How to Build a Global ETF Portfolio on the ASX With 3 Funds

6 hrs ago

Australia operates one of the world’s most dividend-friendly tax systems. Franking credits, semi-annual reporting cycles, and a market heavily concentrated in banks and miners create an environment where dividend income can compound meaningfully over time. Yet the same features that make the ASX attractive for income investors also produce some of the most spectacular dividend traps in developed markets. A yield that looks generous on a stock screener can, on closer inspection, reflect a falling share price rather than a reliable income stream.

The difference between a sustainable dividend portfolio and a costly mistake sits in the mechanics. Understanding how to read yield in context, how franking credits transform after-tax returns, what a payout ratio reveals about durability, and when the dividend calendar works against an investor is not optional knowledge. This guide walks through every decision layer involved in evaluating an ASX dividend stock: how to read the numbers, when to buy, how to avoid the traps, and how reinvestment compounds the outcome.

Dividend yield is a simple calculation: the annual dividend per share divided by the current share price, multiplied by 100. If a stock pays $1.00 in annual dividends and trades at $20.00, the yield is 5%. It is the first number most income investors check, and that instinct is reasonable. Yield offers a quick comparison between stocks, sectors, and asset classes.

The problem is in the denominator. Because yield uses the share price as its base, it moves in the opposite direction to the stock. A falling share price pushes yield up automatically, even if the dividend itself has not changed. This means a rising yield is not always a reward signal. It is sometimes a distress signal: the market is pricing in a likely dividend cut, and the yield looks attractive only because the share price has already collapsed.

