How Zero Commissions Changed the Maths on Thematic ETFs

2 hrs ago

Superannuation is one of the most tax-advantaged vehicles available to Australian investors, yet a confirmed ATO rule change taking effect 1 July 2026 is likely to pass most fund members by without a single decision made. Concessional caps rise to $32,500 and non-concessional caps to $130,000 from that date, opening a wider window for tax-sheltered wealth accumulation. The cap increase itself, however, is not where the largest opportunity sits. For the majority of members, the real value lies in accumulated unused cap space from prior years, an investment option inside their fund that has never been reviewed, and the compounding cost of neglecting both. This guide explains the mechanics of contribution caps, carry-forward rules, and bring-forward arrangements in plain terms, then applies them at each life stage and quantifies what sitting in a default fund is likely costing over a 25-year horizon.

The strategic value of every contribution and fund choice decision in the sections that follow rests on one thing: the gap between what investment returns are taxed inside superannuation and what they are taxed outside it. That gap is larger than most members realise, and it compounds every year.

Three rates define superannuation’s advantage in the accumulation phase and beyond:

Now consider the alternative. An Australian earning between $90,000 and $120,000 faces a marginal tax rate of 34.5% to 39% (including the 2% Medicare levy) on investment income held in their own name. The gap between that rate and super’s 15% is not a rounding error. It is the entire strategic case for maximising what goes into the fund.

