What a Random ASX Backtest Reveals About Managing Market Risk

2 hrs ago

Michael Burry, the investor who shorted the US housing market before the 2008 financial collapse, published a warning on his Substack on 8 May 2026 urging investors to reduce technology stock exposure and build cash reserves ahead of what he characterises as a late-stage AI bubble. The warning arrived as the Philadelphia Semiconductor Index (SOX) traded roughly 56% above its 200-day moving average, with major US equity indices sitting at record highs driven almost entirely by appetite for AI-adjacent semiconductor and large-cap technology names. Burry’s fund, Scion Asset Management, has simultaneously disclosed put options on the SOXX ETF with a January 2027 expiration. What follows examines what Burry actually said, what his trade structure reveals, how current valuations compare to dot-com era precedents, and what the warning means in practical terms for US retail investors weighing their own semiconductor exposure.

Burry’s Substack post is paywalled, and the precise wording has not been publicly confirmed. Media outlets characterised the argument in different terms: CNBC (9 May) framed it as “Burry’s ‘end is nigh’ on AI bubble,” Bloomberg (9 May) ran with “Big Short 2.0? Burry buys SOXX puts for 30% drop,” and the Financial Times (10 May) led with “Burry urges cash hoards amid tech mania.” The core thesis, as reported across all three, centred on three actions:

“Big Short 2.0? Burry buys SOXX puts for 30% drop” — Bloomberg, 9 May 2026

The warning carried weight because Burry’s 2008 housing call was not a single lucky bet. It was a documented position held under sustained institutional pressure and investor redemption threats for years before the payoff materialised. That said, honest context requires noting his 2021-2022 warnings of a broader market crash, which proved premature and did not fully materialise on his stated timeline. The market heard him then, waited, and moved higher.

The SOX closed at 11,775.50 on 8 May 2026 and reached 11,885.82 by 11 May. The SOXX ETF, which tracks the index, was trading at approximately $521.68 on 10 May, well above its 52-week low of roughly $445.

What makes the current level historically unusual is the extension above the 200-day moving average. At approximately 56% above that trend line, the SOX sits in territory it has rarely occupied for sustained periods. Burry chose this index rather than the S&P 500 or Nasdaq-100 precisely because the concentration of AI-driven gains is most visible here.

Four names account for a disproportionate share of the index’s 2026 advance.

| Stock | Approximate price (May 2026) | Approximate YTD gain |

|---|---|---|

| NVIDIA (NVDA) | $215.20 | Elevated (unconfirmed %) |

| AMD | $455.19 | ~39% |

| Broadcom (AVGO) | ~$430 | ~22% |

| Arm Holdings (ARM) | $212.79 | ~32% |

NVIDIA short interest remains at approximately 1.1% of float despite Burry’s warning, indicating that institutional investors have not broadly replicated his bearish thesis.

The dot-com comparison is the backbone of Burry’s argument, and the numbers make the parallel visible. Between October 1999 and March 2000, the SOX gained roughly 80% in five months before peaking near 1,500. What followed was an approximately 80% drawdown that erased years of gains.

