Why 68% of Australian CFD Traders Lose, and What 2027 Changes

3 hrs ago

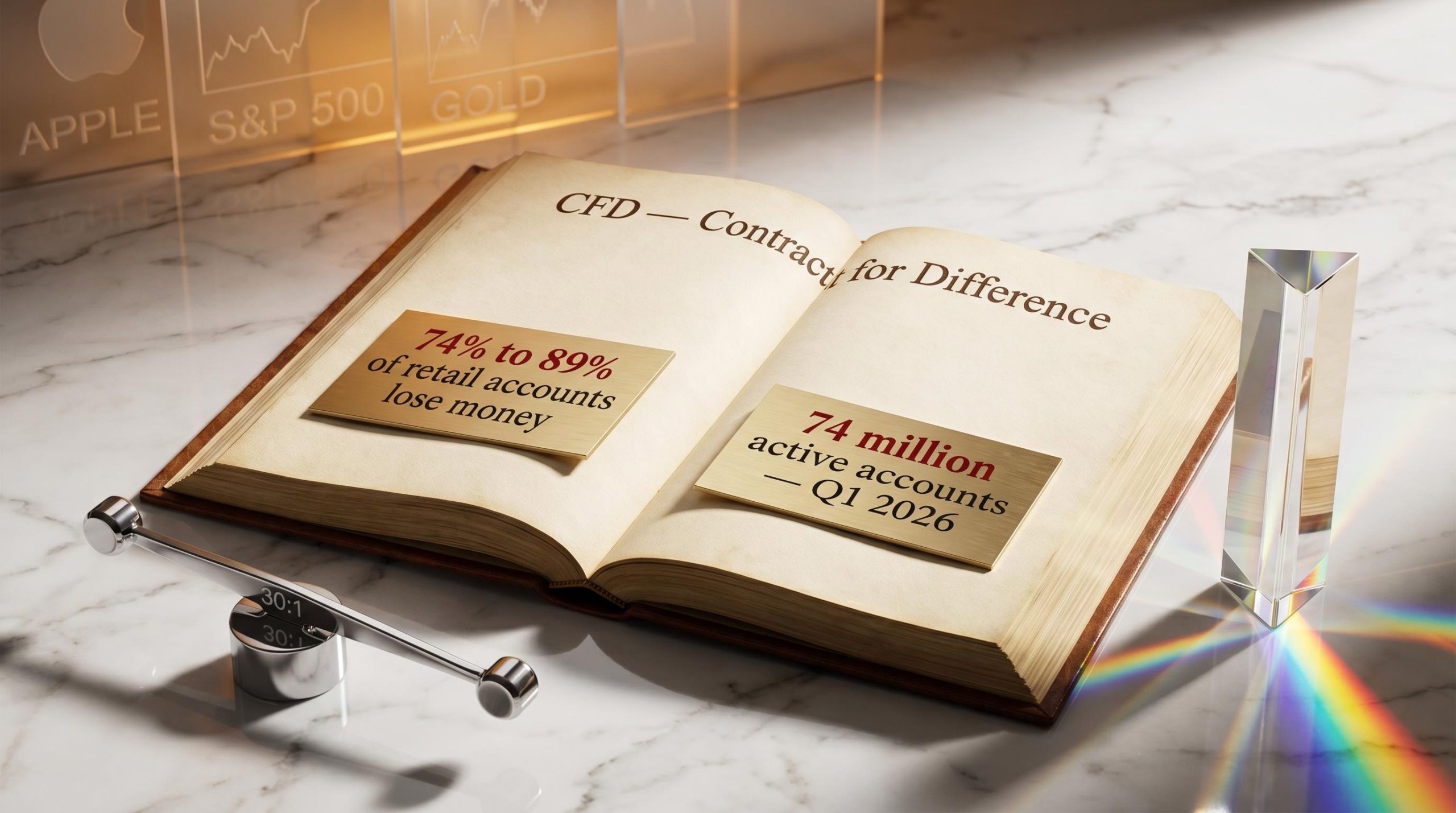

Between 74% and 89% of retail accounts that trade CFDs lose money, according to ESMA data from Q1 2026. Yet CFDs remain one of the most widely used trading instruments in the world, with approximately 74 million active retail accounts globally. That gap between popularity and outcomes begins with a knowledge deficit. Brokers market CFDs as a simple way to trade almost anything, from Apple stock to crude oil, without owning the underlying asset. What that means structurally, and why it matters for risk, is rarely explained clearly to beginners. This guide explains what a CFD is at a structural level, how leverage and margin actually work (including the multiplicative loss relationship most beginners misunderstand), what it means to have no ownership in the underlying asset, and what the global regulatory picture looks like for retail traders in 2026.

