Is Fiserv at $47 a Value Trap or a Deep-Value Opportunity?

20 mins ago

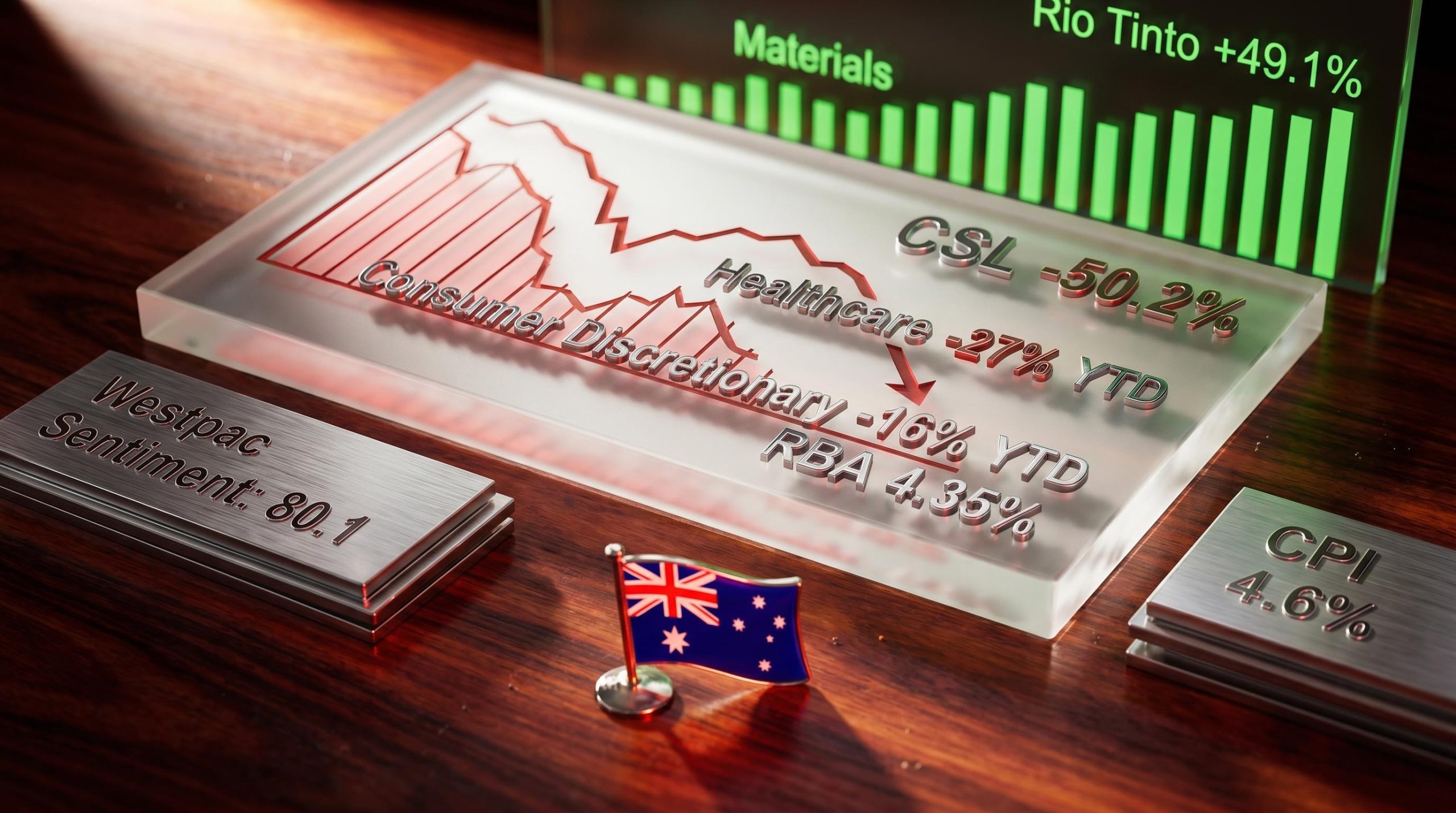

CSL shed 17% in a single session the same week the Reserve Bank of Australia delivered its third consecutive rate hike of 2026. Australia’s largest healthcare company and the central bank collided on the same timeline, and the damage spread fast. By 8 May 2026, the ASX 200 Consumer Discretionary Index had fallen 16% year to date to its weakest level since May 2024, while the healthcare sector was down 27% YTD, with every major constituent simultaneously sitting at 52-week lows. This is not isolated stock volatility; it is sector-level deterioration driven by identifiable and compounding forces. What follows maps exactly which stocks are at multi-year lows, explains the three-layer pressure system driving the selloff, and identifies what the unusual breadth of 52-week lows across six sectors signals for the wider ASX 200.

