On 7 May 2026, the Australian Prudential Regulation Authority (APRA) has continued to maintain its guidelines on the recognition of External Credit Assessment Institutions (ECAIs), a document that has remained in continuous effect since its publication in 2013. APRA’s recognition framework governs how regulated institutions qualify and use external credit ratings for capital adequacy purposes under the Standardised Approach. For compliance teams, treasury desks, and risk officers across Australia’s banking and insurance sectors, understanding the current framework is an immediate priority: what applies in practice, and what does not? This article sets out what the framework covers, how ECAI ratings continue to function under existing prudential standards, and what APRA’s broader regulatory direction signals for the future.

APRA pulls its ECAI recognition guidelines for the first time in over a decade

APRA’s announcement arrived without fanfare. The regulator confirmed the temporary withdrawal of its ECAI recognition guidelines, a document last substantively updated in 2013, citing a periodic review of the framework. No completion date for the review has been specified.

Three confirmed facts define the current position:

- Date of withdrawal: 7 May 2026

- Document status: Temporarily withdrawn pending periodic review; the guidelines had been in continuous effect since 2013

- Stakeholder direction: APRA has directed institutions with questions to its official enquiries channel during the interim period

The absence of a timeline is the detail that matters most. A temporary withdrawal with a six-month horizon is a scheduling exercise. A temporary withdrawal with no specified end date is a planning variable, one that compliance and risk teams cannot resolve internally and must monitor externally.