A CFD is not a purchase. It is a contract between a trader and a broker to exchange the difference in an asset’s price between the moment the contract opens and the moment it closes. No asset changes hands. No shares are transferred. No barrels of oil move.

“A CFD is an agreement to exchange the price difference of an asset, not the asset itself.”

The word “derivative” describes this structure precisely: the instrument derives its value from something else, a share, an index, a commodity, without granting any claim on that thing. A trader holding a CFD on Apple shares has exposure to Apple’s price movement but owns nothing that Apple itself has issued.

The counterparty in every CFD transaction is the broker or CFD provider directly, not another market participant on an exchange. This makes the relationship structurally different from buying shares through a stock exchange, where the trade is matched with another buyer or seller. Brokers may hedge their own aggregate exposure by trading the actual underlying assets on the back end, but the client-facing relationship remains purely contractual.

CFDs cover a broad range of underlying asset classes:

Understanding the contractual rather than ownership nature of a CFD is the foundational insight that makes every other aspect of CFD risk, from leverage to margin calls, comprehensible.

The broker facilitates the trade. The broker also earns from it. These two facts sit together, and understanding how they interact shapes what every position actually costs.

CFD providers generate revenue primarily through the spread: the gap between the bid price (the price at which the broker will buy) and the ask price (the price at which the broker will sell) on any given instrument.

Consider a simple example. If a stock CFD shows a bid of 480 and an ask of 481, the spread is 1 unit. A trader opening a long position enters at 481 but would only be able to close immediately at 480. The position is in a small loss from the moment it opens, equal to the spread, before any price movement occurs.

The three main revenue sources for a typical CFD broker are:

For short-duration trades, spread costs relative to position size can be proportionally significant. This is a built-in cost, not a neutral transaction fee.

“Counterparty” means the broker takes the other side of the trade. When a trader goes long, the broker’s contractual position is short, and vice versa. This creates a structural tension: the broker’s profit on one side of the trade is the trader’s loss on the other.

Regulated brokers, such as UK-based CMC Markets and IG Markets, manage this through internal hedging policies, offsetting their aggregate client exposure in the underlying market. The conflict of interest implied by counterparty positioning is managed under regulatory frameworks, but not eliminated entirely. This is one reason broker regulatory status matters: unregulated counterparties carry meaningfully higher risk. Cost transparency rules remain a current focus of regulatory scrutiny across major jurisdictions.

On a trading screen, a CFD position on Apple and a holding of Apple shares can look remarkably similar. Both show a price. Both move with the market. The similarity ends there.

Direct share ownership represents a proportional claim on company assets. Shareholders hold voting rights, receive dividends, and have legal standing in relation to the company. A CFD position carries none of these rights. The trader holds a contractual agreement with a broker, not a stake in a company.

Dividend treatment illustrates the distinction clearly. When Apple pays a dividend, shareholders receive it as income. CFD brokers typically credit or debit a dividend adjustment to reflect the event, but this is a contractual adjustment between broker and trader, not a dividend entitlement from the company.

CFDs do offer a practical benefit that direct ownership does not always provide. A trader based outside the United States can access US-listed stocks through CFDs without needing foreign currency accounts or direct access to overseas exchanges. This accessibility is part of what drives the instrument’s global popularity.

The structural differences between the two are summarised below.

| Feature | CFDs | Direct share ownership |

|---|---|---|

| Asset ownership | No | Yes |

| Leverage available | Yes (heavily regulated) | Limited (margin accounts only) |

| US retail access | Prohibited | Available |

| Margin call exposure | Yes | Not in standard cash accounts |

| Retail loss rate (approximate) | 74-89% | No equivalent universal figure |

“CFDs are prohibited for US retail investors and treated as securities requiring registration that CFD structures do not satisfy.”

For a beginner deciding between a CFD platform and a brokerage account, the question is straightforward: price exposure or ownership. The answer determines which instrument is appropriate.

The ETF ownership structure sits at the opposite end of the spectrum from a CFD: ETF investors hold actual units in a fund that tracks an underlying index or asset basket, giving them a proportional claim on those holdings rather than a contractual price agreement with a broker.

Leverage is the mechanic that makes CFDs both attractive and dangerous. Understanding it requires starting with the arithmetic, not the warnings.