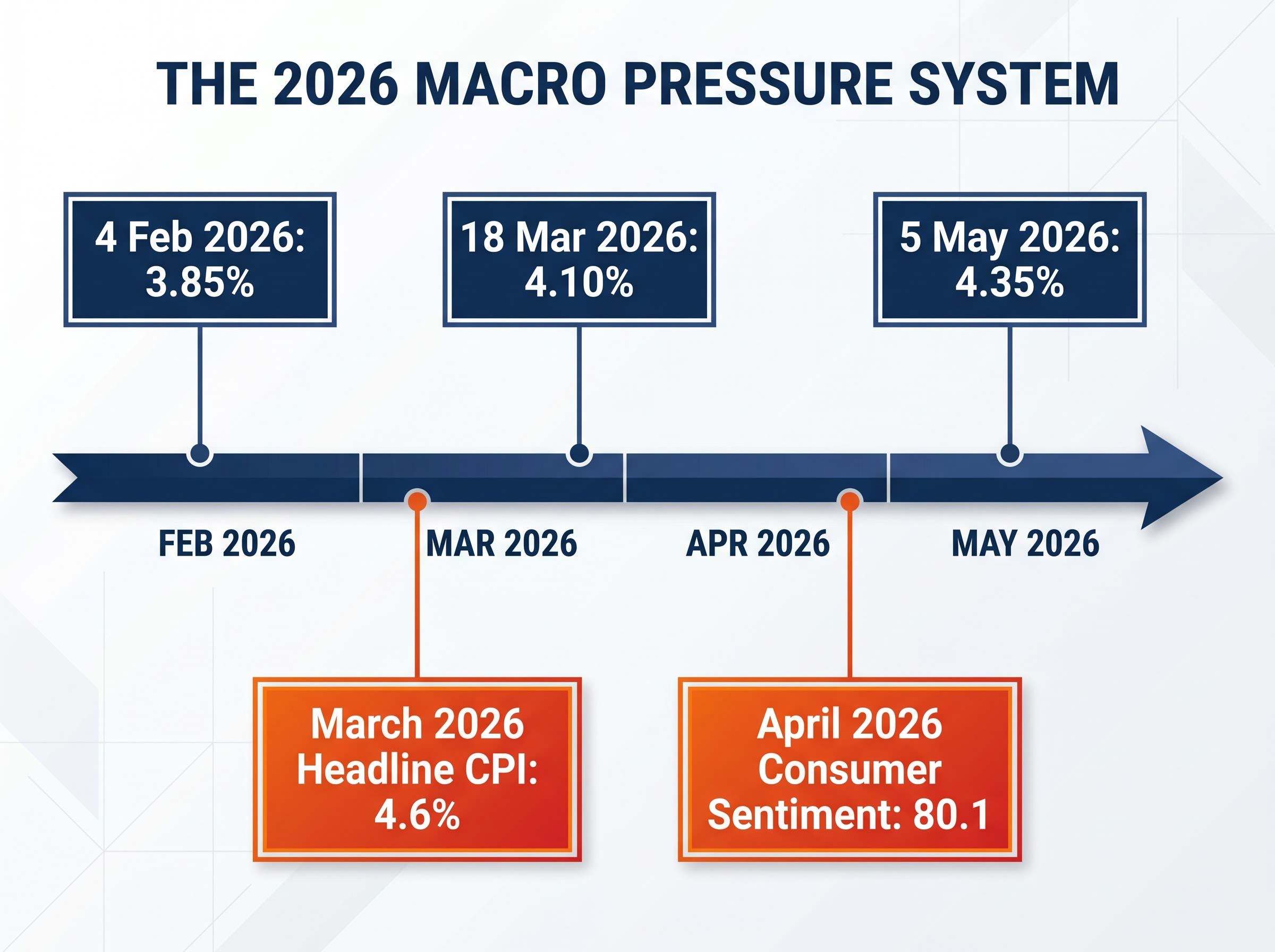

The pressure on Australian households arrived in layers, and each layer compounded the one before it. The RBA’s tightening sequence in 2026 has been steady and unrelenting:

That is 75 basis points of cumulative tightening in three months. Each hike ratcheted up mortgage repayments and business borrowing costs, compressing disposable income before consumers even reached the checkout.

Inflation data released on approximately 29 April 2026 confirmed why the RBA kept tightening. Headline CPI came in at 4.6% year on year for March 2026, with the trimmed mean measure at 3.3% annually. Both readings sit well above the RBA’s 2-3% target band, with petrol price spikes identified as a specific contributor. Real purchasing power is being eroded at the same time borrowing costs are rising.

The fuel and electricity price surge sitting behind the 4.6% CPI print was not a single-category event: a 32.8% monthly spike in fuel costs driven by Brent crude reaching $110-$120 per barrel combined with a 25.4% electricity price increase, and construction cost acceleration that signals shelter inflation could compound well into 2027.

The ABS Consumer Price Index release for March 2026 confirmed headline inflation at 4.6% annually and a trimmed mean of 3.3%, both readings sitting above the RBA’s target band and providing the statistical foundation for the central bank’s decision to continue tightening at its May meeting.

Westpac-Melbourne Institute Consumer Sentiment Index: 80.1 in April 2026, down 12.5% month on month. Any reading below 100 signals net pessimism.

Consumer confidence collapsed before the CSL announcement, before the latest rate hike, and before the worst of the discretionary sector’s selloff. The sentiment reading tells investors that household spending capacity was already under severe strain. The May 2026 consumer sentiment data was not yet published as of 11 May 2026, meaning the full impact of the third rate hike on confidence remains unmeasured.

