May PCE Inflation Hits Target, Keeping Fed on Hold

1 hr ago

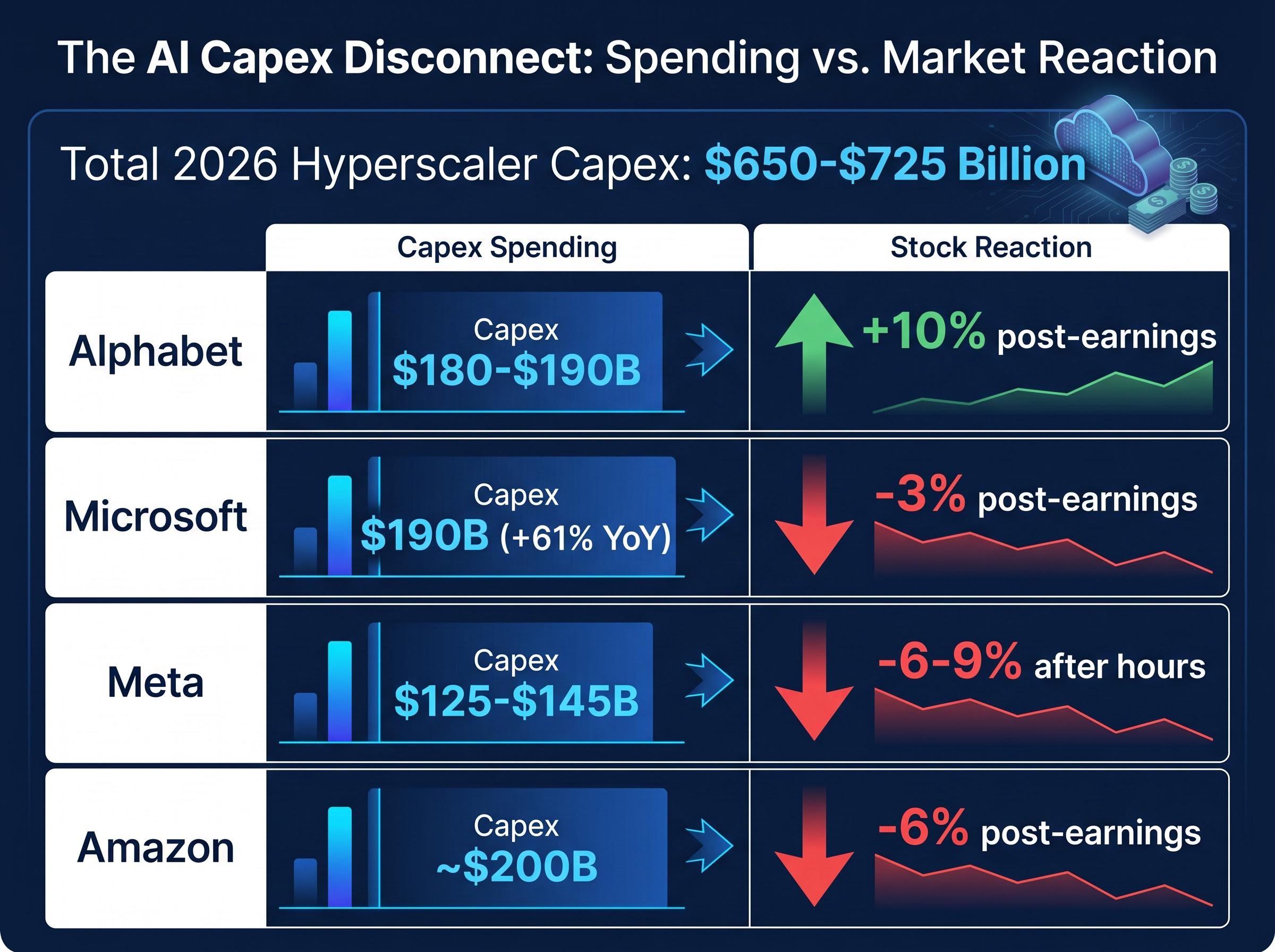

Five of America’s most valuable technology companies reported Q1 2026 earnings within 48 hours of each other in late April. The results were, almost universally, strong. Revenue beats, earnings beats, cloud acceleration, and AI monetisation milestones landed across the board. Several of the stocks fell anyway. The disconnect between operational performance and share price reaction across Alphabet, Amazon, Apple, Meta, and Microsoft tells a pointed story about where investor attention has shifted in the US tech earnings cycle: away from quarterly profit and toward the trajectory of artificial intelligence infrastructure spending, now totalling an estimated $650-$725 billion across the four major hyperscalers in 2026 alone. What follows is a company-by-company scorecard, the analytical logic behind the market’s split verdicts, and what the collective results reveal about whether AI investment is generating returns at scale.

All five companies beat consensus estimates on revenue or earnings per share. Only two saw their stocks rise in the immediate aftermath.

| Company | Key Revenue Metric | YoY Growth | EPS Result | Stock Reaction |

|---|---|---|---|---|

| Alphabet | $109.9B (total revenue) | +22% | N/A (net income $62.6B) | +10% post-earnings; +3.30% as of 1 May |

| Apple | $111.2B (total revenue) | +17% | $2.01 (+22% YoY) | +3.6% after hours; -0.46% as of 1 May |

| Meta | $56.31B (ad revenue) | +33% | $10.44 | -6-9% after hours; +13.25% as of 1 May |

| Microsoft | $82.89B (total revenue) | N/A | $4.27 | -3% post-earnings; +5.32% as of 1 May |

| Amazon | $37.59B (AWS revenue) | +28% | N/A | -6% post-earnings; -7.05% as of 1 May |