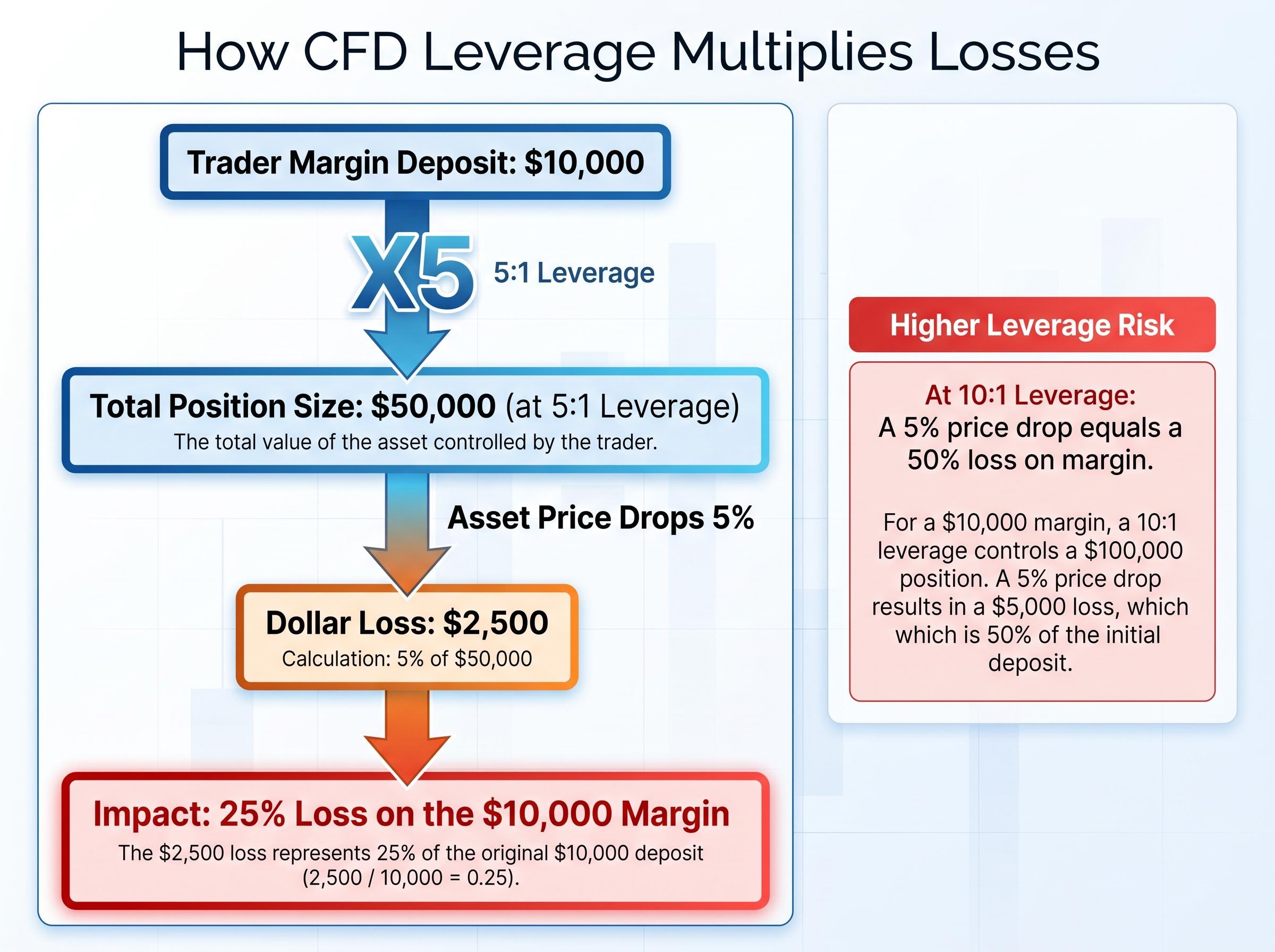

Leverage is the ratio of total position exposure to the margin (the deposit) required to hold that position. Margin is the minimum capital a broker requires to open and maintain a leveraged position.

Here is how it works in practice:

The relationship is multiplicative. Loss percentage on margin equals the leverage ratio multiplied by the asset’s price movement percentage.

“Loss on margin = leverage ratio x asset price movement percentage.”

At 10:1 leverage, that same 5% price drop produces a 50% loss on margin. The arithmetic is consistent across all leverage ratios, and it is the single most important mechanical concept in CFD trading.