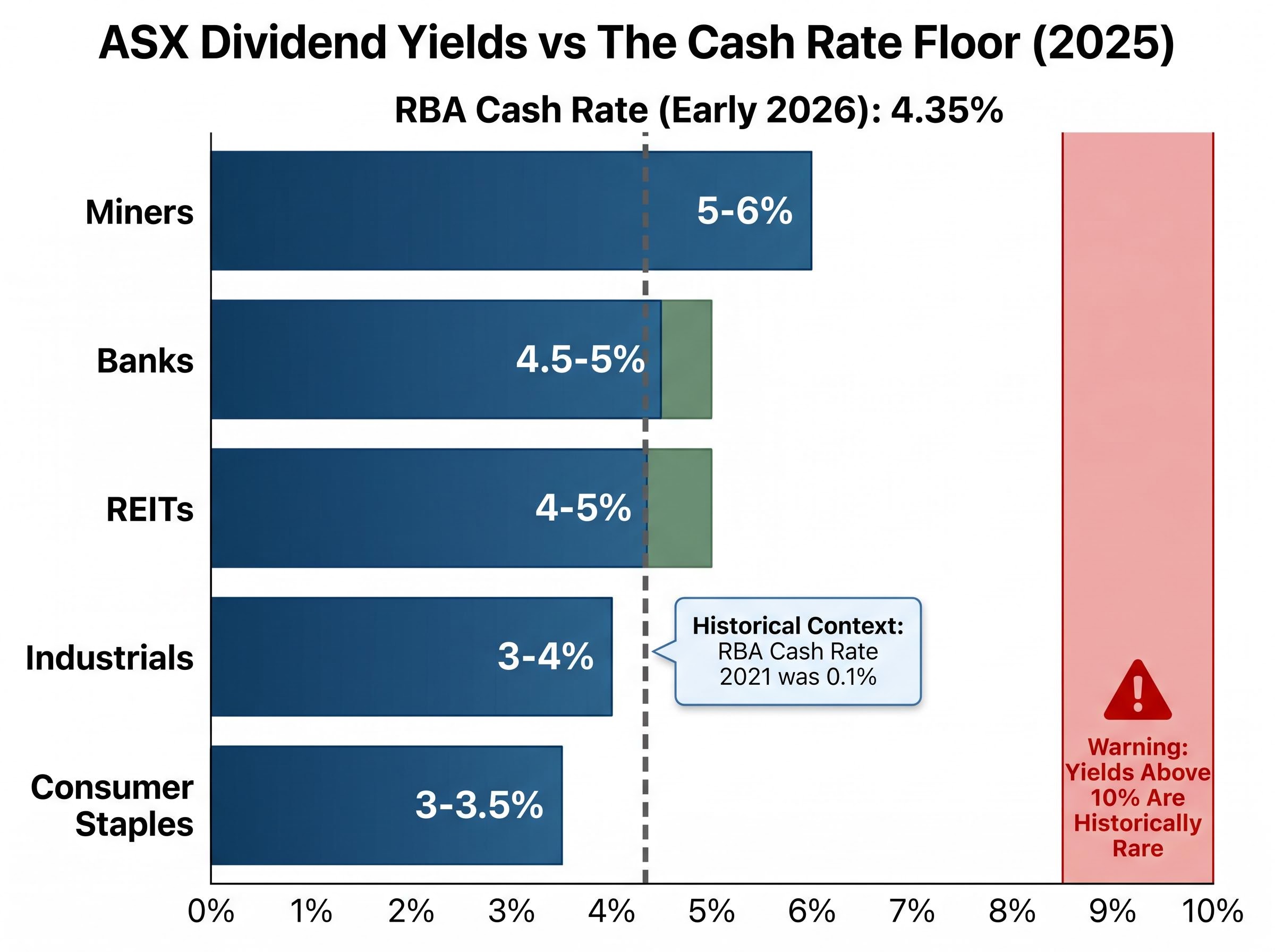

A yield figure only becomes meaningful when measured against two reference points: the sector average and the risk-free rate. The RBA cash rate stood at 4.35% as of early 2026, establishing the floor return available to investors without taking on equity risk.

| Sector / Benchmark | Approximate Yield Range (2025) |

|---|---|

| Banks | 4.5-5% |

| REITs | 4-5% |

| Miners | 5-6% |

| Industrials | 3-4% |

| Consumer Staples | 3-3.5% |

| RBA Cash Rate | 4.35% |

A bank stock yielding 4.6% looks very different when the cash rate is 4.35% than it did in 2021, when the cash rate sat at 0.1%. At current levels, that yield barely compensates for equity risk. A yield above 10% on the ASX is historically rare for sustainable businesses and should trigger scrutiny rather than enthusiasm.

A high dividend yield can be a warning, not a reward. When yield rises because the share price is falling, the market may already be pricing in a cut.

