Australian markets in 2025 and early 2026 have delivered a live experiment in reactive investor behaviour, and the data is now in. A survey conducted by the Australian Shareholders’ Association (ASA) between 27 March and 7 April 2026 found that nearly 25% of retail investors were actively buying into volatility, while a meaningful minority adjusted portfolios around macroeconomic headlines rather than underlying fundamentals. The US tariff announcement of April 2025 and the RBA rate decision of March 2026 both triggered measurable shifts in trading activity across Australian platforms. The question worth examining is not whether investors reacted to these events; they did. The question is what those reactions cost them in real returns, and whether systematic alternatives exist that structurally remove the emotional decision point. What follows is an analysis of the verified behavioural evidence, the specific mechanisms through which reactive trading erodes returns in the Australian context, a concrete case study in gold sentiment, and the practical tools available to counter the impulse.

How Australian investors actually behaved when markets moved

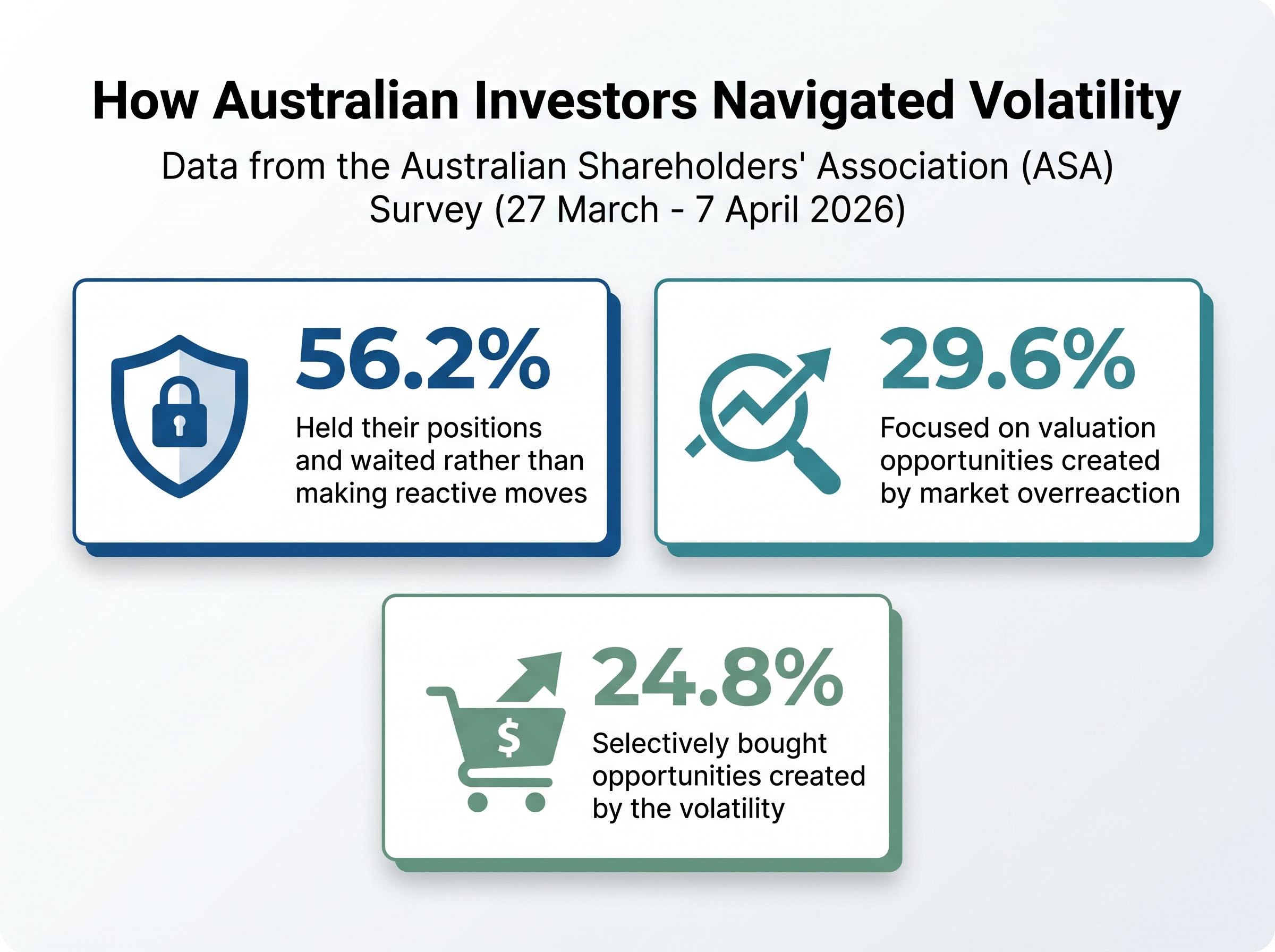

The ASA survey offers the clearest empirical window into how Australian retail investors responded to the volatility of late March and early April 2026. The majority held their nerve. That is the starting point, and it matters.

- 56.2% of respondents reported holding their positions and waiting rather than making reactive moves.

- 24.8% were selectively buying opportunities created by the volatility.

- 29.6% described themselves as focused on valuation opportunities created by market overreaction, rather than reacting to headlines alone.

29.6% of survey respondents focused on valuation opportunities created by market overreaction, suggesting a meaningful segment of the retail market is applying fundamental analysis during periods of stress rather than simply reacting to price movements.

These numbers challenge the assumption that retail investors uniformly panic during downturns. Most did not. However, a reactive minority did trade around headlines, and platform data from Selfwealth by Syfe’s Q1 2026 Investor Pulse captured a broader pattern consistent with this behavioural split: overall trading activity shifted sharply around major macroeconomic announcements, even as aggregate volume reflected holders staying put. The distinction between reduced overall volume and paralysis is worth noting. Lower volume during the RBA event reflected the disciplined majority holding, while a subset adjusted reactively.

The March 2026 RBA rate decision demonstrated algorithmic recalibration on retail platforms at a speed that prior market cycles had not produced, with transaction volumes shifting materially within the same trading session that the announcement landed.

The cost question that follows is not hypothetical. It is structurally embedded in what that reactive minority actually did.

