Why a Rising AUD Is Quietly Eroding Your International ETF Returns

11 hrs ago

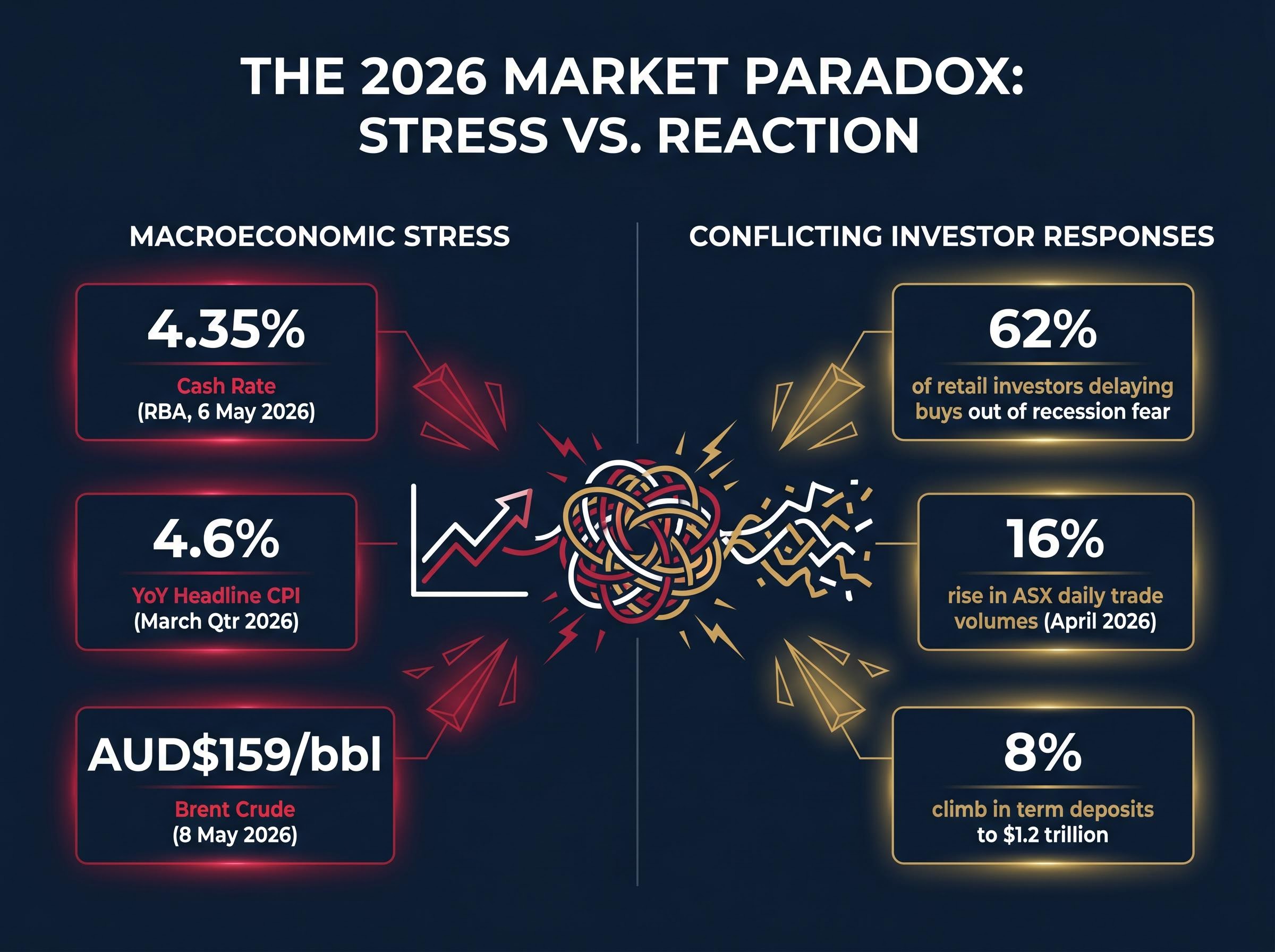

The RBA raised the cash rate to 4.35% on 6 May 2026. Brent crude is trading near AUD$159 per barrel. Headline inflation printed at 4.6% year-on-year in the March quarter. And yet, ASX retail trading volumes climbed 16% year-on-year in April. Australian investors are not sitting still. The question is whether activity and strategy are the same thing. This guide, informed by the behavioural and structural investing principles outlined by Scott Phillips on the nabtrade Your Wealth podcast on 11 May 2026, sets out what pre-commitment means in practice, why certain businesses outperform under stress, and what Australian retail and SMSF investors can do now to protect and grow their portfolios through disciplined, foundational investing strategies.

Activity feels productive. In volatile markets, it rarely is.

The Australian economy is under genuine macroeconomic stress across three fronts:

This is not routine volatility. It is a multi-vector stress environment that tests both portfolios and the people managing them.

The Hormuz strike selloff on 8 May 2026 illustrates exactly how rapidly a single geopolitical event can transmit through two simultaneous channels, surging bond yields and an oil price spike, to erase an estimated $100 billion in Australian market capitalisation in a single session despite Wall Street closing higher overnight.

The behavioural response has been telling. ASX daily trade volumes rose 16% in April 2026 (ASX Group Monthly Activity Report), yet a nabtrade Investor Pulse Survey from the same month found 62% of retail investors citing fear of recession as a reason to delay new purchases. Net flows into term deposits climbed 8% to $1.2 trillion, according to RBA data.

62% of retail investors cited fear of recession as delaying new buys, yet ASX daily trade volumes were up 16% in April 2026.