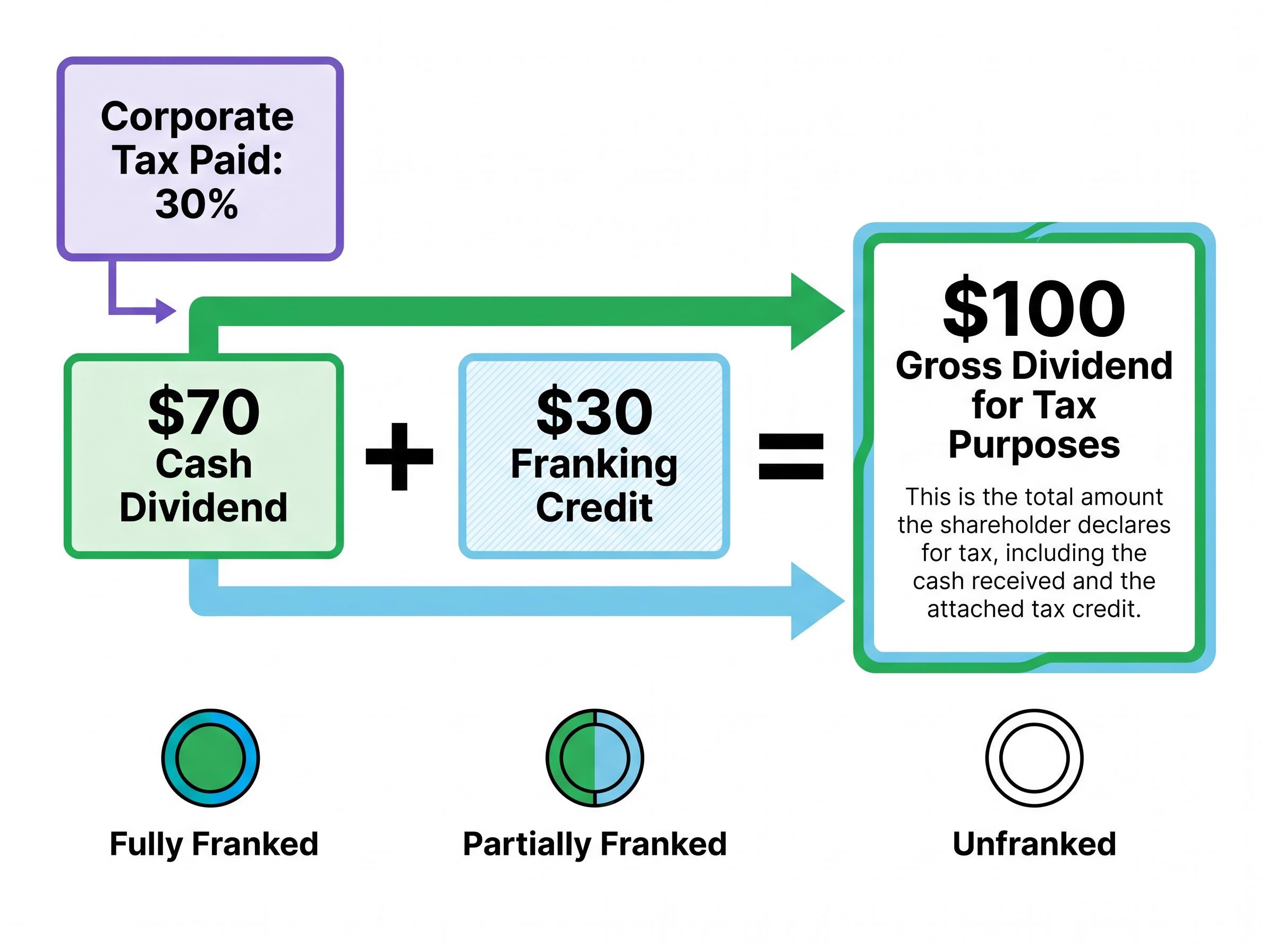

Australia’s dividend imputation system is the single feature that makes ASX dividend investing mechanically distinct from dividend strategies in other markets. When an Australian company pays corporate tax at the 30% rate (or 25% for eligible small businesses), it can attach a franking credit to dividends distributed from those after-tax profits. Shareholders then include both the cash dividend and the attached credit in their assessable income, offsetting the credit against their own tax liability.

The practical result is that a fully franked dividend is worth more than its headline cash amount. Consider a company distributing a $70 cash dividend from profits that were taxed at 30%. The attached franking credit is $30, giving a gross dividend of $100 for tax purposes. An investor whose marginal tax rate is below 30% receives a refund of the excess credit from the ATO. For a superannuation fund taxed at 15%, or a retiree with no taxable income, this refund materially increases the after-tax return.

Not all ASX dividends carry the same franking benefit. Three levels exist:

ANZ’s franking uplift from 70% to 75% on its May 2026 interim dividend illustrates precisely how partial franking changes the grossed-up value calculation for eligible Australian shareholders, lifting the effective per-share value from the headline 83 cents to approximately 109.68 cents.

The after-tax yield of a fully franked dividend is materially higher than the headline cash yield for investors in lower tax brackets. Comparing ASX dividend yields to term deposits or international stocks without adjusting for franking credits produces a systematically misleading comparison.

The payout ratio measures the proportion of a company’s net earnings distributed as dividends, expressed as a percentage. If a company earns $1.00 per share and pays $0.60, the payout ratio is 60%. On the ASX, a sustainable range generally falls between 40% and 70%. A ratio at the lower end leaves comfortable headroom for the dividend to survive an earnings downturn. A ratio above 70% warrants closer examination, particularly if earnings are cyclical.

Commonwealth Bank (ASX: CBA) illustrates the higher end of sustainable. Its yield sits at approximately 3% with a payout ratio of roughly 80%, well-supported by consistent earnings and a strong capital position but leaving limited room for error. ASX Ltd provides a different signal: it reduced its payout ratio to 75-85% of underlying net profit after tax following ASIC’s imposition of a $150 million additional capital charge in December 2025, a direct consequence of the CHESS replacement programme failures.

ASX Ltd’s regulatory capital obligations following the ASIC Final Report published in April 2026 extend beyond a single payout ratio adjustment: the company must accumulate an additional $150 million in capital relative to its December 2025 position, with further capital returns contingent on achieving milestones under the reset Accelerate Program agreed with both ASIC and the Reserve Bank of Australia.

