RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

5 hrs ago

Australian inflation surged from 3.7% to 4.6% in a single month at the start of 2026, and Treasurer Jim Chalmers pointed directly at a war thousands of kilometres away as the cause. The Middle East conflict has become more than a foreign policy problem for Australia; it is now an active driver of domestic prices, borrowing costs, and household budgets.

Understanding the connection between a geopolitical shock in the Persian Gulf and the cost of groceries in Sydney is no longer optional for anyone with a mortgage, a business, or a portfolio. The transmission chain runs from oil fields to petrol stations, through supply chains and central bank boardrooms, and ultimately into monthly repayment schedules and supermarket receipts.

This article traces that full chain, explaining the mechanisms by which the Middle East conflict translates into higher Australian inflation, why the Reserve Bank of Australia (RBA) has responded with three consecutive rate hikes, and what the trajectory ahead depends on.

A conflict in the Middle East might seem remote from the price on an Australian bowser. It is not. Australia is a price-taker in global oil markets, which means domestic pump prices move in close lockstep with Brent crude regardless of where the barrels originate.

As of 5 May 2026, Brent crude is trading at approximately US$113-116 per barrel, well above pre-conflict levels. Australian fuel prices have spiked more sharply than comparable peer economies, signalling unusually strong passthrough from global oil markets into domestic consumer prices.