The Westpac-Melbourne Institute Consumer Sentiment Bulletin for April 2026 documented the 12.5% monthly decline to 80.1, noting that the deterioration was broad-based across all five index components, with family finances over the next 12 months and economic conditions over the next five years recording the steepest falls.

CSL fell approximately 17% in a single session following its FY26 guidance downgrade, announced around 5 May 2026. The stock closed at $119.88, marking a 50.2% decline over the prior year and an approximately 43% drop year to date. For a company of CSL’s index weight, a move of that magnitude does not stay contained.

The damage extended across every major ASX 200 healthcare constituent. As of 8 May 2026, each of the following names sat at a 52-week low simultaneously:

| Stock | ASX Code | Closing Price (8 May 2026) | 1-Year Return |

|---|---|---|---|

| CSL | CSL | $119.88 | -50.2% |

| Sonic Healthcare | SHL | $18.94 | -29.0% |

| ResMed | RMD | $28.56 | -25.4% |

| Ansell | ANN | $26.42 | -18.2% |

| Fisher and Paykel Healthcare | FPH | $29.00 | -12.4% |

The healthcare sector’s year-to-date decline of approximately -27% makes it the worst-performing major sector on the ASX in 2026. CSL’s collapse dragged on every fund and ETF with healthcare exposure, but the table above shows the weakness was already embedded across the sector’s largest names.

The defensive label attached to healthcare stocks by conventional portfolio theory does not survive contact with the XHJ’s 39% 12-month decline: Cochlear’s April 2026 guidance reset, which cut FY26 profit forecasts by 30-35% and triggered a single-session fall of approximately 35-39%, demonstrated that elective healthcare demand is consumer-confidence-sensitive in a way that the defensive classification systematically obscures.

