A 3-Layer Portfolio Strategy for Volatile ASX Markets

1 min ago

Gold just posted its largest monthly decline since October 2008. U.S. Treasuries barely moved. The Australian dollar dropped sharply. If a defensive portfolio was supposed to provide protection during a crisis, April 2026 has been a disorienting month. The Iran war and the partial closure of the Strait of Hormuz have sent energy prices past $100 per barrel and pushed Australian headline CPI to 4.6%. Yet the assets most Australian retail investors rely on for shelter during turbulent periods, including gold, government bonds, and traditional safe-haven currencies, have either lost value or failed to provide meaningful protection. This is not a coincidence, and it is not a failure of the specific assets. It is a structural mismatch between the type of risk currently driving markets and the type of protection these instruments were built to provide. What follows explains exactly why that mismatch exists, what kind of crisis safe havens are actually designed for, and what the current environment means for Australian investors trying to make sense of their defensive allocations.

The numbers tell the story before the explanation does. Gold fell approximately 14.6% in March 2026, its largest monthly decline since October 2008, when it dropped 16.8%. A further 5-6% decline followed in April, bringing the price to approximately $4,430 per ounce as of 28 April. This came after an 80% rally over the preceding two years.

U.S. 10-year Treasury yields moved only 2-5 basis points across April, drifting from roughly 4.29% to approximately 4.31%. In practical terms, bonds provided no price appreciation as a hedge. The Japanese yen and Swiss franc, both long regarded as defensive currency positions, underperformed despite their historical reputations.

The Australian dollar fell to 70.64 US cents following the U.S. missile strike on Iran. The one relative beneficiary was the U.S. dollar itself, which strengthened on the back of domestic energy production capacity and Federal Reserve rate expectations.

“There is almost nowhere to hide now.”

The simultaneous failure of multiple uncorrelated safe havens is what makes this period unusual. Gold, bonds, and defensive currencies rarely all underperform at the same time. When they do, it signals something specific about the nature of the risk in play.

| Asset | Pre-crisis baseline | April 2026 change | Outcome |

|---|---|---|---|

| Gold | ~$4,700/oz (1 April) | Down ~5-6% | Failed as hedge |

| U.S. 10-year Treasuries | ~4.29% yield | +2-5 bps (to ~4.31%) | No price appreciation |

| Japanese yen | Pre-crisis level | Underperformed | Failed as hedge |

| Swiss franc | Pre-crisis level | Underperformed | Failed as hedge |

| Australian dollar | Pre-strike level | Fell to 70.64 US cents | Weakened sharply |

| U.S. dollar | Pre-crisis level | Strengthened | Sole conventional beneficiary |

Gold, government bonds, and defensive currencies were designed to protect against financial risk. Credit stress, deflationary demand shocks, equity market selloffs, and scenarios where inflation expectations remain anchored: these are the conditions under which safe-haven instruments perform their intended function.

In a financial crisis or recession, the dominant threat is a collapse in demand and confidence, not a collapse in physical supply. Consumers stop spending. Businesses delay investment. Credit markets tighten. In that environment, government bonds appreciate because yields fall as central banks cut rates. Gold holds or rises because it acts as a store of value when financial assets lose credibility. Defensive currencies attract flows because investors seek perceived stability.

Gold’s 80% price increase over the 24 months preceding April 2026 illustrates this clearly. It performed well during a period of financial stress and anchored inflation expectations. U.S. 10-year yields above 4% before the crisis began already placed bonds in a structurally difficult position, but the mechanism itself was not broken. The mechanism was simply built for a different threat.

Financial risk, in plain terms, is the risk that confidence in the financial system deteriorates: banks become reluctant to lend, asset prices fall because buyers disappear, and consumers pull back spending. Safe-haven assets are designed to hold or gain value in exactly these conditions.

Physical supply shock risk is fundamentally different. It is a disruption to the actual movement of goods, in this case oil through the Strait of Hormuz, that forces prices higher regardless of what consumers or central banks want. The inflation it produces is not caused by excessive demand. It is caused by constrained supply. That distinction determines whether defensive assets function or fail.

