How Zero Commissions Changed the Maths on Thematic ETFs

4 hrs ago

Australians earning $80,000 a year who salary sacrifice $500 a month into superannuation pay contributions tax at 15% rather than their 32% marginal rate. That 17-percentage-point gap, compounded over decades, is the structural advantage most investors never fully leverage.

The question of where to put $500 a month sits at the intersection of tax law, behavioural psychology, and long-term compounding. Most readers already know they should be investing. What they lack is a concrete, Australia-specific framework for structuring contributions across the vehicles actually available to them: superannuation salary sacrifice, ASX-listed ETFs through a brokerage account, or a deliberate blend of both.

This guide explains how each vehicle works, what the tax treatment costs or saves at typical Australian income levels, when liquidity matters more than tax efficiency, and how to automate the entire system so the decision is made once rather than revisited every pay cycle.

The choice between superannuation and exchange-traded funds is not a question of which is better. It is a question of which trade-off an investor is willing to make at their current stage of life. Super optimises for tax efficiency over long time horizons. ETFs preserve optionality. A blended strategy exists because the two vehicles solve different problems.

Superannuation is a legislated tax structure wrapping an investment portfolio. It is not a product in itself. Contributions made inside super are taxed at 15%, and investment earnings during the accumulation phase are also taxed at 15% (with an effective rate of 10% on capital gains held longer than 12 months). Earnings become tax-free only in the pension phase after age 60 for Australians born after 1 July 1964.

The concessional contributions cap is $30,000 per annum for FY 2024-25 onward. Employer Superannuation Guarantee contributions of 12% of ordinary time earnings (for FY 2025-26) count toward that cap. This means salary sacrifice room must be calculated net of what the employer already contributes.

Exchange-traded funds are pooled index-tracking products listed on the ASX. They are bought and sold like shares through a brokerage account, with full liquidity and no structural tax advantage on contributions. BetaShares A200 and Vanguard VAS both track Australian equities with near-identical exposure but different management costs: A200 charges a management expense ratio (MER) of 0.04%, while VAS charges 0.10%. Vanguard VGS, which tracks international developed markets, charges 0.18%.

ASX-listed ETFs have attracted 2.69 million Australian investors as of 2025, with the market reaching $330.6 billion in funds under management, reflecting a structural shift in how everyday investors access diversified index exposure at costs as low as 0.04% per year.

ETFs can sit inside or outside super. When held outside super, dividends are taxed at the investor’s marginal rate, and the 50% capital gains tax discount applies for assets held longer than 12 months.

The table below compares the two vehicles across the five dimensions that matter most for a contribution decision.

| Attribute | Superannuation | ETFs (outside super) |

|---|---|---|

| Contributions tax treatment | 15% on concessional contributions | Made from after-tax income (no upfront advantage) |

| Earnings tax rate | 15% in accumulation phase | Marginal rate on dividends and income |

| Capital gains treatment | 10% effective (for gains held 12+ months) | Marginal rate with 50% CGT discount (held 12+ months) |

| Access before age 60 | Locked (except specific hardship provisions) | Fully accessible at any time |

| Typical annual costs | Fund administration fee + investment option MER | MER only (e.g., 0.04% for A200) |