The two impulses, overtrading and freezing, look opposite. Both are predictable stress responses rather than rational portfolio management. Recognising that distinction is where the real work begins.

Four biases are doing the most damage in the current environment. Each has a specific mechanism, and each is visible in aggregate Australian investor data right now.

These are not abstract categories. They are the mechanisms behind real capital destruction in Australian portfolios this year.

SMSFs hold 28% of superannuation assets, with total assets under management of approximately $900 billion (APRA, Q1 2026). The behavioural fingerprint in this cohort is clear.

The ATO SMSF quarterly statistics for December 2025 show listed shares representing 27% of SMSF assets and cash and term deposits at 16%, a breakdown that makes the subsequent Q1 2026 rotation toward cash and term deposits even more striking when set against the long-run allocation baseline.

APRA data shows 41% of SMSFs increased cash and term deposit allocations in Q1 2026, up from 35% in 2025. Post-oil-spike selling of energy holdings was reported at approximately 29% of SMSFs. These are aggregate patterns, but they map directly onto the biases described above: loss aversion driving de-risking, recency bias driving reactive selling, and hyperbolic discounting rewarding the short-term comfort of cash at the expense of long-term compounding.

The data does not describe a measured strategic rotation. It describes stress behaviour made visible at scale.

Pre-commitment is the practice of defining investment rules, such as contribution schedules, rebalancing triggers, and gain-locking thresholds, before emotion enters the picture. The concept draws on what behavioural economists call a Ulysses contract: binding yourself to a future course of action while calm so that the decision is already made when stress arrives.