When big ASX news breaks, our subscribers know first

The specific mechanisms that turn reactive trades into lost returns

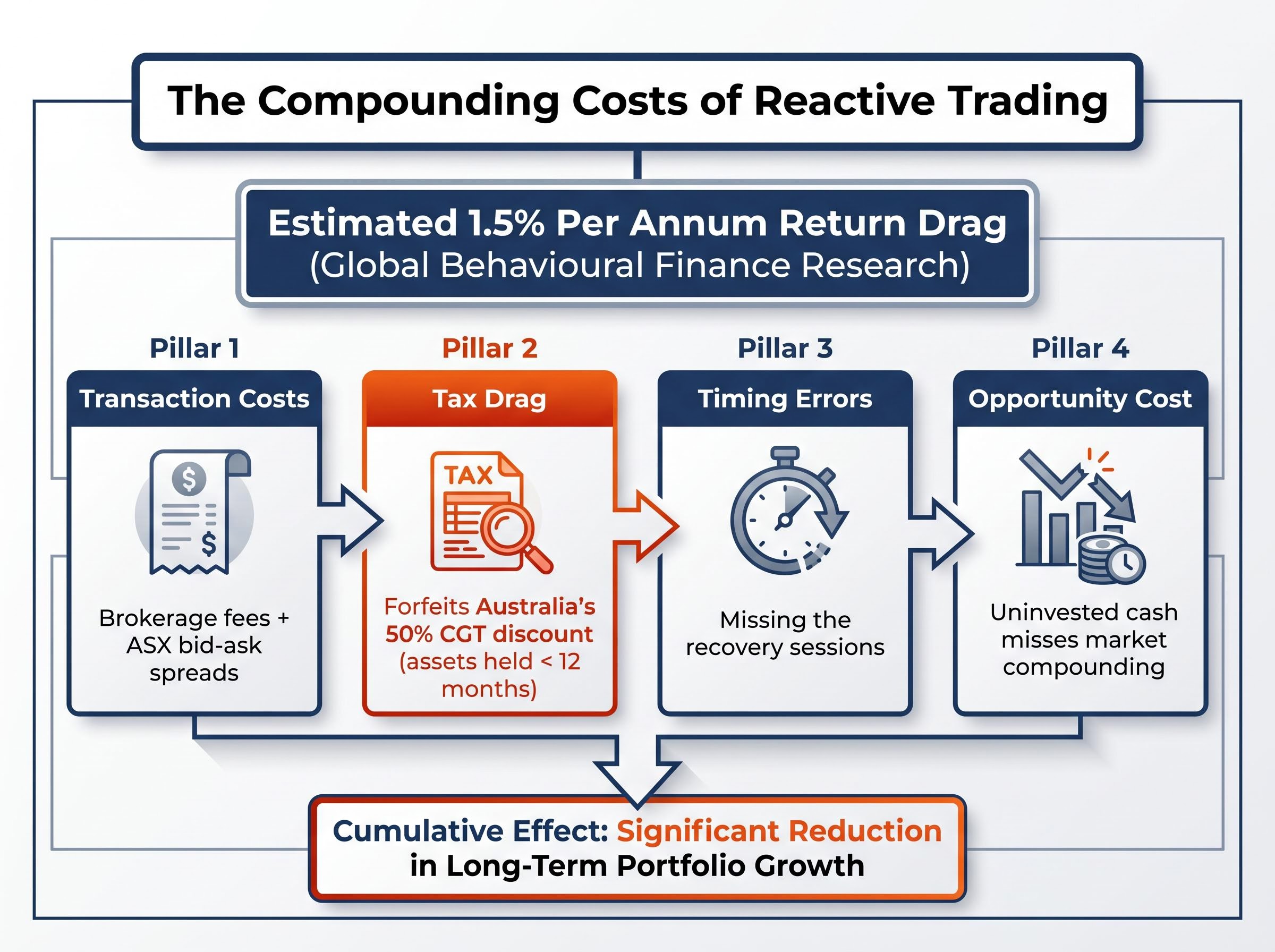

Each reactive trade does not carry a single cost. It carries several, and they compound. Understanding them in sequence makes the cumulative drag concrete rather than abstract.

| Cost Mechanism | What Triggers It | Australian-Specific Factor | Investor Impact |

|---|---|---|---|

| Transaction costs | Each buy or sell order | Brokerage fees plus bid-ask spreads on ASX-listed securities | Direct reduction of net returns per trade |

| Tax drag | Realising gains on assets held under 12 months | 50% CGT discount forfeited; gains taxed at full marginal rate | Structurally larger tax bill on short-term reactive trades |

| Timing errors | Exiting during volatility and missing the recovery | Best trading days cluster near the worst across global and Australian markets | Permanent return shortfall from missing recovery sessions |

| Opportunity cost | Holding cash while waiting for “the right moment” | Uninvested capital misses compounding in a market that trends upward over time | Foregone returns accumulate over months and years |

The Australian capital gains tax structure deserves particular emphasis. Assets held for fewer than 12 months are taxed at the investor’s full marginal rate. Assets held beyond that threshold qualify for a 50% CGT discount. Every reactive trade that crystallises a gain inside that window costs the investor not just brokerage but a structurally larger tax bill. This is not a behavioural argument; it is a penalty written into the tax code.

The ATO CGT discount rules confirm that individual investors must hold an asset for at least 12 months before the 50% discount applies, meaning every reactive trade that crystallises a gain inside that window is taxed at the investor’s full marginal rate with no discount available.