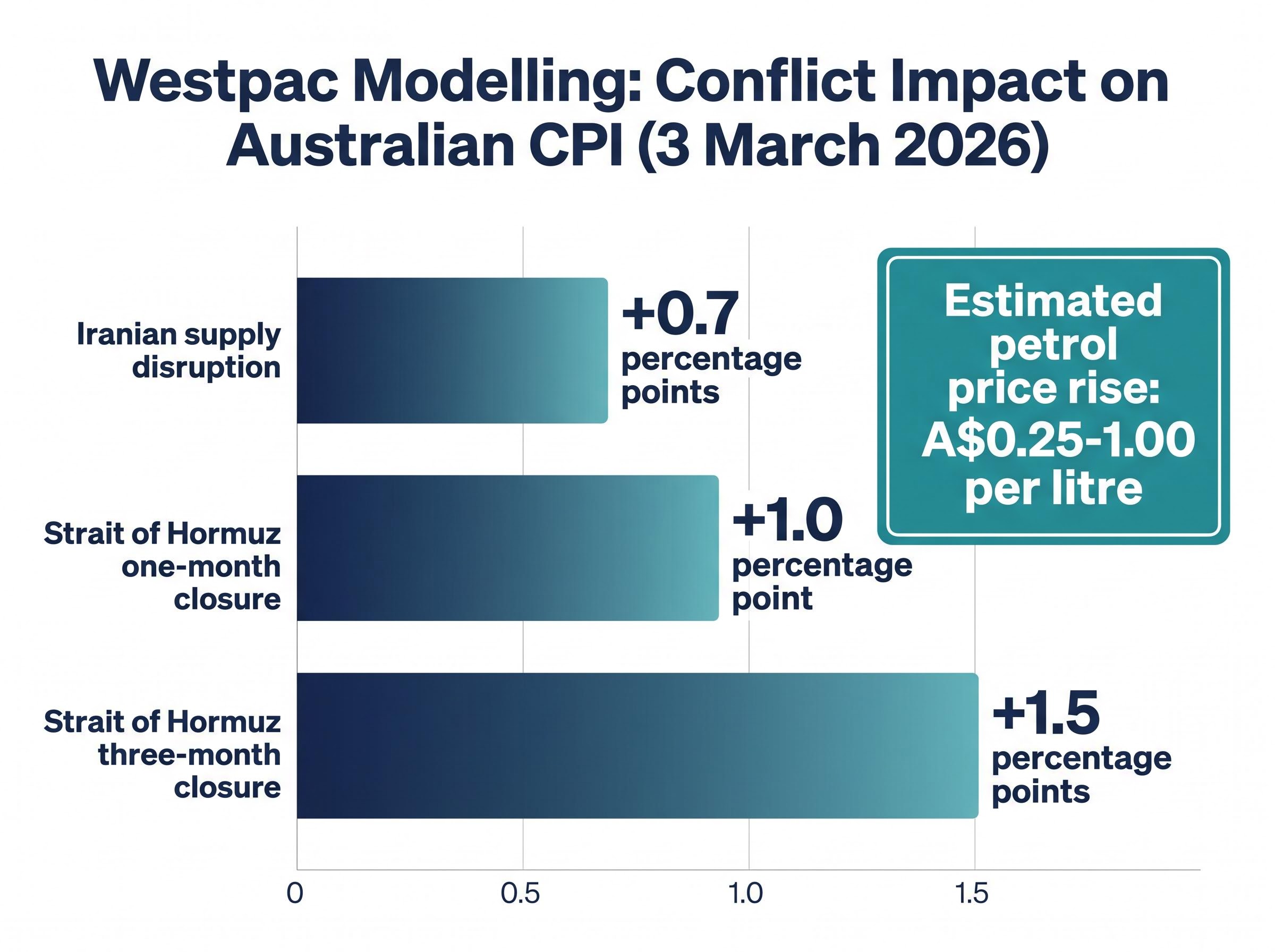

Westpac modelling (published 3 March 2026) estimated petrol prices could rise by A$0.25-1.00 per litre depending on conflict severity, across three escalation scenarios:

A three-month closure of the Strait of Hormuz could add approximately 1.5 percentage points to Australian CPI, according to Westpac scenario modelling.

Fuel is both a direct household cost and the first domino in a longer inflationary chain.

The petrol price spike is the most visible effect. It is not the most consequential.

Higher oil prices translate directly into higher costs for every business that moves goods by road, rail, sea, or air. In a country as geographically spread as Australia, freight costs touch nearly every physical product on a shelf.

Qantas and Virgin Australia have already raised ticket prices in direct response to higher fuel costs. Road freight operators are passing cost increases through to retailers and wholesalers.

The less visible channel runs through energy-intensive inputs. Higher energy costs raise the price of fertilisers, which flows through to farm costs and ultimately to food prices at retail. This is not a theoretical risk; agricultural supply chain costs are already climbing.

State Street, in analysis published on 13 March 2026, warned that second-order effects from sustained fuel spikes may ultimately prove more damaging to inflation than the initial petrol price shock, particularly given Australia’s existing capacity constraints.

Electricity and construction costs are adding a structural layer to the inflation shock that persists independent of where oil prices go next: electricity rose 25.4% annually in March 2026 after Energy Bill Relief Fund payments lapsed, while new dwelling construction costs accelerated sharply as oil-derived building materials and diesel-powered supply chains absorbed the global crude price spike.

The four main transmission channels are:

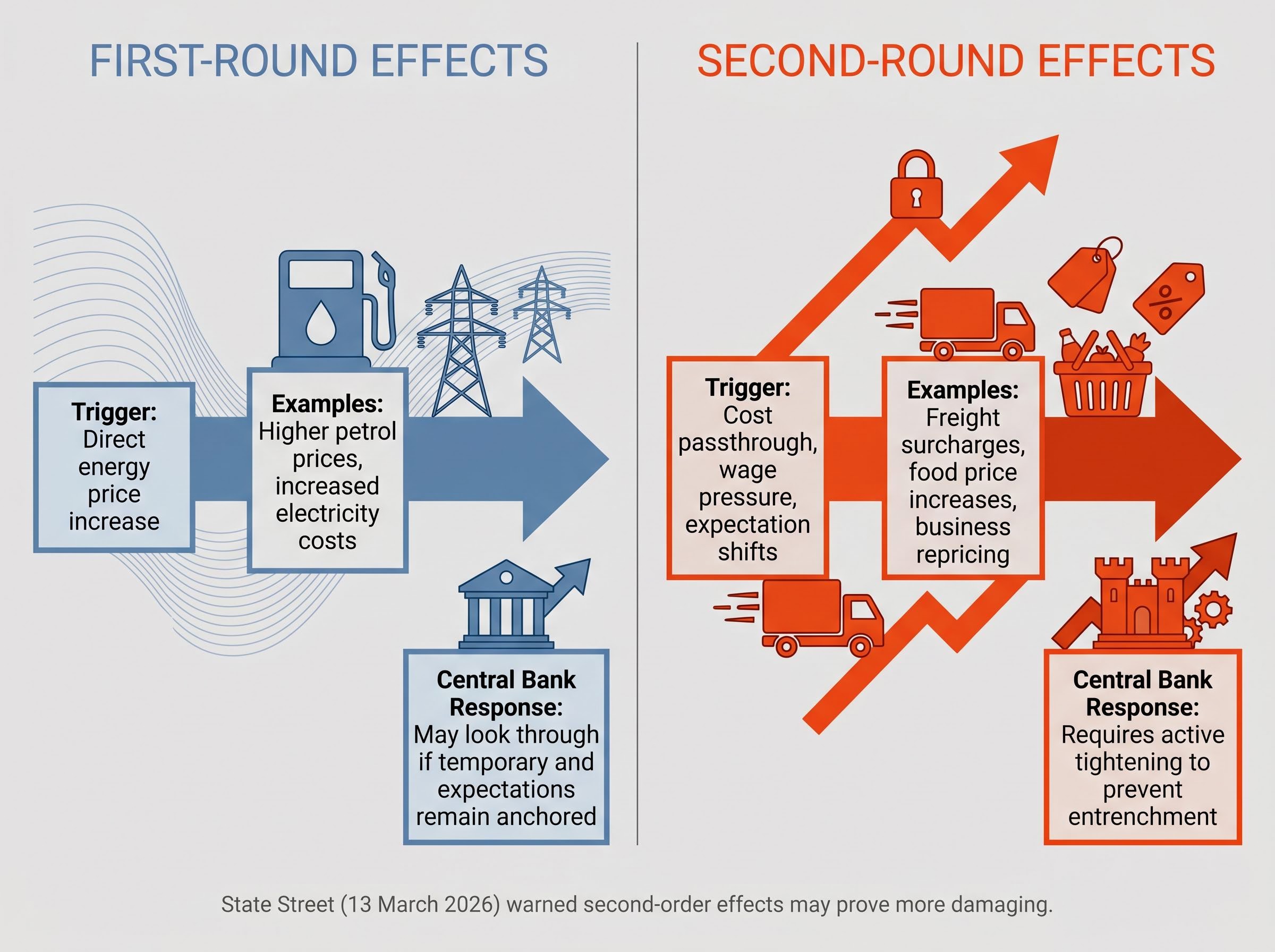

The distinction between first-round and second-round inflation effects is the framework that explains not just what is happening, but why the RBA is reacting the way it is.

First-round effects are the direct price level impacts from an energy shock: petrol costs more, so the consumer price index rises mechanically. These effects are visible, measurable, and, in principle, temporary if the shock fades.

Second-round effects are what central banks fear most. They occur when higher energy costs feed into broader pricing behaviour: freight operators raise charges, retailers mark up goods, workers seek higher wages to offset cost-of-living increases, and businesses begin setting prices in anticipation of further inflation. Once this dynamic takes hold, it becomes self-reinforcing and far harder to reverse.

The RBA confirmed in early 2026 that short-term inflation expectations had moved higher. Many businesses facing rising input costs were considering passing those costs on to consumers. Westpac noted that central banks may initially look through first-round energy effects, but they cannot ignore persistent high prices that begin embedding in expectations.

