What 4 Wall Street Firms See Driving Markets in H2 2026

51 mins ago

Six weeks. $3.8 trillion. The PHLX Semiconductor Index (SOX) has posted its strongest sustained rally since the dot-com era’s peak, and for the first time in 26 years, Intel has an all-time high to show for it. As of 10 May 2026, a broad, multi-company surge in semiconductor stocks has rewritten market capitalisations across the sector, pulled memory chip names to historic valuations, and forced investors to confront a question the industry has not posed this seriously in a generation: is this the start of a durable supercycle, or a repeat of the pattern that ended badly in 2000?

What follows breaks down exactly which companies are leading the rally and by how much, explains the agentic AI demand shift that is structurally different from prior chip booms, and lays out the specific risks that could reverse the gains, giving investors the context they need to evaluate their exposure right now.

The rally’s most important feature is its breadth. Over six weeks, the SOX index climbed to approximately 10,534-11,775, a gain of roughly 45% year to date, adding an estimated $3.8 trillion in aggregate sector market value.

According to the Wall Street Journal, this represents the strongest six-week gain for the SOX index since the dot-com era.

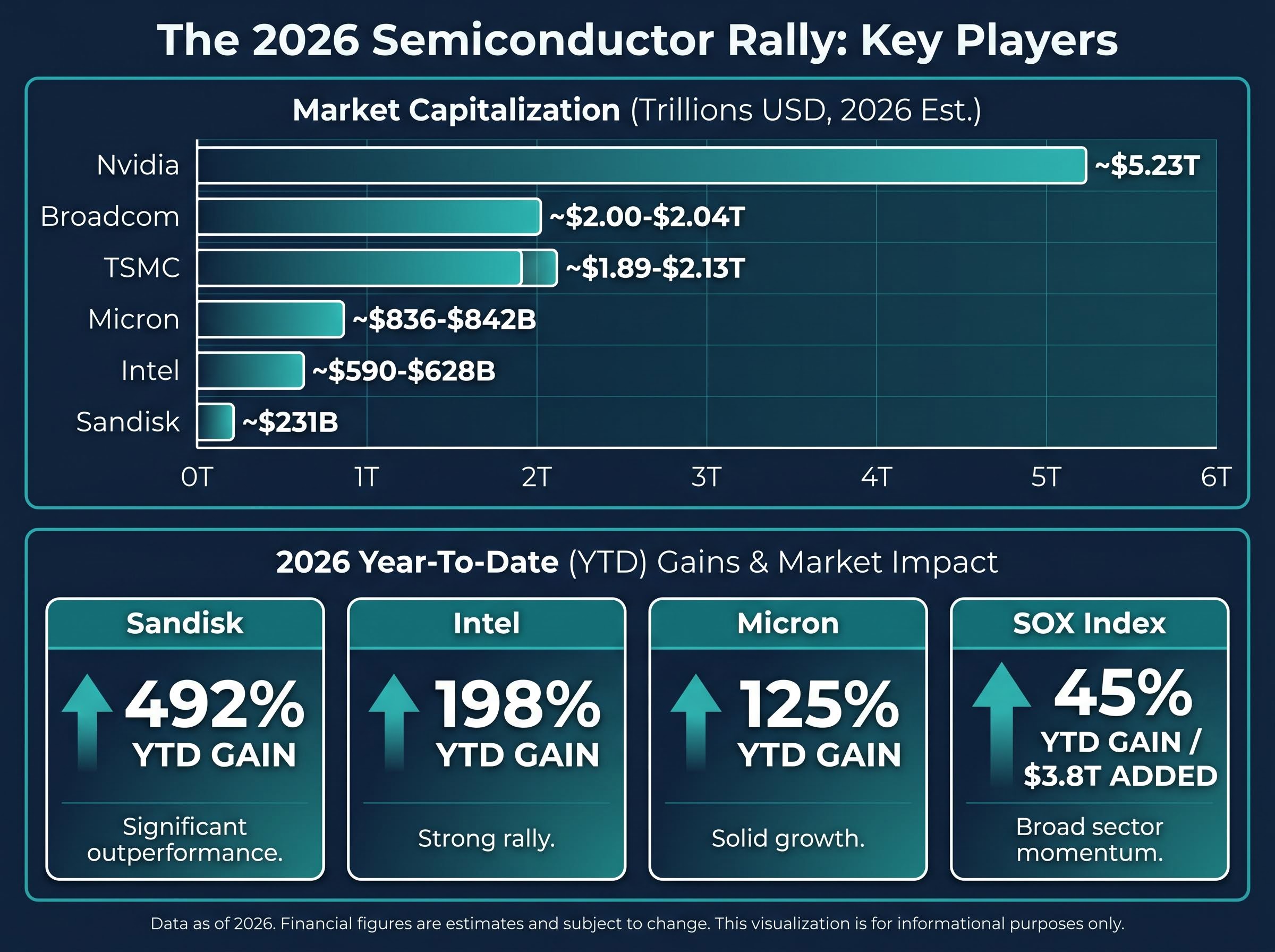

Nvidia remains the sector’s largest name at approximately $5.23 trillion in market capitalisation, but the gains that tell the real story sit further down the roster. Intel (INTC) reached an all-time high in April 2026 at approximately $99-$126 per share, a 198% year-to-date gain that eclipsed a record last set during the 2000 tech bubble. Sandisk (SNDK), independent since its 2025 spin-off from Western Digital, has surged approximately 492% year to date to roughly $1,562 per share, driven by AI memory demand rather than legacy storage revenues.

