ASX 30-day interbank cash rate futures are pricing a 76% probability that the Reserve Bank of Australia will raise the cash rate on Tuesday 5 May 2026, returning it to 4.35% for the first time since its prior peak. A Reuters poll of economists conducted between 27 and 30 April found near-unanimous agreement. Yet a growing cohort now believes 4.35% is merely a staging post on the way to 4.85%. The RBA’s interest rate decision arrives at a point where domestic inflation remains stubbornly above target, a Strait of Hormuz-driven oil shock threatens to embed cost pressures more deeply, and the gap between where markets expect rates to settle and where they may actually land is widening. What follows maps the inflation evidence behind Tuesday’s expected hike, examines what the RBA’s updated staff projections may reveal about the rate path to year-end, and offers a framework for understanding what a sustained high-rate environment means for Australian dollar assets and rate-sensitive investments.

What the RBA is expected to decide on Tuesday, and why the consensus has hardened

Six weeks ago, the March board vote split 5-4 in favour of hiking to 4.10%. That margin was narrow enough to leave open the possibility of a pause. It no longer does.

The consensus for a 25 basis point increase to 4.35% on 5 May has hardened across major bank research desks and the broader economist community, with the Reuters poll confirming the near-unanimity of that expectation. ASX 30-day futures reflect the same view, with pricing across instruments ranging from 62% to 86% probability of the hike.

When RBA rate hike odds first crossed 62% in late April, the market consensus was still anchored by the possibility that softer trimmed mean readings could give the board pause; the shift to near-unanimity by the time of the Reuters poll reflects how rapidly the oil shock recalibrated that calculus.

Reuters poll (27-30 April 2026): Near-unanimous economist expectation of a 25 bps hike at the May meeting, the third consecutive increase in the current tightening cycle.

The three largest domestic forecasters have converged on the same conclusion, though each arrived via a slightly different route:

- Westpac reaffirms the May hike, citing prior inflation discomfort and the need to restrain a tight economy

- ANZ expects the increase despite softer Q1 2026 core inflation readings, pointing to underlying pressures and expected fuel cost pass-through as overriding factors

- NAB anticipates the May hike before pausing to assess fuel price impacts and their potential to embed in inflation expectations

The degree of consensus matters. A rate move that is fully priced carries very different implications for the Australian dollar and rate-sensitive assets than a surprise; the market-moving element on Tuesday is more likely to come from the RBA’s accompanying statement and staff projections than from the headline number itself.

When big ASX news breaks, our subscribers know first

Why Australian inflation remains so stubborn: the domestic story and the oil shock