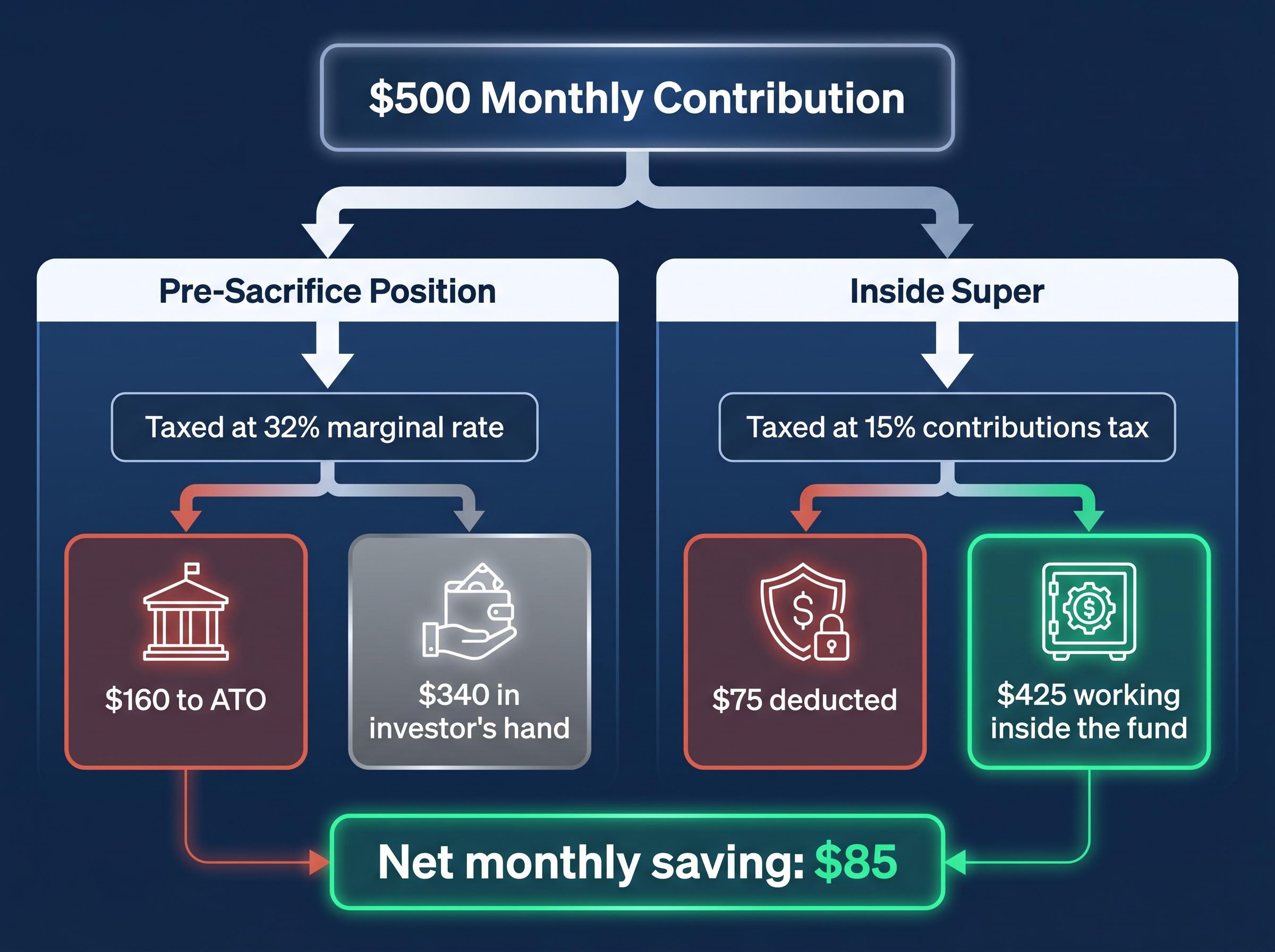

The 17-percentage-point advantage is not an abstraction. For an Australian earning $80,000 to $120,000, it is a specific dollar figure that shows up every month.

Here is how the calculation works for a $500 monthly salary sacrifice:

For an Australian in the $45,001-$135,000 tax bracket, every dollar salary sacrificed into super is taxed at 15% rather than 32%, a 17-percentage-point advantage that compounds from the first contribution.

That $85 per month is not a rounding error. At 8% annual growth, it compounds into a substantial balance differential over 20 years that a side-by-side ETF strategy cannot replicate without the same upfront contribution.

Two qualifications matter. First, accumulation-phase earnings inside super are taxed at 15%, not zero. Projections that model super growth as tax-free overstate the advantage. Second, earners approaching $250,000 in combined income and concessional contributions face Division 293 tax, which lifts the effective super contributions rate to 30%, significantly narrowing the gap.

For ETFs held outside super, franking credits on Australian equity distributions (from holdings such as VAS or A200) can offset marginal-rate tax liability. This is a meaningful advantage not available on international ETFs such as VGS. The 50% CGT discount for assets held longer than 12 months also partially narrows the capital gains gap between ETFs and super.