When big ASX news breaks, our subscribers know first

What ECAIs are and why APRA’s recognition framework exists

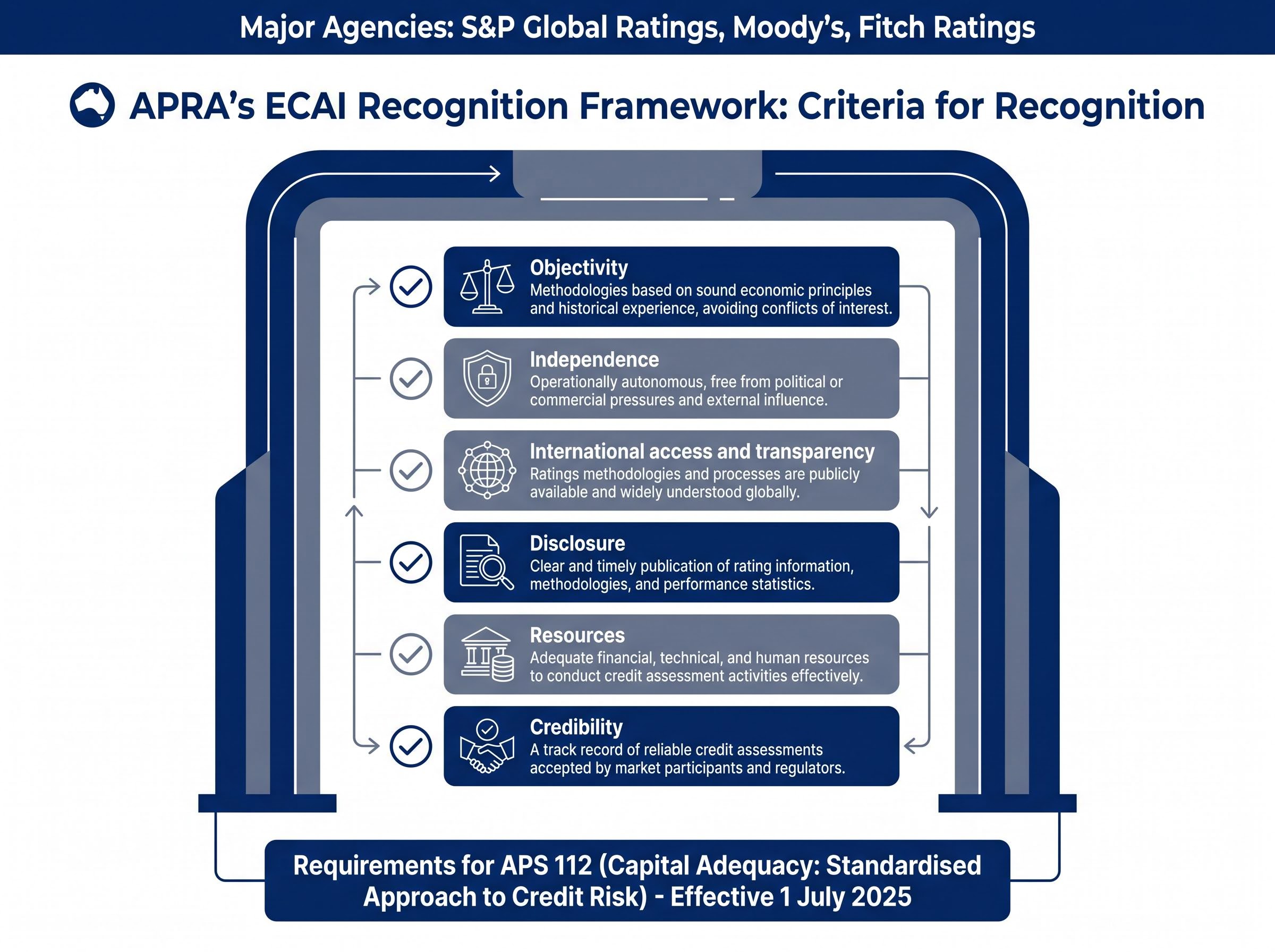

External Credit Assessment Institutions are the credit rating agencies, S&P Global Ratings, Moody’s, Fitch Ratings, and their equivalents, whose ratings regulated institutions use to determine risk weights under the Standardised Approach to credit risk. When a bank holds a corporate bond rated AA- by a recognised ECAI, that rating feeds directly into the risk weight applied to the exposure, which in turn determines how much capital the bank must hold against it.

APRA does not accept ratings from any agency automatically. Its recognition framework requires ECAIs to meet six criteria:

- Objectivity

- Independence

- International access and transparency

- Disclosure

- Resources

- Credibility

These criteria function as a gate. Only agencies that satisfy all six can have their ratings used for regulatory capital purposes under APS 112 (Capital Adequacy: Standardised Approach to Credit Risk), which became effective 1 July 2025.

The Basel Committee criteria for recognising ECAIs under the Standardised Approach establish the international foundation that national regulators like APRA build upon, and the six criteria in APRA’s framework — covering objectivity, independence, transparency, disclosure, resources, and credibility — closely reflect the BCBS template.

Why formal APRA recognition matters for capital calculations

The chain is direct: APRA recognises an ECAI, the ECAI rates an exposure, and the regulated institution applies the corresponding risk weight from APS 112 to that exposure when calculating its capital requirement. Ratings from unrecognised agencies carry no weight in this process.

This matters most for smaller and regional authorised deposit-taking institutions (ADIs) that rely on the Standardised Approach rather than internal ratings-based (IRB) models. Major banks with IRB approval use ECAI ratings as benchmarks for calibration, but their capital calculations do not depend on external ratings in the same way. For Standardised Approach users, the recognition framework is not supplementary; it is a functional prerequisite.

This matters most for smaller and regional authorised deposit-taking institutions (ADIs) that rely on the Standardised Approach rather than internal ratings-based (IRB) models. The ADI licence framework APRA administers governs not only capital adequacy but also the conditions under which institutions can operate and exit the regulated system.

How risk weights and capital rules continue to apply during the review

The withdrawn guidelines governed the recognition process. They did not define the capital rules themselves. That distinction is the single most important fact for any institution assessing the practical impact of the withdrawal.

APS 112, effective since 1 July 2025, remains fully operative. Its Attachment A sets out the risk weight mappings that regulated institutions apply to ECAI-rated exposures, and those mappings are unchanged.

