Endeavour Group’s Dividend Reset: Income Stock or Reinvestment Bet?

5 hrs ago

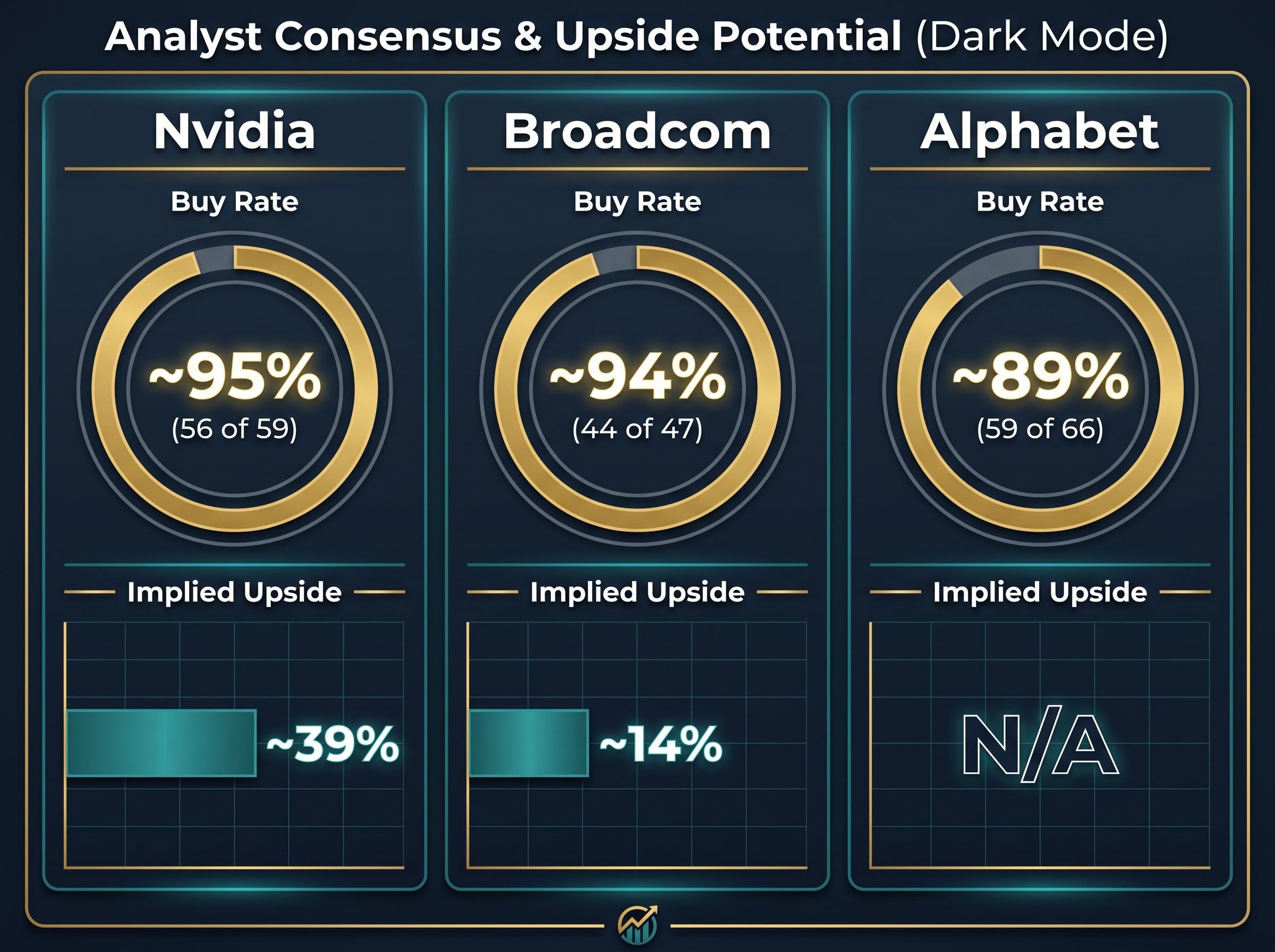

Fifty-nine of 66 analysts covering Alphabet rate it a buy or strong buy. Fifty-six of 59 say the same about Nvidia. Broadcom’s AI semiconductor revenue has surged dramatically in recent quarters. Wall Street is not hedging on AI infrastructure in 2026.