The operational drivers behind the 17% single-session move centred on excess inventory pressures and a substantial impairment charge. CSL revised its FY26 guidance to revenue of approximately $15.2 billion and net profit after tax and amortisation (NPATA) of approximately $3.1 billion. The company flagged impairment charges in the range of $5-$7 billion, attributed to inventory build-up issues.

This is a significant distinction for investors. The downgrade was driven by inventory cycle and balance sheet impairments, not a collapse in underlying demand for CSL’s products. Whether the market treats this as a recoverable operational issue or a structural concern will determine the stock’s trajectory from here. Morgan Stanley maintains a Buy rating on Pro Medicus (PME) with a $200 price target, while Morgans holds an Add rating with 46% implied upside on a healthcare name, suggesting at least some institutional conviction that the selloff has overshot in parts of the sector.

The S&P/ASX 200 Consumer Discretionary Index fell 16% year to date by May 2026, reaching its weakest point since May 2024. The breadth of individual stocks hitting 52-week lows during the week of 8 May 2026 tells the fuller story.

| Stock | ASX Code | Closing Price (8 May 2026) | 1-Year Return |

|---|---|---|---|

| IDP Education | IEL | $2.83 | -71.5% |

| Temple and Webster | TPW | $5.93 | -69.2% |

| ARB Corporation | ARB | $18.66 | -43.6% |

| Nick Scali | NCK | $14.64 | -22.5% |

| Flight Centre | FLT | $10.74 | -21.8% |

| Super Retail Group | SUL | $11.60 | -18.9% |

| Harvey Norman | HVN | $4.48 | -17.7% |

| Light and Wonder | LNW | $114.64 | -15.8% |

| Wesfarmers | WES | $72.25 | -9.9% |

All nine stocks hit 52-week lows as of 8 May 2026. The list spans online retail, education, automotive accessories, furniture, travel, sporting goods, electronics-adjacent retail, gaming, and conglomerates. When names as structurally different as IDP Education and Wesfarmers are hitting new lows in the same week, the signal is sectoral rather than idiosyncratic. This is a market repricing demand risk across the full consumer spectrum.

The macro data describes the pressure. Corporate commentary from late April to early May 2026 confirms where and when it arrived.

Accent Group reported that trading through the end of March was consistent with prior guidance, but late-March geopolitical escalation drove higher fuel prices and a material decline in consumer confidence. April sales and gross margins were both negatively affected.

Endeavour Group noted that after a solid start to the third quarter, Hotels segment sales growth began decelerating in March across all revenue categories, including food, beverages, gaming, and accommodation.

JB Hi-Fi flagged significant cost pressures from supplier component pricing, inventory availability constraints, and intensified competitive conditions.

Three very different consumer-facing businesses, footwear retail, hospitality and gaming, consumer electronics, all identified the same inflection point: late March 2026. The timing aligns precisely with the second RBA rate hike on 18 March and the subsequent collapse in consumer sentiment. These are not forecasts or analyst projections; they are observations from management teams describing trading conditions they were living through.

Per capita recession conditions were embedded in the economy before the May rate hike cycle accelerated: corporate insolvencies reached approximately 12,000 in 2025, the highest since the 1990-91 recession, real wages declined roughly 0.3% as wage growth failed to keep pace with CPI, and consumer confidence had already fallen to a 50-year low by late March 2026.

The convergence of this commentary around a single period gives the macro thesis operational credibility. The deterioration was not gradual. It arrived in a compressed window and hit across categories.

