Why 68% of Australian CFD Traders Lose, and What 2027 Changes

3 hrs ago

Nearly 70% of retail CFD traders lose money, according to FCA-regulated broker disclosures in 2026. The mechanism responsible for most of those losses is not poor stock selection or bad timing. It is leverage.

Contracts for difference (CFDs) are available across equities, forex, indices, and commodities, but the leverage embedded in every trade is what makes them categorically different from buying the underlying asset outright. Intermediate traders who understand the product’s basic structure often underestimate how quickly leveraged exposure compounds both gains and losses. A 5% price move against a leveraged position does not produce a 5% loss on the capital deployed; it can produce a 25% loss, or worse.

What follows is a complete breakdown of how CFD leverage and margin work, using concrete numbers to make the mechanics tangible. It then explains how position sizing, margin calls, and risk management tools interact, and where geographic restrictions shape what leverage retail traders can actually access.

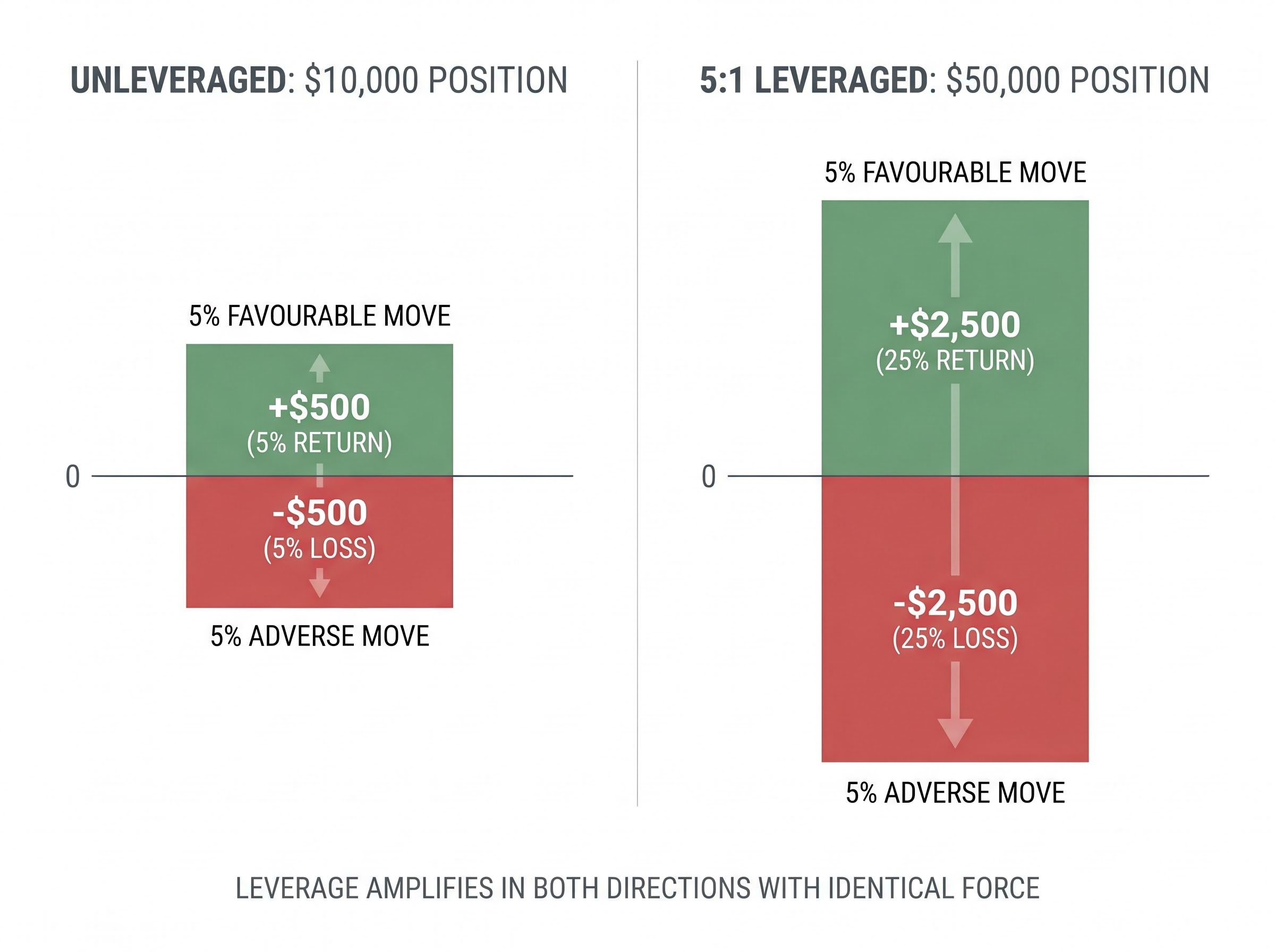

Consider a trader with $10,000 in capital who buys an asset directly. If the asset rises 5%, the gain is $500. If it falls 5%, the loss is $500. The trader captures only the raw price movement against their full capital outlay.