Meta and Microsoft had partially recovered from their post-earnings drops by 1 May 2026 (price return data sourced from Morningstar charting, excluding dividends). Apple was essentially flat. Amazon remained the worst performer.

Combined 2026 capex commitments across the four major hyperscalers reached approximately $650-$725 billion, the figure now dominating investor calculus more than any single quarterly beat.

The pattern is clear: the market is pricing capex trajectory, not current revenue.

Alphabet delivered the earnings cycle’s cleanest AI revenue story. Google Cloud crossed $20 billion in quarterly revenue for the first time, growing 63% year over year, a milestone that directly addressed prior concerns about the company falling behind in AI competition.

The capex raise was received as a confidence signal rather than a liability. Revenue acceleration justified the spend, and the stock rose approximately 10% post-earnings.

Apple told a different kind of positive story. Revenue of $111.2 billion beat the $109.6 billion consensus estimate, and earnings per share of $2.01 represented 22% year-over-year growth. iPhone strength in China and services performance held the line despite memory cost pressures.

Apple avoided the capex debate entirely, and the market rewarded the simplicity. Shares rose 3.6% after hours on 30 April.

The selling pressure on Meta and Microsoft was not a verdict on their businesses. It was a verdict on timelines.

Both partially recovered by 1 May (Meta +13.25%, Microsoft +5.32% price returns per Morningstar data; these represent unverified intraday recoveries).

Analyst characterisations of the post-earnings reaction noted that investor patience with AI infrastructure spend “is not unlimited,” even when quarterly results demonstrate clear operational momentum.

The market is not questioning whether AI works. It is pricing how long the full payback takes.