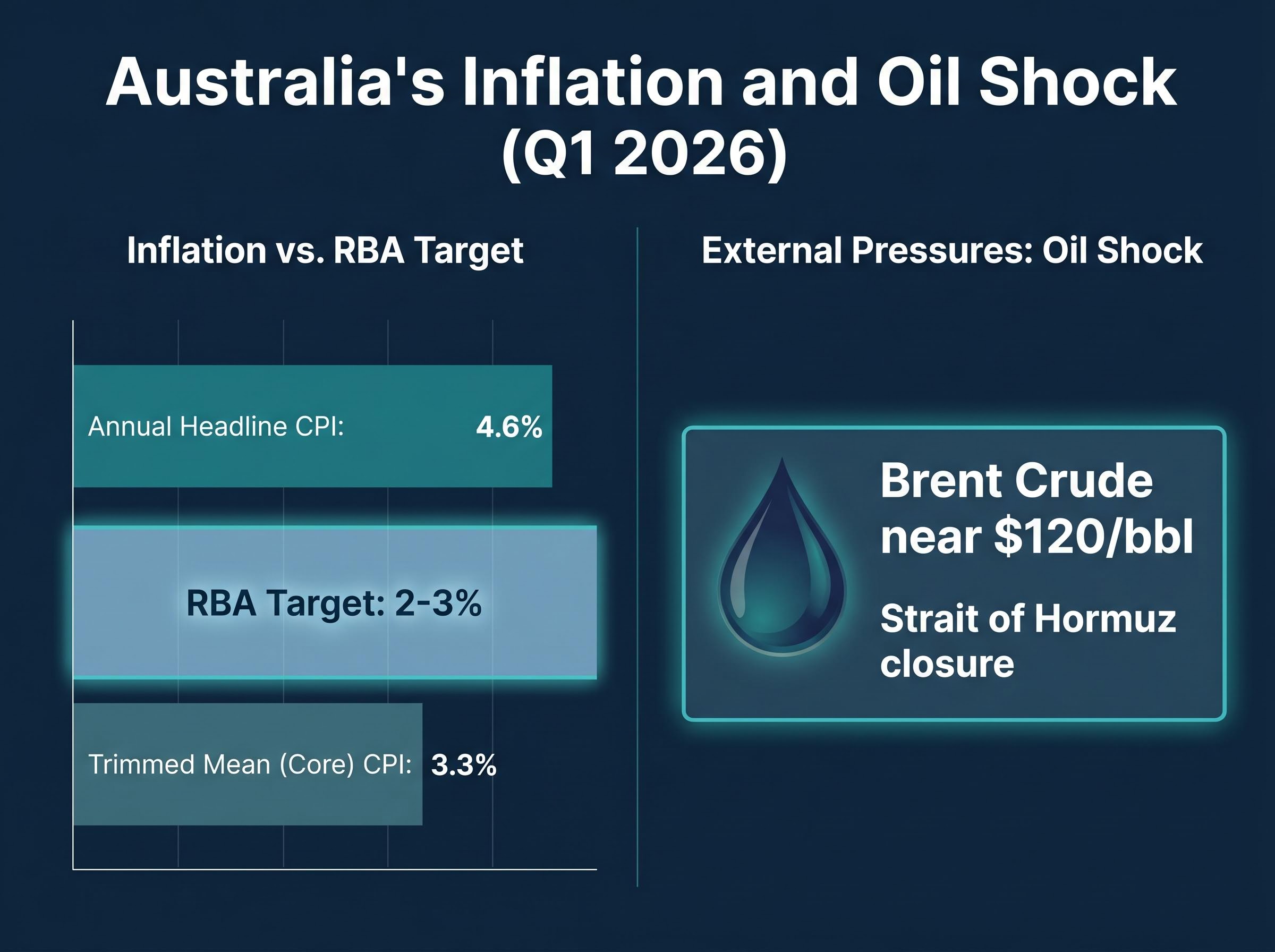

The domestic inflation problem was already difficult before the oil shock made it worse. Q1 2026 data confirmed that prior rate increases have not yet brought price growth back within the RBA’s 2-3% target band.

| Inflation Measure | Q1 2026 Reading | Prior Period Reading | RBA Target |

|---|---|---|---|

| Annual Headline CPI | 4.6% | 3.7% (12 months to February 2026) | 2-3% |

| Trimmed Mean (Core) CPI | 3.3% | 3.3% (unchanged) | 2-3% |

| Monthly CPI (March 2026) | 1.1% (original and seasonally adjusted) | N/A | N/A |

Headline CPI at 4.6% sits a full cycle above the top of the target band. Trimmed mean inflation, which strips out the most volatile items, has not moved at all, remaining stuck at 3.3%. Monthly CPI for March came in at 1.1%, reinforcing the persistence of price pressures heading into Tuesday’s decision.

The ABS Consumer Price Index release for March 2026 confirmed headline annual inflation at 4.6%, trimmed mean at 3.3%, and monthly CPI at 1.1%, each figure sitting outside the RBA’s 2-3% target band and providing the statistical foundation for Tuesday’s near-unanimous tightening consensus.

Then there is the external accelerant. The closure of the Strait of Hormuz has pushed Brent crude near $120/bbl, with broader crude benchmarks above $110/bbl. This is a qualitatively different inflation risk from the demand-driven pressures the RBA has been fighting. Supply-side shocks can embed in expectations even if domestic demand conditions moderate, because they raise input costs across the economy simultaneously.

NAB has specifically flagged the risk that fuel prices could cement inflation expectations in a near-full-capacity economy, complicating the path back to target even if core inflation shows some softness.

The distinction matters for investors: the RBA’s primary tool, the cash rate, is calibrated to suppress demand. It cannot resolve a geopolitical supply disruption. That mismatch is why the rate path remains so uncertain even when Tuesday’s outcome is not.

How central bank rate cycles move asset prices: a framework for Australian investors

The transmission mechanism: from the RBA’s decision to your portfolio

A cash rate increase does not arrive in isolation. It flows through the financial system in stages. When the RBA raises its rate, the cost of overnight lending between banks rises. That feeds through to retail mortgage rates within days, increasing monthly repayments for variable-rate borrowers. It raises the cost of corporate debt, making it more expensive for companies to finance operations and expansion. And it lifts the “discount rate” that investors use to value future cash flows.

The discount rate concept is worth pausing on. When investors price a company’s future earnings, they discount those earnings back to today’s value. A higher discount rate means future earnings are worth less in today’s terms. This is why share prices can fall even when a company’s earnings outlook has not changed: the rate at which those earnings are valued has risen.

RBA research on monetary policy transmission channels identifies housing finance costs and the exchange rate as the two fastest-moving conduits through which cash rate changes reach the broader economy, a finding that explains why property valuations and the AUD respond within days of a rate decision rather than over quarters.