Leverage changes the arithmetic. A broker offering 5:1 leverage allows that same $10,000 to control a $50,000 notional position. The broker extends additional exposure beyond the deposited amount, with the deposit (called margin) acting as collateral for that extension.

The same 5% favourable move now produces a $2,500 gain, a 500% improvement in return on capital deployed. The same 5% adverse move produces a $2,500 loss.

| Scenario | Unleveraged ($10,000 position) | 5:1 Leveraged ($50,000 position) |

|---|---|---|

| 5% favourable move | +$500 (5% return on capital) | +$2,500 (25% return on capital) |

| 5% adverse move | -$500 (5% loss on capital) | -$2,500 (25% loss on capital) |

The symmetry is the point. Leverage amplifies in both directions with identical force.

Leverage does not change the probability of the price moving in your favour. It changes the size of the consequence when it does, or does not.

Margin is the percentage of the total notional position value a trader must hold as a deposit to open and maintain the trade. It is the cost of accessing leveraged exposure, expressed as a fraction of the full position.

The relationship between margin rate and leverage ratio is an inverse mathematical one: they are reciprocals. A 5% margin requirement means the trader deposits one-twentieth of the position, producing 20:1 leverage. A 3.3% margin requirement produces approximately 30:1 leverage. A broker quoting “5% margin” and a broker quoting “20:1 leverage” are saying the same thing in different languages.

Under current regulatory caps, margin requirements vary by asset class:

| Asset class | Margin rate | Leverage ratio | Notional exposure from $1,000 |

|---|---|---|---|

| Major forex pairs | 3.3% | 30:1 | $30,000 |

| Major indices | 5% | 20:1 | $20,000 |

| Commodities (ASIC) | 6.7% | 15:1 | $15,000 |

| Individual shares | 20% | 5:1 | $5,000 |

| Cryptocurrencies | 50% | 2:1 | $2,000 |

A distinction exists between initial margin (required to open the position) and maintenance margin (the minimum equity level required to keep it open). The difference between the two creates a buffer, but that buffer can erode rapidly in volatile conditions.

CFD margin is structurally distinct from margin lending mechanics in that no interest rate applies to the borrowed notional amount; instead, the cost of leverage in CFDs is embedded in overnight financing charges, making the two products superficially similar but economically different in how they meter the cost of sustained leveraged exposure.

A margin call is a notification triggered when account equity drops to a level where used margin is no longer adequately covered. The margin level, calculated as equity divided by used margin and expressed as a percentage, is the metric platforms use to monitor this threshold. A margin call is typically issued when margin level falls below 100%.

If a trader does not deposit additional funds or reduce positions, automated closure begins. Most platforms start liquidating positions, often beginning with the largest or most loss-making, when margin level hits the broker’s close-out threshold (commonly 50%).

In fast-moving markets, slippage can mean positions are closed at worse prices than the margin call threshold implies. The close-out price is not guaranteed.

Leverage ratios describe the amplification available. Unit count determines how much amplification a trader actually takes on. CFD positions are sized in units, where each unit typically represents one share (or equivalent denomination) of the underlying asset.

The margin calculation combines three inputs:

A stock priced at $100, with a position of 200 units and a 20% margin rate, requires $4,000 in margin to control a $20,000 notional position. Each $1 price move produces a $200 gain or loss, because the trader holds 200 units. This is the conceptual equivalent of purchasing 200 shares directly, without the $20,000 capital outlay.

Working backwards from a maximum acceptable loss to the correct unit count is a more disciplined entry method than starting with a position size and hoping for the best.

If a trader determines that the maximum acceptable loss on any single trade is $600, and the stop-loss is placed $3 below the entry price, the appropriate position size is 200 units ($600 divided by $3). The unit count is derived from the risk budget, not selected independently of it.

A 5% adverse move on a 5:1 leveraged position consumes 25% of the deposit. A 20% adverse move, which is well within the range of a volatile individual equity over a matter of weeks, would consume the entire deposit and then some.