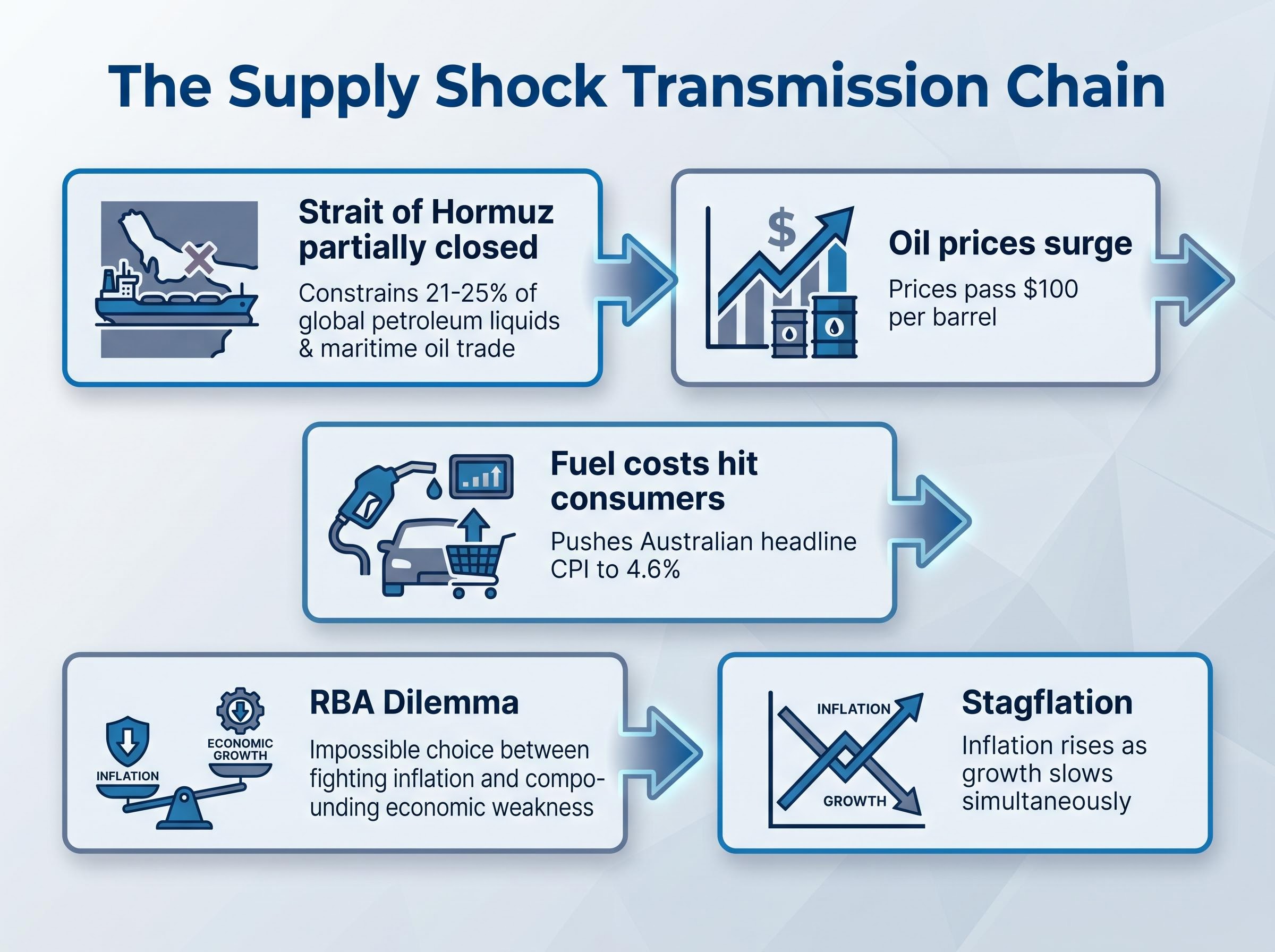

The Strait of Hormuz carries approximately 21-25% of global petroleum liquids and maritime oil trade. When that channel is disrupted, the effect is not abstract. It is physical, sequential, and mechanical.

The EIA data on global oil transit chokepoints confirms that the Strait of Hormuz accounted for approximately 20% of global petroleum liquids consumption and one quarter of total global maritime traded oil in the first half of 2025, figures that place the scale of the current supply disruption in concrete terms.

This is the transmission chain that turns a geopolitical event into a domestic inflation problem. The RBA’s relatively cautious response, despite the elevated CPI figure, reflects the recognition that supply-driven inflation caused by an external shock differs from demand-driven inflation. Rate hikes would not reduce the price of oil. They would only further constrain an economy already absorbing a cost shock.

