Platform trading volumes doubled during the April 2025 US tariff announcement. They fell by more than 20% after the RBA hiked rates in March 2026. Two data points from different corners of the market, separated by nearly a year, yet they trace the same behavioural arc: Australian retail investors are reacting to headlines faster, more frequently, and with greater conviction than at any point in the platform era. Q1 2026 data from Selfwealth by Syfe confirms that the speed at which market information gets priced in has compressed from days to near-instantaneous, creating a structural shift that rewards institutional algorithms and pressures individual investors into mistaking urgency for strategy. What follows is an examination of what that reactive trading pattern actually costs, why the psychology behind it is so difficult to override, and what the data shows about the Australian investors who chose discipline instead.

When the headline hits, so does the trade

The numbers arrived before the narrative. When the US tariff announcement landed in April 2025, trading volumes on the Selfwealth by Syfe platform doubled.

Platform trading volumes doubled during the April 2025 US tariff announcement, according to the Selfwealth by Syfe Q1 2026 Quarterly Investor Pulse.

That was an external geopolitical shock, one that Australian investors had no direct control over and limited ability to price with precision. The response was immediate, voluminous, and largely reactive.

Two market events, one pattern

The March 2026 RBA rate hike produced the mirror image. Trading activity fell more than 20%, a retreat rather than a surge, but the underlying mechanism was identical: a macroeconomic headline triggered a rapid, broad-based behavioural shift across the retail investor base.

These two events differ in origin. One was a foreign trade policy decision; the other was a domestic monetary policy move. Yet both produced the same pattern of compressed, emotionally charged trading activity. That consistency across dissimilar catalysts strengthens the case that the reactive dynamic is structural, not event-specific.

Market information that previously took days or weeks to be priced in is now incorporated nearly instantaneously, according to Selfwealth by Syfe commentary. Reduced entry barriers, zero-commission platforms, and instant data access have fundamentally altered the friction involved in acting on an impulse. The cost of placing a trade has dropped to near zero. The psychological cost of placing a reactive one has not.

The compression of market information pricing from days to near-instantaneous is the product of zero execution lag across retail platforms, a structural shift accelerated by the Q1 2026 global energy volatility cycle and RBA policy moves that together stress-tested how quickly capital rotation could occur across an entire investor cohort.

When big ASX news breaks, our subscribers know first

Why reactive trading feels rational in the moment

The experience starts before the trade. A portfolio screen refreshes. A red number appears. The instinct is not to analyse; it is to act. That instinct has a name, and it has been measured.

Loss aversion, the cognitive bias in which losses feel roughly twice as painful as equivalent gains feel rewarding, is the first mechanism at work. When a portfolio drops 5% in a session, the psychological weight of that loss creates urgency that a 5% gain on another day would not. The impulse to stop the bleeding overrides the longer-term arithmetic.

Recency bias compounds the problem. Investors overweight the most recent data point, whether it is a tariff announcement, a rate decision, or a single bad earnings report, and project it forward as though it represents the new permanent reality.

The key psychological drivers of reactive trading include:

- Loss aversion: the disproportionate pain of losses relative to gains, creating urgency to act

- Recency bias: overweighting the latest headline as a predictor of future outcomes

- Fear of missing out: the perception that inaction during a fast-moving market is itself a losing strategy

Social media, financial influencers, and always-on news cycles amplify each of these. Younger investors are increasingly influenced by social media commentary and low-friction trading platforms, an observation noted across fintech industry analysis. Constant portfolio monitoring normalises the idea that every market movement requires a response.

ASIC’s REP 735 (Retail Investor Research) documents that retail investors consistently make mistakes in market timing, a core component of reactive investing behaviour.

ASIC’s 2025 media release (25-170MR) reinforced this finding, warning investors about the importance of informed decisions amid rising retail market participation. The regulator’s concern is not abstract. It is grounded in measurable outcomes.

