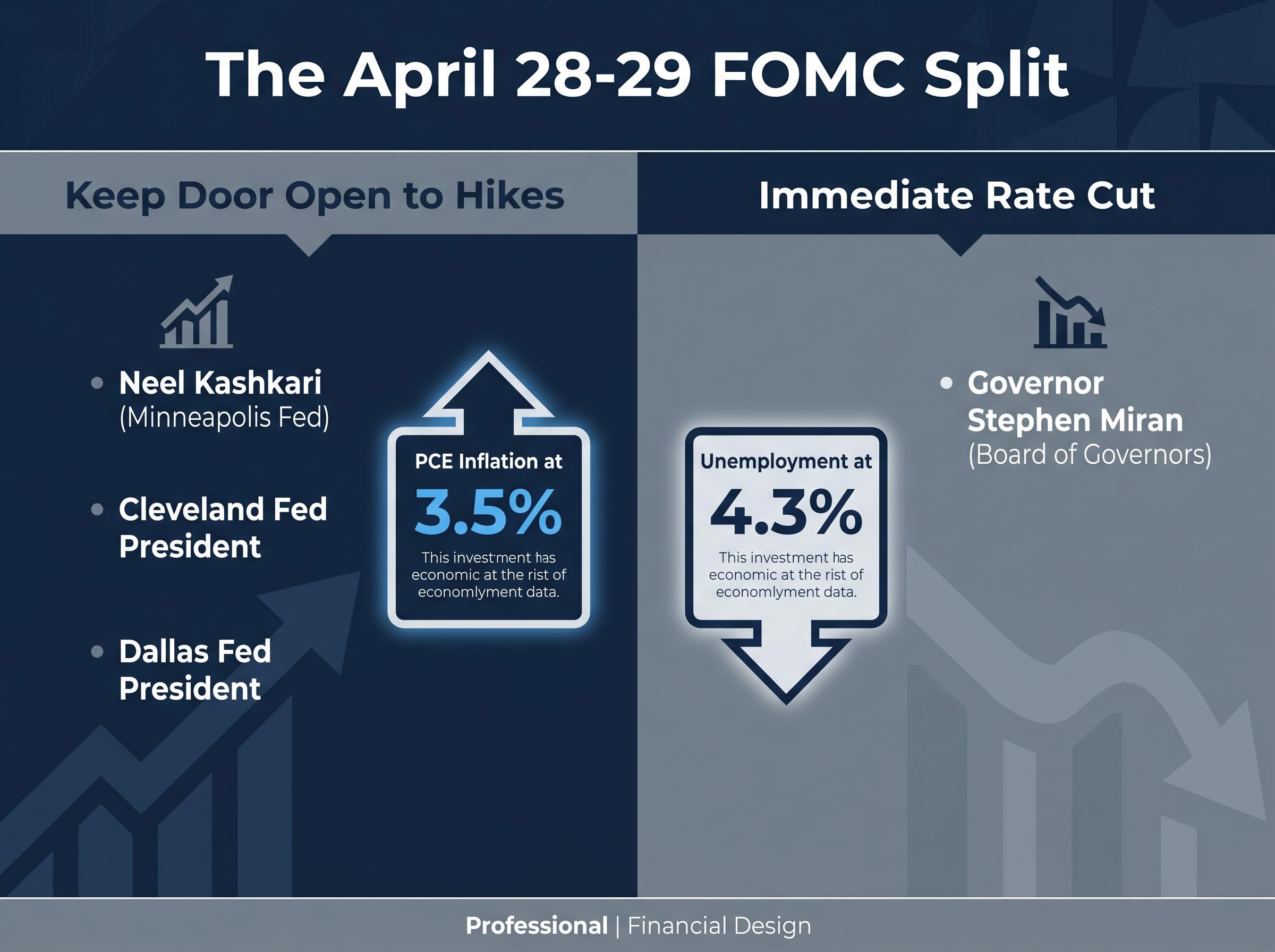

Four Federal Reserve officials dissented at the April 28-29 FOMC meeting, the broadest internal split in years, and the dissents pointed in opposite directions. Three wanted the door open to rate increases. One wanted a cut immediately. The Fed held rates at 3.5%-3.75%, but the vote revealed an institution pulled apart by forces it cannot reconcile: PCE inflation running at 3.5% against a 2% target, unemployment climbing to 4.3%, and a war in Iran now in its tenth week that has closed the Strait of Hormuz and pushed Brent crude to $108-$116 per barrel. The Fed rate decision on 29 April satisfied no faction on the committee, and the fracture lines it exposed carry more signal than the hold itself. What follows is an analysis of what the four-way dissent reveals about the Fed’s internal balance of risk, how the energy shock constrains its options, and what the resulting uncertainty means for rate-sensitive portfolios.

The four-way FOMC dissent that exposed a fractured Fed

Who dissented and why

The April meeting produced four named dissenters, each representing a distinct reading of the same data.

| Dissenter | Institution | Preferred action | Rationale |

|---|---|---|---|

| Neel Kashkari | Minneapolis Fed | Keep door open to hikes | PCE at 3.5% risks embedding inflation if the committee signals cuts prematurely |

| Cleveland Fed President | Cleveland Fed | Keep door open to hikes | Energy-driven inflation could persist beyond the conflict, requiring tighter policy |

| Dallas Fed President | Dallas Fed | Keep door open to hikes | Supply-shock inflation is already transmitting to broader price measures |

| Governor Stephen Miran | Board of Governors | Immediate rate cut | Unemployment at 4.3% signals labour market deterioration requiring pre-emptive support |

Both positions are internally coherent. The hawks see 3.5% PCE and conclude that accommodation would be reckless. Miran sees 4.3% unemployment and concludes that inaction risks a deeper slowdown the Fed will have to chase with larger cuts later.

What the official statement concealed

Despite three hawkish dissents outnumbering Miran’s dovish one by three to one, the official statement retained language pointing toward a cut as the next likely move. That language reflects Chair Powell’s preference for consensus optics. It does not reflect the committee’s actual centre of gravity.