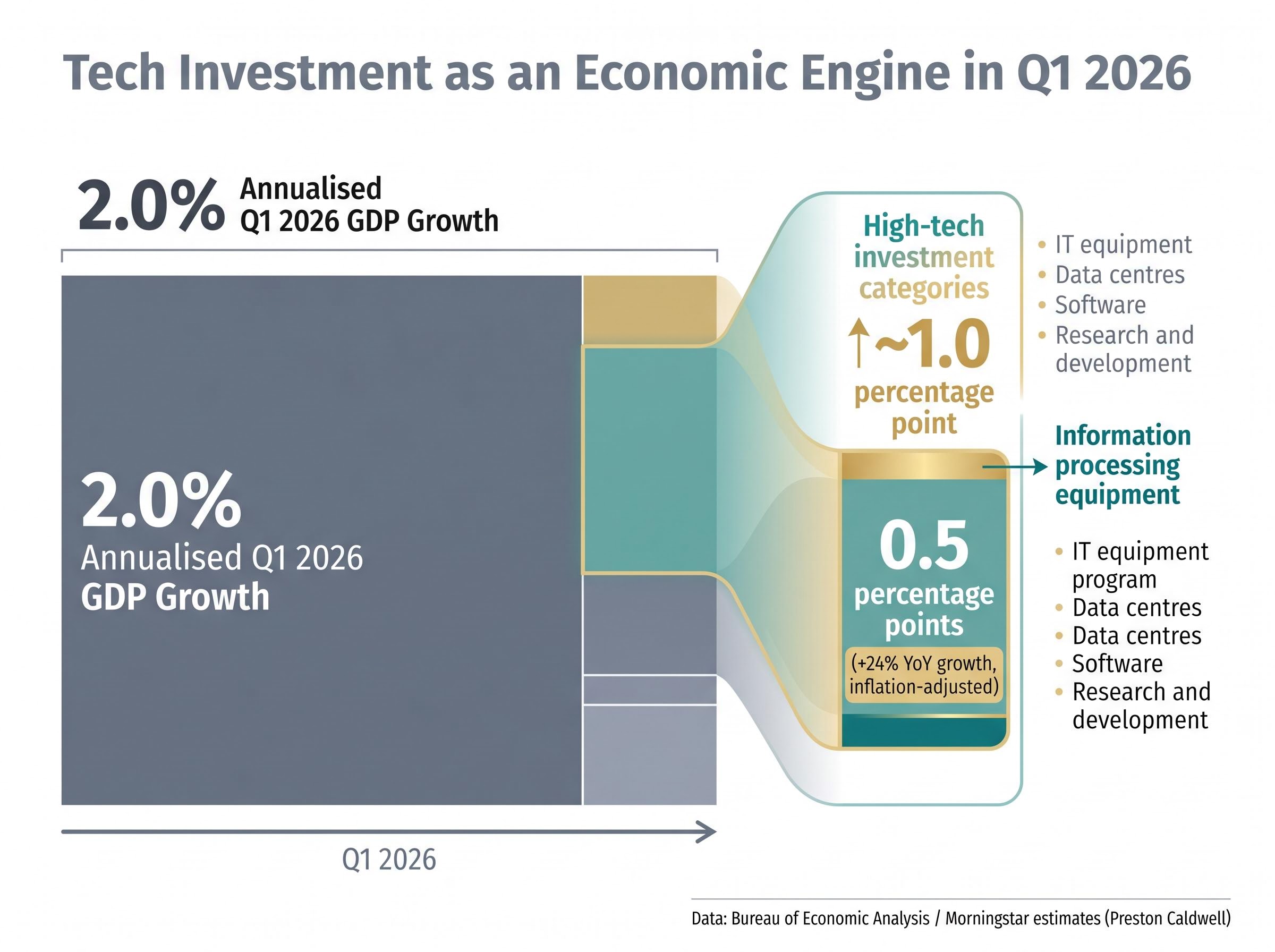

The capex commitments evaluated at the company level are simultaneously functioning as one of the largest demand-side growth drivers in the broader US economy.

Private fixed investment in information processing equipment, a standard proxy for AI’s economic footprint, rose 24% year over year in inflation-adjusted terms during Q1 2026. That single category contributed an estimated 0.5 percentage points to the 2.0% annualised Q1 2026 GDP growth rate, representing roughly one quarter of total economic expansion.

Preston Caldwell, Morningstar Senior US Economist, noted that high-tech investment categories collectively contributed approximately one percentage point to GDP growth, and suggested the Bureau of Economic Analysis may be underestimating IT expenditure.