Which Australian asset classes feel the pressure first

Not all assets respond to higher rates in the same direction. In the current environment, with the cash rate returning to 4.35% and the Australian dollar at approximately $0.7189 against the US dollar (as of 29 April 2026):

- Negatively affected: Residential property and REITs face higher borrowing costs and compressed valuations. Long-duration bonds lose value as yields rise. Equities with high debt loads see financing costs eat into margins.

- More resilient or positively affected: Cash deposits and term deposits offer higher returns. Floating-rate instruments benefit directly from rising rates.

- Complex dynamics: Commodity-linked resource stocks occupy a more nuanced position. Australia’s Index of Commodity Prices fell 0.8% in Australian dollar terms in April 2026, yet oil-exposed names are benefiting from the same energy shock that is driving the RBA’s hand. The net effect depends on the individual company’s cost structure and commodity exposure.

This framework converts Tuesday’s headline number into a practical tool for evaluating any rate-sensitive position, not just those immediately linked to the RBA’s announcement.

The debate about where rates go after Tuesday: 4.35% as peak or staging post

The hike itself is settled. The question that will move markets is what comes after.

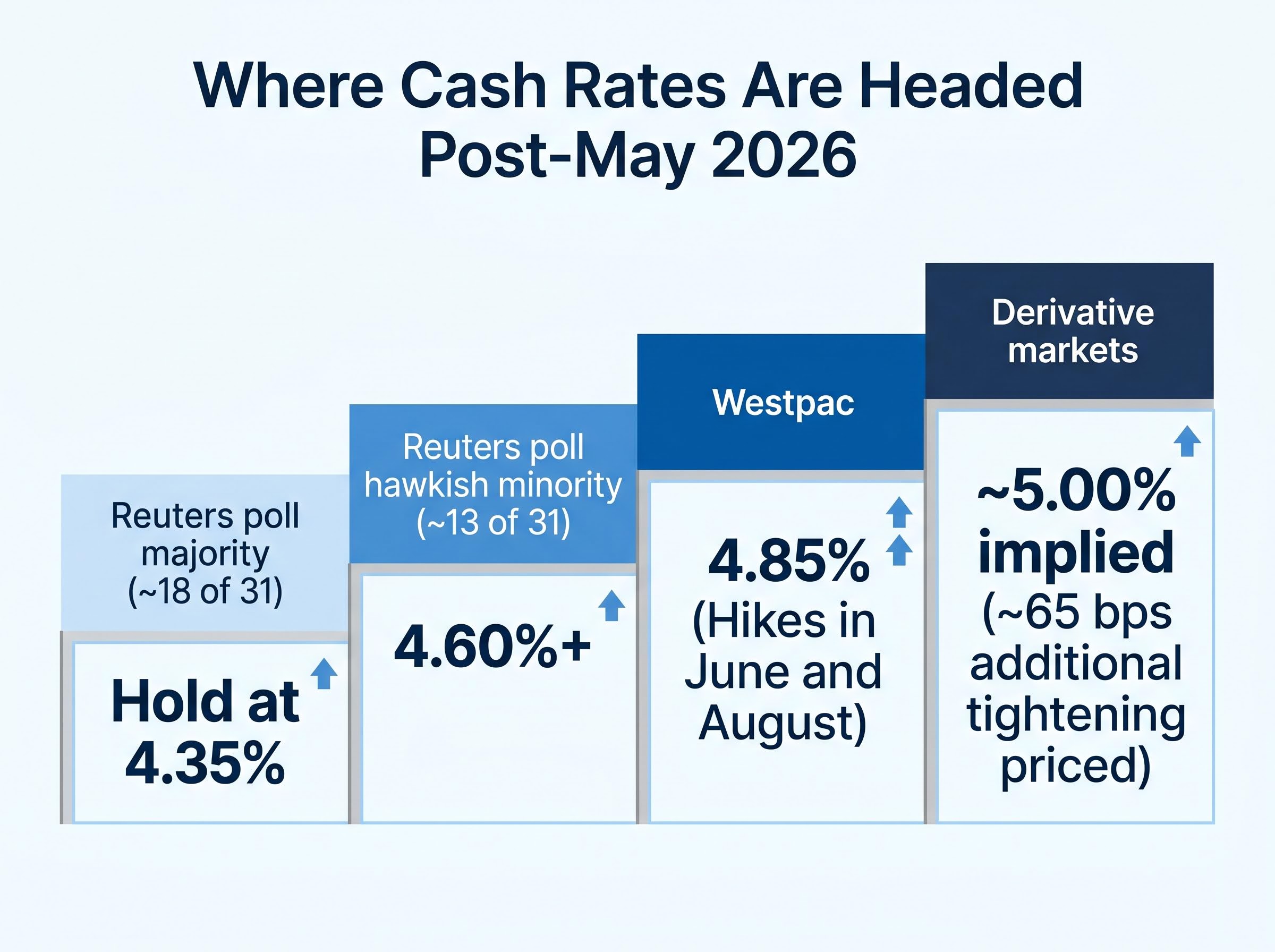

Two camps have formed. The majority view, held by approximately 18 of 31 economists surveyed by Reuters, is that the cash rate holds at 4.35% after May. The hawkish minority, now more than one-third of respondents, forecasts a year-end rate of 4.60% or above.