What emotional investing actually costs

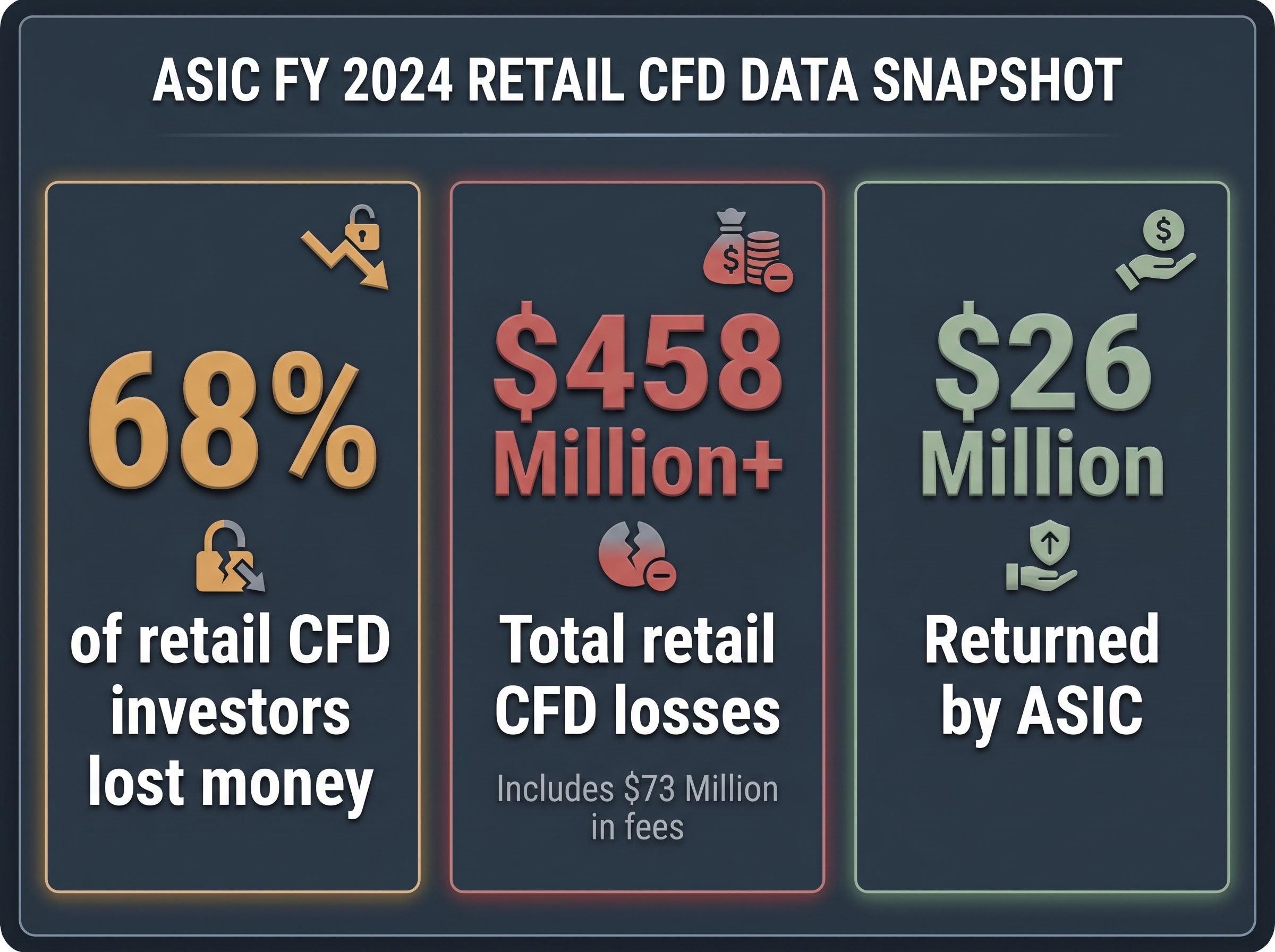

The sharpest available evidence of capital destruction associated with reactive, high-frequency trading among Australian retail investors comes from ASIC’s review of the contracts for difference (CFD) market.

In FY 2024, total retail CFD losses exceeded $458 million, including $73 million in fees alone.

ASIC REP 828 on CFD distribution practices details how product design, marketing, and sales incentives across the CFD sector contributed to the concentration of losses among retail clients, providing the regulatory foundation for the $458 million loss figure and the finding that 68% of retail CFD investors lost money in FY 2024.

68% of retail CFD investors lost money in that period. ASIC returned $26 million to retail CFD investors after a review found that over half the sector breached regulatory rules.

CFDs are leveraged products, and these losses are not a direct proxy for overtrading costs in standard equity markets. That distinction matters. No Australian-specific study published between 2024 and 2026 isolates and quantifies overtrading’s return impact on retail equity investors. The research gap is genuine.

The directional logic, however, is clear. Overtrading in equity markets erodes returns through three compounding mechanisms: transaction costs (even on low-commission platforms, they accumulate), tax drag from triggering short-term capital gains events with each sale, and the opportunity cost of exiting positions that would have recovered over a longer holding period.

The cost of reactive trading extends beyond the visible line items of brokerage fees: Australia’s 50% CGT discount for assets held longer than 12 months means that every short-term sale forfeits a structurally lower tax rate, effectively converting a behavioural impulse into a permanent, government-quantified penalty on returns.

| Trading Behaviour | Financial Risk | Australian Evidence |

|---|---|---|

| Reactive/CFD trading | Direct capital loss, fee erosion | 68% of retail CFD investors lost money; $458M+ total losses (ASIC, FY 2024) |

| Overtrading in equity markets | Transaction costs, tax drag, missed compounding | No quantified Australian study; directional evidence from CFD data and behavioural finance literature |

| Holding through volatility | Short-term drawdown exposure | 56.2% of ASA survey respondents held positions rather than selling (March-April 2026) |

The absence of a precise Australian equity overtrading figure does not diminish the argument. It sharpens it. If $458 million can evaporate in one year from one product category, the aggregate cost of reactive behaviour across the broader retail market is likely far larger, just harder to isolate.