The oil price transmission into recession follows four simultaneous channels: reduced consumer disposable income, rising business input costs, Federal Reserve rate pressure, and a pullback in investment and hiring, and Moody’s Analytics has placed the 12-month U.S. recession probability at 48.6% on the back of Brent crude surpassing $101 per barrel.

The situation remains fluid. The concept of stagflation, where inflation and stagnant growth coexist, emerges naturally from this sequence. It is not a theoretical framework. It is the observable outcome of a physical supply disruption feeding through energy costs into a consumption-dependent economy.

Reuters reported on 26-27 April 2026 that Iran has proposed reopening the Strait of Hormuz as part of broader diplomatic talks, a development that could ease oil prices and shift the dynamics currently dominating markets. The outcome of those talks represents the single most important near-term variable for energy prices and safe-haven performance.

The instinct for many Australian investors has been to assess April 2026 through the lens of 2008. That is the wrong reference point.

The 2008 financial crisis was a demand collapse. Consumer spending fell. Credit markets froze. Deflationary pressure dominated. In that environment, gold and bonds performed strongly because they were doing exactly what they were designed to do: providing shelter from financial system risk.

The 1973 OPEC oil embargo is the closer parallel. A sudden, geopolitically driven supply constraint at a critical energy chokepoint produced simultaneous upward pressure on inflation and downward pressure on growth. Gold and bonds initially underperformed during that supply shock as well. Gold eventually rallied as the stagflationary period extended, but the initial phase looked remarkably similar to what markets have experienced over the past two months.

The comparison matters because it reframes the current safe-haven failure as the expected outcome of this type of crisis, not an anomaly. Gold’s weakness may represent a phase rather than a permanent structural shift, contingent on how long the supply disruption persists. The 80% rally in the two years before April 2026 also means that a significant amount of appreciation had already been priced in before the shock hit, leaving gold vulnerable to any environment that did not match its design specification.

| Crisis | Trigger type | Inflation direction | Gold and bond initial response |

|---|---|---|---|

| 1973 oil shock | Geopolitical supply constraint | Upward (supply-driven) | Initial underperformance; gold rallied later |

| 2008 financial crisis | Credit and demand collapse | Downward (deflationary) | Strong performance as designed |

| 2026 Iran war | Geopolitical supply constraint | Upward (supply-driven) | Underperformance across both |

During a supply shock, the disrupted commodity itself becomes the source of price appreciation. Energy exposure has functioned as the genuine defensive trade in this environment, precisely because it is aligned with the risk rather than working against it.

For Australian investors, two ASX-listed names have offered more stable exposure to this dynamic than direct crude futures. Ampol and Viva Energy both provide crack spread exposure, which is the differential between crude oil input costs and refined product selling prices. When oil prices rise sharply and refining capacity remains constrained, that spread widens, benefiting domestic refiners and fuel distributors even if crude itself is volatile. Both companies carry domestic Australian revenue bases, which insulates them from some of the currency risk embedded in international commodity trades.

Direct commodity futures, by contrast, carry significant contango and roll costs that reduce the practical benefit for retail investors. Contango occurs when longer-dated futures contracts are priced higher than near-term ones, meaning investors lose value each time a contract is rolled forward.

Stagflation investing strategies for supply-shock environments differ structurally from standard recession playbooks: maintaining elevated cash buffers, targeting hydrocarbon exporters with domestic revenue bases, and securing short-duration fixed income all reflect the reality that the primary threat is persistent input cost inflation rather than a collapse in demand.

The Australian dollar’s fall to 70.64 US cents has created an unintended beneficiary among Australian investors: those holding unhedged USD-denominated assets. The exchange rate movement has provided an additional return component on top of any underlying asset performance.

This is not a position most retail investors deliberately constructed as a defensive allocation. It is, however, a real outcome worth understanding when evaluating overall portfolio performance during this period. Australian investors with U.S. equity or bond exposure have received a currency tailwind that has partially offset losses elsewhere.

