For the first time on record, international ETFs overtook domestic funds as the most purchased ETF category on one of Australia’s largest retail trading platforms during Q1 2026. The data, drawn from the Selfwealth by Syfe Quarterly Investor Pulse published in April 2026, captures more than a product preference shift. It marks a measurable break in a decades-old pattern: Australian retail investors defaulting to the local market.

That default was never accidental. Franking credits, familiarity, and domestic brokerage architecture all reinforced it. Yet across every generational cohort simultaneously, the Q1 2026 data suggests the structural constraint is loosening. What follows is an analysis of what drove that shift, who is leading it, what the macroeconomic environment is adding, and what it means for how Australian retail investors approach international ETFs and portfolio construction right now.

A landmark quarter: international ETFs take the top spot

International ETFs became the most purchased ETF category on the Selfwealth by Syfe platform during Q1 2026, surpassing domestically focused funds for the first time. The shift was not confined to one anomalous month. It held across the entire quarter, surviving a 4.0% decline in total Australian ETF market value during March 2026.

Market-wide data corroborates the platform-level finding.

$6.9 billion was invested into international equity ETFs across the Australian market in Q1 2026, reinforcing the Selfwealth by Syfe result as part of a broader behavioural shift rather than a single-platform anomaly.

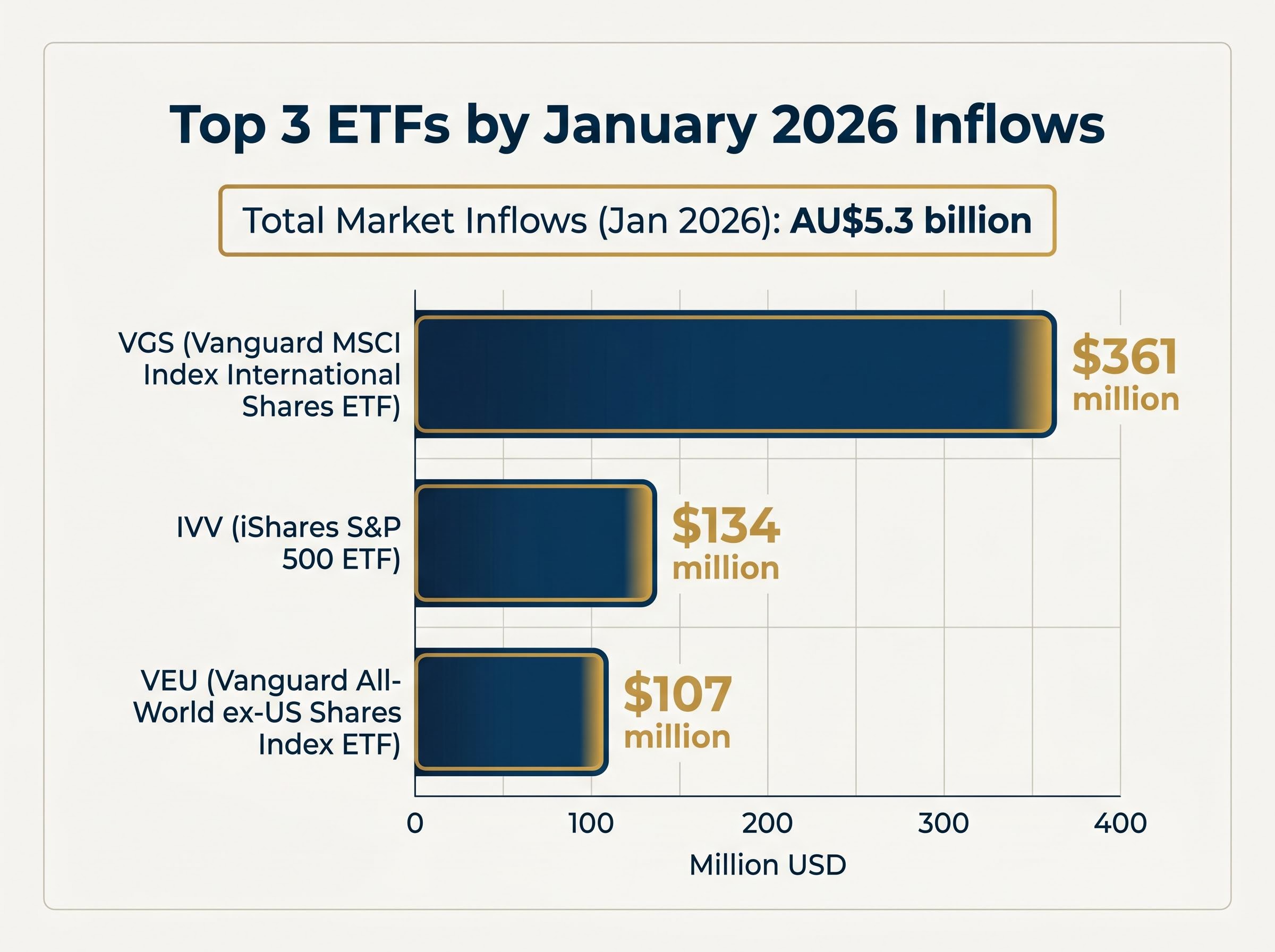

January 2026 alone delivered record ETF inflows of AU$5.3 billion across the market, with international names dominating the leaderboard. The three largest ETFs by January inflows were all internationally focused:

- VGS (Vanguard MSCI Index International Shares ETF): $361 million in January inflows, ranking first among all ETFs

- IVV (iShares S&P 500 ETF): $134 million in January inflows

- VEU (Vanguard All-World ex-US Shares Index ETF): $107 million in January inflows

These are not speculative thematic products. They are broad-market, passive international equity instruments, and retail investors chose them over domestic alternatives in sustained volume. That distinction matters: it signals a conviction-driven reallocation, not a momentum trade.