At the other extreme, BHP, Rio Tinto, and Fortescue all cut dividends during 2024-2025 as commodity prices fell and capital expenditure requirements climbed. A payout ratio above 100%, where a company distributes more than it earns, is the clearest warning sign. It is mathematically unsustainable beyond the short term.

Earnings-based payout ratios can be flattering. Accounting earnings include non-cash items such as depreciation adjustments and accrued revenues, meaning a company can report healthy profits while generating weak actual cash. The free cash flow payout ratio, calculated as dividends paid divided by free cash flow, offers a more reliable view for capital-intensive businesses.

APA Group (ASX: APA) demonstrates this distinction. Its yield of approximately 6.89% appears elevated, but the company’s cash flows are underpinned by long-term contracted infrastructure revenue rather than cyclical earnings. A cash flow analysis justifies the payout where an earnings-only assessment might raise questions.

| Payout Ratio Range | Signal | Example Context |

|---|---|---|

| 40-60% | Comfortable headroom for earnings variation | Industrials, consumer staples |

| 60-80% | Sustainable if earnings are stable; limited buffer | Major banks (CBA ~80%) |

| 80-100% | Elevated risk; any earnings dip threatens the dividend | ASX Ltd post-regulatory charge |

| Above 100% | Company paying more than it earns; unsustainable | Often precedes a cut within 1-2 cycles |

Qualifying for an ASX dividend requires precision around four calendar dates, each with a distinct function for investors. Missing the sequence by a single day can mean missing the payment entirely.

The critical implication of T+2 settlement is that buying shares two trading days before the ex-dividend date is the last opportunity to qualify. An investor who buys one day before the ex-date will not have shares settled on the register in time.

The calendar sequence determines whether an investor receives the cash dividend. A separate compliance layer determines whether they can claim the franking credit.

To claim franking credits, shares must be held “at risk” for at least 45 days around the ex-dividend date, excluding the purchase and sale dates. The “at risk” requirement means shares must be genuinely exposed to market price movement during the holding period, not hedged. Retail investors with total franking credit claims under $5,000 annually are exempt, but this threshold is easily exceeded with a meaningful portfolio.

The 45-day rule was designed specifically to prevent dividend stripping, the practice of buying shares just before the ex-date to capture the dividend and franking credit, then selling immediately after. An investor who receives the cash dividend but fails the 45-day test loses the franking credit, substantially reducing the after-tax return on the position.

The ATO rules on claiming a franking credit refund specify the exact conditions under which shareholders can offset or receive a cash refund of excess credits, including the 45-day holding period requirement that determines whether a position qualifies as genuinely at risk during the relevant period.

Where the preceding sections focused on evaluating dividends defensively, dividend reinvestment plans (DRPs) represent the constructive side of the equation. A DRP allows shareholders to receive additional shares in the company instead of a cash payment, typically without brokerage costs and sometimes at a small discount to market price.

The compounding effect is straightforward but powerful: each reinvested dividend increases the number of shares held, which in turn increases the size of the next dividend payment, which buys more shares again. In a fully franked environment, the compounding is amplified because the reinvested amount effectively reflects the after-tax benefit of the franking credit, not just the headline cash dividend.

CBA’s franking-adjusted total return over the two years to April 2026 demonstrates the compounding arithmetic in concrete terms: a 52.5% price gain expanded to approximately 72% once fully franked dividends were reinvested, with pension-phase superannuation investors receiving the full 30% credit as a refundable ATO offset.

Many large ASX companies offer DRPs, including ASX Ltd itself. Recent corporate developments illustrate the breadth of DRP-eligible stocks: Qantas reinstated its dividend following the COVID-era suspension, while A2 Milk paid its first-ever dividend, reflecting a transition from pure growth reinvestment to capital return. Both mature income payers and transitioning companies can offer DRP participation.

DRP continuity should not be assumed. Between April and December 2020, dividends on the ASX fell 38%, driven primarily by APRA-enforced bank reductions. Companies can suspend or alter DRP terms at any time.

Reinvesting dividends grows both the share count and future dividend income simultaneously. Over a multi-year horizon, this compounding effect can materially outperform a strategy of taking cash and manually redeploying it, particularly when brokerage costs are removed from the equation.

A dividend trap is a specific situation: a high yield that reflects a falling share price driven by market anticipation of a cut, not genuine income value. The investor buys for yield, then receives either a reduced dividend or none at all, while the share price continues to fall. The result is income loss and capital loss simultaneously.

