BlackRock Raises AI and Tech Decoupling to Top Risk Tier

Jul 11, 2026

AMD shares surged roughly 17% after hours on 5 May 2026, a move large enough to lift the entire semiconductor sector into premarket green before most investors had finished reading the headline. The catalyst was a Q1 2026 earnings report that beat revenue consensus by approximately $500 million and a Q2 guidance figure that reset expectations for what AMD’s data centre business can produce at scale. The reaction was not contained to AMD: Intel and ARM Holdings both climbed in premarket trading, signalling that the market interpreted AMD’s results as a sector-wide re-rating event rather than company-specific outperformance.

This article covers what AMD actually reported, why the market reacted as sharply as it did, what Wall Street analysts are saying about AMD’s positioning in the agentic AI era, and what the server CPU total addressable market (TAM) revision means for investors holding or evaluating the stock.

AMD reported total revenue of $10.3 billion against a Wall Street consensus of $9.8 billion, a beat of roughly $500 million that represented 38% year-over-year growth from $7.45 billion in Q1 2025. The scale of the miss in consensus expectations becomes clearer once the divisional breakdown is laid out.

Data centre revenue drove the headline: $5.775 billion, up 57% year over year. But the beat was not a single-segment story. Client revenue came in at $2.9 billion (+26% YoY), while gaming revenue reached $720 million (+11% YoY), meaning every reported segment reinforced rather than diluted the top-line outperformance.

| Segment | Q1 2026 Revenue | Q1 2025 Revenue | YoY Growth |

|---|---|---|---|

| Data Centre | $5.775B | — | +57% |

| Client | $2.9B | — | +26% |

| Gaming | $720M | — | +11% |

| Total | $10.3B | $7.45B | +38% |

On the profitability side, three metrics stood out:

The breadth of the beat across all segments signals structural demand rather than a one-division spike, and that distinction matters for whether the stock sustains its post-earnings move or fades.

AI infrastructure capital flows have shifted materially toward physical hardware and energy assets, with Wall Street projecting $530-$700 billion in global data centre IT spending for 2026 alone, a spending baseline that creates the demand environment AMD’s data centre segment is now directly benefiting from.

The after-hours surge was less about what AMD had already done and more about what it told the market to expect next. Q2 revenue guidance landed at approximately $11.2 billion, against an implied consensus range of $10.5-$11.0 billion, pointing to sequential growth of roughly 9% from Q1.

The guidance metrics in full:

That margin expansion is worth isolating. A company guiding to 56% non-GAAP gross margins while simultaneously accelerating top-line growth is telling the market that its pricing power and product mix are improving in parallel, not one at the expense of the other.

AMD’s Q1 2026 earnings press release confirms total revenue of $10.3 billion, non-GAAP diluted EPS of $1.37, and the Q2 2026 revenue guidance of approximately $11.2 billion, providing the primary source figures underpinning the consensus beat calculations cited throughout analyst commentary.

CFO Jean Hu described the data centre segment as undergoing a “structural inflection in growth” on the 5 May earnings call, framing the guidance beat as a reflection of durable demand shifts rather than a one-quarter pull-forward.

Guidance beats force analyst model revisions forward. That mechanical process, price targets being rebuilt around higher forward revenue and margin assumptions, is the reason the after-hours reaction was disproportionate to the Q1 beat alone.