The numbers speak before the commentary does.

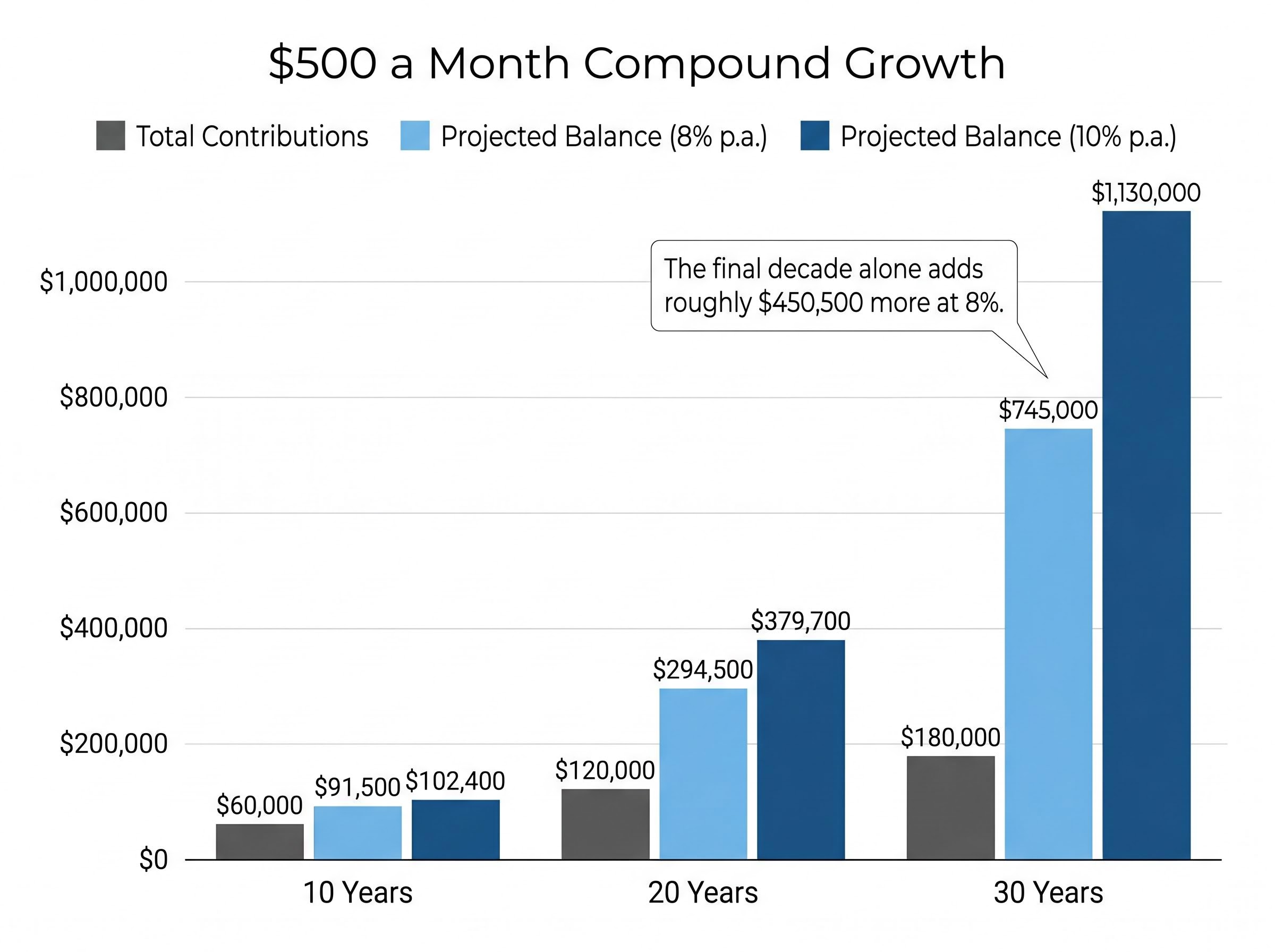

| Time horizon | Total contributions | Projected balance (8% p.a.) | Projected balance (10% p.a.) |

|---|---|---|---|

| 10 years | $60,000 | ~$91,500 | ~$102,400 |

| 20 years | $120,000 | ~$294,500 | ~$379,700 |

| 30 years | $180,000 | ~$745,000 | ~$1,130,000 |

At $500 a month and 8% annual growth, the first 20 years produce approximately $294,500. The final decade alone adds roughly $450,500 more. The acceleration is not intuitive, but it is the single most important feature of compounding: the last decade produces more growth than the first two decades combined.