The sub-categories driving that contribution include:

These high-tech investment categories accounted for more than the entirety of growth in private fixed investment as of Q1 2026, according to Caldwell. For investors, this carries implications beyond individual company balance sheets: the AI capex cycle is now a measurable macroeconomic force affecting monetary policy calculations and equity market valuations alike.

Amazon delivered the earnings cycle’s sharpest illustration of the gap between operational narrative and investor verdict.

AWS revenue hit $37.59 billion in Q1 2026, growing 28% year over year, the fastest rate in 15 quarters. The growth was directly linked to AI adoption, with partnerships including OpenAI, Anthropic, and Meta noted in the capex context. CEO Andy Jassy described AWS as a “bright spot” and pointed to stable consumer spending metrics.

What went right operationally:

What drove the stock lower:

Shares fell approximately 6% post-earnings and sat at -7.05% price return as of 1 May 2026. Unlike Meta and Microsoft, there was no meaningful recovery.

The five-company scorecard leaves one question unresolved: are the capex commitments across these hyperscalers justified by underlying demand, or is spending running ahead of the infrastructure cycle?

Nvidia’s Q1 2026 earnings, scheduled for 20 May 2026, are positioned to answer that question. Two scenarios frame the binary:

Q1 2026 marked the sixth consecutive quarter of double-digit EPS growth for the S&P 500, with the tech sector leading at +12.6% overall. Analyst consensus as of early May 2026 is that the AI cycle is accelerating rather than peaking, but that consensus depends heavily on Nvidia’s forward guidance confirming continued infrastructure demand.

(Note: Tesla reported separately on 22 April, sitting outside this earnings wave.)

The five companies collectively demonstrated that AI investment is producing measurable revenue acceleration, most clearly at Alphabet and Microsoft. Investor sentiment, however, is being shaped not by whether the returns exist, but by how long the full payback window extends.

With Nvidia reporting on 20 May and the Federal Reserve holding rates steady amid unusual internal dissent, the macro and sector context for the AI investment cycle remains unsettled. The Q1 2026 results are a snapshot of an accelerating cycle, not a final verdict. The companies best positioned are those where AI revenue growth is visibly outpacing capex expansion.

Nvidia’s results on 20 May represent the next definitive signal. Azure and Google Cloud quarterly growth rates remain the most reliable indicators of whether hyperscaler AI spend is generating proportionate returns.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

All five major US tech companies, Alphabet, Amazon, Apple, Meta, and Microsoft, beat consensus revenue or earnings estimates in Q1 2026, but only Alphabet and Apple saw their stocks rise immediately after results, as investor focus shifted to massive AI infrastructure spending commitments totalling an estimated $650-$725 billion across the four major hyperscalers.

Despite strong quarterly results, Meta and Microsoft raised their 2026 capex guidance, with Meta lifting its range to $125-$145 billion and Microsoft committing approximately $190 billion, which investors interpreted as extending the payback timeline for AI investment and pushed both stocks lower in after-hours trading.

AWS revenue grew 28% year over year to $37.59 billion in Q1 2026, the fastest rate in 15 quarters, but Amazon shares fell roughly 6% post-earnings because the reaffirmed $200 billion capex commitment for 2026 failed to reassure investors about near-term earnings visibility or the timeline for returns on AI infrastructure spending.

Nvidia's Q1 2026 earnings, scheduled for 20 May 2026, are considered the key signal for whether hyperscaler AI capex commitments are justified by real demand; strong guidance would validate the spending cycle, while cautious guidance could intensify concerns about capex running ahead of returns at Meta, Microsoft, and Amazon.

Private fixed investment in information processing equipment rose 24% year over year in real terms during Q1 2026, contributing an estimated 0.5 percentage points to the 2.0% annualised GDP growth rate, meaning AI capex is now a measurable macroeconomic force, not just a balance sheet consideration for individual tech companies.