Without a stop-loss in place, or if a stop-loss is breached during a price gap, losses on a leveraged CFD position can exceed the initial deposit. This is the scenario negative balance protection was designed to address. Under ESMA, FCA, and ASIC rules (in effect since 2018), retail trader losses are capped at the deposited amount, meaning brokers absorb the excess.

The empirical data on how frequently leveraged CFD trading results in net losses for retail participants is consistent across jurisdictions:

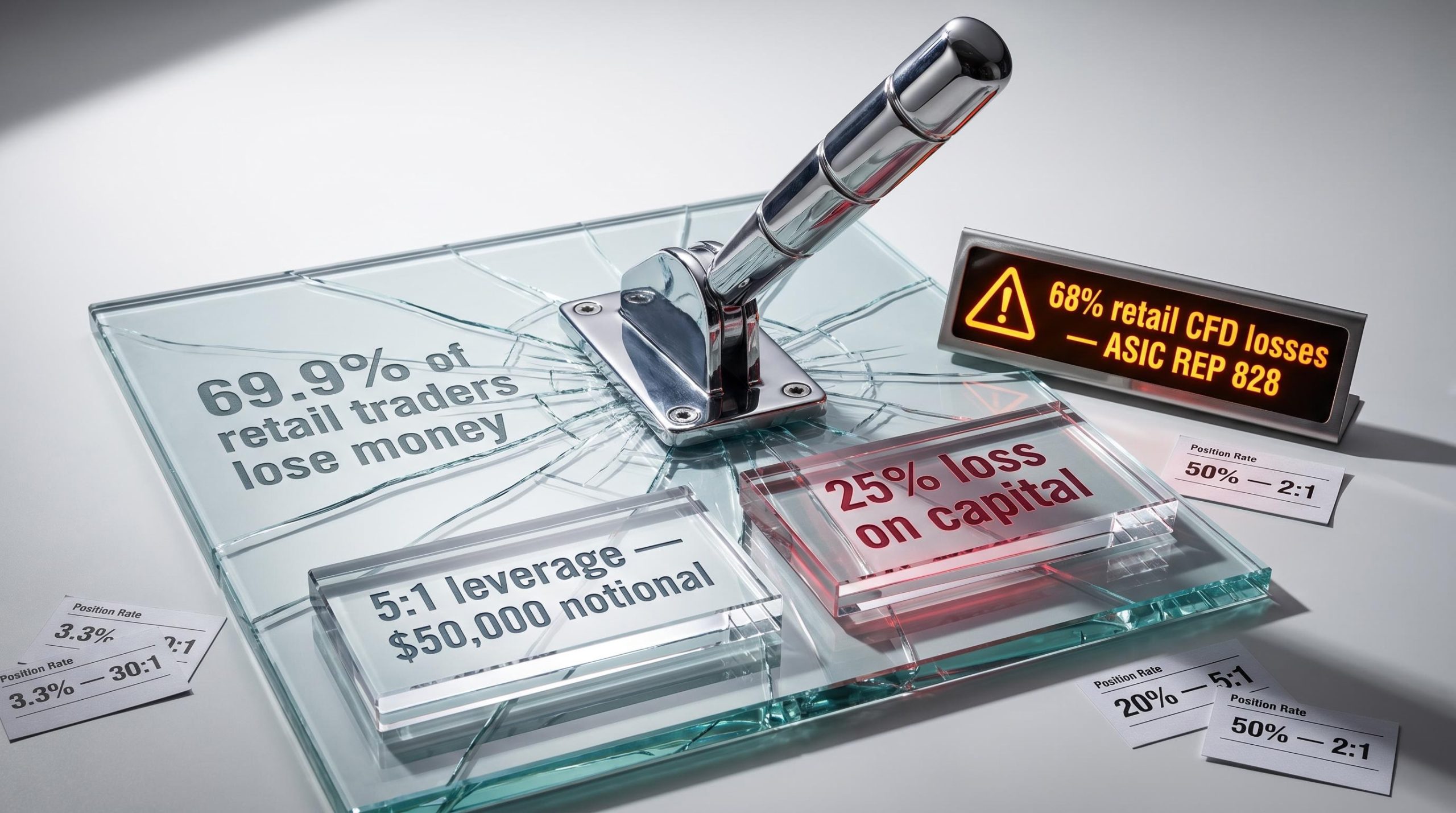

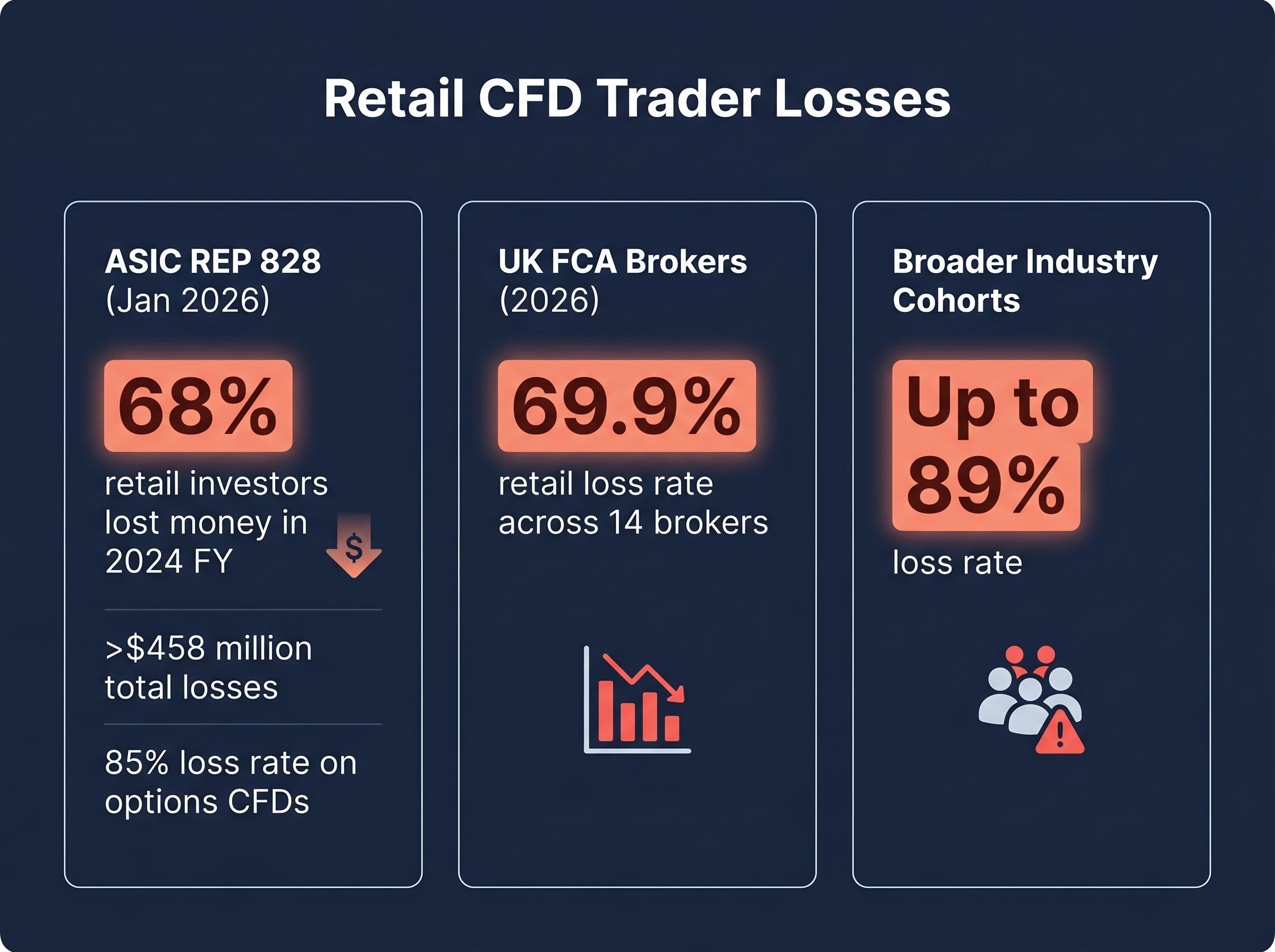

In the 2024 financial year, 68% of retail CFD investors lost money, with total losses exceeding $458 million, according to ASIC REP 828.

These are not hypothetical projections. Negative balance protection sets a hard floor under retail losses, but it does not prevent an account being reduced to zero.

The same ASIC REP 828 data cited here sits inside a broader picture: reactive trading patterns among retail investors, including position entries and exits driven by short-term volatility rather than a defined risk framework, are a documented contributor to the aggregate loss figures that regulators track each financial year.