The APS 112 Attachment A risk weight mappings set out the specific percentage weights that regulated institutions must apply to ECAI-rated exposures across sovereign, bank, and corporate categories, and those tables remain the operative reference for capital calculations regardless of the recognition guidelines review.

| Credit Rating Band | APS 112 Risk Weight | Typical Exposure Category |

|---|---|---|

| AAA to AA- | 20% | Sovereign, bank, and corporate exposures |

| BBB+ to BBB- | 50% | Investment-grade corporate exposures |

| Below BB- | 150% | Sub-investment-grade exposures |

APS 112 remains fully operative. The withdrawn guidelines supplemented the recognition process; they did not define the capital rules themselves.

Day-to-day capital calculations for ECAI-rated exposures proceed without interruption. The interim gap applies to the process by which new agencies might seek recognition or existing recognition might be reassessed, not to the operative risk weight framework.

What the review signals about APRA’s evolving prudential framework

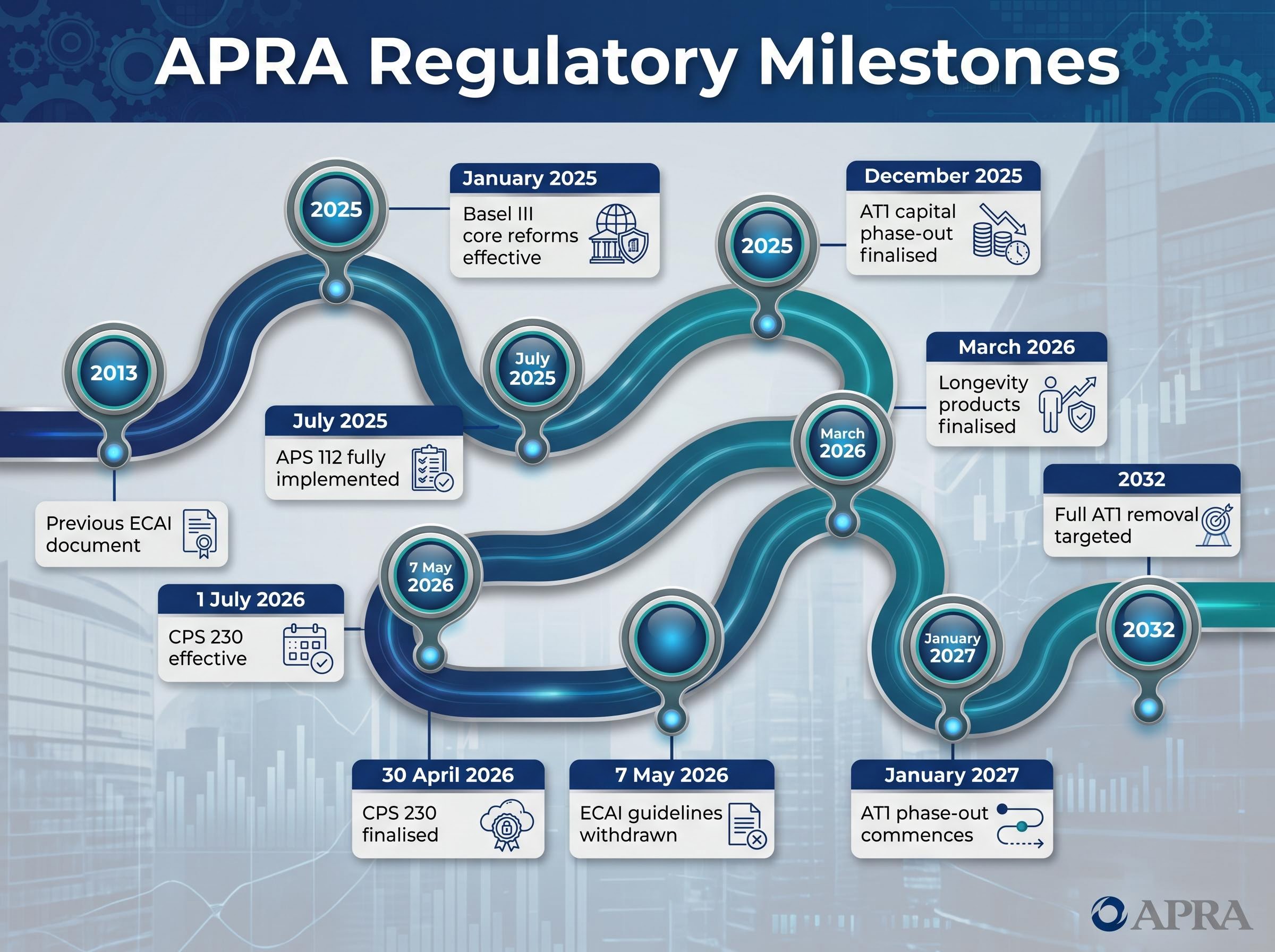

The ECAI guidelines withdrawal does not sit in isolation. APRA has been running one of its most active reform calendars in recent memory, and the review of a 2013-era supplementary document fits a pattern of systematic modernisation rather than ad hoc housekeeping.

Concurrent reform milestones include:

- CPS 230 operational risk amendments: Finalised 30 April 2026, effective 1 July 2026, introducing exemptions for non-traditional service providers and updated guidance for material service provider management

- AT1 capital phase-out: Finalised December 2025, commencing January 2027, with full removal of Additional Tier 1 instruments targeted by 2032

- Longevity products capital changes: Finalised March 2026, introducing an advanced illiquidity premium option for annuity product capital treatment

- Basel III core reforms: Effective January 2025, with APS 112 fully implemented by July 2025

APRA oversees a large regulated sector. The regulator’s decision to review guidelines that predate the current APS 112 architecture by more than a decade aligns with broader international trends toward refreshing static ECAI recognition criteria into more principles-based supervisory frameworks. With the Basel III foundation now in place, auditing the supplementary guidance that was written for an earlier standards architecture is a logical next step.

The same reform momentum underpins APRA’s CPS 234 enforcement posture, with the regulator’s 30 April 2026 supervisory letter making clear that board-level accountability for technology and operational risk gaps will be treated as a measurable compliance obligation rather than aspirational guidance.