In the March Reuters poll, not a single surveyed economist forecast a cash rate of 4.60% or higher by year-end. By late April, more than one-third did. The shift in just five weeks reflects how rapidly the oil shock has altered the policy calculus.

Westpac has published the most detailed articulation of the hawkish case, forecasting additional hikes in June and August 2026 to reach a terminal rate of 4.85%. Derivative markets tell a similar story, pricing approximately 65 basis points of additional tightening by year-end.

Second-round oil price pass-through, the mechanism by which an initial energy price shock embeds across freight, construction materials, and services costs in subsequent quarters, is precisely what makes the difference between a single hike to 4.35% and a multi-step tightening cycle to 4.85% a genuine open question rather than a tail risk.

| Forecaster / Source | Post-May Forecast | Year-End Rate Forecast |

|---|---|---|

| Reuters poll majority (~18 of 31) | Hold at 4.35% | 4.35% |

| Reuters poll hawkish minority (~13 of 31) | Further hikes | 4.60%+ |

| Westpac | Hikes in June and August | 4.85% |

| Derivative markets | ~65 bps additional tightening priced | ~5.00% implied |

The RBA’s updated staff economic projections, released alongside Tuesday’s decision, are likely to be the most market-moving element of the announcement. Those projections will reveal whether the board sees inflation returning to target under current settings or whether further tightening is needed. For mortgage holders and bond investors, the difference between a 4.35% terminal rate and a 4.85% terminal rate is not a rounding error; it represents thousands of dollars in annual repayments and a meaningful repricing of duration-sensitive portfolios.

What a return to 4.35% means for Australian dollar assets in practice

The educational framework from the previous section is now playing out in real time. The Australian dollar, Australian property, and AUD-denominated portfolios are all responding to the tightening cycle, but not in the straightforward way a textbook rate-currency relationship might suggest.

RBA-Fed divergence: The RBA is hiking for a third consecutive meeting while US money markets price no change to the Federal Reserve’s funds rate through the remainder of 2026. This unusual policy divergence is a live factor in AUD/USD dynamics.

A widening rate differential between Australia and the United States would typically support the Australian dollar. Yet the AUD sat at approximately $0.7189 on 29 April, reflecting the countervailing pressures of softening commodity prices (the Index of Commodity Prices down 0.8% in AUD terms in April) and shifting global risk appetite.

The practical implications extend across asset classes:

- Australian dollar: Supported by rate differentials but pressured by commodity softness and global uncertainty. The net direction depends on which force dominates.

- Property and mortgages: A move to 4.35% increases variable mortgage costs immediately. Under Westpac’s 4.85% scenario, the cumulative effect would represent a material escalation in household debt servicing costs.

- Bonds: Long-duration Australian government bonds face further mark-to-market losses if the market reprices for additional hikes.

- Equities: Companies with high leverage face margin compression, while energy producers may benefit from the same oil shock driving the tightening.

- Cash and term deposits: Offer the highest returns in over a decade, making them an increasingly competitive allocation for conservative portfolios.

The rate cycle does not operate in isolation. The divergence between RBA and Fed policy, combined with softening commodity prices, creates a more complex environment than a simple “higher rates equal stronger currency” narrative.

The higher-for-longer scenario is no longer the tail risk

From a contested 5-4 March vote to near-unanimous May consensus, the RBA’s tightening cycle has accelerated faster than markets anticipated at the start of 2026. Tuesday’s rate decision to 4.35% is effectively settled. The real question for investors and households is what the accompanying staff projections reveal about further moves.

The RBA’s experience in 2025, when a premature easing cycle had to be reversed, has made the board more cautious about declaring victory over inflation. With headline CPI at 4.6%, core inflation stuck at 3.3%, and an oil shock threatening to embed cost pressures, “higher for longer” deserves to be treated as the base case rather than a risk scenario.

The historical relationship between oil supply shocks and rate normalisation offers a counterweight to the hawkish consensus: in prior supply-driven inflation episodes, growth damage from elevated energy costs has typically overtaken inflation as the dominant central bank concern within 6-12 months of a shock’s peak, compressing the window for further tightening.

Tuesday’s Statement on Monetary Policy, particularly the updated inflation and GDP growth projections, will carry more information about the terminal rate than the rate decision itself. Those projections are the signal to watch.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections discussed in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.