Trimmed mean inflation, the RBA’s preferred underlying measure, held at 3.3% annually in March 2026 even as the headline rate surged to 4.6%, a divergence that reflects how stripping out volatile fuel items produces a fundamentally different picture of where persistent domestic price pressure actually sits.

| Effect Type | Trigger | Examples in Current Context | Central Bank Response |

|---|---|---|---|

| First-round | Direct energy price increase | Higher petrol prices, increased electricity costs | May look through if temporary and expectations remain anchored |

| Second-round | Cost passthrough, wage pressure, expectation shifts | Freight surcharges, food price increases, business repricing | Requires active tightening to prevent entrenchment |

The RBA has warned that elevated inflation expectations risk becoming entrenched if sustained energy cost pressures continue to feed into broader pricing behaviour.

The duration of the conflict matters far more than its immediate severity. A short-lived spike that fades before second-round effects take hold is manageable. A prolonged shock that shifts expectations is a different problem entirely.

The theoretical transmission chain is not hypothetical. It is already in the data.

The Australian Bureau of Statistics (ABS) reported that CPI rose 4.6% in the 12 months to March 2026, up from 3.7% in the 12 months to February 2026. A jump of nearly one full percentage point in a single month is unusual, and it arrived precisely as the conflict escalated.

Treasurer Jim Chalmers attributed the spike directly to global pressures, including the Middle East war.

“Australians are paying a hefty price for the conflict,” Treasurer Chalmers stated, noting oil shock pressures were expected to intensify and broaden inflation impacts beyond their initial effects.

The RBA responded with three consecutive rate hikes: lifting the cash rate to 4.10% on 17 March 2026, then raising it again to 4.10% on 5 May 2026. Inflation now sits nearly two full percentage points above the top of the RBA’s 2-3% target band. The RBA’s updated forecasts show underlying inflation peaking higher than the February 2026 baseline, even under the benign scenario of eventual conflict resolution.

| Indicator | Figure | Source / Date |

|---|---|---|

| Australian CPI (12 months to March 2026) | 4.6% | ABS, April 2026 |

| Australian CPI (12 months to February 2026) | 3.7% | ABS |

| RBA cash rate | 4.10% | RBA, March 17, 2026 |

| Brent crude | ~US$113-116/barrel | As of 5 May 2026 |

| RBA inflation target band | 2-3% | RBA |

The next ABS CPI release, covering April 2026 data, is scheduled for 27 May 2026. That release will provide the most current read on whether inflationary pressures have continued to build.

An external shock that raises inflation while simultaneously threatening to suppress growth creates a genuine policy tension. The RBA must weigh its price stability mandate against the risk of cooling an economy already absorbing a cost-of-living shock.

The RBA’s decision to move proactively, three consecutive hikes reaching 4.10% by 17 March 2026, reflects a deliberate choice to prevent second-round inflation from becoming entrenched, even at the risk of slowing economic activity.

The May 2026 board vote was not unanimous. Eight of nine board members voted in favour of the hike; one preferred to hold. That split reflects the genuine difficulty of the trade-off.

The RBA cash rate decision published on 5 May 2026 confirmed the board’s assessment that inflation risks from the Middle East conflict had broadened beyond initial energy price effects, with the 2-3% target band now expected to remain out of reach until the conflict’s impact on expectations is contained.

The RBA’s stated policy considerations, in order of emphasis, are:

Two divergent paths lie ahead.

Under the benign scenario, the conflict resolves or de-escalates, fuel prices fall, and underlying inflation peaks before declining as demand moderates and capacity pressures ease in response to tighter policy. Even in this scenario, the RBA has signalled that the inflation peak will be higher than previously forecast.

Under the extended conflict scenario, further global energy price increases compel additional rate hikes. Growth risk amplifies. The conditions for stagflation dynamics, where prices rise while economic activity stalls, become more plausible. Westpac has noted that sustained Brent crude at very high levels could compel tighter monetary policy globally, with the Reserve Bank of New Zealand cited as a peer that may also hike in such a scenario.

The RBA has explicitly warned that a prolonged conflict risks entrenching higher inflation and requiring an extended period of elevated rates.