When big ASX news breaks, our subscribers know first

What home bias actually costs Australian investors

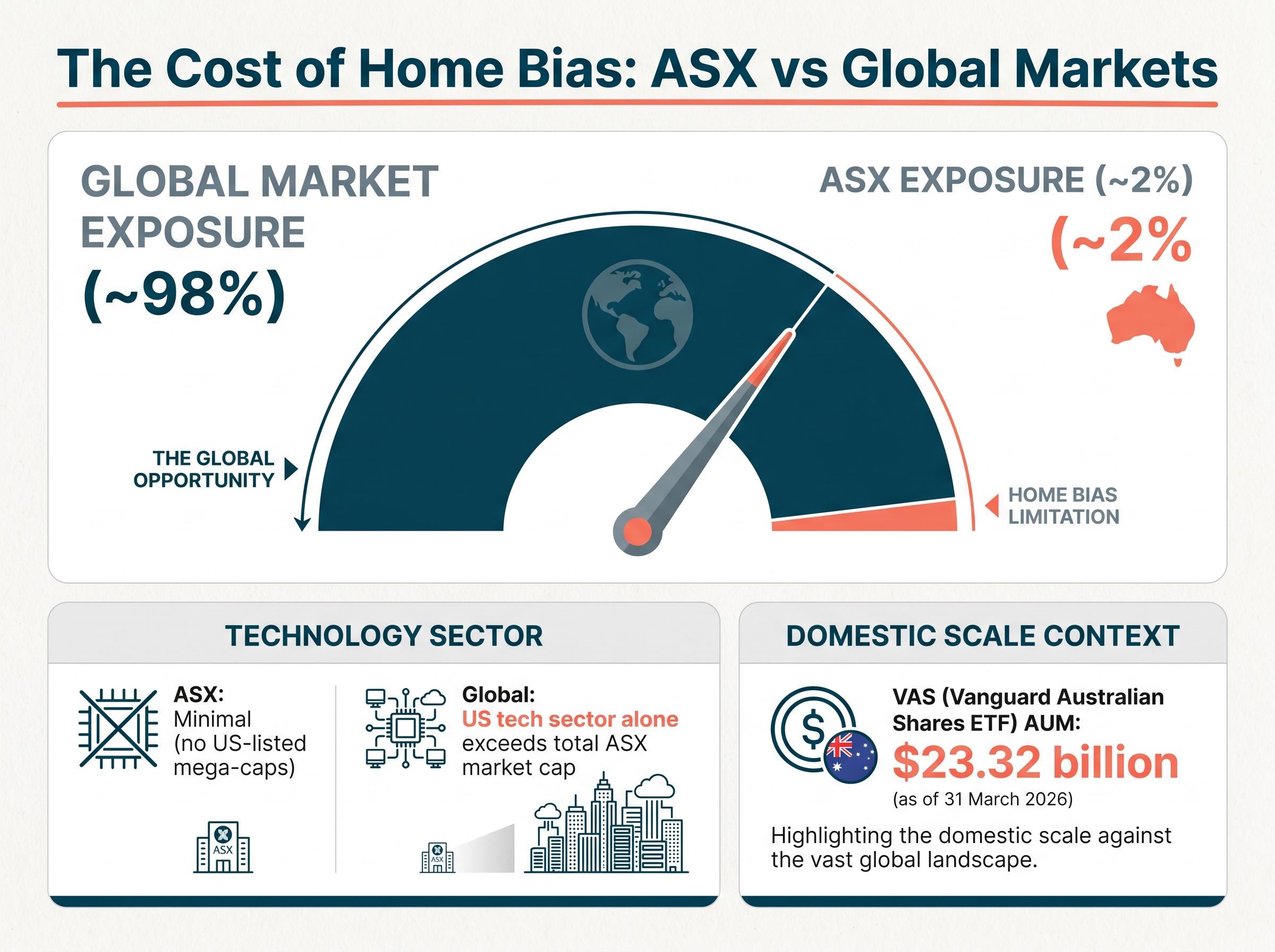

Home bias is the tendency of investors to over-allocate to their domestic market relative to its share of global market capitalisation. In Australia, where the ASX represents approximately 2% of the world’s investable equity universe, that tendency has historically been pronounced.

The bias has never been irrational. Franking credits provide a tax-effective incentive to hold Australian dividend-paying equities. Domestic brokerages default to ASX-listed products. Familiarity with local names reduces the perceived effort of research. Yet the result is a concentrated position: a portfolio dominated by Australian shares is, by construction, an active bet on 2% of global markets.

Home bias in Australian portfolios has persisted partly because the structural incentives reinforcing it, franking credits, default brokerage settings, and familiarity with domestic names, are invisible costs rather than explicit fees, making them harder for investors to weigh against the opportunity cost of a concentrated 2% allocation.

The sectors you cannot get from the ASX alone

The cost of that concentration becomes visible at the sector level.

| Dimension | ASX exposure | Global market exposure |

|---|---|---|

| Share of global equity market cap | ~2% | ~98% |

| Technology mega-cap representation | Minimal (no US-listed mega-caps) | US tech sector alone exceeds total ASX market cap |

| Healthcare and biotech breadth | Limited large-cap healthcare names | Deep coverage across pharma, medtech, genomics |

Technology mega-cap exposure, global healthcare innovation, and broad emerging market growth are structurally unavailable in meaningful weights through domestic ETFs alone. According to Selfwealth by Syfe data, international ETF flows in Q1 2026 concentrated in precisely these gaps, with investors seeking the sector diversity the ASX cannot provide at scale.

VAS (Vanguard Australian Shares ETF) held $23.32 billion in assets under management as of 31 March 2026, illustrating domestic ETF scale. Yet its recent inflow trajectory has been comparatively subdued relative to international peers, a signal that retail capital is moving toward correcting the concentration.