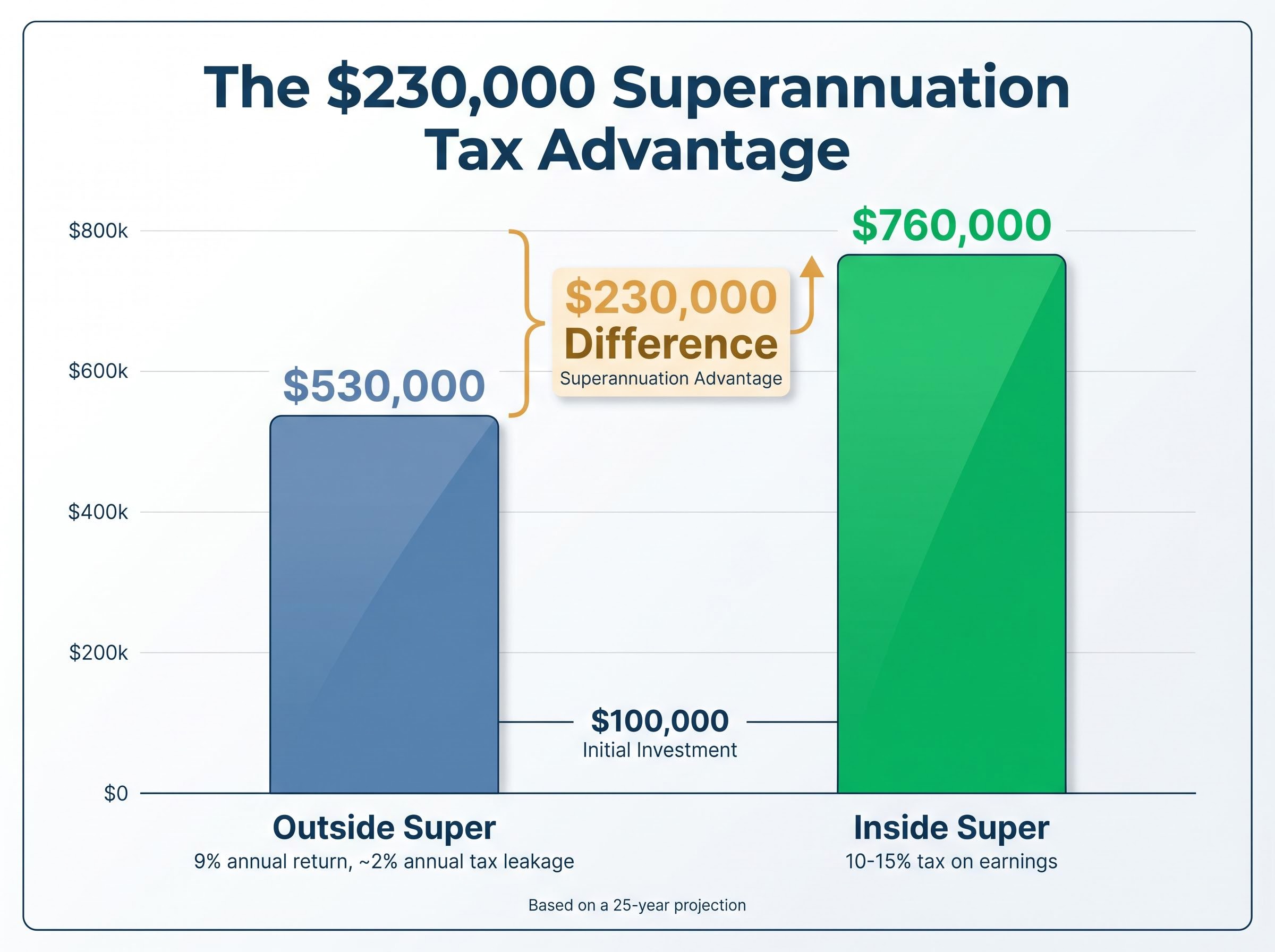

The compounding cost of that gap: $100,000 invested outside super at a 9% annual return, with approximately 2% annual tax leakage, grows to roughly $530,000 over 25 years. The same amount inside super, taxed at 10-15% on earnings, grows to approximately $760,000. That is a $230,000 difference from the tax wrapper alone.

The concession comes with a constraint. Preservation age is 60 for all Australians born after 1 July 1964, which means funds contributed today by someone aged 35 are inaccessible for approximately 25 years. This is the cost of the tax advantage, not a hidden penalty. Every strategy in this guide should be weighed against the reader’s need for liquidity outside superannuation before committing capital to the system.

Salary sacrifice and ETF blending, directing a portion of monthly savings into concessional contributions and the remainder into a low-cost ASX ETF portfolio, addresses the lock-up constraint directly by maintaining liquidity outside super while still capturing the 15% contributions tax rate on the sacrificed portion.

The ATO confirmed the following figures, indexed in line with Average Weekly Ordinary Time Earnings (AWOTE), as at 24 April 2026:

| Item | FY2025-26 | From 1 July 2026 |

|---|---|---|

| Concessional contributions cap | $30,000 | $32,500 |

| Non-concessional contributions cap | $120,000 | $130,000 |

| Bring-forward three-year NCC maximum | $360,000 | $390,000 |

The increase is a useful increment, but it is not the headline story. A $2,500 lift in the concessional cap adds approximately $800 in annual tax savings for someone on a 32% effective rate differential. The larger opportunity, for most members, is the unused cap space already sitting in their ATO account from prior years.

Tax saving illustration: An employee earning $120,000 who salary-sacrifices $15,000 into super saves approximately $4,800 in income tax annually, reflecting the difference between the marginal rate paid on that income outside super and the 15% contributions tax paid inside it.

That annual saving is meaningful. But for members who have not been maximising contributions in recent years, the carry-forward rule described in the next section could deliver multiples of that figure in a single financial year.

The carry-forward mechanism does not arrive as a lump-sum entitlement. It builds, year by year, from each financial year in which a member contributes less than the concessional cap. Those unused amounts accumulate on a rolling five-year basis (from FY2018-19 onward) and can be deployed in a single later year, turning several quiet years into one significant tax reduction.

One urgency element the five-year rolling window does not surface immediately is that carry-forward contribution deadlines are asymmetric: unused amounts from FY2020-21 expire permanently on 30 June 2026, meaning members who delay past that date lose those specific entitlements regardless of their TSB position.

Eligibility hinges on one threshold: Total Super Balance (TSB) must be below $500,000 at the prior 30 June. This figure is confirmed unchanged by the ATO as at April 2026. Members who crossed $500,000 lose access to the rule regardless of how much unused cap space they hold. Members who have been maximising the concessional cap each year have no unused amounts to carry forward; the rule is designed for those who consistently contributed less than the cap.

The profiles most likely to benefit are specific: career-break returners, parents who moved to part-time work for several years, sole traders with variable income, or employees who recently stepped into a higher income bracket after years of modest earnings.

Consider a 45-year-old with a TSB of $420,000 at 30 June 2025 who earned less than the concessional cap during several prior years. Subject to their actual unused amounts, this member could potentially contribute $70,000-$100,000 or more in concessional contributions in a single financial year. The tax saving on each dollar contributed above the standard cap reflects the differential between the member’s marginal rate and the 15% contributions tax, which can reach 32% for someone on a $120,000 salary.

The execution steps are straightforward:

For Australians who experienced income gaps or variable earnings in the past five years, this rule may represent the single largest legal tax reduction available to them this financial year.

