Barclays Warns of Prolonged Market Volatility Under New Fed Reality

14 hrs ago

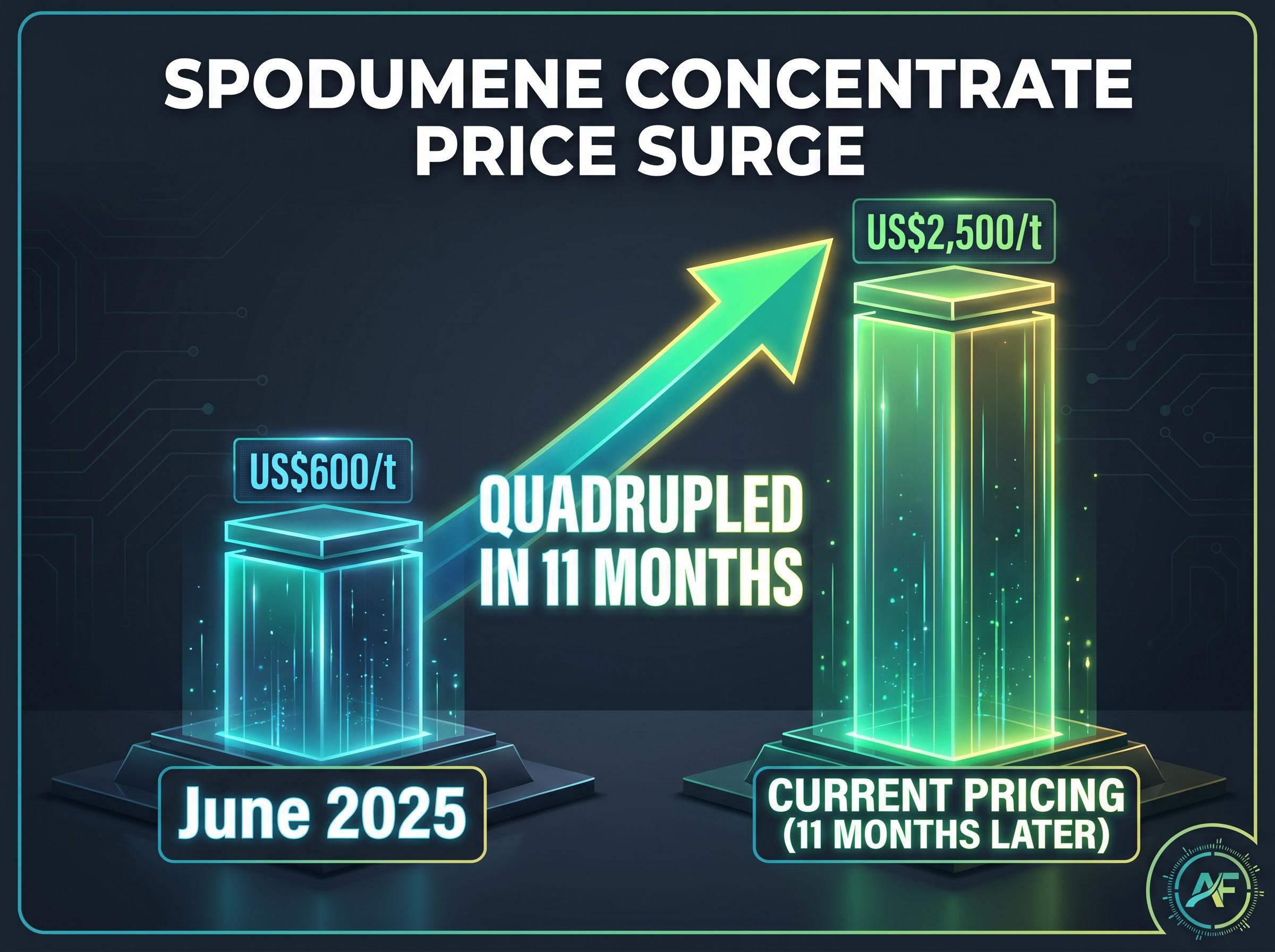

Spodumene concentrate has roughly quadrupled since June 2025, climbing from approximately US$600 per tonne to US$2,500 per tonne in eleven months. ASX lithium stocks are now catching up. During the week ending 8 May 2026, Pilbara Minerals, Liontown Resources, Mineral Resources, IGO Limited, and Rio Tinto all reached new 52-week highs, with Liontown up more than 400% over the past year. The surge arrived as the broader ASX consumer discretionary and healthcare sectors collapsed, a divergence that signals a deliberate rotation into hard commodities rather than broad-market optimism. What follows explains the commodity price recovery underpinning the rally, the structural demand shift that distinguishes this cycle from the last, the supply constraints sustaining elevated prices, and the specific risks investors face at current valuations.

