10 Approved Rivals, Yet S&P Global’s Moat Keeps Compounding

58 mins ago

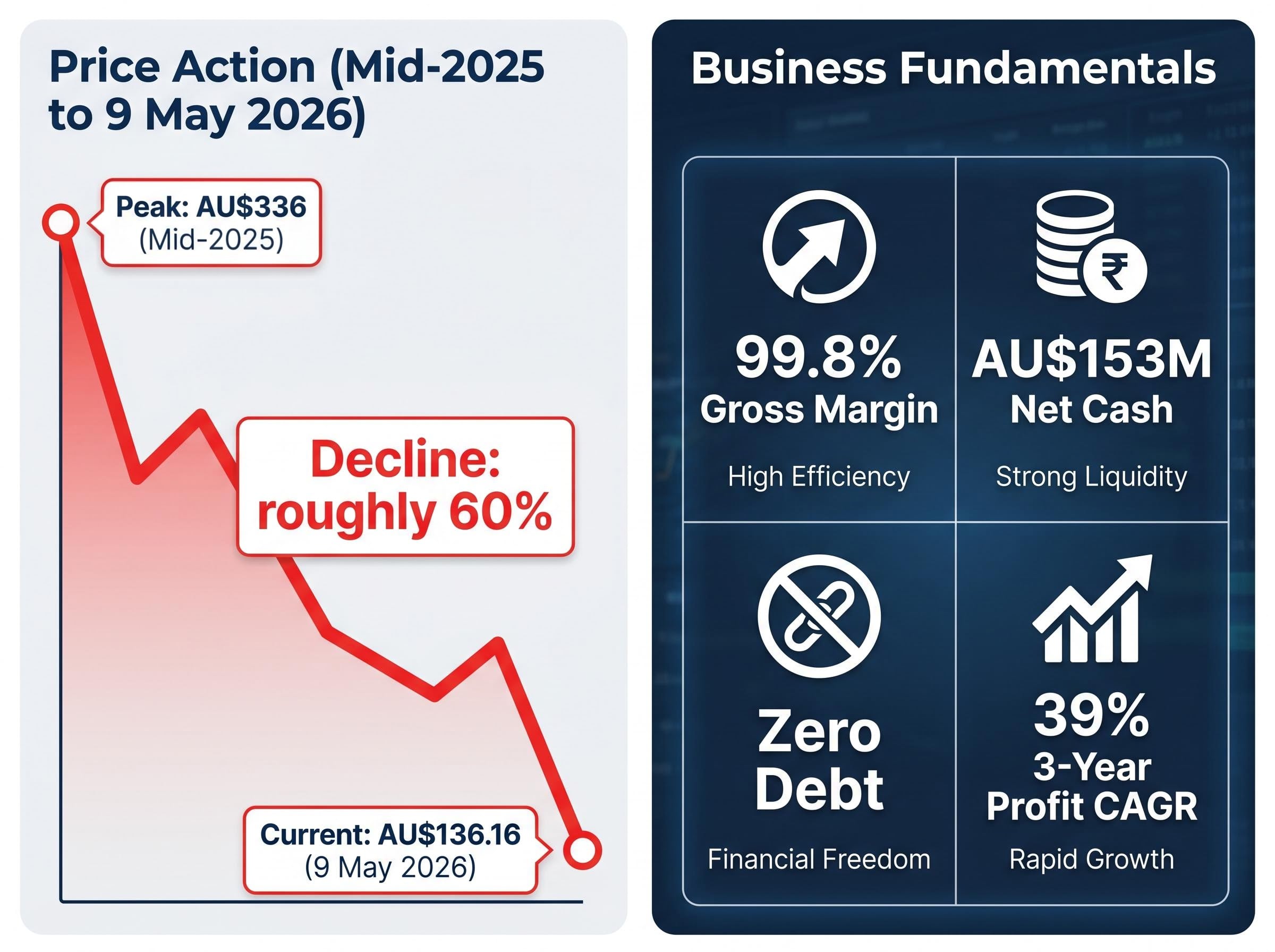

Pro Medicus posted a 99.8% gross margin and a 39% three-year profit compound annual growth rate (CAGR) in its most recent reporting cycle. Its share price has fallen roughly 42% since 1 January 2026.