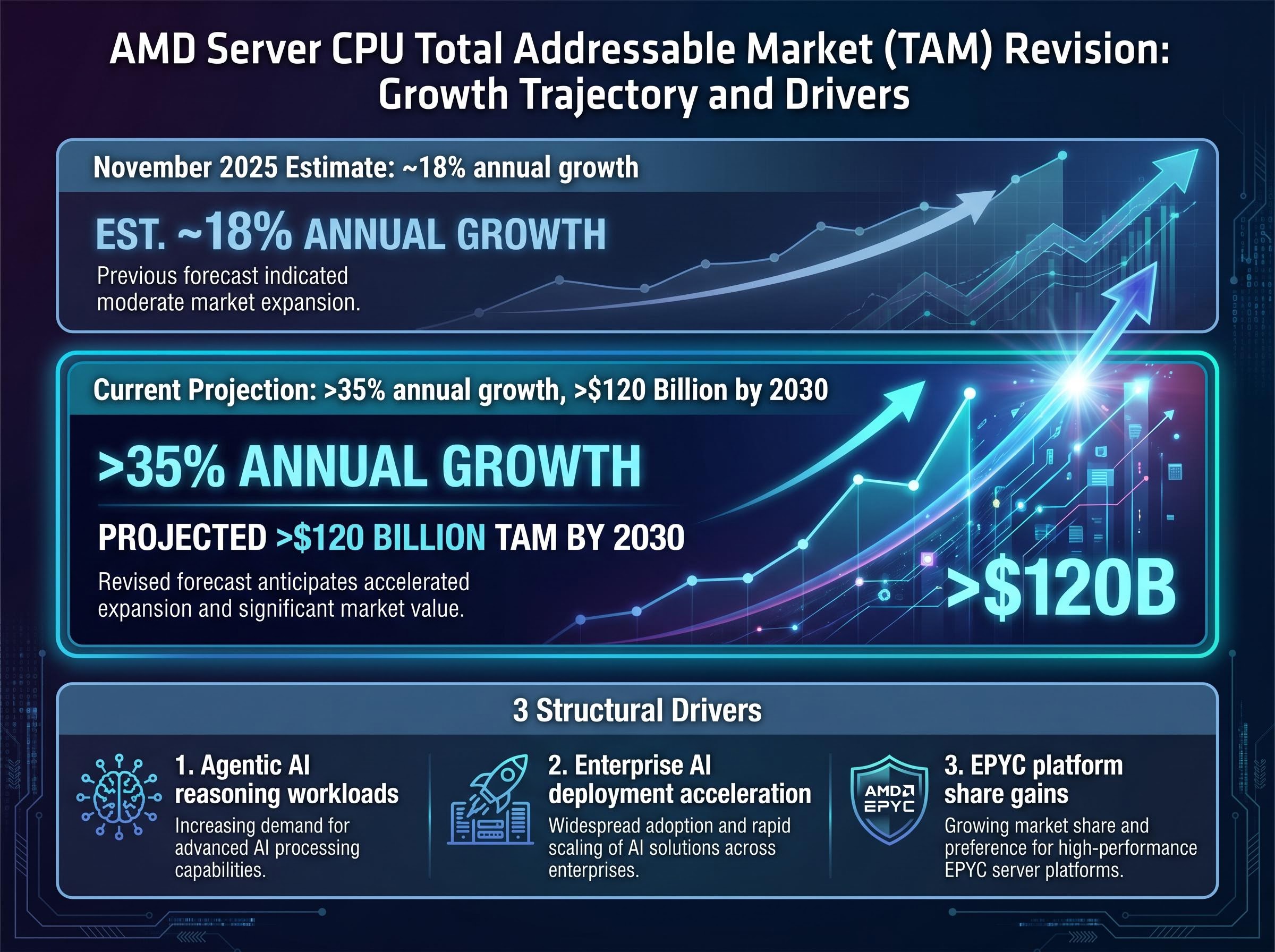

According to unverified figures not confirmed against AMD’s official press release, AMD projects the server CPU TAM at more than $120 billion by 2030, growing at greater than 35% annually.

That figure demands context. In November 2025, AMD estimated the same market growing at approximately 18% annually. The revision nearly doubled the projected growth rate.

The total addressable market for server CPUs is the total revenue opportunity available to all companies selling processors for data centre servers. When AMD revises it upward, it is not claiming AMD itself will capture that entire figure; it is saying the market all server CPU makers are competing for has grown dramatically.

Three structural drivers underpin the revision:

CEO Lisa Su emphasised accelerating AI infrastructure demand on the 5 May earnings call, positioning AMD’s EPYC and Instinct product lines as direct beneficiaries.

For investors, the maths is straightforward. A TAM revision of this magnitude changes the denominator in any market share calculation: even a flat percentage share now implies dramatically higher absolute revenue potential through 2030.

The analyst reaction split cleanly into two camps, and the split itself tells investors where the debate now sits.

JPMorgan reaffirmed its Overweight rating with a $350 price target on 6 May, citing the data centre beat as validation of AMD’s AI infrastructure thesis. Jefferies went further, raising its target to $375 with a Buy rating, characterising agentic AI demand as additive to, not cannibalistic of, the GPU TAM.

The measured counterpoints came from Goldman Sachs and Morgan Stanley. Goldman raised its target from $210 to $240 but maintained a Neutral rating, suggesting the beat did not resolve longer-term valuation concerns. Morgan Stanley raised from $255 to $360 but held Equal Weight, a significant target increase paired with a rating that says the move may already be reflected in the price.

Northland moved in the opposite direction entirely, downgrading AMD to Market Perform.

| Firm | Rating | Prior Target | New Target | Key Thesis |

|---|---|---|---|---|

| JPMorgan | Overweight | — | $350 | Data centre beat validates AI thesis |

| Jefferies | Buy | — | $375 | Agentic AI demand is additive to GPU TAM |

| Goldman Sachs | Neutral | $210 | $240 | x86 positioning strong; valuation concerns remain |

| Morgan Stanley | Equal Weight | $255 | $360 | Beat acknowledged; multiple debate unresolved |

| Northland | Market Perform | — | $260 | Downgraded post-earnings |

Goldman Sachs has separately highlighted x86 architecture advantages for agentic AI, arguing that enterprise software built on x86 does not require re-architecture for AI agent workloads, positioning AMD’s EPYC processors as infrastructure that benefits from AI adoption without needing to displace NVIDIA directly.

Bank of America has estimated AMD could approach approximately 50% CPU market share, though this figure has not been independently verified and should be treated with appropriate caution.