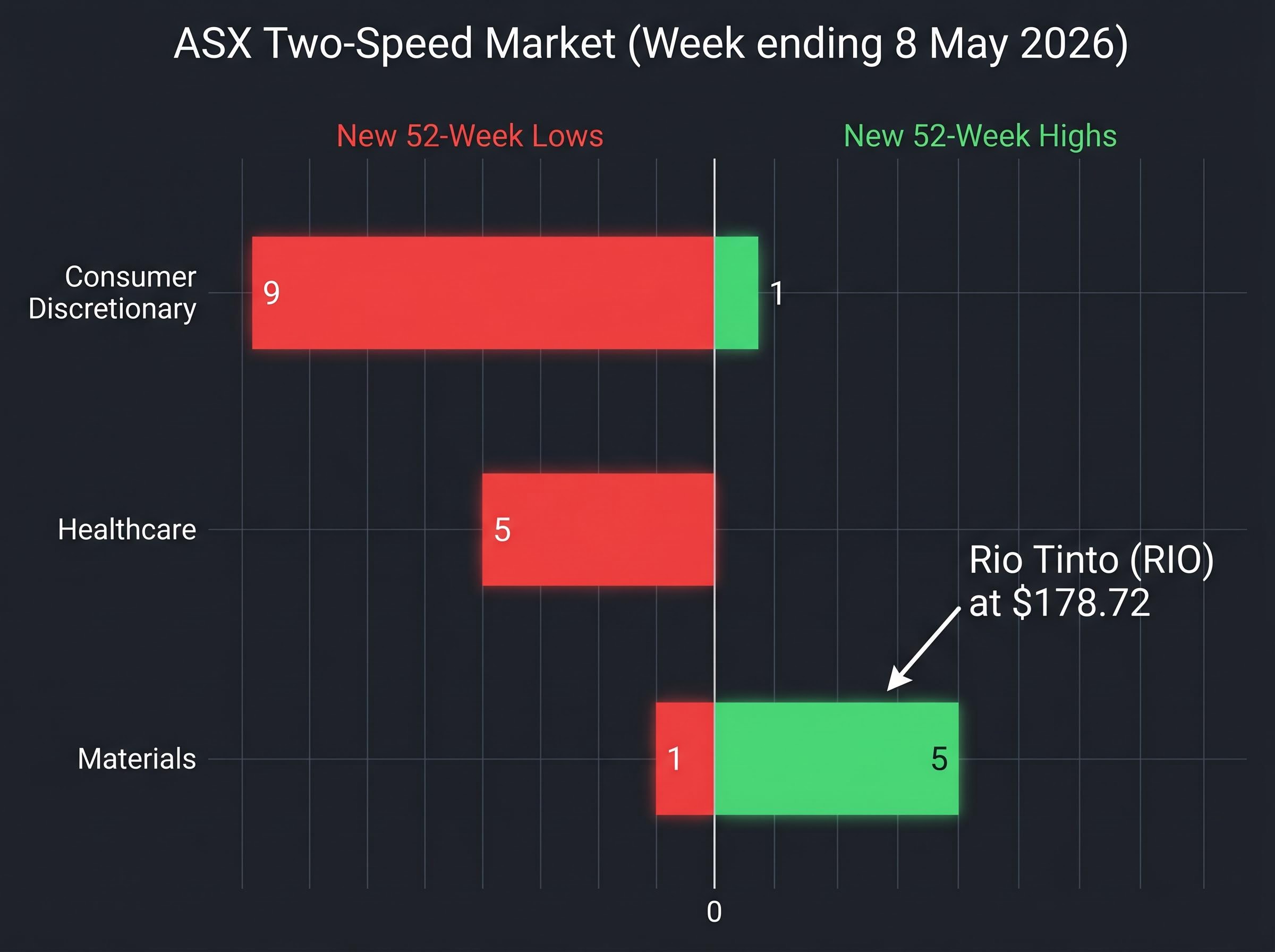

Healthcare and consumer discretionary absorbed the heaviest losses, but the breadth data from Week 20 (ending 8 May 2026) shows the weakness extended further.

| Sector | New 52-Week Highs (Week 20) | New 52-Week Lows (Week 20) |

|---|---|---|

| Consumer Discretionary | 1 | 9 |

| Healthcare | 0 | 5 |

| Materials | 5 | 1 |

| Industrials | 3 | 2 |

| Consumer Staples | 0 | 2 |

| Real Estate | 0 | 1 |

| Technology | 1 | 1 |

| Telecommunications | 0 | 1 |

| Energy | 1 | 0 |

| Financials | 1 | 0 |

| Utilities | 1 | 0 |

Beyond the headline sectors, new 52-week lows appeared across industrials, materials, real estate, staples, technology, and telecommunications. Specific names include:

The contrast, however, is where the signal sharpens. Materials recorded 5 new 52-week highs against just 1 new low. Rio Tinto (RIO) closed at $178.72, up 49.1% over the prior year and at an all-time high. NRW Holdings (NWH) reached $7.03, up 142.4% over the prior year. Gold has risen approximately 110% year to date. Capital is not leaving the ASX. It is rotating within it, and the direction of that flow is measurable.