The numbers speak before the narrative does. Five of the ASX’s most-traded resources names closed the week ending 8 May 2026 at fresh 52-week highs, with year-over-year gains ranging from +49% to +413%.

| Ticker | Close Price (A$) | Weekly Move (%) | YoY Move (%) | 52-Week Status |

|---|---|---|---|---|

| PLS | $6.26 | +2.0% | ~+250% | New 52-week high |

| LTR | $2.45 | ~+2% | +412.6% | New 52-week high |

| MIN | $69.55 | +4.3% | +177.8% | New 52-week high |

| IGO | $8.46 | +10.0% | N/A | New 52-week high |

| RIO | $178.72 | +3.9% | +49.1% | New 52-week high |

IGO was the strongest weekly performer among major lithium names at +10%. Liontown recorded a -7.2% pullback on the week itself, though this occurred from already elevated levels after its +413% yearly gain. Rio Tinto’s close of $178.72 marked a fresh 52-week high but remains below its 2022 ASX record near $190.

The materials sector logged 5 new 52-week highs against just 1 new low during Week 20, the strongest ratio of any ASX 200 sector. By contrast, consumer discretionary posted 9 new 52-week lows and the healthcare sector continued its retreat, including a 17% single-session drop in CSL on a guidance downgrade. The divergence is a sector-level re-rating, not a collection of isolated stock moves.

The sector rotation into lithium that defined Week 20 did not emerge without precedent: the prior week ending 1 May 2026 had already seen eleven ASX 200 names reach new 52-week highs led by Liontown, Pilbara Minerals, and Mineral Resources, against a backdrop of twenty-two constituents hitting annual lows and Australia’s CPI climbing to 4.6% in March 2026.

The stock prices are reflecting something real in the underlying commodity market. As at 8 May 2026, all three lithium commodity classes sit at their highest levels since mid-2023:

Lithium carbonate in 2026: +45% year-to-date, at its highest level since mid-2023.

The recovery is real, but context matters. Lithium carbonate peaked near US$40,000/t during the 2022-2023 supercycle. Current prices remain roughly 35% below that level. Pilbara Minerals’ share price, at $6.26, sits approximately 16% above its own 2023 high, meaning the equity has already priced in more of the recovery than the commodity itself has delivered. Understanding that gap is the difference between recognising a structural recovery and chasing a speculative overshoot.