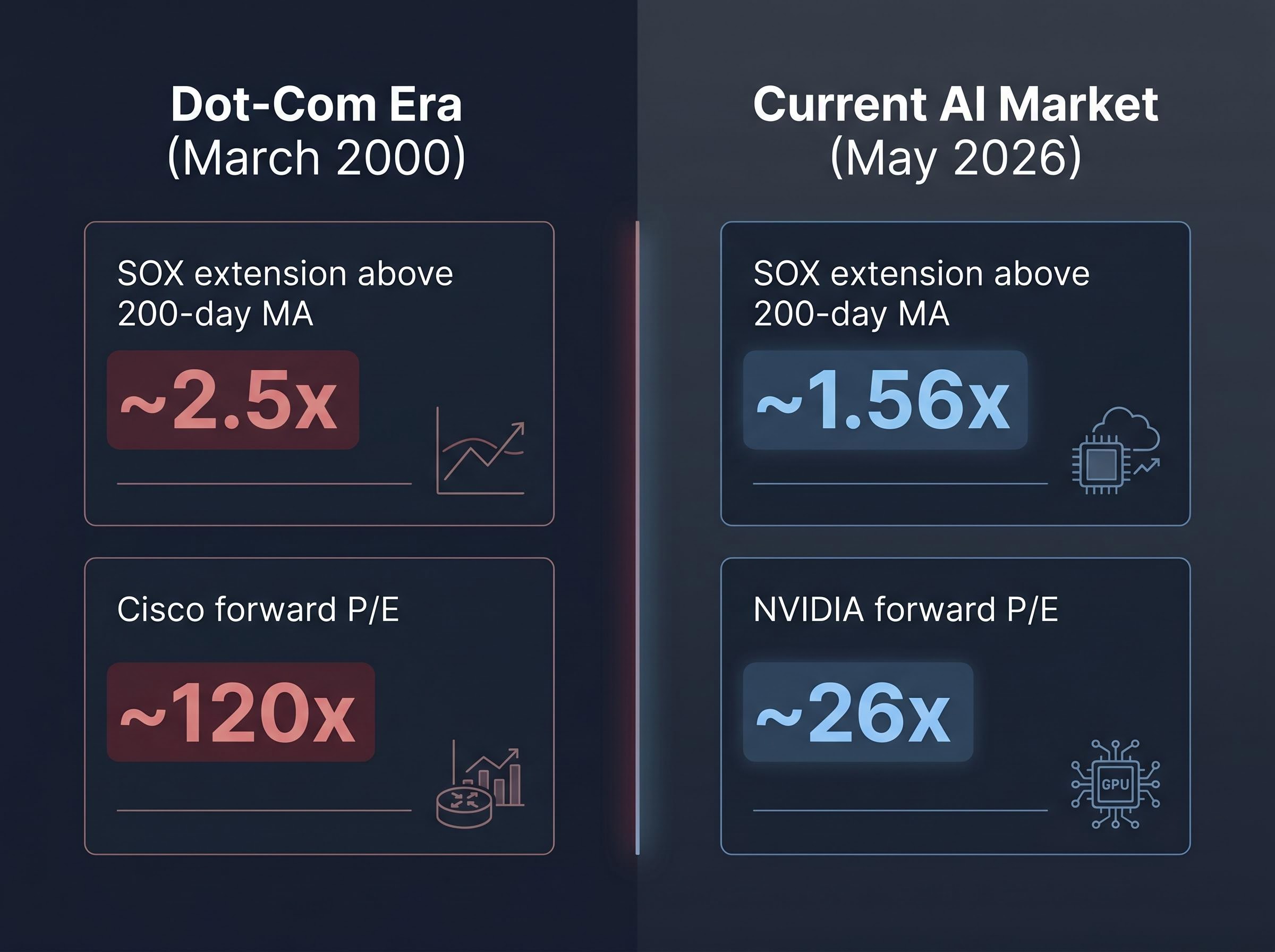

At its 2000 peak, the SOX sat at roughly 2.5 times its 200-day moving average. The current reading of approximately 1.56 times (56% above) is elevated by any historical standard but has not reached that extreme. The gap matters.

Valuations tell a similar story of proportionality. Cisco Systems carried a forward price-to-earnings ratio (forward P/E, a measure of the stock price relative to expected next-year earnings) of approximately 120x at the 2000 peak. NVIDIA’s current forward P/E sits at roughly 26x. AMD trades at a trailing P/E of approximately 75x and Broadcom at roughly 84x, though both figures reflect earnings that have not yet caught up to price appreciation rather than the absence of earnings that defined many dot-com era companies. JDS Uniphase’s approximately 1,800% pre-2000 gain remains the extreme comparison case, and no current semiconductor name has approached that trajectory.

Forward and trailing P/E ratios measure different things and can diverge sharply when earnings are recovering rapidly: a trailing P/E reflects the past four quarters of actual earnings while a forward P/E discounts the next year’s projected earnings, which explains why AMD at approximately 75x trailing can appear expensive even as analysts project a significant compression of that multiple over the next 12 months.

| Metric | Dot-com era (March 2000) | Current (May 2026) |

|---|---|---|

| SOX extension above 200-day MA | ~2.5x | ~1.56x |

| Flagship forward P/E (Cisco / NVIDIA) | ~120x | ~26x |

| SOX gain in 5 months prior to peak | ~80% | Elevated (unconfirmed %) |

Goldman Sachs strategists noted on 30 April 2026 that “AI valuations are elevated but supported by approximately 30% EPS growth; no 2000-style bubble without capex slowdown.”