The case for staying still: what patient investors actually did

The same volatility periods that produced doubled trading volumes and sharp activity drops also produced something less visible but more instructive: a substantial proportion of Australian investors who did not react.

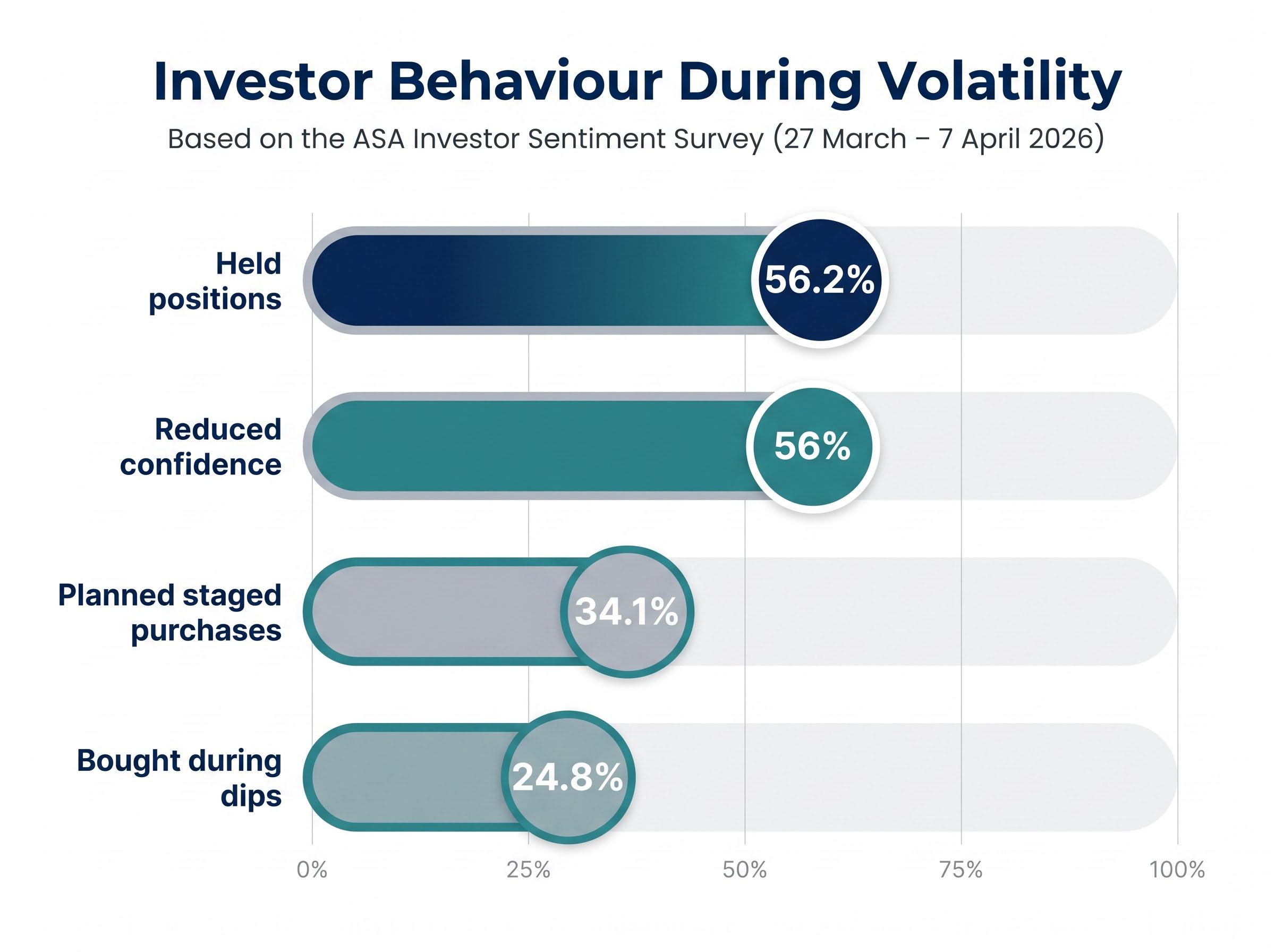

The Australian Shareholders’ Association’s Investor Sentiment Survey, conducted between 27 March and 7 April 2026, found that disciplined behaviour was not marginal. It was the majority position.