The evidence from macro data, sector returns, corporate commentary, and breadth readings converges on a single pattern: the ASX 200 weakness in May 2026 is concentrated in rate-sensitive and consumer-facing sectors, while commodity-linked and infrastructure-adjacent names are actively absorbing reallocated capital. The ASX 200 is down approximately 16% year to date, but that headline figure masks a two-speed market.

For pressure on healthcare and consumer discretionary to ease, two conditions would need to change:

Analyst counterpoint: Morgan Stanley holds a Buy rating on Pro Medicus (PME) with a $200 price target, implying approximately 55% upside from the current price range of $129-$136. Morgans maintains an Add rating on a healthcare name with 46% implied upside.

These selective buy calls suggest institutional conviction that the selloff has overshot in specific names. The macro backdrop has not yet provided a catalyst for sector-wide reversal, but the divergence between price and analyst targets is widening.

For investors assessing whether the healthcare selloff can fully reverse once the RBA pauses, our deep-dive into US structural policy risk for ASX healthcare examines the FDA instability under Commissioner Marty Makary and the RFK Jr.-led reorientation of HHS away from infectious disease prevention, risks that carry no natural cyclical reversal point and sit outside the rate and currency frameworks that most recovery scenarios rely on.

The weakness in ASX healthcare and consumer discretionary stocks in May 2026 reflects a specific set of macro pressures: three consecutive RBA rate hikes totalling 75 basis points, headline inflation at 4.6%, consumer confidence at 80.1, and the CSL guidance downgrade acting as an accelerant on a sector already under strain. This is not a generalised market collapse.

The breadth data confirms a two-speed story. The same week that produced 14 combined new lows in healthcare and discretionary also produced 11 new highs across materials, industrials, energy, financials, and utilities. Rio Tinto hit an all-time high. Gold climbed approximately 110% year to date. NRW Holdings more than doubled.

The operative concern for investors in May 2026 is sector concentration risk. Portfolios overweight in healthcare and consumer discretionary have absorbed substantial damage. Those with materials and infrastructure exposure have outperformed. Understanding where capital is flowing, and under what conditions the current losers could recover, is the actionable distinction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The ASX market weakness in May 2026 is driven by three consecutive RBA rate hikes totalling 75 basis points, headline CPI of 4.6%, a consumer sentiment index of 80.1, and the CSL guidance downgrade that triggered a 17% single-session fall and spread pressure across the entire healthcare sector.

Healthcare is the worst-performing major ASX sector in 2026, down approximately 27% year to date, followed by consumer discretionary, which fell 16% year to date to its weakest level since May 2024, with every major healthcare constituent simultaneously sitting at 52-week lows as of 8 May 2026.

CSL fell approximately 17% in one session after the company revised its FY26 guidance to revenue of around $15.2 billion and NPATA of approximately $3.1 billion, while also flagging impairment charges in the range of $5-$7 billion attributed to inventory build-up issues rather than a collapse in underlying product demand.

Materials, energy, financials, and utilities are recording new 52-week highs during the same week that healthcare and consumer discretionary hit multi-year lows; Rio Tinto reached an all-time high, NRW Holdings more than doubled over the prior year, and gold climbed approximately 110% year to date, signalling a rotation within the ASX rather than a broad capital exodus.

A recovery in these sectors would require the RBA to signal a pause or reversal in its tightening cycle from the current cash rate of 4.35%, and consumer confidence would need to recover above the pessimism threshold of 100 on the Westpac-Melbourne Institute index, which stood at a deeply pessimistic 80.1 in April 2026.