The confluence of higher prices and higher rates is not a prospective risk. It is being felt now.

Household impacts:

Business impacts:

Real household income is being squeezed from three directions simultaneously. Money market rates and Australian bond yields have both risen over the course of 2026, and the Australian dollar has appreciated. Credit remains accessible despite tighter conditions, according to the RBA’s assessment, but borrowing costs have increased materially.

The RBA has warned of a significant income shock if the conflict escalates further and rates need to rise again, compounding the pressure on Australian households already absorbing higher prices across multiple categories.

The combination of rising prices and rising rates is genuinely unusual. In a standard tightening cycle, inflation is domestically generated and rate hikes cool demand to bring it down. In this environment, the inflation is imported via energy prices, yet the RBA must still tighten because the second-round effects are becoming domestic.

Stagflation risk in Australia has moved from a theoretical scenario to an increasingly discussed baseline, with consumer confidence falling to its weakest level since 1973, diesel prices having nearly tripled from January 2026 levels, and corporate insolvencies setting an all-time record in 2025 as businesses absorb simultaneous cost and demand shocks.

The RBA’s baseline assumes eventual conflict resolution and a subsequent fall in fuel prices. Even under that assumption, the inflation peak will be higher than pre-conflict forecasts anticipated. The damage, in other words, is already done; the question is how much further it extends.

Three indicators will determine how the scenario evolves:

The analytical frame for interpreting developments is straightforward: if second-round effects, including inflation expectations, broad goods repricing, and wage pressures, continue to build, the pressure on the RBA to tighten further intensifies regardless of what happens to the oil price itself. The oil shock may pass; the inflationary momentum it generated may not.

The Middle East conflict is not background noise for Australian households and investors. It is an active structural input into domestic inflation, interest rates, and financial planning.

The transmission chain is direct: conflict drives energy prices higher, energy costs ripple through supply chains into a broad range of goods and services, CPI rises well above the RBA’s target band, the central bank responds with rate hikes, and households and businesses absorb the combined shock of higher prices and higher borrowing costs simultaneously.

Readers who understand this chain are better positioned to interpret future RBA decisions, CPI releases, and financial market movements in terms of their own exposure. The 27 May CPI release and the RBA’s subsequent guidance will be the next critical data points in a story that is still unfolding.

Investors wanting to translate this inflation picture into specific portfolio decisions will find our comprehensive walkthrough of ASX inflation positioning, which covers how ASX-listed cash ETFs, quality equity factors, and dollar cost averaging approaches have historically performed during tightening cycles, and why reactive selling on CPI headlines tends to lock in losses ahead of the eventual rate peak.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections and scenario analysis referenced in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.

Australian inflation rose to 4.6% in the 12 months to March 2026, up from 3.7% the month prior, driven primarily by the Middle East conflict pushing global oil prices above US$113 per barrel, which is flowing through petrol prices, freight costs, food prices, and electricity bills.

Australia is a price-taker in global oil markets, so Brent crude increases translate directly into higher petrol prices; those higher energy costs then ripple through freight, fertilisers, and manufacturing inputs, ultimately raising the price of groceries and everyday goods on Australian shelves.

The Reserve Bank of Australia raised the cash rate to 4.10% because sustained energy price increases risk triggering second-round inflation effects, where businesses pass on higher costs, wages rise, and inflation expectations become entrenched, requiring active monetary tightening to prevent that cycle from taking hold.

Second-round inflation effects occur when an initial energy price shock feeds into broader pricing behaviour, including freight surcharges, food price increases, and wage demands, creating a self-reinforcing cycle that central banks must counter with rate hikes, directly increasing mortgage repayments for variable-rate borrowers.

The most critical upcoming data point is the ABS CPI release on 27 May 2026, covering April 2026 data, which will reveal whether the sharp March spike was a one-month event or the start of an accelerating trend; Brent crude price direction and RBA forward guidance language are the other two key indicators to monitor.