Dividend traps are disproportionately destructive. A single trap can erase multiple years of dividend income from an otherwise well-constructed portfolio. Recognising the warning signs before committing capital is the most valuable defensive skill a dividend investor can develop.

The warning signs follow a consistent pattern. A yield above 10% on the ASX is historically rare for sustainable businesses and often indicates the market is pricing in an imminent cut. A payout ratio above 100% is mathematically unsustainable. Declining earnings over three or more years compress headroom even when the payout ratio remains technically below 100%. Weak or negative free cash flow suggests that earnings-based ratios are masking a deteriorating business. Rising debt levels may indicate a company is borrowing to maintain distributions, funding dividends from capital rather than income. The mining sector provides recent examples: BHP, Rio Tinto, and Fortescue all cut dividends during 2024-2025 as the commodity cycle turned.

ASIC’s MoneySmart platform reinforces a principle that applies across all these scenarios: past dividend payments are not a guarantee of future payments.

| Metric | Healthy Signal | Warning Signal |

|---|---|---|

| Payout ratio (earnings) | 40-70% | Above 100% |

| Yield vs. sector average | In line with peers | Above 10% or extreme outlier |

| Earnings trend | Stable or growing | Declining over 3+ years |

| Free cash flow | Covers dividends comfortably | Weak or negative |

| Debt levels | Conservative gearing | Rising debt funding distributions |

Before committing capital to any ASX dividend stock, apply these five steps:

The mechanics covered in this guide, yield interpretation, franking credit valuation, payout ratio analysis, calendar compliance, DRP compounding, and trap identification, form a layered evaluation framework. Each component addresses a distinct risk or opportunity. Applied together, they provide a structured basis for dividend stock selection that goes beyond screening for the highest yield.

The ASX’s concentration in banks and miners creates a specific risk for dividend investors. These sectors often move in correlated cycles: bank dividends came under simultaneous pressure during the 38% dividend fall between April and December 2020, while mining dividends fell collectively during the 2024-2025 commodity downturn. Spreading income sources across banks, REITs, infrastructure, and consumer staples provides more stable aggregate income than concentration in any single high-yield sector.

Rural Funds Group (ASX: RFF) illustrates how REIT distributions are structured differently from company dividends, with sustainability dependent on asset quality and lease terms rather than retained earnings. Understanding these structural differences allows investors to build genuine diversification into their income streams rather than holding multiple positions with the same underlying risk driver.

The framework for evaluating every ASX dividend stock under consideration includes five criteria:

A dividend income strategy that survives market cycles requires more than a list of high-yielding stocks. As ASIC’s regulatory guidance emphasises, dividend yield is not a substitute for analysis of the underlying business.

For investors who want to stress-test this framework against the alternative approach, our full explainer on dividend investing versus total return examines a decade of backtested data and shows where a yield-focused strategy underperforms a total market portfolio, including the tax-timing advantages that total return investors hold in taxable accounts.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Dividend investing in Australia involves buying shares in ASX-listed companies that distribute a portion of their profits to shareholders, often with franking credits attached that represent tax already paid at the corporate rate, which can reduce or eliminate the investor's own tax liability on that income.

When an Australian company pays corporate tax at 30%, it can attach franking credits to dividends paid from those after-tax profits; shareholders include both the cash dividend and the credit in their assessable income, and investors in lower tax brackets, such as retirees or superannuation funds, can receive the excess credit as a cash refund from the ATO, materially boosting after-tax returns.

On the ASX, a payout ratio between 40% and 70% is generally considered sustainable, leaving sufficient headroom to maintain dividends during an earnings downturn, while a ratio above 100% is mathematically unsustainable and often precedes a dividend cut within one to two reporting cycles.

To claim franking credits, Australian shareholders must hold their shares at risk, meaning genuinely exposed to market price movement without hedging, for at least 45 days around the ex-dividend date, excluding the purchase and sale dates; failing this test means the investor receives the cash dividend but forfeits the franking credit, significantly reducing after-tax returns.

Key warning signs of a dividend trap include a yield above 10%, a payout ratio above 100%, declining earnings over three or more consecutive years, weak or negative free cash flow, and rising debt levels that suggest distributions are being funded by borrowing rather than operating income.