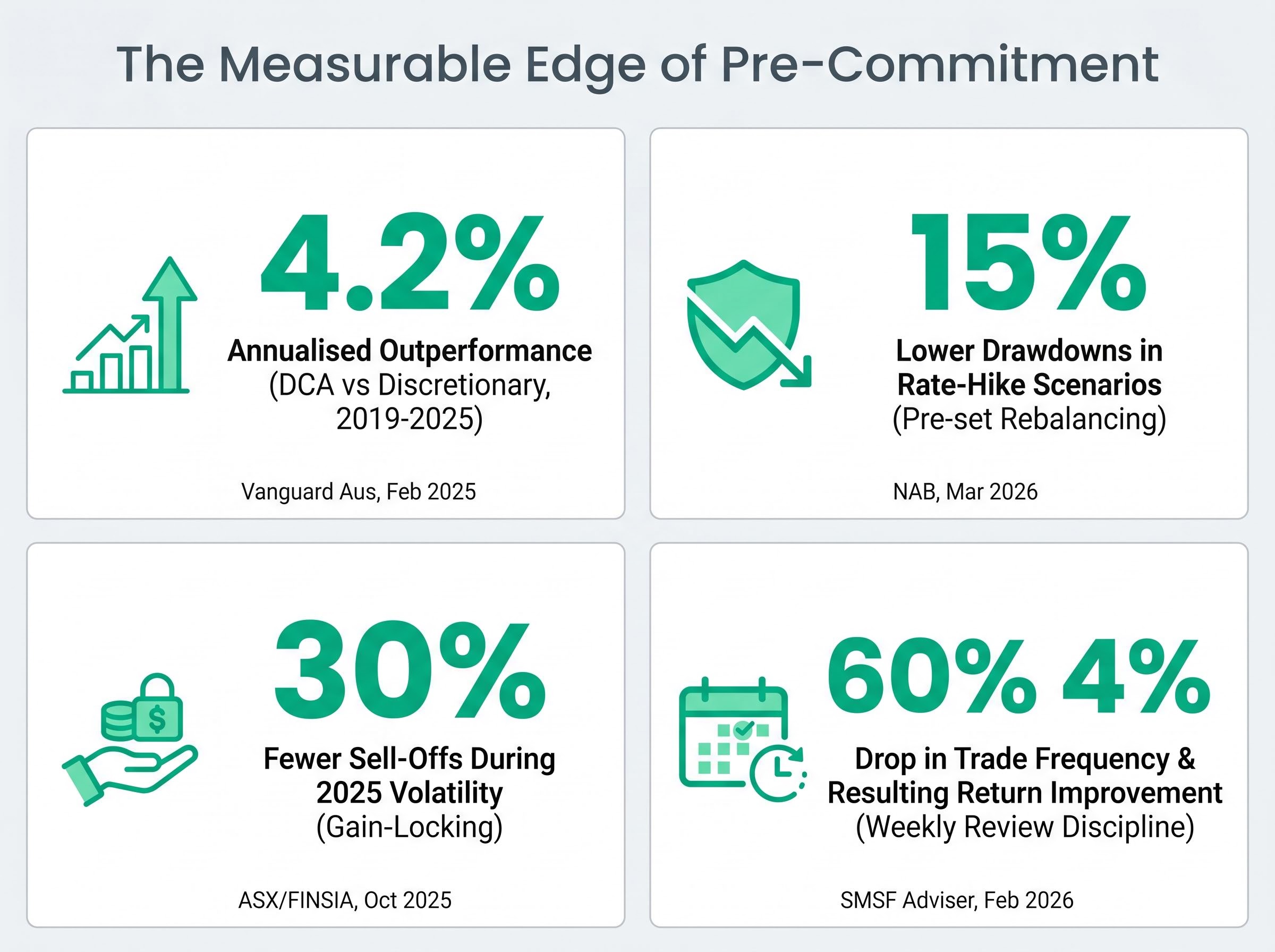

The performance evidence for this approach in the Australian context is substantial:

The dollar-cost averaging evidence is more nuanced than most guides acknowledge: lump-sum investing outperforms DCA in 68-73% of historical periods across major markets, meaning the primary case for DCA is not mathematical optimisation but behavioural protection, removing the investor from the decision at the moment of maximum emotional pressure.

“Pre-commit to ‘invest, add, wait’; it’s behavioural armour.” — Scott Phillips, Motley Fool, quoted in NAB Behavioural Economics Paper, March 2026

The Financial Advice Association Australia (FAAA) recommends complementary structural tools: rules-based rebalancing, cooling-off periods before major portfolio decisions, and pre-committing to a target allocation (such as 60/40 growth-to-defensive) as a behavioural anchor.