For Australian retail investors tracking high-quality ASX growth names, that disconnect is both unsettling and analytically instructive. Pro Medicus is not a struggling business navigating a revenue crisis. It is a premium-rated stock experiencing what appears to be a valuation-driven de-rating, and understanding the difference matters enormously for investment decisions.

This analysis breaks down what is actually driving the PME share price decline, examines the business fundamentals in detail, contextualises the current valuation, and explains the distinction between company quality and whether the price is reasonable given that quality. The goal is not to tell investors what to do. It is to provide the framework for making that decision clearly.

The share price of Pro Medicus peaked at approximately AU$336 in mid-2025. As of 9 May 2026, it traded at AU$136.16.

That represents a peak-to-trough decline of roughly 60%. The scale of that fall has generated several headline figures, each reflecting a different measurement window:

These are not contradictory. They measure different things. The important point is that all three describe the same stock in the same period, and the trajectory has been consistently downward.

What has not followed the price down is the earnings outlook. Analyst forecasts for Pro Medicus revenue and profit have remained broadly stable throughout the decline, which tells investors something specific about what is driving it.

Valuation contraction, or de-rating, occurs when the market revises down the multiple it is willing to pay for each dollar of a company’s earnings, independent of whether those earnings have actually changed. The business keeps delivering the same results; the market simply decides those results are worth less per share than before.

In Pro Medicus’s case, two factors have been cited by brokers as drivers. The first is AI disruption fears in radiology IT, where emerging tools for automated image analysis have raised questions about the long-term relevance of traditional imaging platforms. The second is a broader compression of growth stock multiples in a higher-for-longer interest rate environment, which has weighed on premium-rated ASX technology names across the board.

The ASX healthcare sector decline has been broad and severe, with the S&P/ASX 200 Health Care Index falling 39% over 12 months to a six-year low, meaning that PME’s multiple compression has unfolded against a backdrop of generalised sector-level selling pressure that extends well beyond radiology IT or AI disruption concerns specific to any single company.

Consensus target of AU$210 implies approximately 54% upside from the 9 May price of AU$136.16, with Morgans alone carrying a AU$275 target.

The trailing price-to-earnings (P/E) ratio sits at 60.77x. The forward P/E is 72.46x. Both are high by conventional standards, but both are materially lower than the multiples implied at AU$336.

Pro Medicus is an ASX-listed radiology IT software company founded in 1983, supplying hospitals, imaging centres, and healthcare networks globally. Its primary product is the cloud-native Visage 7 imaging platform, which allows clinicians to view, manipulate, and share medical images at speed across distributed hospital networks.

The revenue model is transaction-based software-as-a-service (SaaS), where hospitals pay per study processed rather than licensing software upfront. That structure differs from legacy on-premise competitors in a way that matters: it ties revenue directly to imaging volume, creates recurring income, and eliminates the capital-intensive hardware cycle that constrains older vendors.