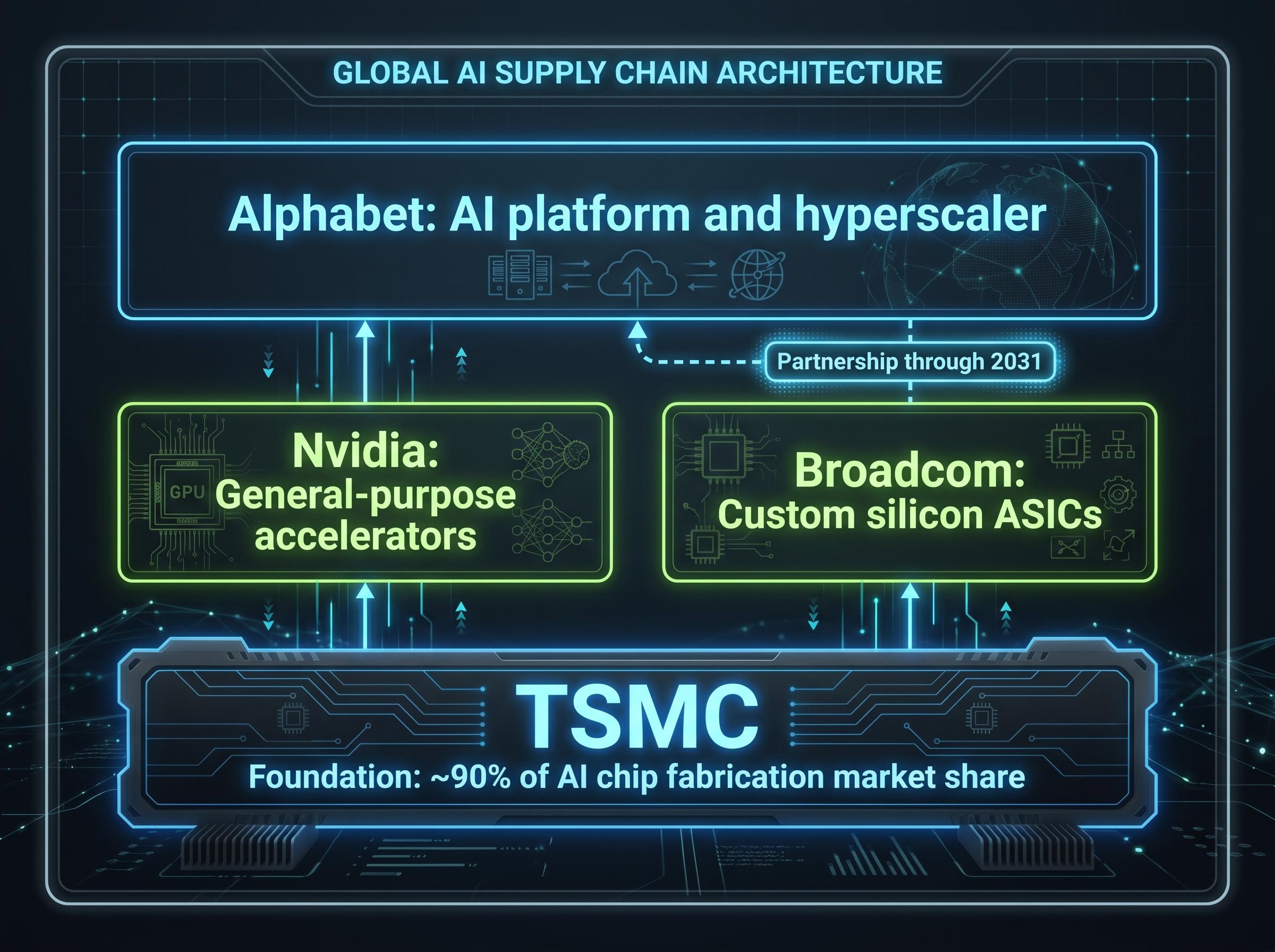

As of early May 2026, three names dominate the conversation when institutional investors evaluate AI stock exposure at scale: Nvidia, which controls the dominant share of AI accelerator hardware; Broadcom, which is building a parallel track through custom silicon; and Alphabet, which sits at the intersection of AI research, cloud infrastructure, and autonomous systems. Each occupies a structurally different position in the AI supply chain, which means the investment case for each looks meaningfully different.

This analysis breaks down where analyst consensus currently stands on each company, what growth catalysts are driving conviction, and how valuation compares to near-term upside potential. The goal is a structured framework for evaluating AI exposure across the hardware, custom silicon, and platform layers.

Nvidia, Broadcom, and Alphabet are not interchangeable AI bets. They occupy distinct and complementary roles in the infrastructure stack, and understanding those roles matters more than comparing their share prices side by side.

The AI supply chain splits into three functional layers:

Alphabet’s dual position is worth pausing on. It is simultaneously a customer of Broadcom’s custom silicon, with a partnership extending through 2031, and a builder of AI products that generate demand across the entire chip stack. That creates a unique dual exposure no other company in this analysis replicates.