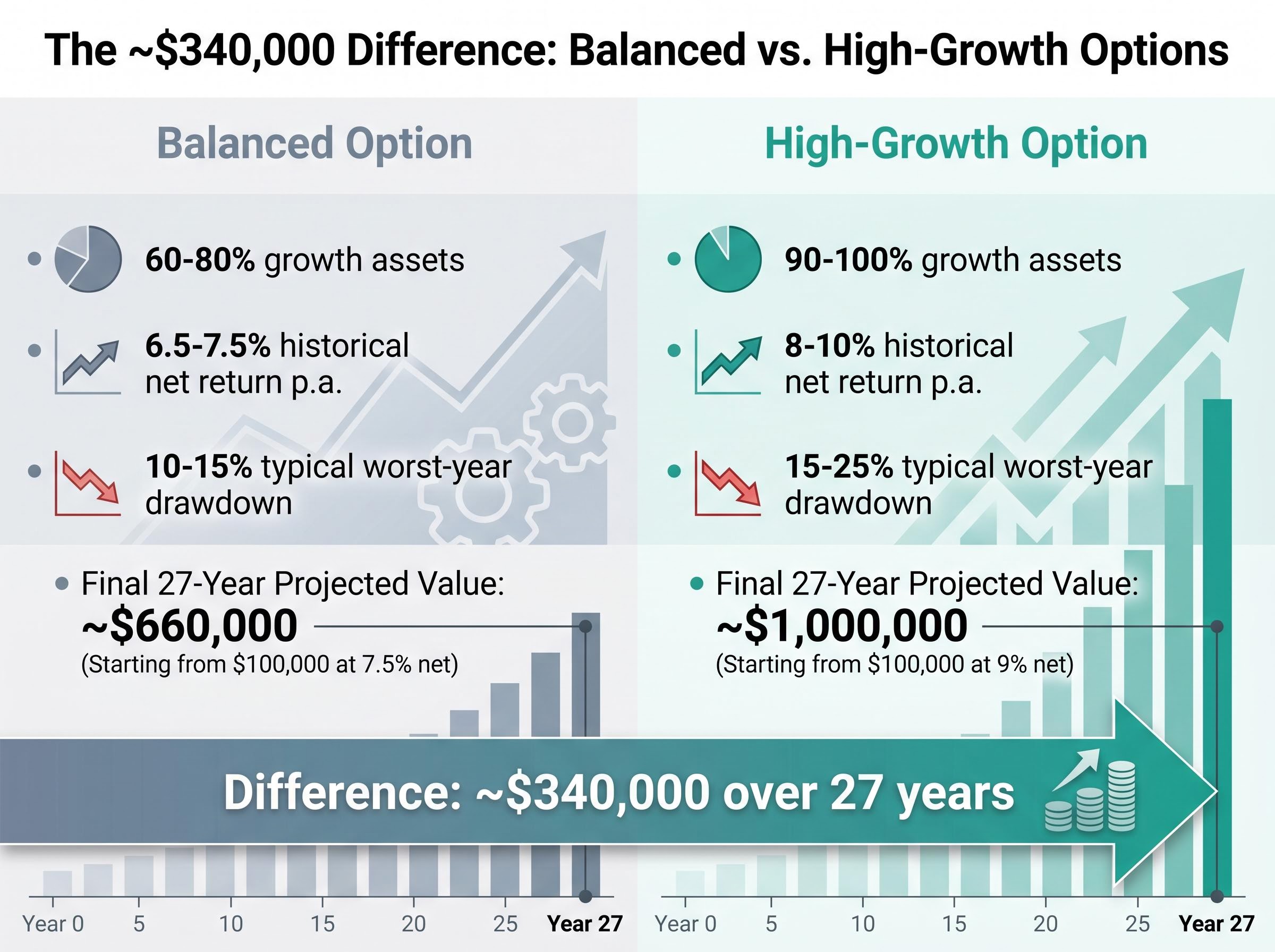

Over 27 years, $100,000 growing at 7.5% per annum net becomes approximately $660,000. The same $100,000 growing at 9% per annum net becomes approximately $1,000,000.

That is a difference of approximately $340,000, from a single administrative choice made (or not made) inside an existing super fund.

The cause is not a fee scandal or a market crash. It is the gap between a default MySuper “balanced” option and a high-growth option within the same fund.

A balanced option typically holds 60-80% growth assets (equities and property) with the remainder in bonds and cash. A high-growth option holds 90-100% growth assets. The structural difference in expected returns between the two, approximately 1.5-3% per annum over 20-30 year horizons according to general industry data, is persistent because it reflects asset allocation, not manager skill.

A significant majority of Australian super fund members remain in default MySuper investment options, a pattern well-documented by APRA and industry observers over many years. For members under 45 with a long accumulation horizon, the investment option decision inside their existing fund is likely the highest-leverage financial choice available, larger in expected dollar terms than optimising contributions alone.

The return differential between a balanced and a high-growth option is partly a function of asset allocation, but hidden superannuation fees embedded in fund architecture, including CGT drag from pooled structures and swap-based index costs that never appear as a line item in fee disclosures, can compress the net return advantage in ways the published option returns do not reveal.