Who is driving the shift, and the generational picture is surprising

The assumption would be straightforward: younger investors, raised on global platforms and US-market content, are pulling the trend. The Selfwealth by Syfe Quarterly Investor Pulse tells a more complicated story. All age cohorts are moving toward greater international ETF exposure simultaneously.

| Generation | Approximate ETF allocation | Key behavioural note |

|---|---|---|

| Baby Boomers | Progressively increasing | Still favour individual equities but incorporating ETFs |

| Gen X | ~50% | Split roughly evenly between ETFs and individual equities |

| Millennials | ~70% | Highest ETF concentration; favour global diversification |

| Gen Z | ~50% | Balanced ETF and equity exposure; disciplined despite social media influence |

Millennials lead in absolute ETF allocation at approximately 70%, but the convergence across cohorts is the more significant finding. Gen Z investors, often characterised as speculative, are demonstrating diversified, disciplined behaviour. Baby Boomers are progressively incorporating ETFs into portfolios that remain tilted toward individual equities.

The generational shift to global ETFs among Australian retail investors is not simply a product of younger cohorts entering the market; it reflects a structural reorientation in how all age groups conceptualise portfolio construction, with ETFs replacing individual stock selection as the default vehicle for building diversified exposure.

81% of existing ETF investors plan to increase their holdings in 2026, according to the BetaShares/Investment Trends ETF Report published in December 2025.

An estimated 300,000 new ETF investors are forecast to enter the Australian market in 2026, adding to the 2.7-3 million Australians who already hold ETFs according to State Street estimates. When every generation moves in the same direction at the same time, the pattern is harder to dismiss as a demographic fashion. It looks structural.

The macro environment that made 2026 the year of the pivot

Three macroeconomic forces independently pushed Australian investors toward international diversification in early 2026. Their convergence explains why this shift is happening now, not just why it makes long-term sense.

- RBA policy divergence: The RBA raised the cash rate to 4.1% in March 2026, diverging from the US Federal Reserve’s rate-cutting cycle. This widening gap reshaped portfolio logic, increasing the relative appeal of offshore assets priced in a weakening US dollar.

- AUD strength: The Australian dollar surpassed 0.70 against the USD by March 2026, making international assets relatively cheaper in AUD terms for Australian buyers and encouraging outward capital flows.

- Geopolitical volatility and diversification conviction: The Australian ETF market lost $13.8 billion (a 4.0% decline) in March 2026 alone. Despite this, international equity ETFs continued attracting strong inflows, suggesting retail investors treated the drawdown as a diversification reinforcement rather than a reason to retreat to domestic safety.

The RBA’s February 2026 Statement on Monetary Policy noted resilient domestic demand but ongoing inflation pressures, conditions that may further encourage investors to diversify rather than concentrate in domestic equities. Platform data adds texture: trading volumes on Selfwealth by Syfe doubled during the US tariff announcement in April 2025, while activity declined more than 20% following the RBA’s March 2026 rate hike. Australian investors are sensitive to macro signals, and they are acting on them.

RBA policy and portfolio construction decisions are more tightly linked in 2026 than in most preceding years, with the cash rate at 4.1% while Australian 10-year government bond yields have risen to 5.02%, a combination that pressures long-duration domestic bonds and changes the relative return calculus between ASX equities and offshore growth assets.

The RBA monetary policy decision in March 2026 cited a material pick-up in inflation during the second half of 2025 and greater capacity pressures as the primary drivers of the rate increase, conditions that reinforced investor logic for seeking returns outside an increasingly restrictive domestic policy environment.

Currency dynamics and the hedging question

AUD strength in 2026 has made the hedging decision more consequential. An unhedged international ETF benefits when the AUD weakens (because offshore returns translate into more Australian dollars) but suffers when the AUD strengthens, as it did through early 2026.

Currency-hedged international ETFs, which neutralise exchange rate movements, have gained traction alongside unhedged products. For investors building global exposure in a strong-AUD environment, the choice between hedged and unhedged variants is no longer a secondary consideration; it directly affects realised returns.

Building a globally diversified portfolio: what the shift means in practice

The three leading international ETF instruments by January 2026 inflow volume each serve a distinct portfolio role, and understanding that distinction matters more than simply following flows.

| ETF code | Index tracked | January 2026 inflows | Primary portfolio role |

|---|---|---|---|

| VGS | MSCI World ex-Australia | $361 million | Broad developed-market international exposure |

| IVV | S&P 500 | $134 million | Concentrated US large-cap exposure |

| VEU | FTSE All-World ex-US | $107 million | Non-US global diversification |

VGS offers the broadest single-product solution for an Australian investor seeking developed-market exposure outside the ASX. IVV concentrates that exposure in US equities, carrying its own concentration risk in exchange for access to US tech and growth sectors. VEU complements a US-heavy portfolio by covering Europe, Asia-Pacific, and emerging markets.

