returns even when investment performance is adequate.

Sovereign wealth funds have historically underperformed a standard 60/40 portfolio, partly due to politically motivated investment decisions. That track record is relevant context for any fund with a government mandate.

Contrast the fund’s profile with what is already available:

| Factor | Canada Strong Fund | XIU (iShares S&P/TSX 60) | VDY (Vanguard High Dividend) |

|---|---|---|---|

| Liquidity | Terms pending; likely illiquid | Daily | Daily |

| Geographic concentration | Canada only (strategic sectors) | Canada (broad TSX) | Canada (dividend equities) |

| Tax status | Pending confirmation | TFSA/RRSP eligible | TFSA/RRSP eligible |

The right answer varies by investor. Someone with significant international diversification and a 15-plus year investment horizon faces a materially different calculus than someone already concentrated in Canadian equities with a 5-year horizon.

Many retail investors will arrive at this product assuming a government guarantee makes it effectively risk-free. That assumption needs correction.

A confirmed principal guarantee would make the product structurally comparable to a government bond in terms of downside protection. It would not protect against inflation erosion, opportunity cost, or the effects of a long lock-up period. If capital is locked for a decade and inflation averages 3% annually, the real value of a nominal principal guarantee deteriorates meaningfully.

As of May 2026, the guarantee has not been confirmed. Its precise mechanism, whether it covers nominal principal, inflation-adjusted principal, or something else entirely, remains a material unknown.

Three scenarios illustrate how the guarantee question reshapes portfolio positioning:

The fiscal dimension matters as well. If retail principal is guaranteed and projects underperform, the government absorbs the downside. Sovereign wealth funds have delivered approximately 6.3% average returns over ten years. The spread above borrowing costs (approximately 2.8 percentage points) is the theoretical margin for fiscal sustainability, and it is not wide.

The fiscal sustainability of debt-funded vehicles depends less on the total stock of government debt than on the spread between borrowing costs and investment returns, a distinction that is often lost in headline debt metrics but is central to evaluating whether the Canada Strong Fund’s financing structure remains viable as interest rates evolve.

The Trans Mountain Pipeline is the most directly relevant precedent. Purchased in 2018 for CAD $4.5 billion, the expansion was completed in 2024 at a final cost of CAD $34 billion, approximately six times the original estimate.

The Canada Infrastructure Bank, established in 2017, received mixed assessments, with a House of Commons committee recommending its dissolution in 2022.

These are not disqualifying facts. They are data points that warrant scrutiny of project selection and governance quality in the Canada Strong Fund.

Investors who want Canadian strategic sector exposure right now have liquid, transparent options available:

These products lack the sovereign wealth fund model’s strategic equity focus on national-priority projects. The Canada Strong Fund, once its retail terms are confirmed, may offer genuinely differentiated exposure to large-scale Canadian assets that listed ETFs cannot replicate. That distinction is real, but it needs to be supported by confirmed product terms, not political framing.

Private equity access for retail investors has historically been constrained by high minimums, long lock-ups, and limited transparency, which is precisely why the Canada Strong Fund’s retail product, if well-designed, could represent a structurally different entry point into large-scale private infrastructure and resource equity that is currently unavailable through standard listed vehicles.

Monitor the Spring Economic Update 2026 for retail product specifications before making any capital commitment.

The following sources should be monitored in order of expected information priority:

Investors who already work with an advisor should ask how an illiquid domestic equity product would fit within their existing Canadian asset concentration. A second question worth raising: how would a confirmed principal guarantee change the product’s classification in a portfolio construction context, as bond-like or equity-like?

CIRO-registered advisors will be developing suitability frameworks as product terms are disclosed. Those frameworks should inform any recommendation.

The underlying investment thesis addresses a real structural problem. Canada’s investment productivity gap is documented, the resource base is substantial, and the regulatory reform agenda is tangible. The fund’s design, an arm’s-length Crown corporation investing on a commercial basis, is a credible framework.

The retail product, however, cannot be responsibly evaluated until its terms are confirmed. The principal guarantee question remains the single most important pending detail, and the four specific triggers that should prompt reassessment are: Spring Economic Update 2026 publication, confirmation or denial of the principal guarantee, TFSA/RRSP eligibility status, and fee structure disclosure. Mark Carney’s background at Brookfield Asset Management (with assets held in a blind trust) adds a layer of conflict-of-interest context that investors should note.

It is legitimate to consider participation in part for reasons beyond pure financial return. But that framing should supplement a rigorous review of confirmed product terms, not replace one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding fund returns, product terms, and government policy outcomes are speculative and subject to change based on market developments and policy decisions.

—

The Canada Strong Fund is a Canadian Crown corporation announced on 27 April 2026 by Prime Minister Mark Carney, seeded with CAD $25 billion over three years to take equity stakes in national-priority sectors including energy, critical minerals, agriculture, and infrastructure. It is designed to operate on a fully commercial basis with arm's-length governance, and a retail investment product is planned but not yet finalised as of May 2026.

TFSA and RRSP eligibility for the Canada Strong Fund retail product has not been confirmed as of May 2026. This is one of five material unknowns investors should monitor before making any capital commitment, with the Spring Economic Update 2026 from the Department of Finance expected to provide clarity.

A principal guarantee has been discussed in connection with the Canada Strong Fund but has not been confirmed as of May 2026. If confirmed, it would offer downside protection comparable to a government bond but would not protect against inflation erosion or opportunity cost during any lock-up period.

The three primary risks are portfolio concentration in Canadian strategic sectors already dominant in the TSX, infrastructure illiquidity that could lock up capital for a decade or more, and domestic bias that compounds existing overweight exposure for investors already holding significant Canadian equities. Political interference in project selection is an additional risk supported by precedents such as the Trans Mountain Pipeline cost overrun.

Investors should monitor the Spring Economic Update 2026 from the Department of Finance, which is the primary expected source for retail product specifications, and track updates from the Canada Strong Fund Transition Office. In the meantime, liquid alternatives such as XIU or VDY already provide exposure to Canadian strategic sectors with daily liquidity and confirmed tax status.