Beneath all three sits a shared dependency: TSMC holds approximately 90% of AI chip fabrication market share, meaning the foundational manufacturing layer underpins every company discussed here.

The AI hardware capex cycle has effectively reshuffled the priority order of technology sector analysis, with hyperscaler infrastructure expenditure projected to expand from roughly 50% of operating cash flow in 2024 to 90% by 2027, a reallocation so large that hardware suppliers have become the primary beneficiaries of the AI buildout rather than its architects.

Nvidia holds approximately 80-92% of the AI accelerator market. That figure is the foundational reason behind the most lopsided analyst consensus in the S&P 500, not the stock’s past performance.

56 of 59 analysts polled by S&P Global rate Nvidia a buy or strong buy as of April 2026.

The Vera Rubin AI computing platform, launched in January 2026, represents Nvidia’s latest architectural upgrade and sustains the annual cadence that has kept competitors from closing the gap. Each generation resets the performance benchmark that hyperscalers use to justify their infrastructure spending.

The question is where the next leg of the return comes from. At a $4.8 trillion market capitalisation, Nvidia is the largest company in the world by market cap. The analyst consensus price target of $275.25 implies approximately 39% upside from the 4 May 2026 closing price, but that growth needs to be earned through continued data centre demand, not assumed.

| Metric | Value |

|---|---|

| Stock price (4 May 2026) | $198.48 |

| Analyst consensus target | $275.25 |

| Implied upside | ~39% |

| Market cap | ~$4.8 trillion |

| Gross margin | 71.07% |

| Buy/strong buy ratings | 56 of 59 |

| 52-week range | $110.82 – $216.82 |

A 71.07% gross margin and a 0.02% dividend yield tell a clear story: Nvidia is priced for reinvestment and growth, not income. The consensus is that data centre demand will sustain the trajectory, but with 56 of 59 analysts already on the buy side, any negative surprise carries outsized risk simply because so few voices are positioned for it.

Broadcom’s AI semiconductor revenue surged year-over-year in Q1 2026, and total revenue rose 29% over the same period. The velocity is real.

The AI revenue trajectory tells a growth story that is still in its early innings:

Whether that trajectory reflects a structural shift in chip demand or a complementary market that grows alongside Nvidia rather than displacing it is the more measured question behind the headline figures.

An Application-Specific Integrated Circuit (ASIC) is a chip designed for a single, specialised task rather than general-purpose computation. Where Nvidia’s GPUs handle a broad range of AI workloads, an ASIC is built to do one thing with maximum efficiency.

The hyperscaler logic is straightforward: when a company runs AI workloads at the scale of Google or Meta, a chip optimised precisely for its model architecture can deliver better performance-per-watt and lower cost per inference than a general-purpose GPU. This does not necessarily replace Nvidia’s market, but it creates a parallel demand stream that Broadcom is uniquely positioned to serve through its design expertise and long-term partnerships.

GPU and ASIC coexistence within the same hyperscaler data centre is a structural feature of the current buildout rather than a transitional state, meaning Nvidia’s general-purpose accelerators and Broadcom’s custom silicon are addressing different workload layers simultaneously rather than competing for the same procurement budget.

At 38 times forward earnings and a 14% average price target premium, 44 of 47 analysts rate Broadcom a buy or strong buy. The valuation is pricing in significant growth, but the entry-point dynamic differs from Nvidia: a lower multiple, a 0.60% dividend yield, and a revenue ramp that has not yet peaked.

Alphabet’s AI credentials predate the current investment cycle by more than a decade. Google DeepMind developed the Transformer architecture, the foundational model structure that underpins virtually all modern large language models. That research lineage is not a historical footnote; it is embedded in the company’s operating structure.

That claim has a precise citation: the original Transformer architecture paper, published in 2017 by researchers from Google Brain, introduced the attention mechanism that became the structural foundation for GPT, Gemini, and virtually every subsequent large language model at commercial scale.

Three active growth vectors are drawing analyst attention:

The most tangible signal of management conviction is the $180-$190 billion capital expenditure commitment for 2026, with further increases expected in 2027. Companies do not commit capital at this scale without high confidence in return on investment.

89% of analysts covering Alphabet rate it a buy or strong buy: 59 of 66 surveyed.

At a market capitalisation of approximately $4.6 trillion, a stock price of $383.25 (as of 4 May 2026), and a 52-week range of $147.84-$387.38, Alphabet is trading near the top of its range. The 60.43% gross margin and 0.22% dividend yield position it as a reinvestment-led growth story. Yet its valuation narrative receives less coverage than Nvidia’s, creating a potential information asymmetry for investors who have not fully mapped the breadth of Alphabet’s AI exposure.