The core framework that emerges from April 2026 is not complicated, but it requires a shift in how defensive assets are evaluated. Three questions clarify the assessment for any position marketed as protection:

The Reuters reporting from 26-27 April on Iran’s proposal to reopen the Strait of Hormuz introduces genuine optionality into the outlook. If the supply disruption eases, energy prices could moderate, and conventional safe havens may reassert their function as financial risk returns to the foreground. The 1973 precedent suggests that if the stagflationary conditions persist, gold could eventually rally as it did in the mid-1970s, but that depends on duration.

The gold price recovery outlook depends heavily on how long the stagflationary phase persists: Goldman Sachs maintains a $5,400 per ounce target for late 2026, anchored to central bank accumulation of 750-850 tonnes and Federal Reserve rate reductions, though the firm’s model also identifies equity-driven liquidation risk as a short-term downside factor.

The RBA’s constrained position remains a consideration for fixed-income holders. Supply-driven inflation limits the effectiveness of rate hikes, which means Australian bonds may continue to offer limited protection until the underlying supply shock resolves.

The outcome of the Strait of Hormuz diplomatic talks represents the single most important near-term variable for whether conventional safe havens recover their protective role or whether energy-aligned positioning remains the more effective defensive strategy.

Reacting to a single crisis episode by abandoning long-term allocations carries its own risks. The instinct to understand why a portfolio behaved unexpectedly is sound. The instinct to overhaul a strategy based on one phase of one crisis is less so.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements are subject to change based on market developments.

The 2026 crisis has not broken safe-haven assets. It has revealed the precise boundary of what they were designed to protect against. Supply shocks require supply-side hedges. Financial safe havens protect against financial risk. The mismatch between the two explains April’s disorienting results more completely than any failure in the assets themselves.

For Australian retail investors, this is a clarifying moment. Gold’s initial underperformance during the 1973 oil shock followed a similar pattern before precious metals eventually responded to prolonged stagflation. Whether the current phase follows the same trajectory depends on how the Strait of Hormuz situation resolves, and Australian CPI at 4.6% is a reminder that the RBA’s position remains constrained regardless.

The ABS Consumer Price Index for March 2026 identifies transport costs, including fuel, as a primary contributor to the 4.6% headline rate, providing the official measurement behind the inflation figure that now defines the RBA’s policy dilemma.

Supply shocks require supply-side hedges; financial safe havens protect against financial risk. Matching the instrument to the threat is the framework that outlasts any single crisis.

The diplomatic talks reported on 26-27 April are the specific development to monitor. Their outcome will determine whether the supply shock persists, extending the conditions under which energy-aligned positioning outperforms, or begins to unwind, reopening the space for conventional defensive assets to function as intended.

Investors who want to move beyond the immediate crisis framing and build a durable response to sustained volatility will find our full explainer on systematic investing strategies for Australian investors, which examines dollar-cost averaging into diversified index products, the capital rotation patterns visible in Q1 2026 data, and how younger investor cohorts are structuring ETF allocations to absorb ongoing market shocks.

Safe haven assets such as gold, government bonds, and defensive currencies are designed to protect against financial risk, including credit stress, deflationary demand shocks, and equity market selloffs. They perform their intended function when the dominant threat is a collapse in confidence and demand, not a disruption to physical commodity supply.

Gold fell approximately 14.6% in March 2026 and a further 5-6% in April, while U.S. Treasury yields barely moved, because the crisis was driven by a physical supply shock (the partial closure of the Strait of Hormuz) rather than financial system stress. Safe haven assets are built to hedge financial risk, not supply-driven inflation, so they failed to provide protection during a fundamentally different type of crisis.

The partial closure restricted global oil supply, pushing energy prices past $100 per barrel, which fed directly into Australian consumer prices and lifted headline CPI to 4.6%. This placed the RBA in a difficult position because raising rates to fight supply-driven inflation would further weaken an economy already absorbing a significant cost shock.

Energy sector equities with domestic revenue bases, particularly ASX-listed Ampol and Viva Energy, offered more stable exposure because their crack spread earnings align with rising oil prices rather than working against them. Australian investors holding unhedged USD-denominated assets also benefited from the Australian dollar's fall to 70.64 US cents.

The 1973 oil shock precedent suggests gold initially underperformed during the supply disruption but eventually rallied as stagflationary conditions extended into the mid-1970s. Goldman Sachs maintains a $5,400 per ounce target for late 2026, though recovery depends heavily on how long the current supply disruption persists and whether diplomatic talks succeed in reopening the Strait of Hormuz.