The official FOMC statement released on 29 April confirmed the federal funds rate hold at 3.5%-3.75% and recorded the four named dissenters, making it the primary regulatory document against which all subsequent market interpretation has been measured.

The result is a gap between stated guidance and internal sentiment. Markets must interpret not just what the Fed said, but how much of what it said the committee actually believes.

When big ASX news breaks, our subscribers know first

What the leadership transition adds to an already unstable equation

Chair Powell’s term ends later in May 2026, and Kevin Warsh is expected to assume the chairmanship. The handover arrives at the precise moment the committee faces its most ambiguous policy environment in years.

What the current data lets Warsh actually do

Warsh signalled a preference for a more accommodative posture during his pursuit of the role. That preference is real. What is also real is the committee arithmetic and the data he will inherit.

Inheriting a 3.5% PCE reading and a four-way dissent where hawkish dissenters outnumbered dovish ones three to one leaves minimal room for an early dovish signal without triggering a credibility cost. A new chair faces a sequential set of constraints before pivoting to accommodation:

- Establish anti-inflation credibility: Markets and the committee need evidence that a new chair takes the 3.5% PCE reading seriously before they will accept any move toward easing

- Secure committee majority: The April dissent pattern shows Warsh would need to shift at least two hawkish members to build a majority for cuts

- Wait for data to shift: Until PCE moves meaningfully toward target or unemployment deteriorates further, the data does not support the pivot Warsh’s stated preference implies

The distinction between preference and capacity is the relevant one. Warsh’s accommodative instinct may be genuine, but the institutional and data context constrains its expression. The transition is a source of uncertainty in its own right, extending the period during which investors should expect unpredictable Fed signalling.

Balance sheet reduction may carry a larger simultaneous impact across fixed income, equities, and real estate than rate timing alone: accelerated quantitative tightening can steepen the yield curve even as the Fed holds or cuts short-term rates, creating a scenario where Warsh’s stated accommodative instinct on the fed funds rate coexists with tightening financial conditions through the long end.