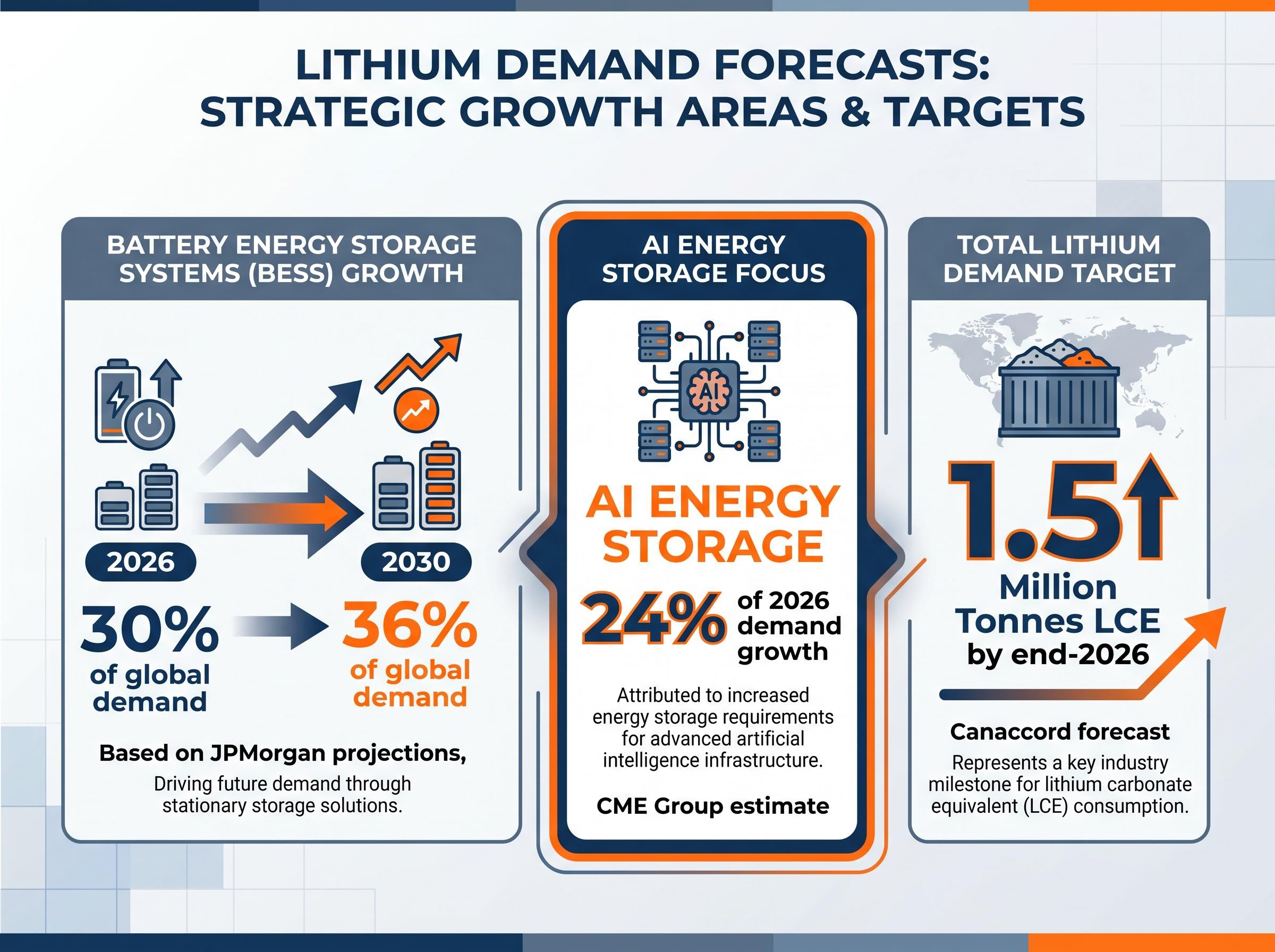

The last lithium boom was an electric vehicle story. This one is not, or at least not exclusively. Battery energy storage systems (BESS), which are large-scale battery installations used to store and dispatch electricity for grid stability, have emerged as the single most important new demand driver. The distinction matters because BESS demand is tied to infrastructure investment cycles, which tend to be longer and less sensitive to consumer sentiment than vehicle sales.

JPMorgan projects that energy storage will represent 30% of global lithium demand in 2026, rising to 36% by 2030, according to analysis published via Firstlinks.

JPMorgan BESS projection: Energy storage to account for 30% of global lithium demand in 2026, rising to 36% by 2030.

Three demand drivers are sustaining the current cycle, ranked by current scale:

Geoscience Australia’s critical minerals framework, which underpins the national Critical Minerals Strategy 2023-2030, formally classifies lithium as a strategic resource on the basis of its role in national security and clean energy transition, giving ASX-listed lithium producers a policy tailwind that did not exist with the same force during the 2022-2023 supercycle.

Canaccord forecasts approximately 15% demand growth to around 1.5 million tonnes of lithium carbonate equivalent (LCE) by end-2026. A demand base anchored in energy infrastructure rather than consumer vehicle adoption alone carries a different risk profile, one that is less vulnerable to economic cycle downturns.

Demand alone does not explain why prices have stayed elevated. The supply side has been equally important in sustaining the rally.

CATL’s Jianxiawo (Yichun) lithium mine restart is the key supply normalisation variable. The mine’s return to production had previously weighed on market sentiment, and its full ramp-up remains a factor that could moderate future pricing. No confirmed restart timeline is available in current reporting. If the mine returns to full capacity while other curtailments ease, the supply-side support for current prices narrows.

Corporate deal activity is often the strongest signal that large-balance-sheet players view current commodity prices as durable enough to justify long-dated asset acquisition. Source data for the week ending 8 May 2026 references corporate actions involving Atlantic Lithium and European Lithium.

A verification caveat is warranted: specific deal terms and announcement details for these two entities have not been independently confirmed via ASX announcements as at the time of writing. Investors should check the ASX announcements database directly before acting on M&A-related positioning.

