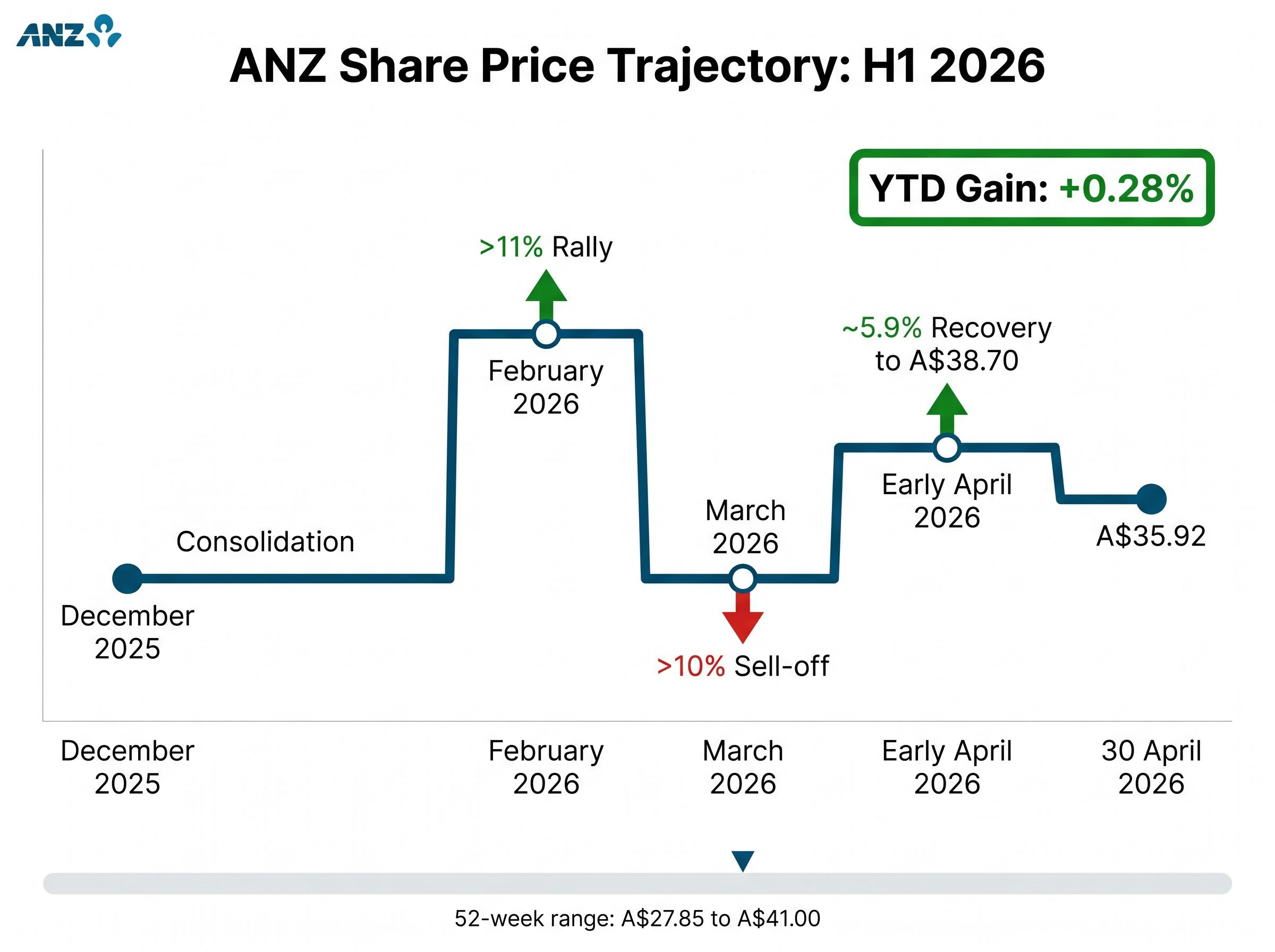

ANZ shares have traced a 20-percentage-point arc since December, swinging from a post-earnings high near A$41.00 to a March trough below A$30, then clawing back to A$35.92 as of 30 April 2026. The net result: a year-to-date gain of +0.28%. All that movement, and the stock is almost exactly where it started.