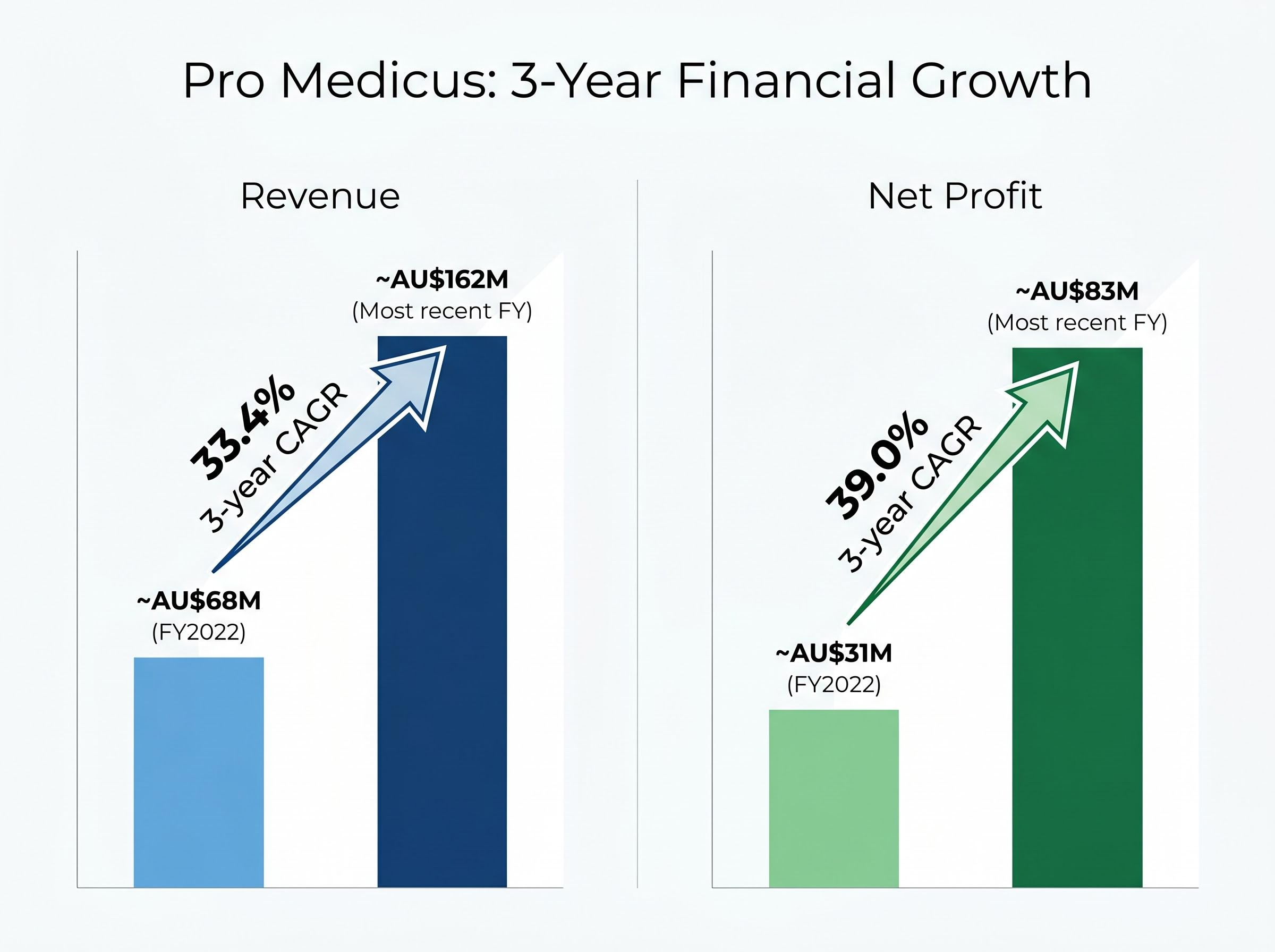

The three-year financial record tells a story of compounding growth at scale.

| Metric | FY2022 (approx.) | Most recent FY | Growth / Level |

|---|---|---|---|

| Revenue | ~AU$68M | ~AU$162M | 33.4% three-year CAGR |

| Net profit | ~AU$31M | ~AU$83M | 39.0% three-year CAGR |

| Gross margin | ~99% | 99.8% | Near ceiling |

| Return on equity | — | 50.7% (FY2024) | Top-decile ASX |

The half-year results for the period ending December 2025 reinforced the trajectory:

These are not typical metrics for an ASX technology company at any capitalisation level. They explain why Pro Medicus commanded a significant premium, and they are necessary context before evaluating whether the current price represents fair value, an overshoot, or ongoing overvaluation.

Gross margin measures the percentage of revenue remaining after subtracting the direct costs of delivering the product or service, before operating expenses such as salaries, marketing, and research. A 99.8% gross margin means that for every dollar of revenue Pro Medicus collects, less than one cent goes to the cost of delivering that service.