The final decade of a 30-year investment period produces more growth than the preceding two decades combined. Pausing contributions during downturns disproportionately costs investors this late-stage acceleration.

At 10% annual growth, closer to the Australian share market’s historical average of approximately 9-10% per year inclusive of dividends over 30 years, the same $500 monthly contribution could exceed $1.1 million.

Context matters here. According to APRA’s December 2025 quarterly data, the average super balance for Australians aged 60-64 is $395,852 for men and $313,360 for women. The Association of Superannuation Funds of Australia (ASFA) estimates a comfortable retirement requires approximately $595,000 for singles and $690,000 for couples. The gap between average balances and adequacy benchmarks is substantial, and it underscores why structured additional investing beyond employer SG contributions carries urgency.

Accumulation-phase super projections must be modelled at 15% earnings tax, not zero, to give an accurate comparison with ETF growth scenarios. The figures above represent pre-tax projections; the net outcome inside super will be slightly lower after the 15% earnings tax is applied, though still ahead of the marginal-rate tax treatment applied to ETF earnings outside super.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The allocation decision rests on two variables an investor can assess immediately: marginal tax rate and years to preservation age.

The calculation takes three steps. First, multiply annual salary by 12% to determine employer SG contributions. For an $80,000 salary, employer SG equals $9,600. Second, subtract the employer contribution from the $30,000 concessional cap: $30,000 minus $9,600 equals $20,400 of available salary sacrifice space. Third, confirm the intended contribution sits within that space. At $500 per month ($6,000 per year), the contribution is well within cap for most earners on $80,000 or above.

Carry-forward provisions allow use of unused cap space from the prior five financial years if total super balance is below $500,000.

Carry-forward contributions allow eligible Australians to deploy up to five years of unused concessional cap space in a single year, and unused amounts from the 2020-21 financial year expire permanently on 30 June 2026, creating a hard deadline for members who have not yet acted on that capacity.

Salary sacrifice must be arranged with an employer before the relevant pay period and cannot be applied retrospectively.

Three illustrative allocation profiles provide a starting framework:

The split is not permanent. As income grows, as time horizons shorten, and as super balances approach adequacy benchmarks, the optimal ratio shifts. The framework here provides a starting allocation to revisit annually.

These statements are general in nature. Investors should consult a licensed financial adviser for personalised advice on the salary sacrifice to ETF allocation ratio, as individual circumstances vary significantly. ASIC’s MoneySmart website (moneysmart.gov.au) provides additional comparison tools.

Strategies that require active monthly decisions consistently fail. Spending decisions compete with investing decisions in the same mental budget at the same moment, and spending almost always wins.

The structural solution is to ensure contributions leave the account within 24 hours of pay day, before discretionary spending patterns activate. This is the mechanism behind “pay yourself first”: the money is redirected before the temptation to spend it arrives.

Consistent behaviour over time is a more decisive factor in long-term wealth outcomes than investment selection, income level, or market timing.

Salary sacrifice into super has one structural advantage beyond tax efficiency: the contribution never reaches the investor’s bank account. The behavioural friction of the transfer decision is removed entirely. ETF contributions require deliberate setup to match this automation, but it is achievable.

$500 per month is approximately $16.50 per day. Framed this way, the commitment feels proportionate to the outcome it produces over decades.

Market corrections can produce 20-30% portfolio value declines. Financial media typically frames these negatively, which is precisely the moment most investors pause contributions. Yet automated contributions during a correction purchase more units at lower prices, making consistency during downturns mathematically advantageous over the long term. Investors who maintained contributions through past downturns have historically achieved stronger long-term wealth outcomes than those who paused and waited for recovery.