Global behavioural finance research estimates a return drag of approximately 1.5% per annum attributable to behavioural biases. No Australian-specific figure has been confirmed, but the mechanisms above apply with equal force locally, and the CGT structure amplifies them.

Why investors react this way: the behavioural mechanics behind news-driven trading

Knowing the costs is not the same as understanding why investors incur them. Three cognitive biases are most directly responsible for news-driven reactive trading:

- Loss aversion: Investors tend to weight potential losses approximately twice as heavily as equivalent gains, according to behavioural finance research. This distorts sell decisions during downturns, making the urge to exit feel rational even when the underlying investment case has not changed.

- Recency bias: Investors overweight the most recent market move when projecting near-term outcomes. A sharp drop on Monday shapes expectations for Tuesday, regardless of whether the fundamentals support that extrapolation.

- Herding behaviour: When other participants are visibly selling, the social pressure to follow compounds the cognitive pressure. The combination creates a feedback loop that accelerates reactive decisions.

Each of these biases is well-documented in behavioural finance literature. None of them is irrational in origin; they are cognitive shortcuts that served humans well in environments where physical threats required fast responses. Financial markets are not that environment, but the brain treats them as though they are.

How speed amplifies behavioural biases

The Q1 2026 Investor Pulse from Selfwealth by Syfe observed that market pricing of new information is occurring more quickly than in prior periods. This compresses the decision window investors feel they have, artificially increasing urgency.

The speed of news absorption does not, however, change the underlying investment case for any given holding. It changes only how quickly other participants price in new information. Recognising that distinction is the difference between resolving to “be more disciplined” and understanding the specific mechanism that needs to be countered.

Gold in 2025 and 2026: a case study in sentiment-driven cycles

Gold provides a useful case study precisely because it is not a speculative fringe asset. It is a mainstream defensive holding, and yet in 2025 and 2026, it became a vehicle for the same reactive behaviour the data identifies elsewhere.

The sentiment arc followed a recognisable pattern:

- Uncertainty rises, gold demand surges. Geopolitical instability and macroeconomic uncertainty in late 2025 drove elevated demand for gold as a hedge, pushing allocation toward the asset across retail platforms.

- Confidence recovers, capital rotates out. As investor sentiment improved in Q1 2026, capital began rotating toward financial equities and growth-oriented assets. Gold purchase activity as a proportion of total trades on the Selfwealth by Syfe platform declined.

- Late buyers absorb the retreat. Investors who entered the gold trade at peak sentiment, driven by headlines rather than portfolio construction, were most exposed to the cooling phase.

Gold purchase activity as a proportion of total trades on the Selfwealth by Syfe platform fell to below 70% of its prior levels in Q1 2026, as capital rotated toward growth assets following the sentiment peak.

Gold retains a legitimate role in diversified portfolios as an inflation and geopolitical hedge. The problem is not owning gold. The problem is concentrating in it at the peak of a sentiment cycle, which is precisely what reactive, news-driven behaviour tends to produce.

The broader pattern of capital rotation away from defensive assets that characterised Q1 2026 was not a retreat from markets; it was a repositioning, with offshore-focused funds absorbing flows that had previously sat in domestic equities and safe-haven holdings like gold.

Systematic strategies that remove the reactive decision point

The diagnosis is clear; the prescription follows. Dollar-cost averaging (DCA) and automated investing are not primarily return-maximisation strategies. They are behavioural circuit breakers, designed to remove the investor from the decision at the moment of maximum emotional pressure.

Research from BetaShares, Stockspot, and Hudson Financial Planning shows that lump-sum investing outperforms DCA in approximately 68-75% of historical periods in Australian markets. DCA produces roughly 0.5-1% lower annual returns over 10-plus year horizons compared to lump-sum deployment, because capital sits uninvested while waiting for scheduled entry points.