The analogy is real but imperfect. The altitude is genuine; the question is whether the earnings underneath it are genuine too.

The counterarguments carry institutional weight and specific data, and retail investors weighing their own positions should hold both sides of this debate simultaneously.

Goldman Sachs semiconductor revenue forecasts project a 49% surge in global revenues by end of 2026, with AI-related hardware potentially reaching over $700 billion in Q4 2026 alone, providing a concrete earnings floor that strategists argue distinguishes the current cycle from the revenue-absent environment of 2000.

SOXX short interest stands at approximately 5.2% of float as of May 2026, up 15% month over month. Growing, but still modest. Reuters reported on 9 May that Citadel and Millennium added NVIDIA call options during the month, suggesting the largest institutional players remain positioned for further upside.

Burry warned of a broader market correction in 2021 and again in 2022. Both proved premature. The market sold off in 2022 but recovered on a timeline that did not reward the short thesis as structured.

The honest question is not whether Burry is wrong. It is whether he is early again, and whether an investor can afford to wait for his timeline to play out while holding positions that could move significantly in either direction.

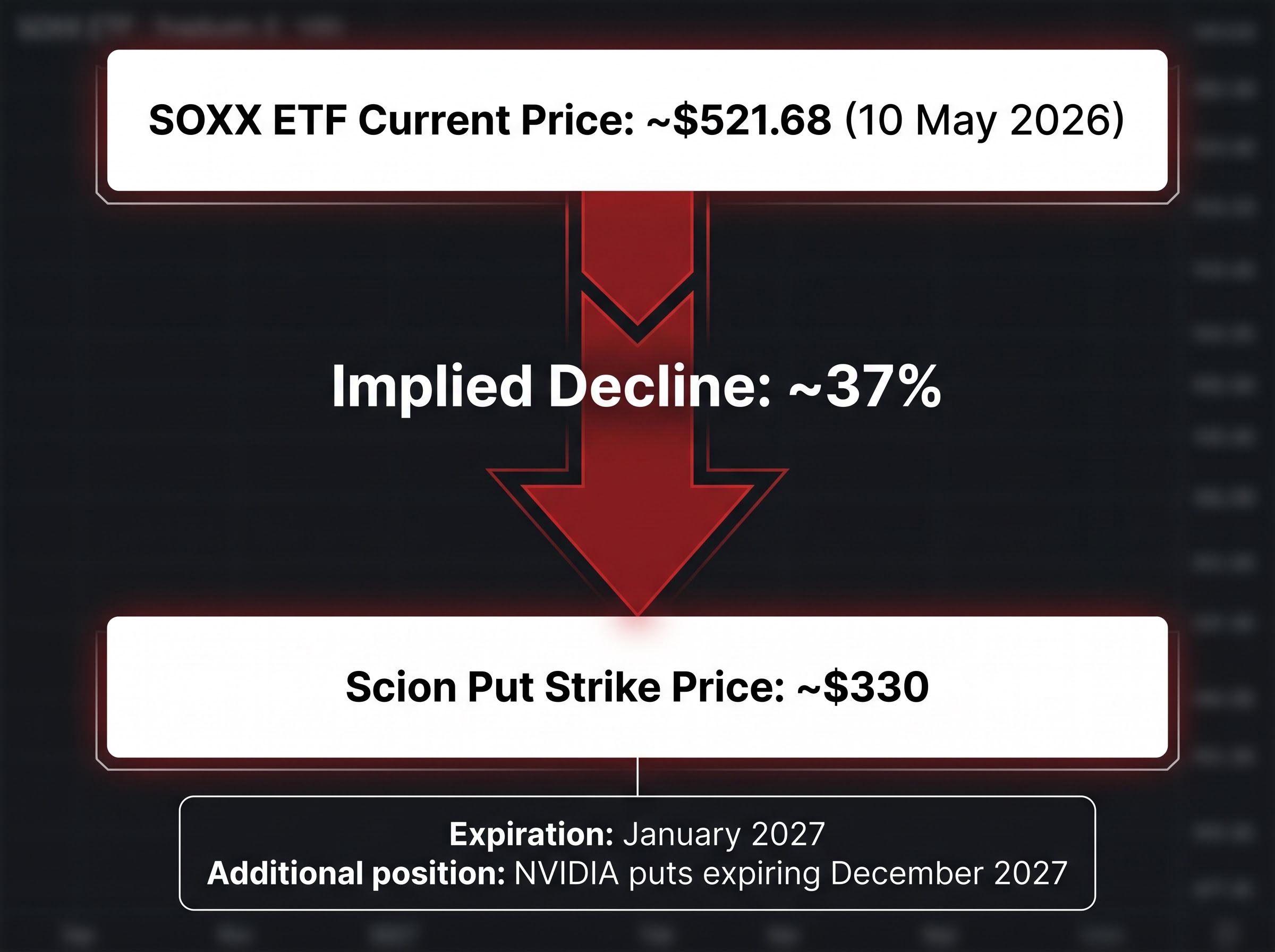

The most practically useful signal in this story is not the Substack warning itself but the structure of Scion’s disclosed position. The fund holds put options on the SOXX ETF with a January 2027 expiration and a strike price of approximately $330, per its recent 13F filing. With SOXX trading near $521.68, the $330 strike represents a bet on a decline of roughly 37% from current levels. Scion also holds NVIDIA puts expiring December 2027.

SEC Form 13F reporting requirements obligate institutional investment managers with over $100 million in qualifying assets to disclose equity holdings including put and call options on a quarterly basis, which is why Scion’s SOXX and NVIDIA put positions became publicly visible and reportable by media outlets.

This is a leveraged professional trade with a defined risk window. Burry himself stated in his Substack post that short selling is “not appropriate for most individual investors” and that put options are currently expensive.

Implied volatility in semiconductor options rises materially ahead of earnings events as demand for hedging increases, and with SOXX puts currently expensive by Burry’s own characterisation, the volatility premium embedded in those contracts is itself a cost that retail investors would absorb if they attempted to replicate the trade structure.

“Short selling is not appropriate for most individual investors.” — Michael Burry, Substack, 8 May 2026

Retail investors who feel compelled to act on the warning have simpler risk-management responses available:

Replicating Burry’s trade is not his message. Building awareness of portfolio concentration is.

The SOX sits 56% above its 200-day moving average. That is a fact both sides of this debate acknowledge. Burry’s directional argument about historical elevation is supported by the data even if his timing is contested by institutional voices citing 30% earnings growth and a $1 trillion data centre capex cycle that did not exist in 2000.

Neither argument is frivolous. The decision facing retail investors is whether to remain fully exposed to a sector trading at historically elevated extensions with full awareness of the dot-com precedent, or to reduce exposure and accept the cost of potentially early positioning.

Reviewing semiconductor and technology weighting against stated risk tolerance, rather than reacting to a single headline, remains the most defensible starting point. Burry’s prior record suggests he deserves serious attention; it also suggests that attention should include the full timeline, not just the calls that proved correct.

Investors exploring the structural question in greater depth will find our full explainer on AI bubble frameworks, which applies Minsky’s financing stages, the Shiller CAPE, Hussman’s GVA metric, and behavioural indicators to the current AI cycle, and includes specific portfolio actions around rebalancing and auditing Magnificent Seven concentration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Michael Burry published a Substack warning on 8 May 2026 urging investors to reduce technology and semiconductor stock exposure and build cash reserves, arguing the AI-driven rally shows characteristics of a late-stage bubble similar to the dot-com era of 1999-2000.

Scion Asset Management disclosed put options on the SOXX ETF with a January 2027 expiration and a strike price of approximately $330, representing a bet on a roughly 37% decline from the ETF's May 2026 trading price of around $521.68; the fund also holds NVIDIA puts expiring December 2027.

The Philadelphia Semiconductor Index currently trades approximately 56% above its 200-day moving average, compared to roughly 2.5 times (150% above) at the March 2000 peak, and NVIDIA's forward P/E of around 26x is far below Cisco's approximately 120x forward P/E at the dot-com peak.

Goldman Sachs argued on 30 April 2026 that approximately 30% earnings-per-share growth in AI-linked companies provides a fundamental floor absent in 2000, while analysts also point to a roughly $1 trillion data centre spending cycle as a concrete earnings anchor that distinguishes today's market from the dot-com era.

Burry himself stated that short selling and put options are not appropriate for most individual investors; instead, retail investors can trim overweight semiconductor allocations back to stated portfolio targets, set stop-loss levels on individual holdings, and consult a financial adviser before considering any derivative exposure.