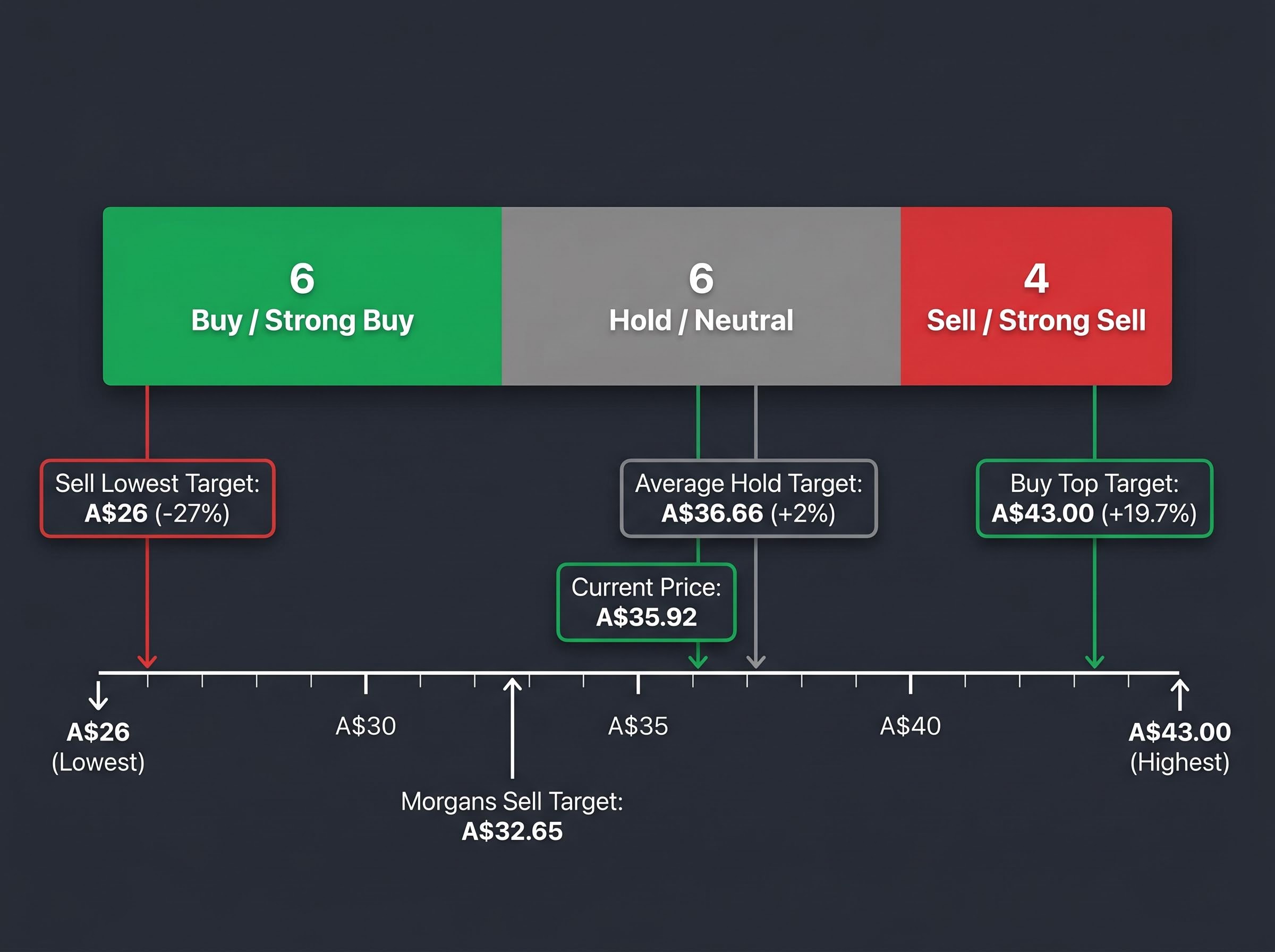

The 14 analysts covering ANZ are split into three nearly equal camps, with six rating the stock a buy, six a hold, and four a sell. The average 12-month price target of A$36.66 implies roughly 2% upside from today’s close, while the widest targets range from A$26 to A$43. With the Reserve Bank of Australia (RBA) set to announce its rate decision on 5 May 2026, and ANZ economists flagging a possible hike to 4.35%, retail investors face a genuinely contested picture: a Q1 cash profit that beat expectations by a wide margin, a consensus target that offers little buffer, and a macro catalyst that could shift the earnings trajectory within days.

What follows unpacks the split broker consensus, explains how a rate hike flows through to bank profitability, and offers a framework for weighing conflicting analyst signals when evaluating financial stocks.