- 56.2% of respondents held their positions during volatility rather than selling

- 24.8% selectively bought during market dips

- 34.1% planned staged or incremental purchases

- 29.6% cited valuation as their primary priority during volatility

- 56% reported reduced confidence in their investment outlook amid geopolitical tensions

That last figure is worth pausing on. More than half of respondents felt less confident, yet the majority chose not to act impulsively. Emotional awareness did not automatically produce reactive behaviour.

Holding steady vs. buying deliberately

There is a meaningful distinction between the 56.2% who held and the 24.8% who bought during dips. Holding can be passive; it may reflect inertia as much as strategy. Buying during a drawdown is an active decision that requires both conviction and a pre-existing framework for identifying value.

The 29.6% who cited valuation as their primary focus during volatility were engaging in the kind of deliberate, fundamentals-driven analysis that behavioural finance research consistently associates with better long-term outcomes. These investors were not ignoring the headlines. They were reading them and choosing a different response.

Building a portfolio that does not need you to react

The most effective counter to reactive trading is not willpower. It is architecture. A portfolio structured to reduce the number of timing decisions an investor faces also reduces the psychological pressure that produces impulsive trades.

Three structural strategies accomplish this:

- Dollar-cost averaging (DCA): Systematic, staged purchases spread over regular intervals remove the timing decision entirely. The investor commits capital at predetermined points regardless of market conditions, averaging entry costs over time and eliminating the emotional burden of choosing the “right” moment. The 34.1% of ASA survey respondents who planned staged investments were already practising this approach. Auto-invest features, available at daily, weekly, fortnightly, or monthly intervals on platforms such as Selfwealth by Syfe, provide a structural implementation of DCA.

- Geographic diversification: Spreading exposure across multiple markets reduces vulnerability to single-market volatility events. In Q1 2026, international ETFs surpassed domestic funds as the most purchased ETF category on the Selfwealth by Syfe platform, a signal that Australian investors are already building this buffer into their portfolios.

International ETF inflows tell the fuller story of the geographic diversification shift: global equity ETFs attracted $17.3 billion in net inflows through October 2025, compared with $10.6 billion into Australian equity ETFs over the same period, and 65% of ETF investors nominated global equities as their next intended investment, figures that reframe the Q1 2026 platform data as the visible peak of a multi-year structural reallocation.

- Structured portfolio construction: Diversification across asset types (ETFs and direct equities), sectors, and geographies creates a portfolio less sensitive to any single headline.

| Strategy | How It Works | Australian Data Point |

|---|---|---|

| Dollar-cost averaging | Regular, fixed-amount purchases regardless of market conditions | 34.1% of ASA respondents planned staged investments (March-April 2026) |

| Geographic diversification | Spreading exposure across domestic and international markets | International ETFs overtook domestic funds as the leading ETF category on Selfwealth by Syfe in Q1 2026 |

| ETF-based portfolio construction | Using diversified ETFs as core holdings to reduce single-stock concentration risk | Millennials allocate approximately 70% of portfolio holdings to ETFs (Selfwealth by Syfe, Q1 2026) |

What the generational ETF data signals

The generational breakdown reinforces the structural shift. Millennials allocate approximately 70% of their portfolio holdings to ETFs. Gen Z and Gen X each allocate approximately 50%. Even Baby Boomer investors are progressively incorporating ETF holdings alongside equity-focused portfolios.

This is not a niche trend. Across every age cohort measured on the Selfwealth by Syfe platform, diversified, low-cost portfolio construction is the dominant approach. A concurrent rotation away from gold (which fell below 70% of gold-related trades in Q1 2026) and toward financial equities is consistent with improving sentiment and reduced defensive positioning.

Speed is the market’s new normal. Discipline is the investor’s edge.

The acceleration of information pricing is structural. It will not reverse. Headlines will continue to land in milliseconds, platforms will continue to make trading frictionless, and the psychological pull to respond at the same speed will persist.

The data from Q1 2026, however, reveals an asymmetry that favours the patient investor. Trading volumes doubled on a single tariff announcement, yet the majority of surveyed investors held their positions through the same volatility period. 56% reported reduced confidence, and still the dominant response was disciplined inaction or deliberate value-seeking.

ASIC’s continuing regulatory focus on protecting retail investors from products and behaviours that amplify emotional decision-making reflects the institutional recognition that this tension between speed and discipline is not going away. The regulator’s interventions, including the $26 million returned to CFD investors, are remedial. The investor’s structural advantage is preventive: build a portfolio that does not require split-second decisions, and the speed of the market becomes irrelevant to long-term returns.

Selfwealth by Syfe’s Q1 2026 Quarterly Investor Pulse characterises Australian investors as more knowledgeable, flexible, and globally oriented than in prior periods.

That characterisation, grounded in platform data rather than aspiration, is the foundation. The market moves fast. The investor who builds systematically does not need to.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.