Log into the fund’s member portal. The current investment option is typically visible on the dashboard under “investments” or “portfolio.” Switching is usually processed within one to two business days and does not trigger a capital gains tax event inside the fund. The only tax implication is that future earnings continue to be taxed at the applicable 15% rate. The barrier is awareness, not complexity.

Readers should verify current fund-specific returns via APRA Quarterly Superannuation Statistics or their fund’s own investment performance pages before making any changes.

The APRA MySuper Product Heatmap provides a standardised, fund-by-fund comparison of net investment returns, fees, and member outcome sustainability across all MySuper products, giving members the data needed to assess whether their default option is competitive before switching.

Superannuation tools do not change with age, but their priority order does. A 34-year-old and a 52-year-old reading the same ATO guidance face different constraints, different compounding horizons, and different liquidity needs. What follows is an opinionated recommendation for each stage, not a menu of options.

The gap between the tax rates inside and outside super compounds most painfully for members who do not realise how far behind the typical accumulation curve they are sitting; retirement savings benchmarks by age, drawn from APRA data, show that the average Australian in their early fifties holds roughly $198,400, more than $430,000 below the ASFA comfortable retirement threshold for a single person.

| Life Stage | Primary Focus | Key Tool | Liquidity Consideration |

|---|---|---|---|

| Under 40 | Growth option; begin salary sacrifice modestly | Investment option switch to high-growth | Preserve liquidity for emergency fund, property deposit, or business capital |

| 40-50 | Maximise concessional contributions; deploy carry-forward | Carry-forward concessional contributions (if TSB under $500,000) | Moderate; lock-up less constraining with 15-25 years to preservation age |

| 50 and over | Full concessional cap; bring-forward NCC if a liquidity event occurs | Bring-forward NCC (up to $390,000 over three years from 1 July 2026) | Low; preservation age of 60 is near enough to make lock-up a minor concern |

Under 40: Superannuation is the right vehicle for long-term wealth, but not at the expense of short-term financial security. Salary-sacrificing even $5,000-$10,000 per year above the employer Superannuation Guarantee Contribution (SGC), currently 11.5% in FY2025-26, captures the tax differential without over-committing liquidity. The highest-impact action at this stage is switching to a high-growth investment option. With 25-30 years of compounding ahead, the return gap compounds into six figures.

40-50: This is the window where the carry-forward rule is most potent. TSB below $500,000 is common at this stage, and 15-25 years of compounding at 9% versus 7.5% represents the largest dollar impact window in a member’s accumulation life. Members who experienced career breaks, parental leave, or part-time work in the past five years should check their unused concessional cap via myGov as a first step.

50 and over: The full $32,500 concessional cap from 1 July 2026 should be the baseline target. If a business sale, inheritance, or property event generates a lump sum, the bring-forward rule allows up to $390,000 in non-concessional contributions over three years. With preservation age close, the lock-up trade-off is minimal.

Three things to do before 30 June 2026:

The cap increases from 1 July 2026 are confirmed and worth planning around. But for most readers, the three highest-leverage decisions are already available:

Personal circumstances vary, and the ATO’s myGov portal, a fund’s member services team, or a licensed financial adviser are the appropriate next steps for individual calculations. The system rewards those who engage with it. The cost of inertia, whether measured in default fund underperformance or unused cap space that quietly expires, compounds every year, not just at retirement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Illustrative projections are based on reasonable historical assumptions and are subject to market conditions and various risk factors.

The carry-forward rule allows Australians with a Total Super Balance below $500,000 to use unused concessional contribution cap space from the previous five financial years in a single year, potentially enabling a much larger before-tax contribution and a significant one-off tax reduction.

From 1 July 2026, the concessional contributions cap rises to $32,500 and the non-concessional contributions cap rises to $130,000, with the three-year bring-forward maximum increasing to $390,000, as confirmed by the ATO in April 2026.

Log into ATO myGov and navigate to your superannuation section, where you can view your unused concessional cap carry-forward statement showing the exact amounts available from each financial year within the five-year rolling window.

A balanced option typically holds 60-80% growth assets and has historically returned around 6.5-7.5% per annum net, while a high-growth option holds 90-100% growth assets and has historically returned around 8-10% per annum net, a difference that can compound to approximately $340,000 over 27 years on a $100,000 starting balance.

Members who have not already triggered a bring-forward arrangement can contribute up to $390,000 in non-concessional contributions over three years from 1 July 2026, making this tool particularly valuable for those aged 50 and over who receive a lump sum from a business sale, inheritance, or property event.