That comparison, however, misses the point for the reactive investor. The correct comparison is not lump-sum versus DCA. It is any systematic strategy versus discretionary timing, where discretionary timing is the consistent underperformer.

The performance gap between reactive versus systematic investing approaches in the Australian market widened materially through early 2026, as $6.9 billion in quarterly inflows into global equity ETFs demonstrated that systematic deployment into diversified index products was absorbing the capital that discretionary traders were rotating out of domestic defensives.

| Approach | Typical Return Profile | Behavioural Risk | Best Suited For |

|---|---|---|---|

| Lump-sum investing | Outperforms in 68-75% of historical Australian periods | Requires conviction to deploy capital during uncertainty | Investors with high discipline and available capital |

| Dollar-cost averaging | Approximately 0.5-1% lower annual returns over 10+ years | Low; removes timing decisions from the process | Investors prone to reactive trading or with regular income to deploy |

| Discretionary timing | Typically underperforms both systematic approaches | High; every decision point introduces emotional interference | Not recommended as a primary strategy |

The Selfwealth by Syfe auto-invest feature offers Australian investors a concrete tool for implementing systematic strategies. It enables scheduled recurring purchases across existing holdings at the following intervals:

- Daily

- Weekly

- Biweekly

- Monthly

For investors who recognise themselves in the reactive minority, the practical value is immediate. A pre-committed schedule removes the decision from real time, which is exactly when behavioural biases exert the most pressure.

The return on patience: what the data tells long-term Australian investors

The evidence from the 2025-2026 volatility period converges on a single observation. The investors who fared best were not those who made the smartest tactical calls. They were the ones who made the fewest reactive ones.

The 29.6% of ASA survey respondents who focused on valuation opportunities represent a behaviour worth studying. They used volatility as a signal to examine fundamentals rather than as a trigger to exit. That approach aligns with what behavioural finance literature has consistently demonstrated across multiple market cycles: short-term fluctuations diminish in significance over longer investment horizons.

Generational shifts in portfolio construction are reshaping the composition of the disciplined investor cohort itself, with Millennials allocating a substantially higher share of capital to broad-market index products than older cohorts, a structural preference that embeds systematic behaviour by design rather than discipline.

Australia’s 50% CGT discount for assets held longer than 12 months is, in effect, a government-sanctioned incentive to hold through volatility rather than react to it. The tax code itself rewards patience with a structurally lower tax burden on gains.

This reframes patience not as passive inaction but as an active, evidence-supported strategy with a specific return mechanism behind it.

What a disciplined response looks like in practice

The ASA survey data points to three behaviours that characterise the disciplined investor cohort:

- Holding through volatility rather than selling in response to short-term price moves.

- Reviewing valuations rather than headlines, using downturns to assess whether prices have moved below fundamental value.

- Using pre-committed investment schedules to avoid reactive decision-making at moments of peak emotional pressure.

These are behaviours, not personality traits. They can be adopted, practised, and structurally supported through the tools available to Australian retail investors today.

Markets will keep moving: the case for building a system before the next announcement

The next macroeconomic announcement will arrive. The next geopolitical disruption will move prices. The question for each investor is whether the response will be determined in the moment, under emotional pressure, or decided in advance through a system designed to absorb volatility without reactive intervention.

The ASA survey found that 56.2% of Australian retail investors already held positions through the most recent period of volatility. The disciplined majority exists. The goal is to move more investors into it and to give the reactive minority a structural alternative.

The following steps can be taken before the next event arrives:

- Review current holdings against a pre-defined investment thesis, not against the most recent headline.

- Set up automated recurring purchases at a frequency that matches regular income or capital availability.

- Establish a written policy for when a portfolio review is triggered (scheduled intervals, not market events).

- Confirm that any planned sell decisions qualify for the 12-month CGT discount before executing.

The time to build a system is before the volatility arrives, not during it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—