This is a structural characteristic, not a cost-efficiency achievement. When the product is software delivered via cloud infrastructure, the marginal cost of processing an additional imaging study is negligible. There is no hardware to ship, no technician to dispatch, no physical installation to perform. Revenue scales; costs do not.

That matters for competitive positioning. Legacy picture archiving and communication system (PACS) vendors using on-premise architectures face fundamentally different cost structures. Even if a competitor matched the Visage 7 product feature-for-feature, replicating the economics would require rebuilding the delivery model from the ground up.

Pro Medicus CEO Dr Sam Hupert characterised AI as “complementary” to the business rather than disruptive during the February 2026 earnings call.

The balance sheet reinforces the picture:

In the competitive landscape, Sectra ranked highest in the 2026 Best in KLAS large PACS report, with Agfa and INFINITT also named. Pro Medicus’s cloud-native architecture and transaction-based model remain its primary differentiator. A debt-free, cash-rich company with near-100% gross margins has far more options than a leveraged competitor facing the same market conditions.

A company can be genuinely exceptional and simultaneously priced so high that future returns will be poor. It can also be exceptional and recently de-rated to a price that offers genuine upside. These are distinct questions, and conflating them is the source of two common errors in growth stock investing.

The framework requires two steps:

With a forward P/E of 72.46x and a forward revenue growth forecast of 17.7% per annum, investors must decide whether that multiple is justified by the growth runway, or whether the de-rating from AU$336 still leaves the stock expensive at AU$136.

Broker consensus provides a data point, not a verdict. According to FT.com data from March 2026, coverage consisted of 4 Buy, 7 Outperform, 2 Hold, and 0 Sell ratings across 13-14 analysts.

| Broker / Source | Price target | Rating |

|---|---|---|

| Morgans | AU$275 | Buy |

| Bell Potter | AU$240 | — |

| Simply Wall St consensus | AU$210 | Undervalued (post-de-rating) |

Over AU$280M in minimum contract value was signed in H1 FY2026. The three-year return on equity (ROE) forecast sits at 39.1%. Zero analysts carry a Sell rating. These are data points that inform the quality-value distinction; they do not resolve it.

The concern is legitimate. AI tools for image analysis, automated reporting, and diagnostic assistance are developing rapidly. In theory, they could reduce dependency on traditional PACS infrastructure by shifting the analytical workload away from the imaging platform layer. Investors pricing AI disruption into Pro Medicus are not irrational.

Where the narrative becomes less precise is in its application to Pro Medicus’s specific position. Visage 7 is a platform that hosts, delivers, and enables the viewing of imaging data at speed. AI diagnostic tools need that data to operate. They are more likely to be integrated into the delivery layer, as clients or add-ons, than to replace it. This is the basis for CEO Sam Hupert’s “complementary” framing.

Structural disruption risk in ASX healthcare operates on a different timeline to cyclical macro headwinds: while rate and currency pressures have natural reversal points, policy-driven changes to FDA approval processes and US procurement behaviour carry no built-in correction mechanism, which is why AI disruption concerns specific to radiology IT deserve analysis that separates near-term sentiment from longer-run platform obsolescence scenarios.

The H1 FY2026 contract wins and the Maryland announcement suggest that hospital procurement cycles, which typically run 3-7 years in duration, are continuing to select Pro Medicus at pace. This is not proof that AI disruption will never materialise, but it is evidence that the buyers closest to the technology, hospital IT departments and procurement committees, are not yet behaving as if it will.

A substantial holder notice filed on 13 April 2026 may indicate institutional accumulation, though the filing alone does not confirm the direction or intent of the position change.

ASIC’s substantial holding notice rules require filers to disclose the nature of their relevant interest and the circumstances giving rise to it, which is why a single filing cannot confirm whether the position change represents accumulation, disposal, or a structural reclassification of an existing holding.

