Financial markets are pricing a 76% chance that the Reserve Bank of Australia (RBA) will lift the cash rate to 4.35% tomorrow, which would mark the highest level since the post-GFC tightening cycle. The trigger is clear: Q1 inflation landed at 4.6% on 29 April 2026, its hottest reading since September 2023, and the breadth of price pressures across housing, transport, goods, and services has left the RBA board with limited room to stand pat. With the Monetary Policy Board currently in session (4-5 May 2026) and the decision due at 2:30 pm AEST on 5 May, the stakes extend beyond a single quarter-point move. A federal budget loaded with cost-of-living relief arrives one week later on 12 May, and global stagflation signals are complicating the calculus for Governor Michele Bullock. What follows breaks down the inflation data driving the expected hike, what the budget means for the rate path, and the specific implications for Australian borrowers and investors who need to act on this information now.

What the Q1 inflation numbers are really telling the RBA

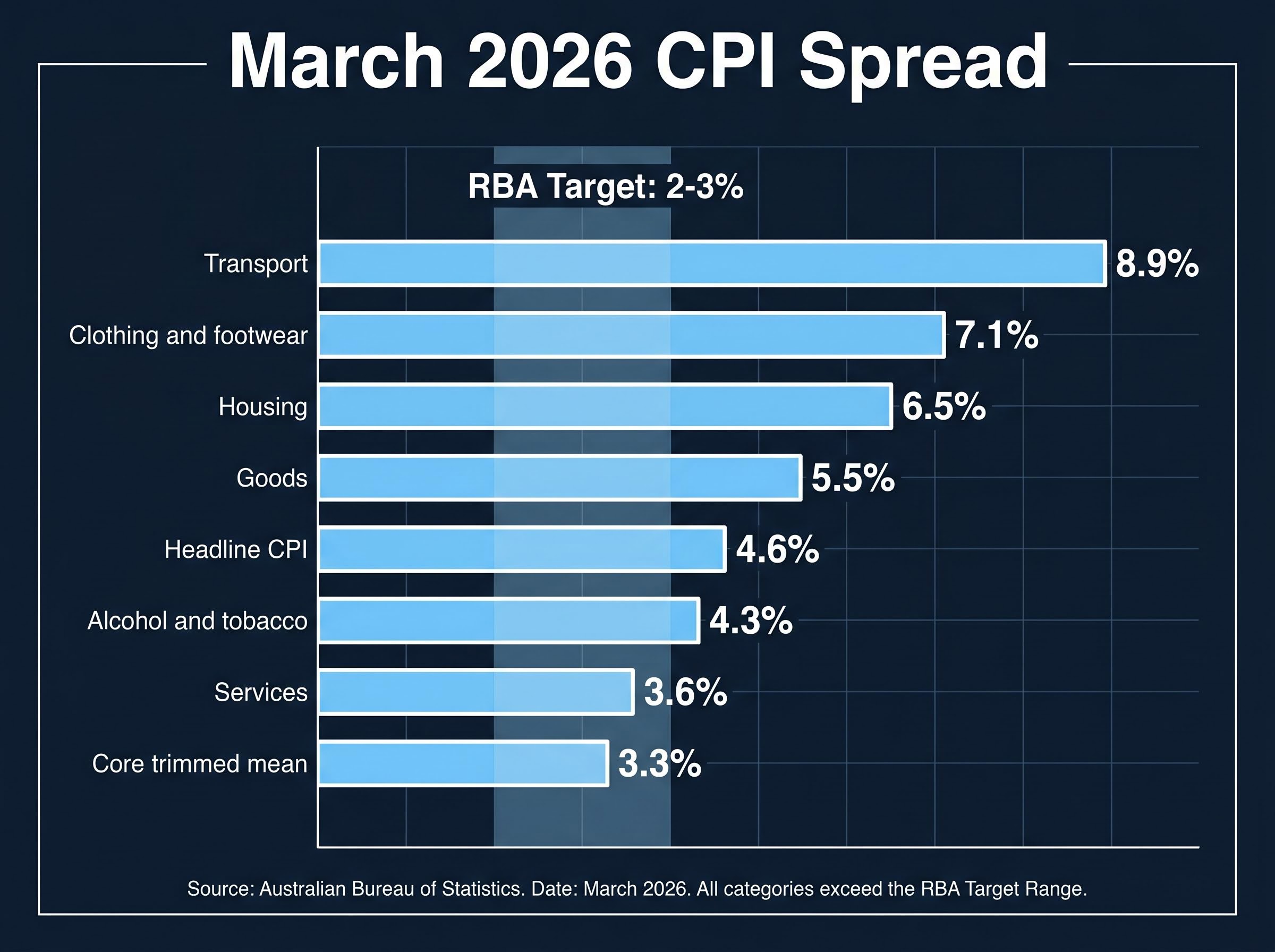

The headline figure alone would be enough to keep the board uncomfortable. Annual CPI hit 4.6% in Q1 2026, with the core trimmed mean sitting at 3.3%, well above the RBA’s 2-3% target band.