Broadcom (AVGO) and TSMC (TSM) have both crossed $2 trillion in market capitalisation, joining Nvidia in a mega-cap tier that did not exist twelve months ago.

| Company (Ticker) | Price (May 2026) | Market Cap | YTD Gain |

|---|---|---|---|

| Nvidia (NVDA) | ~$215 | ~$5.23T | — |

| Intel (INTC) | ~$99-$126 | ~$590-$628B | ~198% |

| Sandisk (SNDK) | ~$1,562 | ~$231B | ~492% |

| Western Digital (WDC) | ~$480 | ~$165B | ~950% (1yr) |

| Micron (MU) | ~$667-$746 | ~$836-$842B | ~125% |

| Broadcom (AVGO) | ~$423-$430 | ~$2.00-$2.04T | — |

| TSMC (TSM) | ~$411-$419 | ~$1.89-$2.13T | — |

The composition of the move, spanning CPUs, memory, foundry, and equipment names, signals a sector-wide repricing rather than a speculative spike concentrated in a single theme.

Prior waves of AI enthusiasm created demand spikes: a product launch, a model release, a burst of inference traffic. Agentic AI operates on a different principle entirely.

Agentic AI refers to autonomous systems that run continuously, around the clock, without human prompting. Rather than responding to individual queries, these agents execute multi-step tasks independently, generating sustained compute and memory demand that does not cycle off. The distinction matters for chip demand because always-on operation converts what was once episodic inference load into permanent, compounding baseline consumption.

The key demand characteristics are distinct from prior AI cycles:

Agentic AI workload demand is doing more than converting inference from episodic to continuous: AMD’s Q1 2026 procurement data shows the shift is repricing the server CPU total addressable market from an 18% annual growth assumption to 35%, implying a market above $120 billion by 2030 and extending the hardware investment thesis well beyond GPU suppliers.