ASIC REP 828, published in January 2026, documented these outcomes through a sector-wide review of CFD issuers, finding multiple brokers in breach of distribution obligations and securing nearly $40 million in refunds for affected retail clients.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The loss statistics carry weight. So does the fact that specific tools exist to narrow the range of possible outcomes on any given trade. The following five tools are listed in order from basic to most protective:

The standard stop-loss is the most widely used, but it carries a core limitation: execution is not guaranteed at the specified price if the market gaps through that level. A stock that closes at $100 on Friday and opens at $94 on Monday will skip past a stop-loss set at $97.

GSLOs address that gap risk directly. Where a standard stop is free but subject to slippage, a GSLO guarantees execution at the specified price, regardless of how far the market moves between price ticks. The trade-off is a broker-charged premium, typically only applied if the order is triggered.

Traders should verify GSLO availability and cost on their specific platform before assuming this protection is standard. Not all brokers offer GSLOs across all asset classes.

In the United States, CFDs are entirely prohibited for retail traders by the SEC and CFTC. This prohibition has remained unchanged as of 2026.

In the United States, CFDs cannot legally be offered to retail traders at all. This is not a leverage limit. It is a product ban.

Outside the US, the product is available but subject to jurisdiction-specific leverage caps. ESMA, FCA, and ASIC impose broadly similar frameworks, with one notable variation in commodities:

| Asset class | ESMA cap | FCA cap | ASIC cap |

|---|---|---|---|

| Major forex pairs | 30:1 | 30:1 | 30:1 |

| Non-major forex, gold, major indices | 20:1 | 20:1 | 20:1 |

| Commodities, non-major indices | 10:1 | 10:1 | 15:1 |

| Individual equities | 5:1 | 5:1 | 5:1 |

| Cryptocurrencies | 2:1 | 2:1 | 2:1 |

In Singapore, the MAS caps most CFDs at 20:1 maximum leverage for retail traders. ESMA issued a formal reminder in February 2026 reaffirming CFD firm obligations under product intervention measures. ASIC’s January 2026 sector review found multiple brokers in breach of leverage limits, securing nearly $40 million in refunds.

ESMA’s CFD product intervention measures, reaffirmed in a February 2026 public statement, cover leverage limits, mandatory margin close-out rules, negative balance protection, and standardised risk warnings that all EU-authorised CFD firms must apply to retail accounts.

Leverage figures of 100:1 for forex that appear in generic educational materials are non-compliant for retail traders under current ESMA, FCA, and ASIC rules. A trader accessing leverage beyond these caps may be relying on a non-compliant or offshore broker, which carries counterparty risk beyond the leverage itself.

The core insight across every section of this article is the same: leverage determines how much of a price move is captured per unit of capital deployed. It does not increase the probability of a price move going in the trader’s favour.

The three variables that define a leveraged CFD trade are not independent choices. They form an interconnected system:

Adjusting one variable without recalibrating the other two changes the risk profile of the trade in ways that may not be immediately obvious. The question is not “how much leverage can I access?” but “how much leverage is consistent with a position size that keeps any single trade’s maximum loss within an acceptable percentage of my account?”

The regulatory loss rates, 68% under ASIC and 69.9% across FCA-regulated brokers, are empirical evidence that maximum leverage is not optimal leverage. Negative balance protection prevents losses from exceeding the deposit, but it does not prevent the deposit from reaching zero.

Regulatory caps define the maximum leverage available. How much of that maximum you actually use is the only leverage decision that is entirely yours.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

CFD leverage allows traders to control a much larger notional position than their deposited capital, for example 5:1 leverage means $10,000 controls a $50,000 position. This amplifies both gains and losses proportionally, so a 5% adverse price move produces a 25% loss on the capital deployed.

A margin call is triggered when account equity falls to a level where the used margin is no longer adequately covered, typically when the margin level drops below 100%. If additional funds are not deposited or positions reduced, the broker will begin automatically closing positions, often starting with the largest or most loss-making ones.

Under current FCA and ASIC rules, retail traders are capped at 30:1 for major forex pairs, 20:1 for major indices, 5:1 for individual equities, and 2:1 for cryptocurrencies. CFDs are entirely prohibited for retail traders in the United States by the SEC and CFTC.

According to ASIC REP 828 published in January 2026, 68% of retail CFD investors lost money in the 2024 financial year with total losses exceeding $458 million. FCA-regulated broker disclosures in 2026 show a 69.9% retail loss rate across 14 brokers.

Key risk management tools include standard stop-loss orders, trailing stop-losses, position sizing calculators, and guaranteed stop-loss orders (GSLOs) which ensure execution at a specified price even if the market gaps. Negative balance protection, mandatory under ESMA, FCA, and ASIC rules, also ensures retail traders cannot lose more than their deposited amount.