The RBA cash rate target framework sets out the board’s price stability mandate, including the 2-3% inflation target band that Q1 2026 CPI has now breached by more than 150 basis points on the headline measure.

What makes this reading harder to dismiss is not the headline but the spread. Housing inflation is running at 6.5%. Clothing and footwear accelerated to 7.1%. Goods inflation jumped from 3.5% in February to 5.5% in March. Services inflation held at 3.6%, stubbornly above the target ceiling. Alcohol and tobacco added 4.3%.

Transport inflation swung from -0.2% in February to 8.9% in March 2026, a single-month reversal that reflects oil prices holding above US$80 per barrel for three consecutive months amid ongoing Middle East conflict.

The RBA’s March 2026 statement explicitly flagged material inflation risk and acknowledged a real possibility that price growth stays above target longer than forecast. That language reads differently now, with Q1 data confirming exactly the scenario the board warned about.

| CPI Category | March 2026 Reading | Prior / Target |

|---|---|---|

| Annual CPI (headline) | 4.6% | RBA target: 2-3% |

| Core trimmed mean | 3.3% | RBA target: 2-3% |

| Housing | 6.5% | RBA target: 2-3% |

| Transport | 8.9% | -0.2% (Feb 2026) |

| Goods | 5.5% | 3.5% (Feb 2026) |

Simultaneous acceleration across unrelated spending categories signals this is not a temporary spike the RBA can look through. For borrowers and equity investors, the breadth of the data explains why market pricing is so one-sided.

Household inflation expectations reached 5.9% in April 2026 according to ANZ-Roy Morgan data, a level that raises the risk of second-round wage and price effects; when households expect sustained inflation, wage negotiations and business pricing decisions adapt accordingly, embedding the very persistence the RBA is trying to eliminate.

When big ASX news breaks, our subscribers know first

Why 76% market certainty is not the same as certainty

ASX 30-day futures imply approximately 74% probability of a 25 basis point hike to 4.35%, as of the 30 April close. A Finder survey published on 1 May 2026 placed 75% of experts in the hike camp. Broader market instruments put the odds somewhere between 72% and 86%.

The major banks are aligned:

- Westpac expects a 25bp hike, citing persistent inflation discomfort

- CBA forecasts a May hike driven by sustained inflationary pressure

- NAB also calls for a move to 4.35%

- AMP’s Shane Oliver views market pricing as overly aggressive, suggesting the probability of a hike is lower than the implied 76%

The March 2026 board vote was 5-to-4 in favour of hiking, the narrowest possible majority. That margin is the clearest evidence that internal RBA disagreement on the tightening question is genuine, not performative.

A 76% probability still embeds a meaningful chance of no movement. Retail investors who treat the hike as a foregone conclusion before 2:30 pm AEST tomorrow are carrying more positioning risk than the numbers support.

How Australian interest rates got here, and where the path leads

The current cash rate of 4.10% reflects a tightening cycle that has already moved well beyond what most borrowers expected. The March 2026 hike was the most recent step, and market pricing suggests it will not be the last.

ASX implied yield curves signal a cash rate approaching 4.8% by the end of 2026. If that pricing holds, it implies two further hikes beyond the expected May move, a trajectory that would take rates to levels not seen in over a decade.

The three things to watch from Tuesday’s 2:30 pm AEST release

The May meeting is a Statement on Monetary Policy (SoMP) meeting, which means the RBA’s updated economic forecasts will accompany the decision. That makes three distinct pieces of information worth watching, in order of forward significance:

- The rate decision itself (hike to 4.35% or hold at 4.10%), released at 2:30 pm AEST on 5 May 2026

- The SoMP’s updated inflation and GDP forecasts, released simultaneously, which will signal how the board sees the economy evolving over the next 12-18 months

- Governor Bullock’s press conference at 3:30 pm AEST, where the tone of forward guidance, and any indication of whether the board remains split, will carry more weight for rate path pricing than the binary decision

The SoMP forecasts will matter as much as the rate call. Investors watching only the hike/hold binary risk missing the more important signal: the RBA’s own projection of where inflation and growth are heading next.

The federal budget enters the frame one week later

The RBA may hike on Tuesday. Seven days later, on 12 May 2026, Treasurer Jim Chalmers delivers the federal budget. The timing creates a policy collision that neither institution can ignore.