How a closed strait becomes a Fed policy problem

The Strait of Hormuz carries roughly 20% of global oil and natural gas trade. Its closure, following U.S.-Israel airstrikes on Iran that began 28 February 2026, is not a sentiment shock or a speculative disruption. It is a structural supply event that removes a measurable share of global energy from the market.

The Hormuz closure removed approximately 13 million barrels per day from global supply, a disruption the IEA has described as having no modern parallel in scale or duration, and it is that baseline removal, not speculative positioning, that accounts for most of the price level the Fed is now treating as a structural input to its inflation models.

The transmission into monetary policy runs through three distinct channels:

- Energy prices to CPI and PCE: Brent crude at $108-$116 per barrel feeds directly into headline inflation readings, pushing PCE to 3.5% and CPI to 3.3%

- Supply chain disruption to goods inflation: Rerouted shipping and constrained capacity raise input costs across manufacturing sectors

- Demand destruction to labour market softness: Higher energy costs compress consumer spending and corporate margins, weakening employment

A corporate executive referenced by Kashkari estimated that even if the strait reopened today, supply chains would require approximately six months to normalise, placing full recovery no earlier than late 2026. The lag matters because it means the Fed cannot wait for resolution before acting; it must set policy on incomplete and evolving data.

A Barclays analyst note dated 1 May 2026 warned that current price increases have been relatively contained, but further inventory depletion could produce a sharp, non-linear price spike that would accelerate the inflationary impulse beyond current forecasts.

Bombing operations halted approximately four weeks before 3 May, yet prices remain elevated. The gap between the military pause and the economic relief tells its own story.