The following table summarises documented outcomes across the two approaches.

| Approach | Drawdown Behaviour | Documented Performance Outcome |

|---|---|---|

| Pre-committed (DCA, rules-based rebalancing) | 15% lower drawdowns under rate-hike scenarios | 4.2% annualised outperformance vs. discretionary (Vanguard Australia, Feb 2025) |

| Discretionary (market-timing, reactive selling) | Higher drawdowns during volatility; 30% more sell-offs without pre-commitment mechanisms | Underperformance linked to disposition effect and recency-driven trading (ASX/FINSIA, Oct 2025) |

Pre-commitment is not a vague aspiration. It is a documented strategy with measurable performance outcomes that Australian retail and SMSF investors can implement within existing brokerage platforms.

Scott Phillips, speaking with Gemma Dale (Director of SMSF and Investor Behaviour at nabtrade) on the 11 May 2026 Your Wealth podcast episode, argued that the quality of investment decisions is directly connected to the structure and regularity of how an investor reviews their portfolio. The claim sounds intuitive. The evidence suggests it is also measurable.

A case study published by SMSF Adviser (February 2026) tracked a retail investor who switched to a weekly-review-only discipline following the May 2025 federal election volatility. The result: trade frequency fell by 60%, and the investor self-reported an approximately 4% return improvement. The mechanism is straightforward. Less frequent, more structured review reduces the number of moments where emotion can override a plan.

Gemma Dale frames this habit-review structure as particularly relevant for SMSF trustees, who carry fiduciary responsibility and are especially vulnerable to reactive decision-making when portfolio values fluctuate. For this cohort, reviewing less often but more deliberately is not laziness; it is governance.

These are executable within existing platforms such as nabtrade, CommSec, or SelfWealth:

The scale of the change matters less than the fact of making it structured and documented.

Behavioural discipline is half the equation. The other half is what sits in the portfolio.

High-quality businesses, defined by strong competitive advantages, pricing power, and resilient cash flows, are structurally advantaged during inflationary, high-rate environments. They can pass costs through to customers, sustain dividends under margin pressure, and attract defensive capital rotation when risk appetite contracts.

The following table summarises the sectors and specific ASX-listed names that analysts highlight as fitting this profile in the current environment.

| Sector | ASX Ticker(s) | Key Defensive Characteristic | Analyst View / Source |

|---|---|---|---|

| Consumer Staples | WES, COL | Pricing power through essential goods; volume resilience across retail formats | WES up approx. 8% YTD (Macquarie, April 2026); COL yield approx. 3.58% |

| Healthcare | CSL, RHC | Dominant market positions; non-discretionary demand; outperformance in recessionary conditions | CSL: UBS Outperform rating, consensus target approx. $197-$210 |

| Utilities | APA, AGL | Infrastructure yield; very low correlation to broader market stress (APA 5-year beta approx. 0.25) | APA yield approx. 5.52-6.2% (Goldman Sachs, March 2026) |

| Telecommunications | TLS | Stable ARPU; 5G network position; defensive income profile | Characterised as “SMSF staple” (Bell Potter, Feb 2026) |

Not all analysts share this defensive bias. Citi (April 2026) prefers resource and mining stocks such as BHP for commodity tailwinds from elevated oil and metals prices, a view that contrasts with the staples-and-healthcare consensus from Macquarie and others. The debate is genuine, and investors should weigh both perspectives against their own risk tolerance.

Quality factor ETF selection on the ASX involves three genuinely different products, QUAL (unhedged, $7.98 billion in assets), QHAL (AUD-hedged), and QLTY (equal-weight, lowest fee at 0.35% per annum), with the critical decision variables being currency hedging preference and portfolio concentration rather than simply choosing the largest or cheapest fund.

A Sydney-based SMSF holder profiled by the Australian Financial Review (March 2026) applied a 10% annual profit-take rule on CSL holdings and avoided the 2025 dip by systematically reducing exposure after gains, crediting behavioural frameworks including Phillips’ pre-commitment approach.