The lithium M&A deal specifics for Atlantic Lithium and European Lithium include confirmed transaction values of US$285 million and US$835 million respectively, with Zhejiang Huayou Cobalt and Critical Metals as the acquiring parties, details that place the strategic capital conviction behind the sector rally on firmer ground than deal rumour alone.

The gap between bearish calls and market reality: UBS’s last confirmed action on Pilbara Minerals was a Sell rating with a $2.25 price target in September 2025. PLS closed at $6.26 on 8 May 2026, nearly three times that target.

Consensus tells a different story. PLS carries a Moderate Buy rating across 16 analysts tracked by CommSec, while MIN holds a Moderate Buy across 15 analysts. M&A acceleration at this stage of the commodity cycle is consistent with late-discovery-phase behaviour, where producers move to secure resource assets before prices climb further.

The macro thesis is sound. The individual equity valuations are a separate question entirely.

Liontown’s +412.6% year-over-year gain dwarfs the underlying lithium carbonate recovery of +150% over the same period. That gap represents an equity premium built on expectations that prices will continue rising, and premiums of that magnitude compress violently when expectations shift. PLS sits approximately 16% above its own 2023 high, which implies the market is already pricing this recovery as more durable than the last one.

The specific risk factors at current levels:

Investors weighing position sizing after a multi-week rally will find our deep-dive into ASX lithium technical signals useful: it examines momentum indicators for PLS, LTR, and CXO individually, maps the gap between commodity price recovery and equity pricing across each name, and covers the Global X Battery Tech and Lithium ETF (ASX: ACDC) as a diversified alternative to single-stock concentration.

For investors who have already initiated positions, the BESS-led demand shift, ongoing supply constraints, and institutional ETF flows through VOLT provide a credible medium-term floor for the thesis. The demand base is broader and more infrastructure-linked than in 2022-2023, which lends the recovery more structural support than the prior cycle enjoyed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The week’s divergence, viewed at sector level, reveals a capital rotation with clear macro logic behind it:

That ratio is not a coincidence. Hard assets historically attract capital when nominal growth is uncertain, and the combination of elevated geopolitical risk and accelerating infrastructure spending is funnelling institutional money toward resources at the expense of consumer-facing sectors. NRW Holdings (ASX: NWH), an industrials infrastructure name, reinforced the theme with a +9.2% weekly gain and +142.4% year-over-year performance.

For investors who prefer diversified exposure rather than single-stock concentration risk, the VOLT ETF, launched in April 2026, provides institutional-grade access to the lithium miners basket on the ASX. The sector rotation data confirms that the lithium and resources rally reflects a real shift in capital allocation, not momentum chasing in a single commodity.

Commodity supercycle valuation multiples provide a useful anchor for calibrating how much re-rating potential remains: major mining companies currently trade at roughly 7-8x EV/EBITDA versus approximately 14x during the 2008-2010 boom, a gap that supports the bull case but also illustrates how quickly crowded institutional positioning can compress returns if the demand thesis wobbles.

—

Spodumene concentrate is a lithium-bearing mineral extracted from hard rock deposits and sold as a feedstock for lithium chemical production. Its price directly drives revenue and margins for ASX producers like Pilbara Minerals, so a rise from US$600 per tonne in June 2025 to US$2,500 per tonne by May 2026 translates materially into higher earnings expectations and share price re-ratings.

The 2026 rally is underpinned by a broader demand base than the prior cycle, with battery energy storage systems (BESS) for grid-scale renewable infrastructure now accounting for an estimated 30% of global lithium demand alongside EV growth, while supply curtailments in China and Zimbabwe have kept prices elevated rather than allowing a rapid reversal.

Pilbara Minerals (PLS), Liontown Resources (LTR), Mineral Resources (MIN), IGO Limited (IGO), and Rio Tinto (RIO) all reached new 52-week highs during the week ending 8 May 2026, with year-over-year gains ranging from approximately 49% for Rio Tinto to over 412% for Liontown.

VOLT is the ETFS Global Lithium Miners ETF launched on the ASX in April 2026, offering diversified exposure to a basket of lithium mining companies rather than concentrating risk in a single stock, making it a lower-volatility alternative for investors seeking participation in the lithium sector rally.

The main risks include equity valuations that have already moved well ahead of underlying commodity prices (Liontown is up over 400% year-over-year versus lithium carbonate up 150%), the historical boom-bust pattern in lithium pricing, potential supply normalisation if curtailed mines such as CATL's Jianxiawo operation restart, and broader macro deterioration affecting portfolio-level risk across the ASX.