What “policy paralysis” actually means at the Fed

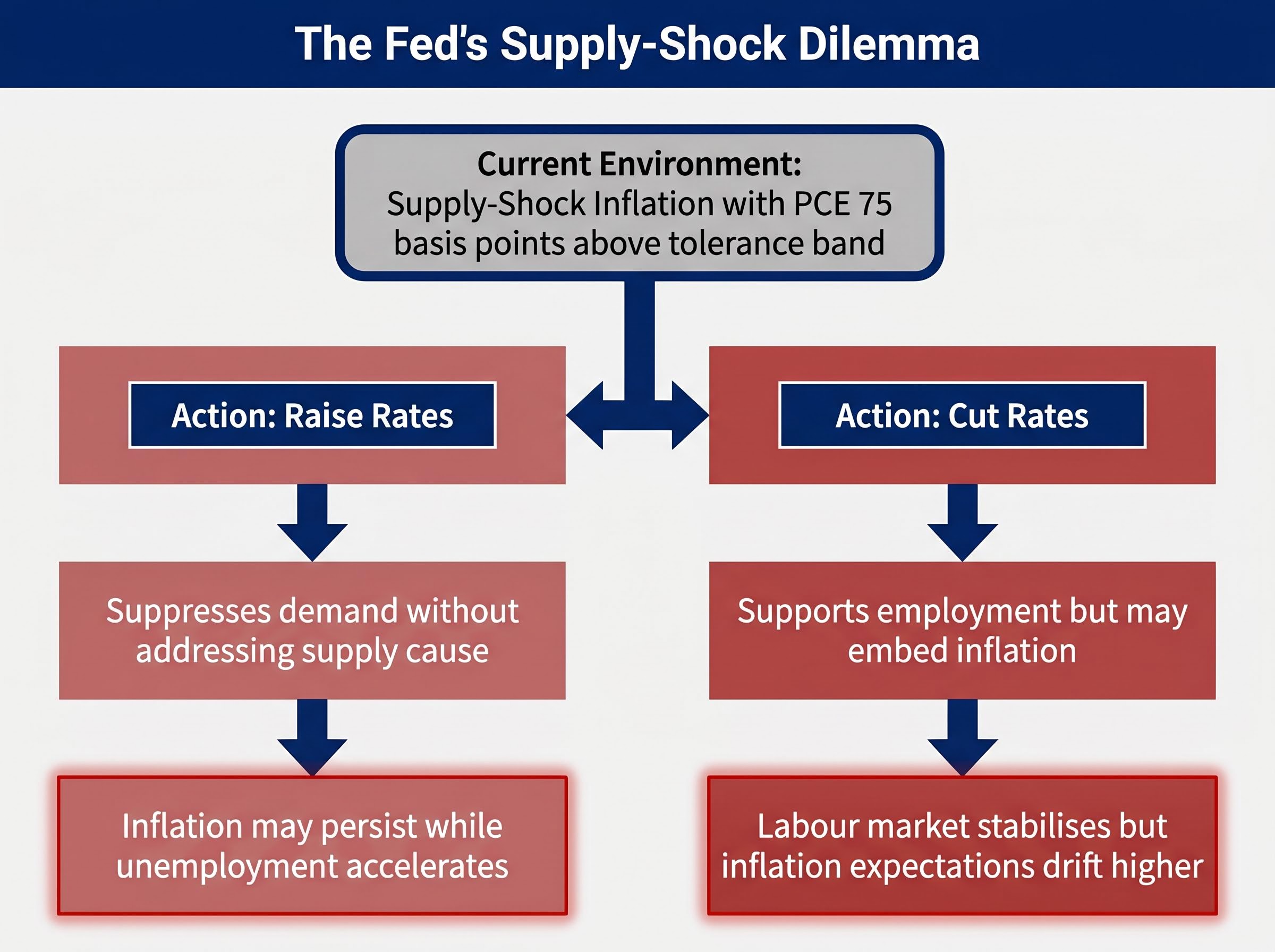

Under normal conditions, the Fed’s dual-mandate framework operates with a clean logic. When inflation runs above target, the committee raises rates to cool demand. When unemployment rises and growth slows, it cuts rates to stimulate activity. The two tools point in opposite directions, but they rarely need to fire simultaneously because inflation and labour market weakness typically do not arrive from the same source at the same time.

Supply-shock inflation breaks this framework. Cost-push inflation (prices rising because inputs cost more) is mechanically different from demand-pull inflation (prices rising because consumers are spending aggressively). The Fed’s interest rate tools are designed to address demand. They cannot drill oil, reopen a shipping lane, or rebuild a supply chain. Raising rates would suppress the demand side of the economy without touching the supply-side cause of the inflation, accelerating the labour market deterioration the conflict is already producing. Cutting rates to protect employment risks embedding higher inflation expectations at a moment when PCE sits 75 basis points above the top of the Fed’s tolerance band.

Supply-constrained inflation operating through an energy channel behaves differently from the demand-driven variety: central banks globally are confronting the same analytical problem the Fed faces, with disinflationary forces from Chinese manufacturing and AI productivity gains operating beneath the surface while headline energy costs dominate the near-term price signal.

| Scenario | Fed response | Outcome |

|---|---|---|

| Normal demand-driven inflation | Raise rates to cool spending | Inflation falls as demand contracts |

| Supply-shock inflation (current) | Raise rates: suppresses demand without addressing supply cause | Inflation may persist while unemployment accelerates |

| Supply-shock inflation (current) | Cut rates: supports employment but may embed inflation | Labour market stabilises but inflation expectations drift higher |

Kashkari stated publicly on 3 May that he could not assure markets a cut was forthcoming, nor rule out a hike, a formulation that captures the bind precisely.

This is not institutional indecision. It is a logical consequence of tools designed for one type of problem being applied to another.

The Treasury-Fed split and what Bessent’s optimism ignores

Treasury Secretary Scott Bessent appeared on Fox News Sunday on 3 May and argued that energy prices would fall sharply after the conflict’s resolution, citing futures markets and U.S. export capacity as supporting evidence.

Bessent projected that post-conflict oil prices would be substantially below start-of-year levels and below any point in the 2020-2025 period.

The confidence is notable. It rests on a specific view: that U.S. naval operations preventing Iran from extracting Hormuz transit tolls, combined with American energy export capacity, will produce a structural decline in global energy costs once the military situation resolves. Futures markets, as Bessent noted, were already pricing in some degree of normalisation.