A nabtrade case study from the May 2026 Your Wealth podcast found that an investor who pre-committed to monthly ASX 200 ETF additions throughout the oil price volatility period outperformed discretionary approaches by approximately 7% through compounding of additional units purchased at lower prices. The combination of quality holdings and pre-committed buying discipline is where the behavioural and structural arguments converge.

Tax management is not a compliance exercise. In Australia’s superannuation and capital gains framework, how and when an investor sells can alter after-tax returns as meaningfully as what they buy.

The capital gains tax (CGT) discount is the structural incentive to stay invested. Individuals holding assets for more than 12 months receive a 50% CGT discount. SMSFs receive a 33.3% discount. Short-term panic selling does not only lock in paper losses; it triggers full marginal-rate CGT exposure, compounding the financial damage of reactive behaviour.

Three tax-efficiency actions, ordered by priority:

Franking credits represent tax already paid at the corporate level (currently 30% for large companies). When those credits flow through to investors via fully franked dividends, they reduce or eliminate the investor’s tax on that income. For SMSFs in pension phase, excess franking credits are refunded by the ATO, making fully franked Australian equities one of the most tax-efficient income sources available.

Concessional contributions of up to $30,000 per annum (2026 cap) offer a complementary advantage. These contributions are tax-deductible for the individual and taxed at just 15% within the super fund. Systematic, pre-committed concessional contributions are, in effect, a tax-advantaged version of the DCA discipline described earlier.

For SMSF trustees and self-directed investors wanting to model the full scale of the structural benefit, our deep-dive into the superannuation tax wrapper advantage quantifies the projected $230,000 wealth gap between identical portfolios held inside and outside super over 25 years, with worked comparisons across the 32.5% and 37% marginal rate brackets and an explanation of how pension-phase zero tax compounds the advantage further.

The principles in this guide are not separate tips. They form a single architecture: behavioural pre-commitment (rules before emotion), habit structure (a fixed review cadence that reduces reactive interference), quality portfolio positioning (businesses with pricing power and defensive cash flows), and tax-efficient holding (CGT discounts, franking credits, and concessional contributions working together over time).

The current environment is genuinely uncertain. Westpac forecasts continued rate pressure if oil holds above $130/bbl. AMP holds a more dovish view, expecting cuts by Q3 2026. Neither institution is certain, and a sound plan must hold across both scenarios.

The call to action is specific: commit this week to one pre-commitment rule, one habit change, and one portfolio quality check. Document each. The scale of the change matters less than the structure behind it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Pre-commitment in investing means defining rules such as contribution schedules, rebalancing triggers, and profit-taking thresholds before emotion enters the picture, so decisions are already made when market stress arrives. It draws on the concept of a Ulysses contract, binding yourself to a rational plan while calm so that fear or greed cannot override it later.

Foundational investing strategies for Australian SMSF investors include pre-committed dollar-cost averaging, rules-based portfolio rebalancing, holding quality businesses with pricing power, maximising concessional contributions up to the $30,000 annual cap, and prioritising fully franked equities to leverage refundable franking credits in pension phase.

Dollar-cost averaging involves investing a fixed dollar amount at regular intervals regardless of market conditions, which removes the investor from the decision at moments of maximum emotional pressure. Vanguard Australia found pre-committed DCA investors outperformed discretionary traders by 4.2% annualised over 2019-2025.

The four biases doing the most damage are loss aversion, which causes premature selling or paralysis; recency bias, which drives reactive portfolio shifts based on recent events; hyperbolic discounting, which prioritises short-term emotional relief over long-term compounding; and the disposition effect, which leads investors to sell winners too early and hold losers too long.

Franking credits represent corporate tax already paid at the 30% rate, which flows through to investors via fully franked dividends and reduces or eliminates tax on that income. For SMSFs in pension phase, any excess franking credits are refunded by the ATO, making fully franked Australian equities one of the most tax-efficient income sources available.