The automation setup requires four steps:

Once these four steps are complete, the monthly investment runs without further decisions.

Platform selection matters less than the decision to start. The goal of this section is implementation: close the article, take the first concrete action within 30 minutes.

Three account types are required: a superannuation fund (chosen or employer default), a brokerage account for ETFs, and a dedicated high-interest transaction or savings account as the liquidity buffer. Standard financial planning guidance recommends three to six months of expenses in accessible savings before redirecting surplus to investment accounts.

Australians with multiple super accounts from previous employers pay duplicate administration and insurance fees. Consolidation through the myGov portal is a priority step before increasing contributions. The ATO’s YourSuper comparison tool and APRA’s published fund performance data provide objective benchmarks for fund selection.

The steps are straightforward: provide a tax file number, verify identity, link a bank account, confirm CHESS sponsorship status, and fund the account before setting up the recurring transfer schedule.

CHESS-sponsored accounts give the investor direct ownership of shares registered in their name with ASX Settlement, the system that records and settles trades on the exchange. Custodian models hold shares on behalf of the investor through the platform. For long-term investors, the CHESS-sponsored model provides a layer of protection if the platform itself experiences financial difficulty, though it should not be a reason to delay the first contribution while researching indefinitely.

Platforms available to Australian investors include CommSec, SelfWealth, Pearler, and Stake (fees and features should be verified directly with each provider, as they change frequently). When evaluating a brokerage platform, consider:

Micro-investing apps such as Raiz and Spaceship provide lower-barrier entry but typically carry higher proportional fees at small balances. Most investors should transition to direct ETF platforms once monthly contributions reach $200-$500. Stockspot offers a managed ETF portfolio service and a separate super product for investors who prefer a managed rather than DIY approach.

All product decisions should be made with reference to individual circumstances. ASIC MoneySmart (moneysmart.gov.au) provides independent comparison tools, and investors should consider seeking advice from a licensed financial adviser.

The vehicle choice, whether super, ETFs, or both, matters less than having a structure that runs automatically regardless of market conditions or fluctuations in personal motivation.

Three decisions define the framework. First, determine the salary sacrifice amount within the concessional cap. Second, select an ETF allocation and platform. Third, set the automation schedule so the system operates without monthly intervention.

As income grows and balances compound, the annual review becomes the only active decision required. Revisit the super-to-ETF ratio once per year, check the contribution against the concessional cap (particularly if salary has changed), and confirm the automation is running.

Long-term wealth accumulation across 10-20 year horizons is governed by a small number of compounding mechanics that most investors understand conceptually but rarely apply with structural discipline: uninterrupted time in market, total-return reinvestment rather than income withdrawal, and minimising tax drag through vehicle selection at the point of contribution rather than after returns have already been diluted.

For practical next steps, ASIC MoneySmart provides budgeting tools and the ATO’s myGov portal allows investors to check existing super balances and consolidate accounts. The YourSuper comparison tool supports fund selection. For personalised advice, particularly on the salary sacrifice to ETF allocation ratio, consulting a licensed financial adviser is recommended.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Salary sacrifice into superannuation is an arrangement where you redirect a portion of your pre-tax salary into your super fund, meaning those contributions are taxed at 15% rather than your marginal income tax rate, which can be as high as 47%.

The concessional contributions cap is $30,000 per financial year for FY 2024-25, which includes both your employer's Superannuation Guarantee contributions and any additional salary sacrifice amounts you arrange.

Superannuation offers significant tax advantages on contributions and earnings but locks your money away until at least age 60, while ETFs held outside super are fully accessible at any time but contributions are made from after-tax income with earnings taxed at your marginal rate.

A practical starting point is to calculate your available salary sacrifice room within the $30,000 concessional cap, direct a portion to super via a salary sacrifice agreement with your employer, and set up an automated direct debit to a brokerage account for the remainder to purchase low-cost ASX ETFs like A200, VAS, or VGS.

Carry-forward contributions allow eligible Australians with a total super balance below $500,000 to use any unused concessional cap space from the previous five financial years in a single year, with unused amounts from FY 2020-21 expiring permanently on 30 June 2026.