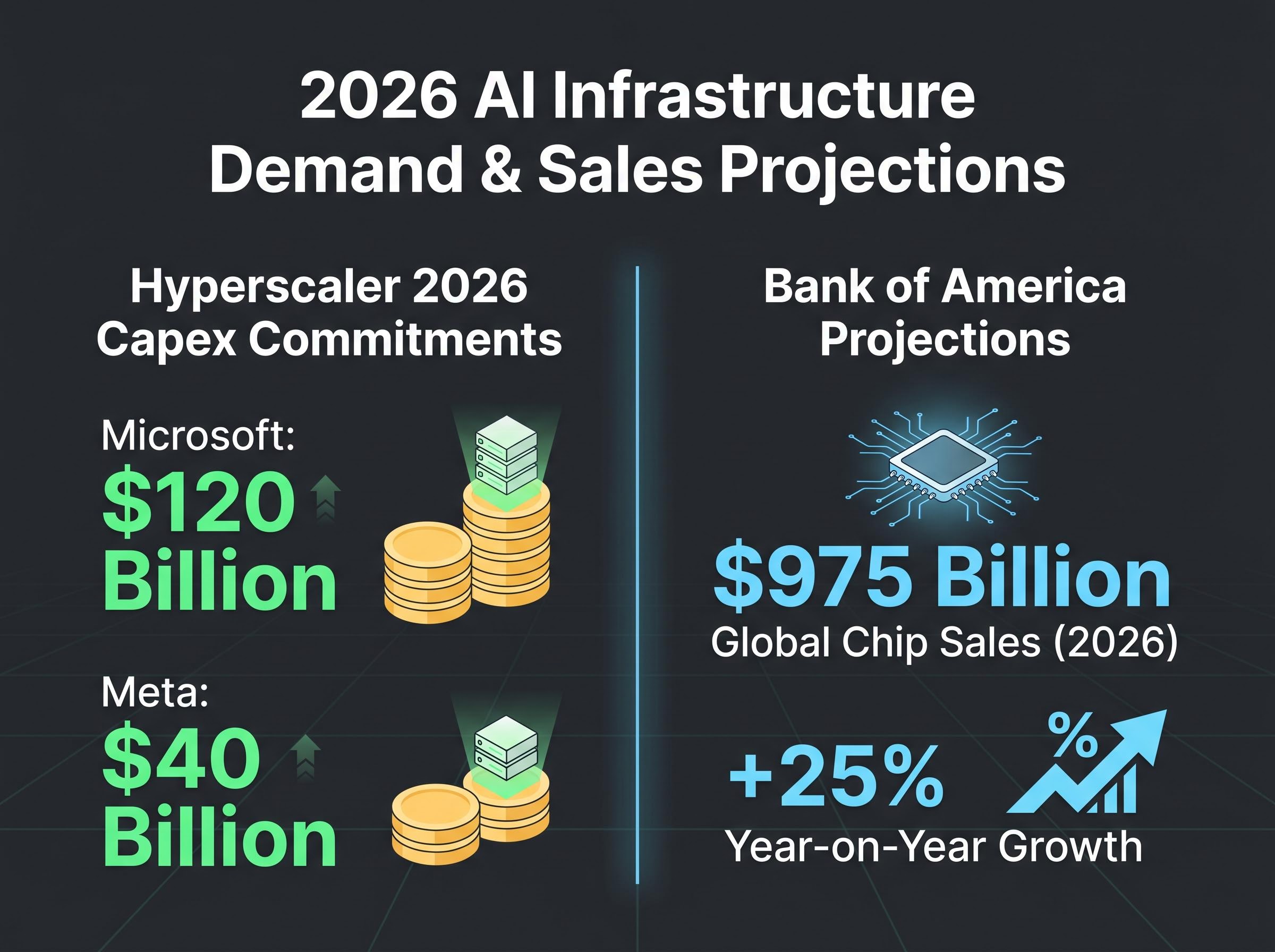

The spending commitments backing this demand signal are concrete. Microsoft announced $120 billion in AI infrastructure capital expenditure for 2026 during its Q1 FY2026 earnings. Meta has committed approximately $40 billion in AI infrastructure capex for the same period. Specific 2026 figures for Google (Alphabet) and Amazon were not independently confirmed at the time of publication, though both companies’ infrastructure programmes are understood to be ongoing.

Bank of America projects approximately $975 billion in global chip sales in 2026, roughly 25% higher year on year, with AI semiconductor revenue growing approximately 50% annually. The bank characterised the current environment as the “midpoint of a decade-long transformation” in AI hardware.

Hyperscaler capex commitments of this scale represent multi-year procurement contracts, not quarter-to-quarter discretionary spend. That distinction is the single most important context for evaluating whether the rally has fundamental support.

The price charts look alarming. The income statements tell a different story.

In 2000, the semiconductor rally was built on speculation about future earnings that never materialised. In 2026, the re-rating is occurring in companies already producing record profits. Micron (MU) reported Q2 FY2026 net income of $13.79 billion, a record, completing an arc from losses in 2023 to the largest quarterly profit in the company’s history. The stock has gained approximately 125% year to date.

The valuation anomaly is striking.

Micron trades at approximately 8.9 times forward earnings, a multiple below the S&P 500 average, despite a 125% year-to-date rally. Denise Chisholm of Fidelity Investments has noted that earnings growth of this magnitude is an anomaly versus historical norms.

Samsung Electronics reported Q1 2026 operating profit of 57.2 trillion KRW (approximately $38-$42 billion), a year-on-year increase of roughly 750%, driven by AI memory chip demand.

Samsung’s operating profit surged approximately 750% year on year in Q1 2026, anchoring the earnings case for the broader memory sector.

Lam Research posted record Q2 FY2026 revenue of $5.345 billion and guided Q3 to $5.7 billion, reflecting continued investment in memory fabrication equipment. Jonathan Cofsky of Janus Henderson has observed that technology firms’ chip procurement is generating exceptional profits for producers.

When the most beaten-up memory name in the sector trades at a discount to the S&P 500 on forward earnings even after a 125% rally, the valuation conversation becomes more nuanced than a simple “it has run too far” dismissal.

The GPU names get the headlines. The memory names tell the supply story.

High-bandwidth memory (HBM), the specialised memory used in AI accelerators, sits in a structurally constrained supply position. Demand from agentic AI workloads has consistently outpaced production capacity, and the shortage conditions, flagged by Lam Research as exceeding prior forecasts, are expected to persist. The demand chain follows a specific sequence:

This supply tightness explains why Sandisk’s approximately 492% year-to-date gain and Micron’s record $13.79 billion Q2 net income are not interchangeable with GPU-driven gains. They reflect a commodity-level scarcity dynamic where pricing power persists as long as demand outpaces production.