Four months of sharp moves, and ANZ shares are almost where they started

The price chart tells a story of whiplash. Since December, ANZ has moved through five distinct phases, each driven by different forces, yet the stock sits almost exactly where it began the year.

52-week range: A$27.85 to A$41.00

The key moves, in sequence:

- December 2025: Shares traded in a narrow range, consolidating after the FY25 reporting cycle.

- February 2026: The Q1 trading update triggered a rally of more than 11%, with shares ending the month roughly 9% higher.

- March 2026: A sector-wide sell-off dragged ANZ down more than 10%, driven by geopolitical tensions, elevated fuel costs, and trade-related uncertainty.

- Early April 2026: A partial recovery of approximately 5.9% over two weeks lifted shares back toward A$38.70.

- Mid-to-late April 2026: Shares softened again to A$35.92, with no company-specific catalyst behind the decline.

That last point matters. The April slide from A$38.70 to A$35.92 was not triggered by an earnings miss, a guidance downgrade, or a management change. It was macro noise acting on a stock that had already absorbed a significant fundamental positive. A year-to-date return of +0.28% after that sequence is not stability; it is the residue of forces pulling in opposite directions.

When big ASX news breaks, our subscribers know first

A Q1 earnings result that should have settled the debate, but did not

By most conventional measures, ANZ’s first-quarter result was strong enough to shift the narrative. The numbers told a clear story of margin improvement and disciplined cost management at a time when the sector needed both.

- Cash profit: A$1.94 billion, up 75% year-on-year relative to the FY25 half-average

- Revenue: Up 1% quarter-on-quarter

- Net interest margin (NIM): 1.56%, up 2 basis points quarter-on-quarter

The 2-basis-point NIM improvement may appear modest in isolation, but it represents active margin expansion heading into a potentially higher-rate environment. Combined with cost discipline (FY26 cost guidance held at approximately A$11.5 billion, per Morgans’ 6 April 2026 note) and lower impairments, the result gave bulls a credible foundation.

The share price response was immediate. ANZ surged more than 11% in the days following the February release, a move that priced in a genuine reassessment of earnings quality.

Why the February rally did not last

Within weeks, the gains were gone. The March sell-off erased more than 10% of ANZ’s value, and the drivers were entirely external: geopolitical tensions, elevated fuel costs, and trade-related uncertainty swept through the banking sector broadly.

The April softness that followed was similarly disconnected from ANZ-specific announcements. This pattern, strong fundamentals overwhelmed by macro headwinds, is the central tension in the current investment case. Is the stock cheap because the market is mispricing a solid earnings story, or cheap because broader risks have not yet flowed through to the next quarterly result?

How interest rates move through a bank’s earnings (and what the May RBA decision means for ANZ)

Before assessing the RBA’s potential impact, the transmission mechanism itself is worth understanding. It determines the size and timing of any earnings benefit.

Net interest margin (NIM) is the spread between what a bank earns on its loans and what it pays on deposits, expressed as a percentage of interest-earning assets. A wider spread means more profit per dollar lent.

When the RBA raises the cash rate, banks typically reprice variable-rate loans quickly, often within days. Deposit rates, however, tend to move more slowly and by smaller increments. This gap between loan repricing speed and deposit repricing speed is what drives NIM expansion in a rising-rate environment.

The transmission is not instantaneous, and it varies by bank depending on the mix of fixed versus variable loans, the proportion of low-cost transaction deposits, and competitive pressures on savings rates. For ANZ, with a current NIM of 1.56% and a loan book weighted toward variable-rate mortgages, a 25-basis-point hike would create a directional tailwind for margins, though the precise magnitude depends on how aggressively the bank passes through deposit rate increases.

The RBA’s current cash rate sits at 4.10% following the March 2026 hike. The next board meeting runs 4-5 May 2026, with the decision announced on 5 May. Market and bank commentary points to a possible further hike to 4.35%.

| Cash Rate Scenario | Directional NIM Impact | Timing Consideration | Likely Earnings Direction |

|---|---|---|---|

| Hold at 4.10% | Neutral to mildly negative | Existing margin benefits stabilise; no new tailwind | Flat to modest pressure if deposit competition intensifies |

| Hike to 4.35% | Positive (loan repricing leads deposit repricing) | Loan book reprices within weeks; deposit lag of 1-3 months | Supportive for Q2 and H2 margins if deposit pass-through remains partial |

Investors who understand this mechanism can form their own directional view on the earnings impact rather than relying solely on broker estimates that may not yet reflect an additional hike.

