VGS Leads Vanguard ETF Pack With 14% FY26 Capital Return

1 hr ago

Most retail investors check the ASX 200 daily without asking how a company earns its place on it, or what had to happen years earlier before that inclusion was even possible. The path from private company to benchmark constituent involves two distinct gates: meeting the ASX’s eligibility standards to list at all, and then growing large and liquid enough to be selected for Australia’s most-watched equity index. These stages are connected, but they are governed by different rules, different bodies, and different timelines. What follows explains how the ASX works at both levels, walking through what the exchange requires before a company can list, how the S&P/ASX 200 index is constructed and updated, and what the distance between the two stages looks like in practice.

Listing on the ASX is a regulated admission process. It is not a commercial transaction any company can simply purchase once it reaches a certain size. The exchange maintains two eligibility pathways, each designed to ensure that companies seeking public capital meet a minimum standard of financial substance.

The first is the profit test: a company must demonstrate A$1 million in aggregated profit over the preceding three years, plus at least A$500,000 in consolidated profit in the most recent 12 months. The second is the assets test, which applies to companies that have not yet reached profitability but can demonstrate either A$4 million in net tangible assets or a market capitalisation of at least A$15 million. Companies using the assets test must also hold at least A$1.5 million in working capital.

The assets test threshold of A$4 million in net tangible assets is not an arbitrary number; it corresponds directly to the working capital and leverage signals that experienced investors extract from financial statements, and ASX balance sheet analysis converts those raw figures into the ratios that reveal whether a newly listed company is genuinely solvent or simply meeting the minimum bar.

The ASX Guidance Note 1 admission criteria codify both the profit test and assets test thresholds in detail, along with the shareholder spread requirements and free float minimums that every applicant must satisfy before its listing application can proceed.

| Criterion | Profit test | Assets test |

|---|---|---|

| Financial threshold | A$1M aggregated profit (3 years) + A$500K last 12 months | A$4M net tangible assets OR A$15M market cap |

| Working capital requirement | None specified | A$1.5M minimum |

| Minimum free float | 20% | 20% |

Both pathways exist for a reason. The profit test filters for established businesses with demonstrated earnings. The assets test accommodates earlier-stage companies, particularly in sectors such as biotech or technology, where revenue generation may lag behind capital deployment.

Financial thresholds are only part of the picture. The ASX also requires a minimum shareholder spread: at least 300 non-affiliated investors, each holding a parcel worth at least A$2,000. This rule exists to ensure that newly listed companies have genuine ownership diversity from day one, which in turn supports meaningful liquidity once trading begins.

A minimum free float of 20% reinforces this. It prevents a company from listing with the vast majority of its shares locked in insider hands, ensuring there is a sufficient pool of tradeable securities for market participants to buy and sell.

Clearing the eligibility gate is the beginning, not the end. Listing grants a company access to public capital markets and the continuous trading infrastructure of ASX Trade, but it also imposes ongoing disclosure and compliance obligations that persist long after the IPO.

Continuous trading runs from 10:00 AM to 4:00 PM AEST, flanked by pre-open and post-close phases that allow orders to queue and final prices to settle. During the main session, orders are matched electronically on a price-time priority basis, meaning the best-priced order entered first gets filled first. The system supports several order types:

One feature of the ASX that distinguishes it from some international exchanges is the absence of designated market makers. Liquidity depends entirely on participating buyers and sellers rather than a quoting party obligated to maintain two-sided markets. For investors, this means that thinly traded stocks can experience wider bid-ask spreads, particularly outside the largest 200 companies.

Regulatory oversight: ASIC oversees market conduct on the ASX under the Corporations Act. Listing obligations are not static; they evolve through ongoing consultation. For example, an amendment to Listing Rule 17.5, effective 16 January 2026, expanded suspension obligations for entities that file sustainability reports after the due date.

The S&P/ASX 200 is not a fixed list. It is a rule-governed, continuously maintained index, and the body that manages it is not the ASX itself but S&P Dow Jones Indices. Inclusion follows a published methodology rather than editorial discretion, and it is re-evaluated every quarter.

The index comprises the top 200 eligible ASX-listed companies ranked by float-adjusted market capitalisation. Float-adjusted weighting means that only freely tradeable shares count toward a company’s index weight; shares held by insiders or locked under escrow are excluded from the calculation. The practical effect is that the largest companies exert disproportionate influence on the index’s daily movement.

Rebalancing occurs quarterly, with effective dates in March, June, September, and December. At each review, S&P Dow Jones Indices recalculates rankings based on updated market caps and applies its liquidity screens. Companies that have fallen below the threshold are removed; those that have grown into range are added. There is no fixed minimum market cap for inclusion, but the smallest constituent at any given rebalance typically carries a capitalisation of approximately A$1-2 billion.

| Criterion | ASX listing eligibility | ASX 200 index eligibility |

|---|---|---|

| Minimum free float | 20% | 30% |

| Financial threshold | Profit test or assets test | Top 200 by float-adjusted market cap |

| Governing body | ASX (under ASIC oversight) | S&P Dow Jones Indices |

| Review frequency | At admission (ongoing compliance) | Quarterly rebalance |

For the 2024/25 financial year, the S&P/ASX 200 gained 9.97%, closing at 8,542.3 points.