Three portfolio construction considerations emerge from the data:

- Domestic versus global weighting: With the ASX at roughly 2% of global market cap, any allocation materially above that level represents an active domestic overweight. How far above 2% is appropriate depends on individual tax circumstances (franking credits), income needs, and risk tolerance.

- Hedged versus unhedged decision: In a strong-AUD environment, currency-hedged international ETFs reduce exchange-rate drag on returns. The trade-off is forgoing potential gains if the AUD subsequently weakens.

- Thematic versus broad-market exposure: Thematic international ETFs (sector-specific or niche products such as BetaShares’ planned space-themed ETF RCKT) represent a smaller but growing segment. They complement, rather than replace, broad-market core holdings.

State Street projects the Australian ETF market will reach AU$380 billion in assets under management by end-2026, with AU$40+ billion in net inflows forecast. International equity is positioned to remain the dominant inflow category.

The State Street 2026 Global ETF Outlook projects Australian ETF net inflows surpassing AU$40 billion for the year, with total assets under management reaching AU$380 billion and the number of domestic ETF holders exceeding three million, figures that frame the Q1 2026 behavioural shift as the leading edge of a significantly larger structural reallocation.

Selfwealth by Syfe data shows investors are increasingly reactive to macro announcements. That reactivity carries a risk: letting short-term volatility override a diversification thesis that the same investor adopted for long-term structural reasons.

The momentum behind the numbers points one way

The Selfwealth by Syfe Q1 2026 Quarterly Investor Pulse identified four behavioural shifts occurring simultaneously: a preference for international ETFs over domestic alternatives, cross-generational convergence toward global exposure, event-driven trading sensitivity, and declining gold enthusiasm. Gold buying on the platform declined below 70% of total gold-related trades in Q1 2026, signalling reduced safe-haven demand and improved risk appetite.

Gold rotation and risk sentiment data from Q1 2026 add another dimension to the picture: gold buying on major platforms declined below 70% of total gold-related trades as improving investor confidence drove capital toward financial sector equities and growth assets, a pattern that sits alongside the international ETF inflow trend rather than contradicting it.

That combination of signals points toward a market that is structurally repositioning, not temporarily rotating.

Conditions that could slow or reverse the trend deserve monitoring:

- A sharp AUD depreciation, restoring the relative appeal of unhedged domestic assets and reducing the cost advantage of buying international equities

- A sustained RBA pivot toward easing, which could improve the domestic earnings outlook and attract capital back to ASX-listed equities

- A prolonged global equity drawdown severe enough to shake conviction in the diversification thesis itself

Lower entry barriers, digital platforms, and broader access to financial information have permanently changed how Australian retail investors engage with global markets. These are structural shifts in market infrastructure, not cyclical conditions that revert.

With 470 ASX-listed ETFs as of March 2026 and product launches continuing to expand international options, the supply side is reinforcing the demand shift. State Street’s end-2026 inflow forecast of AU$40+ billion, with international equity expected to remain the dominant category, suggests the direction is set for the remainder of the year, absent a material macro reversal.

The border-crossing moment for Australian retail investing

Q1 2026 represents a documented inflection point in Australian retail investor behaviour. For the first time on a major platform, international ETFs displaced domestic funds as the preferred category, and the shift held across every generational cohort.

The forces behind it, policy divergence between the RBA and the Fed, a strong Australian dollar, expanding product availability, and lower barriers to global access, are not temporary. They are conditions that reinforce each other.

Whatever an investor’s generation or current allocation, the evidence suggests reviewing domestic concentration is now mainstream behaviour rather than an outlying strategy. The data does not prescribe a specific allocation. It does suggest that the cost of ignoring the question has become harder to justify.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.