The Fed cannot share that confidence, and the market signals suggest investors cannot either. The 2-year Treasury yield at approximately 3.89% and the 10-year at approximately 4.39% reflect a term premium that has not collapsed in the way it would if investors fully believed in the rapid normalisation scenario. CME FedWatch data shows a 94.9% probability of a hold at the June 2026 meeting, not a cut.

Three structural constraints limit how quickly Bessent’s scenario could materialise:

- Shipping infrastructure bottlenecks: Rerouted global shipping cannot reverse overnight; port capacity and insurance premiums adjust with lag

- Supply chain normalisation lag: The six-month estimate means physical goods flows do not respond to diplomatic announcements

- Iran’s uncertain compliance: Any post-conflict arrangement depends on enforcement mechanisms that have not been negotiated

The gap between Treasury’s forward-looking optimism and the Fed’s data-dependent caution is itself informative. Markets pricing a near-certain June hold are telling investors which institution they find more credible on timing.

What Fed uncertainty means for rate-sensitive portfolios right now

A prolonged hold at 3.5%-3.75% with no clear directional signal changes the valuation environment for rate-sensitive assets. The 2-year yield at approximately 3.89% and the 10-year at approximately 4.39% produce a spread of roughly 50 basis points, a curve that is neither inverted nor steeply positive. Where it moves from here carries signal: widening would suggest the market is pricing in an eventual cut; flattening or inversion would suggest the market sees hikes as the more likely next move.

| Asset class | Prolonged hold | Surprise hike | Surprise cut |

|---|---|---|---|

| Long-duration bonds | Range-bound; carry attractive at current yields | Capital losses as yields rise | Capital gains as yields fall |

| REITs and utilities | Stable but capped; yield competition from cash | Underperform as discount rates rise | Outperform as rate-sensitive sectors re-rate |

| Growth equities | Valuation multiples compressed but stable | Further multiple compression | Multiple expansion |

| Cash and short-duration | Attractive real yield; optionality preserved | Yields rise further; cash position rewarded | Yields fall; opportunity cost of staying short |

In a genuine hold-with-no-clear-direction environment, the asymmetry of risk shifts. The cost of being wrong on rate direction is higher than in a clear cutting or hiking cycle. Three leading indicators will determine whether the current paralysis breaks:

A barbell approach to inflation positioning, pairing defensive commodity hedges with exposure to AI and technology growth engines, has emerged as one framework for navigating the simultaneous presence of a near-term supply shock and the longer-run disinflationary forces that AI productivity gains and Chinese manufacturing overcapacity are generating beneath the surface.

- The next PCE print: Any move toward 3% or below would give the committee room to lean dovish; any move above 3.5% strengthens the hawkish faction

- Iran diplomatic developments: A credible ceasefire or reopening of the Strait of Hormuz would relieve the supply-side pressure that is driving the Fed’s bind

- The June 2026 FOMC meeting: With 94.9% probability of a hold already priced, the statement language and any dissent shifts will carry more signal than the rate decision itself

The Fed’s credibility is the real variable in play

The Iran conflict has not simply created a policy problem for the Federal Reserve. It has created a communication credibility problem. The April statement retained cut-leaning language that three of four dissenters opposed. The forward guidance points in a direction the committee’s own vote does not support. The incoming chair holds preferences the current data does not accommodate.

This second-order damage, the gap between what the Fed says and what its own members believe, persists even after the geopolitical trigger resolves. Warsh will inherit a committee that has publicly disagreed with each other, a 3.5% PCE reading, and a market that has priced in paralysis with a 94.9% probability of a June hold. Any early policy signal from the new chair carries a credibility cost the old chair’s statement already imposed.

The June FOMC meeting is the next data point that will either restore some directional clarity or extend the uncertainty. Markets have already placed their bet on which outcome is more likely.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Fed policy direction are speculative and subject to change based on economic data, geopolitical developments, and committee composition.