The data storage supply constraints driving Sandisk’s 492% year-to-date gain and Western Digital’s near-950% one-year move extend well beyond HBM: major hardware suppliers have sold out production capacity through 2026, enterprise hardware prices for high-capacity models surged up to 60%, and cloud providers are passing upstream cost increases directly to enterprise customers.

Lam Research’s Q3 guidance of $5.7 billion confirms that memory fab investment is accelerating, but the lead times on new capacity mean investors in memory names may be pricing in a sustained window of scarcity pricing rather than a temporary imbalance.

Three specific risk categories could reverse the gains, each with quantifiable dimensions.

The BIS export control rules for advanced semiconductors, revised effective January 2026, shifted the license review policy for chips including the Nvidia H200 and AMD MI325X to a case-by-case evaluation framework for exports to China and Macau, a regulatory posture that leaves meaningful scope for further tightening if policy priorities shift.

Steve Sosnick, chief strategist at Interactive Brokers, has noted that the velocity of gains is unlike anything observed in prior market cycles.

No major Wall Street institution has issued a formal bubble warning as of early May 2026. Bank of America characterises the path forward as “choppy” even under its base case, and the concentration of demand in a handful of hyperscaler buyers means the rally is unusually sensitive to a small number of capital allocation decisions.

The fundamental support is real: record earnings at Micron and Samsung, hyperscaler capex commitments exceeding $160 billion from Microsoft and Meta alone, and a supply-constrained memory market that shows no signs of near-term relief. Against that, the SOX index is up 45% year to date, individual names have gained hundreds of percent, and Steve Sosnick’s characterisation of the move’s velocity as unprecedented is difficult to dismiss.

Bank of America’s $975 billion global chip sales forecast frames the rally as structural. Peter Feinberg, a retired lawyer and long-term investor, has expressed discomfort with a gain trajectory unlike anything in prior cycles, a sentiment that represents the caution camp alongside the institutional bull case.

The one data point that distinguishes 2026 from 2000: valuations are stretched in price terms but defensible in earnings terms.

The dot-com era investment peak the article uses as its comparison point has now been materially surpassed: US IT hardware and software spending reached 4.9% of GDP in Q1 2026, above the dot-com peak of approximately 4.2% and the cloud buildout peak of approximately 3.8%, placing the current cycle in genuinely unprecedented macro territory rather than simply at the upper end of a prior range.

Micron at approximately 8.9 times forward earnings, cheaper than the S&P 500 average after a 125% rally, is the kind of anomaly that dot-com era semiconductor stocks never possessed.

The catalysts most likely to determine whether the rally extends or stalls are identifiable and have specific timelines:

Samsung’s continued HBM ramp, measured against its Q1 operating profit of 57.2 trillion KRW, provides the clearest benchmark for whether the earnings foundation holds. Goldman Sachs’ price target of 260,000 KRW for Samsung remains a key level for gauging institutional conviction.

Bank of America’s $975 billion global chip sales forecast serves as the year-end benchmark for tracking whether the sector is meeting, exceeding, or falling short of the structural growth narrative.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The PHLX Semiconductor Index (SOX) tracks the performance of major semiconductor companies and is widely used as a benchmark for the sector. As of May 2026, it has risen approximately 45% year to date, posting its strongest six-week gain since the dot-com era.

Agentic AI refers to autonomous systems that operate continuously without human prompting, executing multi-step tasks independently around the clock. Unlike prior AI waves that created episodic demand spikes, agentic AI converts inference load into permanent, compounding baseline consumption, generating sustained demand for GPUs and high-bandwidth memory.

Micron trades at approximately 8.9 times forward earnings, below the S&P 500 average, because its earnings growth has been extraordinary: the company reported record Q2 FY2026 net income of $13.79 billion, completing a turnaround from losses in 2023. The valuation reflects strong earnings rather than speculative multiple expansion.

The three main risks are a slowdown in hyperscaler capital expenditure (which could trigger an estimated 20% correction), US-China export controls that Bank of America estimates could reduce sector growth by 5-10%, and broader consumer sentiment weakness, with the University of Michigan index hitting a record low of 48.2 in May 2026.

Sandisk (SNDK) has surged approximately 492% year to date to around $1,562 per share, driven by AI memory demand, while Intel (INTC) gained approximately 198% year to date and reached an all-time high not seen since 2000. Micron (MU) has gained approximately 125% year to date alongside record quarterly profits.