The RBA is tightening monetary policy to cool demand. The government is loosening fiscal policy to ease cost-of-living pressure. Both actions land in the same fortnight.

The mechanism is straightforward: expansionary fiscal measures stimulate spending at exactly the moment the central bank is trying to suppress it. The pre-announced measures include:

- Energy rebate extensions, designed to offset household electricity costs

- Potential fuel excise reductions, which would lower transport costs

- Personal income tax cuts, effective 1 July 2026, injecting additional disposable income into the economy in the same quarter the RBA is fighting inflation

Fiscal stimulus into an inflation problem typically forces the central bank to work harder to achieve its price stability mandate. For retail investors, the budget interaction raises the probability of additional RBA hikes beyond May, extending mortgage stress and maintaining downward pressure on rate-sensitive equities.

Second-round oil price effects through freight costs, construction materials, and services pricing are still working through supply chains and were largely absent from the Q1 quarterly data, meaning the inflation picture for mid-2026 may look materially worse before Q2 and Q3 CPI readings clarify whether the March surge was a one-off or the start of a broader pass-through cycle.

Global stagflation signals and why the RBA cannot ignore them

The IMF’s April 2026 World Economic Outlook projected global growth of 3.1% for 2026, paired with a concurrent rise in inflation. That combination, slower growth alongside rising prices, is the definition of stagflation pressure.

The Bank of Japan offered a live case study at its May meeting. It held rates despite raising its core inflation projection to 2.8%, because its growth outlook deteriorated sharply: the FY2026 GDP growth forecast was cut from 1.0% to 0.5% in a single update.

The Bank of Japan slashed its FY2026 GDP growth forecast from 1.0% to 0.5% while simultaneously raising its inflation projection, a combination that Oxford Economics characterised as resembling mild stagflation.

What global slowdown means for the Australian rate outlook

The RBA’s 5-to-4 March vote suggests at least four board members already weigh the growth risk heavily. Australia’s economy, dependent on commodity exports and trade flows, is not insulated from a global demand contraction. A sustained slowdown would reduce commodity prices and export revenues, weakening the economic foundation supporting current rate levels.

If global growth deteriorates further, the RBA may face its own version of Japan’s dilemma: an inflation rate that demands tightening and a growth outlook that cannot absorb it. That tension could force a pivot faster than the yield curve’s 4.8% year-end pricing currently implies.

What a rate hike means for Australian borrowers and investors tomorrow

No major lender has confirmed pass-through decisions ahead of the announcement:

- CBA has flagged potential variable rate adjustments

- ANZ has flagged potential variable rate adjustments

- Westpac has flagged potential variable rate adjustments

- NAB has flagged potential variable rate adjustments

All four are expected to pass through a full 25bp increase to variable mortgage rates if the RBA moves.

| Mortgage Balance | Monthly at 4.10% | Monthly at 4.35% | Monthly at 4.80% |

|---|---|---|---|

| $600,000 | $3,220 | $3,300 | $3,440 |

| $800,000 | $4,293 | $4,400 | $4,587 |

The AUD/USD is trading around 0.7207 ahead of the decision, having risen from cycle lows of 0.6843. The ASX 200 sits at approximately 8,704 points. For equity investors, the more important variable than tomorrow’s binary outcome is whether Bullock’s press conference signals a pause after May or confirms the market’s two-more-hikes pricing toward 4.8% by year-end.

The decision lands tomorrow at 2:30 pm AEST, and what happens next will matter more

The rate call is the start of a sequence, not the end of a story. Three events in the next eight days will determine the actual rate path for 2026:

- 2:30 pm AEST, 5 May 2026: Rate decision and Statement on Monetary Policy release at rba.gov.au, including updated inflation and GDP forecasts

- 3:30 pm AEST, 5 May 2026: Governor Bullock’s press conference, where forward guidance and any indication of continued board division (a 5-to-4 board is materially different from a unanimous one) will shape rate path expectations

- 12 May 2026: Federal budget delivery, with personal income tax cuts effective 1 July 2026 and energy rebates potentially extending fiscal stimulus into the same quarter the RBA is tightening

Retail investors who understand that the SoMP and press conference carry more forward information than the binary hike/hold decision will be better positioned to interpret market reactions on 5-6 May and adjust their mortgage or portfolio strategy accordingly.

For investors wanting to reposition portfolios around a prolonged high-rate environment, our full explainer on stagflation investing strategies covers the specific asset allocation moves that have historically performed in supply-shock stagflation cycles, including the role of hydrocarbon exporters, short-duration fixed income, and cash buffers when both equities and bonds face simultaneous headwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding interest rate projections and market pricing are subject to change based on evolving economic conditions and RBA board decisions.