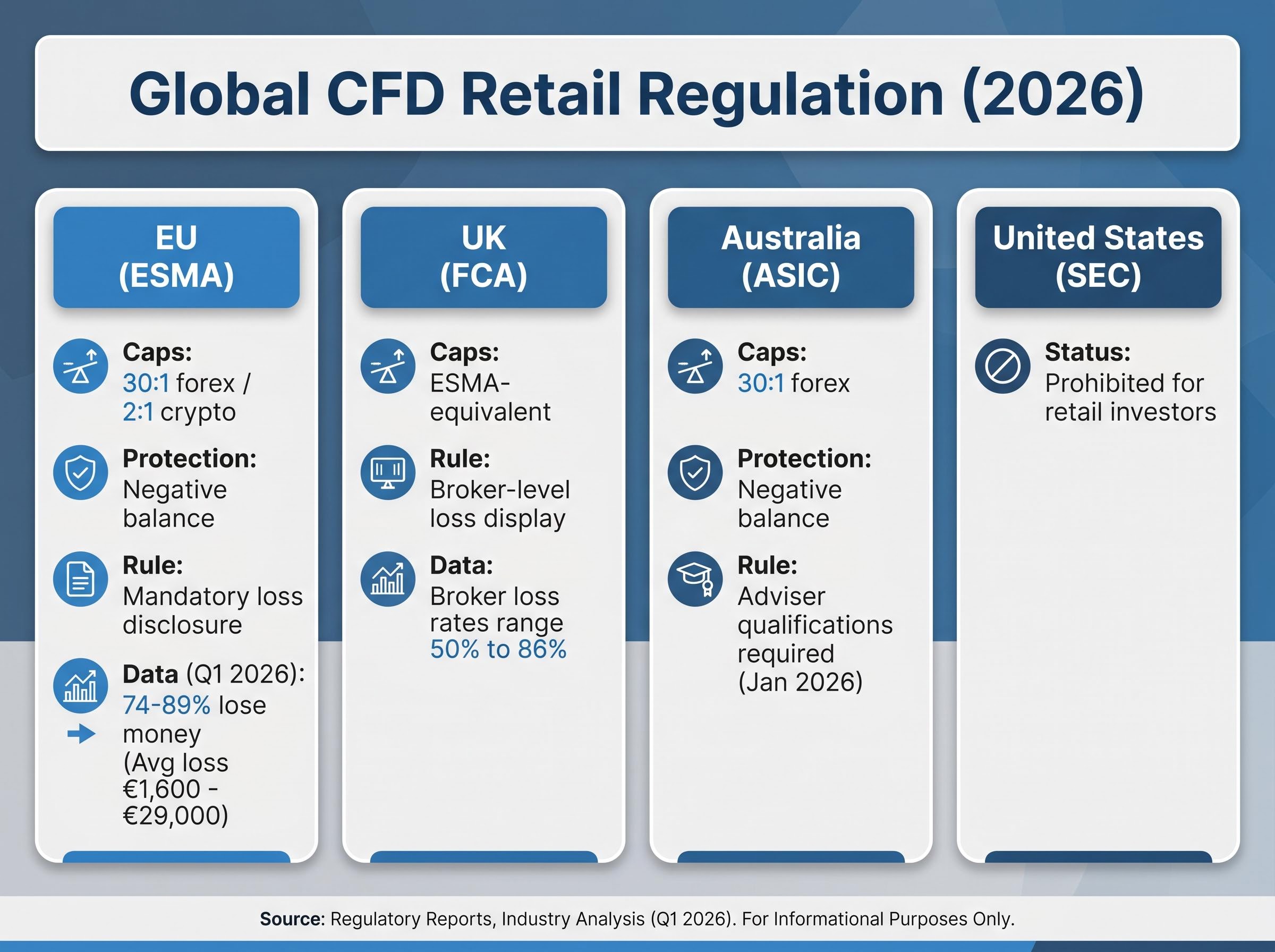

Retail leverage caps under current regulation set the upper limits: 30:1 for major forex pairs (under ESMA, FCA, and ASIC rules), scaling down to 2:1 for cryptocurrencies under ESMA rules.

When a position moves against the trader, account equity declines. When it falls below the broker’s defined margin threshold, the broker issues a margin call.

Trading 212, for example, currently initiates a margin call when account status drops below 45%. If the call is not addressed, the broker closes positions automatically, typically on a first-in-first-out basis. Thresholds vary by broker, but the principle is consistent.

Automatic liquidation can lock in losses at the worst moment in a fast-moving market, before the trader has time to respond or add funds. For a beginner, internalising the multiplicative loss relationship before placing a first leveraged trade is far more effective than learning it from a margin call notification.