Investors wanting to map the full scope of Alphabet’s AI exposure before drawing portfolio conclusions will find our full explainer on Alphabet’s Q1 2026 earnings and AI structure, which covers the $5.11 EPS result against a $2.64 consensus estimate, the 63% Google Cloud growth rate, and the Waymo ride-count milestone that analysts believe remains largely unpriced in the current share price.

All three companies carry analyst buy rates above 85%. That unanimity is itself a data point worth interrogating.

| Company | Buy/strong buy ratings | Total analysts | Buy rate (%) | Implied upside to target |

|---|---|---|---|---|

| Nvidia | 56 | 59 | ~95% | ~39% |

| Broadcom | 44 | 47 | ~94% | ~14% |

| Alphabet | 59 | 66 | ~89% | N/A |

Nvidia’s 39% implied upside is the most aggressive figure in the table. At a $4.8 trillion base, closing that gap requires sustained data centre order momentum and successful Vera Rubin ramp. Broadcom’s 14% premium reflects a more moderate consensus but still assumes the fiscal 2027 revenue target is achievable. Alphabet’s buy rate is the highest at 89%, though a granular consensus price target was not available in the data reviewed.

The broader macro context provides a tailwind: hyperscaler capex commitments, Federal Reserve easing, and sustained institutional momentum are all supporting the AI infrastructure buildout. Some selective value-seeking is emerging among investors, but the directional consensus has not shifted.

Sell-side analysts covering large-cap growth stocks tend to cluster around buy ratings. Coverage mandates, corporate access relationships, and career incentives all align with maintaining constructive relationships with management teams.

The meaningful data point is not the buy rate itself but the dispersion of price targets and the specific catalysts analysts cite as conditions for those targets being met. The catalysts that follow are where that specificity lives.

Four near-term events will either validate or challenge the current consensus:

TSMC holds approximately 90% of AI chip fabrication market share, a shared supply chain concentration risk across all three companies that individual analysis often underweights.

TSMC’s foundry market share concentration, estimated at approximately 72% of the global foundry business, means that supply disruptions, geopolitical restrictions, or capacity constraints at a single manufacturer would simultaneously affect every company examined in this analysis.

Intel’s data centre and AI segment revenue reached $13.6 billion in Q1 2026, up 22% year-over-year, signalling a recovering competitive presence that could further pressure margins across the sector over time.

The three investment cases form a coherent framework when viewed through the supply chain structure introduced at the start of this analysis. Nvidia offers broad AI hardware exposure with the highest implied upside and the highest execution expectations priced in. Broadcom provides custom silicon growth with a more moderate valuation and a longer-dated revenue ramp that has not yet peaked. Alphabet delivers platform-layer AI exposure backed by the deepest research lineage and the most diversified revenue base of the three.

Alphabet versus Nvidia portfolio allocation involves a different analytical framework than the chip-layer comparisons this article focuses on: Alphabet’s $109.9 billion in Q1 2026 revenue, 750 million Gemini monthly active users, and 500,000 weekly Waymo rides represent a diversification of AI monetisation vectors that a pure hardware position does not replicate.

What the research does not resolve is worth stating clearly. Broadcom’s detailed earnings-per-share and margin guidance for Q2 FY2026, Alphabet’s specific Google Cloud growth rate, and granular Waymo expansion metrics are all pending. These should be confirmed against primary sources before position decisions are made.

The hyperscaler capex cycle, represented most concretely by Alphabet’s $180-$190 billion commitment for 2026, signals that institutional conviction in AI infrastructure has not peaked. Individual stock valuations require careful scrutiny, but the structural investment thesis remains intact.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Nvidia, Broadcom, and Alphabet are the three names commanding the strongest analyst conviction in 2026, with buy or strong buy ratings from 89% to 95% of covering analysts across the three companies.

Nvidia GPUs are general-purpose accelerators that handle a broad range of AI workloads across industries, while Broadcom ASICs are custom chips designed for a single hyperscaler's specific model architecture, offering better performance-per-watt for large-scale inference workloads.

As of 4 May 2026, the analyst consensus price target for Nvidia is $275.25, implying approximately 39% upside from its closing price of $198.48, based on ratings from 56 of 59 analysts who rate it a buy or strong buy.

Alphabet sits at the intersection of AI research, cloud infrastructure, and autonomous systems, with Google DeepMind having developed the original Transformer architecture, Google Cloud cited as the fastest-growing major cloud provider, and Waymo operating as the leading commercial autonomous ride-hailing service.

TSMC holds approximately 90% of AI chip fabrication market share, making it the foundational manufacturing layer for Nvidia, Broadcom, and Alphabet's custom silicon, meaning any supply disruption at TSMC would simultaneously affect all three companies.