The next major ASX story will hit our subscribers first

What regulated institutions should do while the review is underway

The practical posture for institutions during the interim period is straightforward, if not quite business-as-usual in terms of regulatory monitoring.

- Continue applying APS 112 without interruption. The risk weight mappings in Attachment A remain the operative reference for all ECAI-rated exposures. No change to capital calculation processes is required.

- Route unresolved recognition questions to APRA’s official enquiries channel. Any institution that encounters a question about ECAI recognition that cannot be resolved by reference to APS 112 alone should use the formal contact point APRA has designated for the interim period.

- Flag the review in regulatory monitoring workplans. The absence of a specified completion date means compliance and risk teams should treat this as an open item requiring periodic checking rather than a time-bound deliverable. Being positioned to act promptly when updated guidance is issued will reduce the adjustment burden.

Institutions that maintain their existing APS 112-based processes and keep the review on their regulatory radar are positioned to absorb any updated guidance without operational disruption.

For compliance officers and risk teams wanting to map these concurrent supervisory pressures to their own governance frameworks, our full explainer on APRA’s board-level AI governance expectations covers the specific accountability standards, CPS 234 interpretive weight, and board literacy requirements APRA has now made enforceable across banking, insurance, and superannuation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A framework in transition, not in doubt

The withdrawal of APRA’s ECAI recognition guidelines is a process step, not a signal of instability in Australia’s credit risk capital framework. APS 112 continues to govern how external ratings translate into risk weights and capital requirements. The broader context of APRA’s 2025-2026 reform agenda, from CPS 230 to the AT1 phase-out to Basel III implementation, confirms that this review is part of a deliberate modernisation exercise.

When the replacement guidance arrives, it will need to reflect the post-Basel III standards architecture that the 2013 document was never designed to serve. Regulated institutions and their advisers should monitor APRA’s website and enquiries channel for updates as the review progresses.

—