Three interpretations of the current Pro Medicus price are available to investors, and each requires believing something specific about the next three to five years.

| Interpretation | Growth assumption | Multiple direction | Competitive view |

|---|---|---|---|

| Overdone de-rating | Revenue growth sustains above 20% p.a. | Re-rates toward 100x+ as growth is confirmed | Cloud-native moat holds; AI integrates rather than displaces |

| Fair recalibration | Growth moderates to 15-17% p.a. | Multiple stabilises at 60-75x | Competitive position intact but premium narrows |

| Value trap | Growth decelerates below 15% p.a. | Multiple compresses further toward 40-50x | AI or competitor disruption erodes contract momentum |

“Reaction feels overcooked; 2H setup far better than price implies.” — Morgans, late March 2026

The analyst consensus target of AU$210 implies approximately 54% upside from the 9 May price. Morgans’ AU$275 target implies over 100% upside. Zero of 13-14 covering analysts carry a Sell rating.

What bounds the downside scenario is the financial profile itself. A company with 99.8% gross margins, AU$153M in net cash, zero debt, and a 39% three-year profit CAGR has materially more resilience than a leveraged peer facing the same valuation compression. Even the value trap scenario does not imply existential risk; it implies disappointing returns from a still-profitable business.

Quality stock valuations have narrowed toward their 10-year average relative to the broader market as of early 2026, meaning that the macro environment creating valuation pressure on high-multiple names like PME is simultaneously improving the relative entry point for quality-screened positions across the ASX, a dynamic that frames the current de-rating as part of a wider repricing rather than company-specific deterioration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Pro Medicus in May 2026 is a case study in the gap between business quality and price reasonableness. The 99.8% gross margin has not compressed. The 39% three-year profit CAGR has not reversed. The 50.7% ROE has not deteriorated. What changed is the multiple the market assigns to those results, and whether the new multiple is correct is the open question.

The durable investment principle at work here applies well beyond this single stock: premium-quality businesses frequently command premium valuations, and when those valuations compress, it does not automatically follow that either the quality or the opportunity has disappeared. The question is always what is now priced in, at AU$136.16 versus a consensus target of AU$210, and whether the forward revenue growth forecast of 17.7% per annum and ROE forecast of 39.1% justify the remaining 72.46x forward multiple.

The challenge of individual AI stock selection in technology-adjacent sectors parallels the dot-com experience closely: investors who correctly identified the internet as transformative still suffered severe losses by concentrating in the wrong companies, and the same dynamic is visible in 2026 ASX AI-exposed names where single-stock volatility has produced declines of 29-67% even while ETF-level exposure delivered positive returns.

Investors tracking this situation should monitor four signals in the months ahead:

The PME selloff is a live illustration of one of the most instructive and recurring patterns in growth stock investing. Investors who understand the distinction between quality and value will be better equipped for the next instance of it, regardless of whether they ultimately buy Pro Medicus at this price.

The PME share price decline is driven primarily by valuation de-rating rather than business deterioration. Analysts cite AI disruption fears in radiology IT and broader multiple compression across high-growth ASX technology stocks in a higher-for-longer interest rate environment.

A valuation de-rating occurs when the market lowers the earnings multiple it assigns to a stock without the underlying business fundamentals changing. In Pro Medicus's case, revenue and profit forecasts have remained broadly stable while the share price has fallen roughly 42% from January 2026, reflecting a repricing of the premium rather than a collapse in earnings.

Broker consensus places the Pro Medicus price target at approximately AU$210, implying around 54% upside from the 9 May 2026 price of AU$136.16. Morgans carries the most bullish target at AU$275, and zero of the 13-14 covering analysts hold a Sell rating.

AI diagnostic tools require imaging data to function and are more likely to integrate with platforms like Visage 7 than replace them. Pro Medicus CEO Sam Hupert described AI as complementary to the business during the February 2026 earnings call, and over AU$280M in new minimum contract value was signed in H1 FY2026, suggesting hospital procurement teams are not yet factoring disruption into vendor selection.

Pro Medicus reported a 99.8% gross margin, a 39% three-year net profit CAGR, a 50.7% return on equity, AU$153M in net cash, zero debt, and half-year revenue of AU$124.8M growing at 28.4% year-on-year, making it one of the most profitable software businesses listed on the ASX.