The split between bullish and neutral ratings tells investors the debate has shifted from “can AMD execute?” to “at what multiple should that execution be valued?”, a materially different risk conversation.

A $60 billion Meta chip supply agreement covering five years of MI300X and MI325X GPU shipments beginning in H2 2026 adds a contractually anchored revenue layer to AMD’s data centre growth story that the headline quarterly figures alone do not capture, providing multi-year demand visibility that analysts at Goldman Sachs have described as de-risking a significant portion of AMD’s 2027 revenue.

Intel’s premarket gain on 6 May was the clearest signal that the market read AMD’s results as a demand story, not a share-theft story. If investors had interpreted AMD’s data centre beat as purely competitive wins against Intel, Intel would have sold off. Instead, Intel rallied, suggesting the market believes overall enterprise AI server spending is expanding at a pace that lifts both companies.

The semiconductor sector dynamics playing out around Intel extend beyond AMD’s earnings call: Apple’s preliminary discussions with Intel and Samsung about US-based chip manufacturing, which emerged on 5 May 2026, add another layer to the Intel investment thesis, with the market pricing execution risk rather than potential revenue into Intel’s share price despite the strategic appeal of diversifying away from TSMC.

Three sympathy-move data points framed the morning’s premarket session:

ARM’s simultaneous move is particularly notable because it operates on a different architecture entirely. When both x86 (AMD, Intel) and ARM-based processors rally on the same earnings report, the signal is about total AI infrastructure spending, not architecture-specific share dynamics.

Samsung reaching $1 trillion market capitalisation on 6 May places it alongside TSMC as only the second Asian company to reach that threshold. The milestone reflects capital rotating into hardware AI infrastructure globally, extending the investment thesis beyond US-listed semiconductor names.

Investors positioned only in AMD, or only in one segment of the AI hardware trade, may be underexposed to the breadth of the infrastructure spending cycle that AMD’s results are now helping to validate.

The earnings report established a thesis. The next question is where the evidence either extends or complicates it.

Three forward catalysts, in priority order:

AMD stock entered 6 May up approximately +20% year to date, a figure that frames how much of the forward thesis may already be priced into the current share price.

For investors weighing whether to enter or add to a position after the post-earnings move, the July event represents the next point at which new information could materially shift the risk-reward calculation. The Q1 beat and Q2 guidance reset the baseline; the product roadmap and customer pipeline will determine whether the TAM revision translates into sustained revenue acceleration or remains a projection.

AMD’s Q1 beat and Q2 guidance revision represent a structural re-rating of the server CPU market opportunity, not a one-quarter outperformance story. The near-doubling of AMD’s own TAM growth rate estimate, from 18% to more than 35% annually, reframes the revenue potential of the EPYC platform through 2030.

The analyst reaction reflects this honestly. Operational execution is broadly acknowledged across Wall Street, but the multiple debate remains open. The gap between Jefferies’ $375 target and Goldman Sachs’ $240 target captures the range of views on what that execution is worth. Any new buyer is accepting that tension.

The 22-23 July “Advancing AI 2026” event and the 6th Generation EPYC launch cycle represent the next evidence gates. Product specifics, customer commitments, and roadmap clarity at that event will either extend or stress-test the narrative this earnings cycle established.

Investors weighing the multiple debate after AMD’s post-earnings move will find our full explainer on AI hardware valuation risks a useful counterpoint: it examines why escalating inference costs are making generative AI applications structurally unprofitable, what a deceleration in hyperscaler 2027 capex guidance would mean for semiconductor valuations, and why derivative markets may be underpricing earnings-driven correction risk in major technology positions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The server CPU total addressable market is the total revenue opportunity available to all companies selling processors for data centre servers. AMD revised its growth rate estimate for this market from approximately 18% annually to more than 35% annually, projecting the market will exceed $120 billion by 2030, which significantly raises the revenue ceiling for AMD's EPYC platform.

AMD reported Q1 2026 total revenue of $10.3 billion against a Wall Street consensus of $9.8 billion, a beat of approximately $500 million representing 38% year-over-year growth, with adjusted non-GAAP EPS of $1.37 also exceeding consensus of $1.25-$1.30.

AMD guided Q2 2026 revenue to approximately $11.2 billion, above an implied consensus range of $10.5-$11.0 billion, representing sequential growth of roughly 9% from Q1, alongside a non-GAAP gross margin guidance of approximately 56%.

Intel and ARM Holdings both climbed in premarket trading on 6 May 2026 because the market interpreted AMD's data centre results as evidence of broad AI infrastructure spending expansion, not AMD-specific share gains at competitors' expense, signalling a sector-wide re-rating event.

AMD's next major catalyst is the 'Advancing AI 2026' showcase event scheduled for 22-23 July 2026 in San Francisco, where the company is expected to provide product and roadmap updates on its 6th Generation EPYC CPUs, MI450 Series accelerators, and Helios AI platforms.