The margin lending mechanics that govern LVR thresholds and margin call timelines in traditional share lending follow a similar logic to CFD margin requirements, but the regulatory framework, cost structure, and forced-liquidation triggers differ in ways that matter for any investor comparing leveraged instruments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Regulation is not a formality. It is the difference between a broker that is required to protect retail clients and one that is not. The major regulatory regimes each impose specific obligations on CFD providers.

| Jurisdiction | Regulator | Key retail protections |

|---|---|---|

| European Union | ESMA | Leverage caps (30:1 forex to 2:1 crypto), negative balance protection, mandatory loss rate disclosure |

| United Kingdom | FCA | ESMA-equivalent leverage caps, mandatory broker-level retail loss rate display |

| Australia | ASIC | 30:1 leverage cap for forex, negative balance protection, new adviser qualification requirements (January 2026) |

| United States | SEC | CFDs prohibited for retail investors; treated as unregistered securities |

The mandatory retail loss rate disclosures required in the EU and UK are regulatory instruments designed to be read, not legal boilerplate. Current ESMA figures show that between 74% and 89% of retail CFD accounts lose money, with average losses ranging from €1,600 to €29,000 per client.

ESMA’s product intervention opinion on CFDs found that between 74% and 89% of retail clients lose money trading the instrument, with some individual distributors recording retail loss rates as high as 90%, a finding that underpins the leverage caps and mandatory disclosure rules now applied across EU member states.

“Between 74% and 89% of retail CFD accounts lose money, with average losses ranging from 1,600 euros to 29,000 euros per client (ESMA, Q1 2026).”

These figures represent a regulatory position on product suitability, not merely a disclaimer. Individual FCA-regulated brokers display their own loss rates, which range from 50% to 86% depending on the broker and asset class.

ASIC introduced new adviser qualification requirements effective January 2026, affecting how CFD products can be recommended in Australia. Across all three active regulatory regimes (EU, UK, Australia), the direction is consistent: tighter disclosure, lower leverage, and explicit warnings about retail suitability.

For a beginner choosing a broker, regulatory status is a practical filter. A regulated broker is required to disclose how many of its clients lose money. An unregulated one is not.

CFDs are designed for short-term price speculation, not investment or asset accumulation. Both ESMA and the FCA explicitly assess them as unsuitable for most retail investors. That assessment is based on the data, not on opinion.

A beginner considering CFDs should work through a preparation checklist before committing capital:

The five most actively traded CFD asset classes in 2026 provide a practical starting point for understanding where retail activity concentrates:

The global active retail CFD account count reached approximately 74 million in Q1 2026. This is a mainstream product category, but the loss rate data across individual FCA-regulated brokers, ranging from 50% to 86%, makes the risk profile clear. Any decision to open a CFD account is better made as an informed one than a reactive one.

For investors wanting to place the CFD cost structure in a wider context, our full explainer on the real cost of leveraged investing examines how variable margin lending rates above 10% per annum in Australia compound the return hurdle that any leveraged position must clear, with worked comparisons across different leverage scenarios.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A CFD is a price agreement, not an asset. Every risk associated with it, from leverage amplification to margin calls, from the counterparty relationship to the absence of ownership rights, flows from that foundational fact.

Regulatory environments in the EU, UK, and Australia provide meaningful protections for retail clients. Leverage caps, negative balance protection, and mandatory loss rate disclosures are real safeguards. They do not, however, change the underlying mechanics of the instrument. A 30:1 leverage cap still permits a 5% price move to produce a 150% loss on margin.

Understanding what CFDs are at a structural level is the prerequisite for deciding whether they belong in a trading strategy at all. For those who decide the answer is yes, that same structural understanding is what separates informed position sizing from the outcomes reflected in the 74-89% retail loss rate. The knowledge comes first. The account comes after.

A CFD (Contract for Difference) is a contract between a trader and a broker to exchange the difference in an asset's price between when the contract opens and when it closes. No asset is purchased or transferred; the trader gains price exposure without owning the underlying share, commodity, or index.

Leverage allows a trader to control a larger position than their deposited margin; at 5:1 leverage, a $10,000 deposit controls a $50,000 position, meaning a 5% price drop produces a 25% loss on the margin, not a 5% loss. This multiplicative relationship is the most important mechanical concept beginners need to understand before trading CFDs.

According to ESMA data from Q1 2026, between 74% and 89% of retail CFD accounts lose money, with average losses ranging from 1,600 euros to 29,000 euros per client. Individual FCA-regulated brokers report retail loss rates ranging from 50% to 86% depending on the broker and asset class.

No, CFDs are prohibited for retail investors in the United States and are treated by the SEC as unregistered securities that CFD structures do not satisfy. Retail traders in the US cannot legally access CFD products through regulated channels.

Beginners should use a demo account first to understand how positions, margin, and leverage interact without financial risk, verify the broker holds authorisation from a recognised regulator such as the FCA, ESMA, or ASIC, and read the mandatory retail loss rate disclosure on the broker's platform as genuine guidance before committing any capital.