Sixteen analysts, three camps: what a deeply split broker consensus actually tells you

A consensus rating of Hold, drawn from 14 analysts, sounds like a clear signal. The distribution beneath it tells a different story.

| Rating Category | Number of Analysts | Implied Move from A$35.92 |

|---|---|---|

| Buy / Strong Buy | 6 | Up to +19.7% (highest target: A$43.00) |

| Hold / Neutral | 6 | Approximately +2% (average target: A$36.66) |

| Sell / Strong Sell | 4 | Down to -27% (lowest target: approximately A$26) |

Morgans maintained its Sell rating on 6 April 2026 with a price target of A$32.65, implying roughly 9.1% downside from the current close. Simply Wall St estimates fair value at A$36.66, suggesting the stock trades at an approximate 10.8% discount to PE-based fair value.

The spread from A$26 to A$43 is not analyst error. It reflects genuine disagreement on a small number of contested assumptions: the persistence of NIM expansion, the credit cycle trajectory, and the macro environment’s impact on loan growth.

Three things a retail investor should extract from any split broker consensus:

- Distribution shape matters more than the average. A 6-6-4 split is a fundamentally different signal from a 12-2-2 split, even if both average out to Hold.

- Target range width signals assumption sensitivity. A A$17 spread between the highest and lowest targets indicates that small changes in rate or credit assumptions produce large valuation differences.

- Peer context adds perspective. All other major Australian banks carry sell or strong sell consensus ratings. ANZ being rated Hold, in relative terms, positions it as comparatively less negatively viewed among the big four.

A practical framework for evaluating ANZ when the signals conflict

Rather than treating the conflicting signals as noise to be averaged out, investors can separate them by type and time horizon. Three categories capture the full picture.

- Momentum signals (near-term). ANZ trades at A$35.92, roughly 12.4% below its 52-week high of A$41.00. The stock has failed to hold above A$38 twice in April. Short-term price action is not confirming the fundamental story, and the consensus target of A$36.66 offers only A$0.74 of upside buffer from current levels.

- Earnings quality signals (medium-term). The Q1 cash profit of A$1.94 billion and NIM expansion of 2 basis points to 1.56% represent a solid fundamental foundation. Cost guidance remains unchanged at approximately A$11.5 billion. These are the numbers the bull case rests on, and they have not deteriorated.

- Macro catalyst signals (near-term, with medium-term implications). The 5 May RBA decision is the single most proximate event capable of shifting the earnings trajectory. A hike to 4.35% would provide a directional NIM tailwind; a hold at 4.10% would remove one leg of the constructive case without invalidating it entirely.

The tension is clear. Earnings quality supports the stock at these levels, but price momentum and the thin upside to consensus targets argue for caution.

The May 5 decision as a near-term litmus test

The RBA announcement functions as a binary test of one leg of the investment case. A hike to 4.35% would validate the rate-driven margin expansion thesis and could provide a catalyst for the stock to re-test the A$38 level. A hold would not destroy the fundamental story, but it would remove the most immediate positive catalyst and shift the earnings improvement timeline further out.

One caution: macro catalysts of this nature are frequently priced in ahead of announcements. If markets have already moved to reflect a high probability of a hike, the announcement itself may not produce further share price gains. The reaction to the decision, rather than the decision itself, will be the more informative signal.

The signals are split because the story is genuinely unresolved

The analyst disagreement on ANZ is not a failure of research. It reflects a stock whose investment case hinges on assumptions that cannot yet be verified.

The bull case is conditional: it requires a rate hike to be confirmed, NIM expansion to continue beyond Q1, and the share price to recover toward the consensus target of A$36.66.

For the constructive case to prove correct, three conditions need to hold:

- The RBA hikes to 4.35% on 5 May, providing a fresh NIM tailwind.

- ANZ’s NIM trajectory of 1.56% and rising holds through the next quarterly update, confirming that margin expansion is durable rather than a one-quarter artefact.

- The share price recovers from A$35.92 toward the consensus target range, closing the gap to the A$36.66 average.

For the bear case, represented by Morgans’ A$32.65 target, to prove correct, macro headwinds need to persist, deposit competition needs to compress the NIM benefit, and the broader sector sell-off needs to resume.

The honest assessment is that neither outcome is assured. Market-implied RBA probabilities and competitor NIM data are not publicly available from verified sources at the time of writing, which means any rate-driven thesis should be treated as directional rather than precise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.