Knowing how the index is constructed helps investors who hold ASX 200 ETFs or index funds understand why their portfolio composition shifts when a rebalance occurs, and what the triggers for those shifts actually are.

Over 2,000 companies are listed on the ASX. Only 200 belong to the benchmark index. That ratio reveals the gap: inclusion is not a merit badge awarded for meeting a fixed standard. It is a competitive ranking, and holding a position within it requires a company to remain larger and more liquid than more than 90% of its listed peers.

The distance between the two gates is measurable in specific criteria:

A company can list successfully and still spend years, or permanently, outside the index. The ASX 200 is indifferent to corporate ambition. It reflects where float-adjusted market cap places a company relative to its peers at each quarterly review.

The structural gap between listing and index inclusion has a compounding implication: cap-weighted index construction mechanically increases exposure to companies as they grow and reduces it as they shrink, which explains the persistent pattern of index outperformance over individual stocks across long measurement periods on the ASX.

Each quarterly rebalance typically involves a small number of additions and removals, not wholesale reshuffling. At the March 2025 rebalance, Strike Energy was among those added while Core Lithium was removed. At the June 2025 rebalance, Guzman y Gomez entered the index and Insignia Financial exited. These rotations illustrate the steady recalibration of the index at its margins.

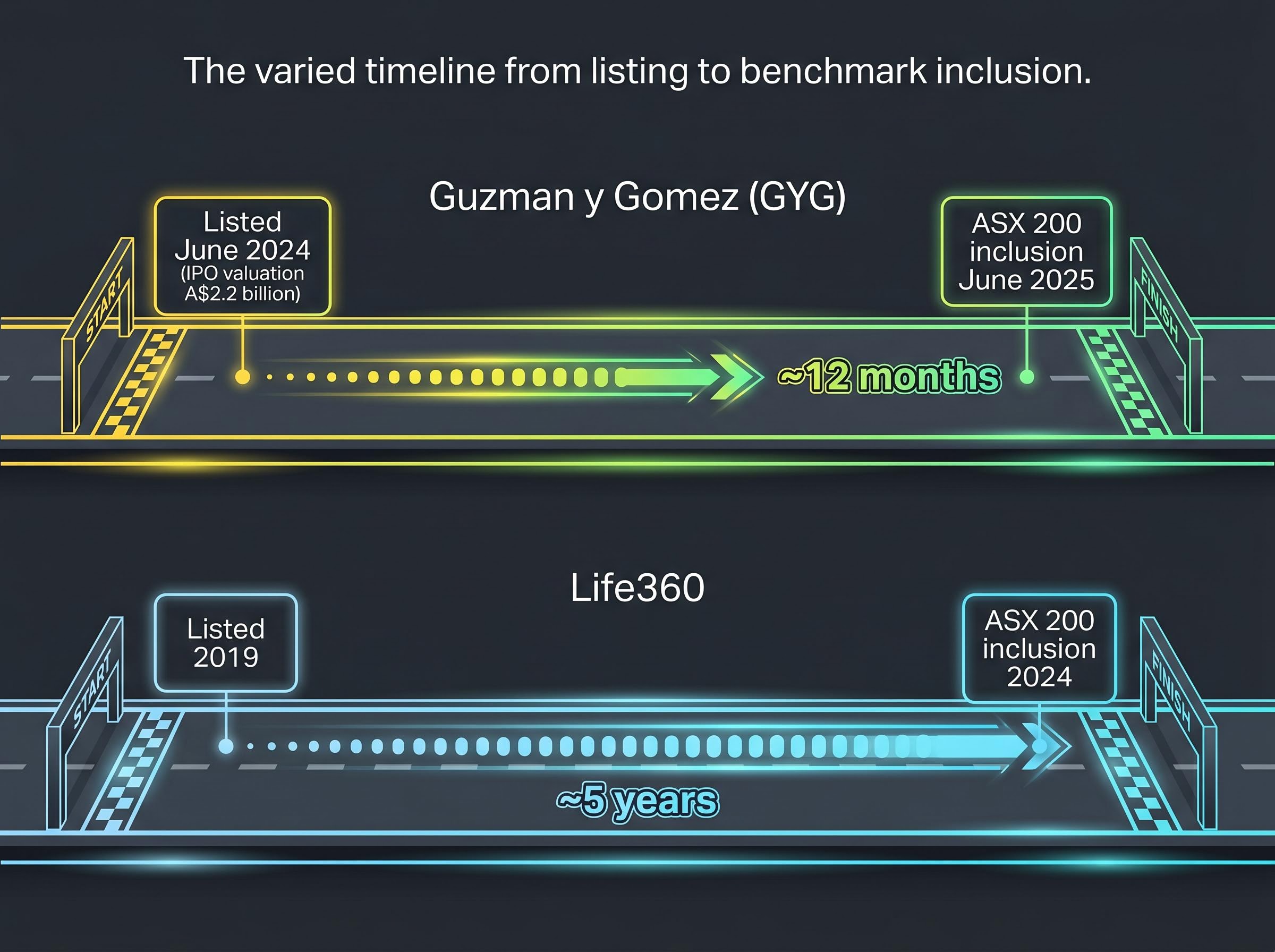

The timeline from listing to index inclusion is neither predictable nor short. Two recent cases illustrate how varied the path can be.

Guzman y Gomez (GYG) listed on the ASX in June 2024 with an IPO valuation of A$2.2 billion. Strong post-listing market cap growth pushed the fast-casual restaurant chain into the ASX 200 at the June 2025 rebalance, approximately 12 months after its debut.

Guzman y Gomez listed at an IPO valuation of A$2.2 billion in June 2024, one of the largest Australian food-sector listings of the year.

Life360, a family safety technology company, took a markedly different path. It listed in 2019 and did not achieve ASX 200 inclusion until 2024, approximately five years later. Its trajectory depended on sustained revenue growth and market cap expansion over multiple years.

| Company | Listing year | IPO valuation | Year of ASX 200 inclusion | Approximate time to index |

|---|---|---|---|---|

| Guzman y Gomez (GYG) | 2024 | A$2.2 billion | 2025 | ~12 months |

| Life360 | 2019 | Not widely reported | 2024 | ~5 years |

The index draws no distinction between a company that listed last year and one that listed a decade ago. Only current float-adjusted market cap rank and liquidity determine whether a company qualifies. For investors holding index-tracking products, these case studies show how the growth trajectories of individual companies directly affect what their ETF holds.

Every trade executed on ASX Trade passes through a post-trade infrastructure layer that most retail investors never see but rely on with each order. This layer has two distinct stages:

Clearing is the confirmation step. After a trade is matched, ASX Clear verifies the details, calculates obligations, and manages counterparty risk between the parties. A trade that has been cleared is confirmed but not yet finalised.

Settlement is the finalisation step. CHESS processes the actual transfer of securities and corresponding payment after a prescribed period following the trade. Until settlement is complete, the buyer does not formally hold the securities and the seller has not received payment.

ASIC provides regulatory oversight across these systems under the Corporations Act. APRA oversees financial stability for relevant entities within the broader market infrastructure. Together, these bodies ensure that the system supporting every ASX trade operates within a regulated framework.

ASIC oversight of ASX governance extends beyond listing rules: in April 2026, ASIC released its Final Report on a regulatory inquiry that had examined the exchange’s governance, capability, and risk management since mid-2025, resulting in a A$150 million capital charge and a 30 June 2026 deadline for ASX to reset its transformation program with both ASIC and the RBA.

The framework is straightforward once the two gates are visible. ASX listing is regulated by ASX Listing Rules under ASIC oversight. ASX 200 composition is governed by S&P Dow Jones Indices methodology. The criteria differ, the governing bodies differ, and the timelines differ.

The practical implications depend on how an investor engages with the market:

Investors who understand how the ASX 200’s competitive ranking works often look beyond it: the index’s structural concentration in banks and resources means quality-screened alternatives to the ASX 200 can provide materially different sector exposure, filtering for high return on equity and low financial leverage rather than float-adjusted size alone.

Both gates continue to evolve. Listing rules are subject to ongoing ASX consultation, as the January 2026 Listing Rule 17.5 amendment demonstrated. Index methodology is updated periodically by S&P Dow Jones Indices. The framework is stable, but it is not static.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A company must pass either the profit test (A$1 million aggregated profit over three years plus A$500,000 in the most recent 12 months) or the assets test (A$4 million in net tangible assets or A$15 million market capitalisation), along with a minimum 20% free float and at least 300 non-affiliated shareholders.

The S&P/ASX 200 is Australia's benchmark equity index comprising the top 200 ASX-listed companies by float-adjusted market capitalisation; it is governed and rebalanced quarterly by S&P Dow Jones Indices, not the ASX itself.

ASX listing requires clearing minimum financial and governance thresholds set by the exchange, while ASX 200 inclusion is a competitive ranking based on float-adjusted market cap and liquidity, reviewed quarterly by S&P Dow Jones Indices, with the smallest constituent typically worth around A$1-2 billion.

The ASX 200 is rebalanced quarterly in March, June, September, and December; companies are added or removed based on updated float-adjusted market capitalisation rankings and liquidity screens applied at each review.

The timeline varies considerably: Guzman y Gomez entered the index approximately 12 months after its June 2024 IPO, while Life360 took around five years from its 2019 listing to achieve inclusion in 2024.