The Reserve Bank of Australia adjusted policy settings in March 2026, and local trading platforms registered the shift immediately. This rapid response occurred against a backdrop of extreme global energy volatility during the first quarter. Retail investor behaviour as a strategic indicator now operates without its traditional buffer, fundamentally altering how quickly market momentum builds.

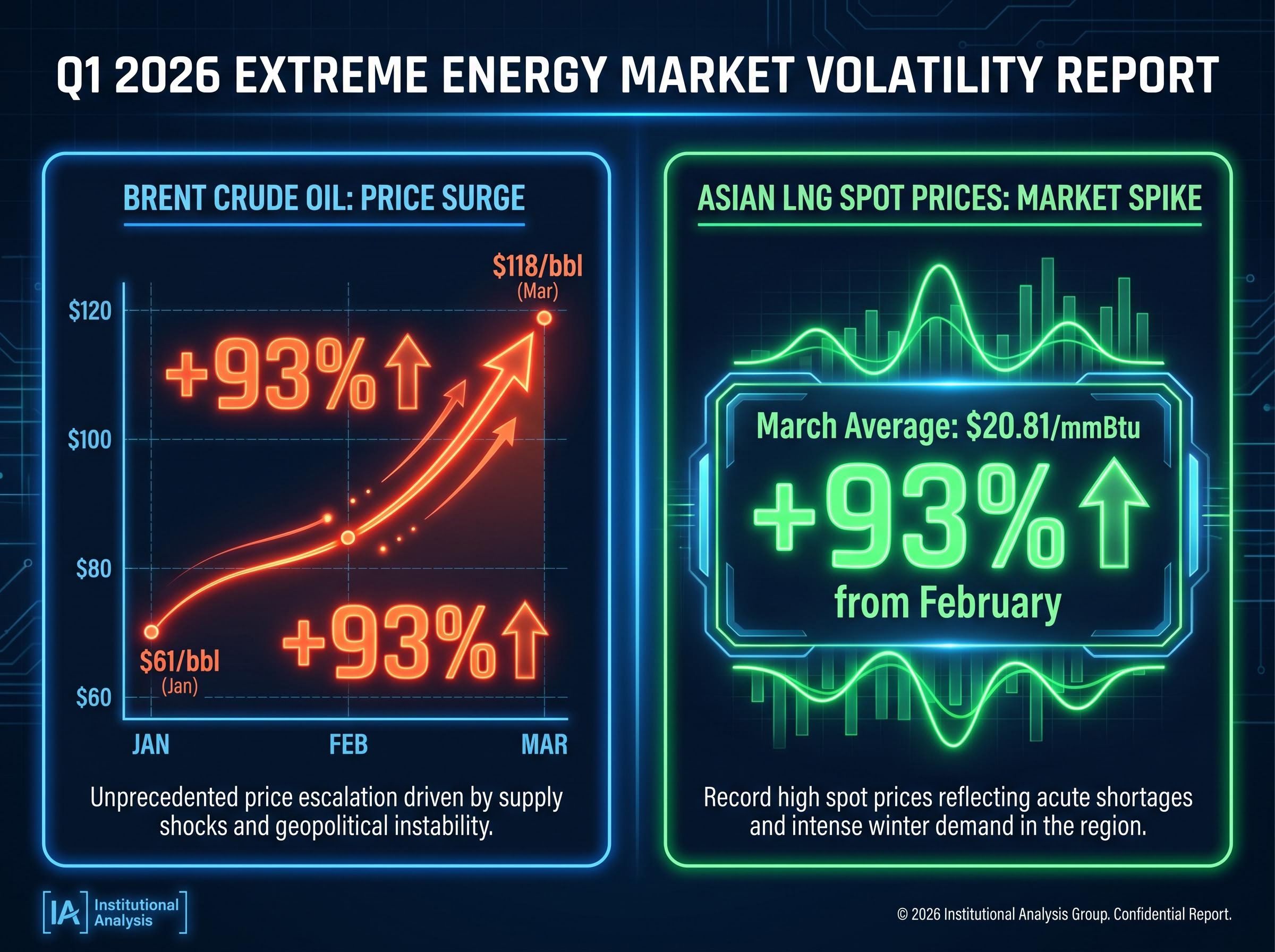

Energy markets delivered massive shocks that tested the resilience of domestic portfolios. Brent crude oil surged 93% from $61/bbl to $118/bbl between January and March. Asian LNG spot prices averaged $20.81/mmBtu in March, representing a 93% increase from February levels.

The historical delay between macroeconomic news breaking and retail trading execution has disappeared completely. Investors process and price in these severe global fluctuations in real time. The gap between the shock’s severity and the market’s response reveals how consumer participants are recalibrating their risk assessments.

The End of the Execution Lag

According to industry analysis, platform engagement decreased subsequent to the March RBA action to elevate borrowing costs. The withdrawal of retail liquidity happened within hours rather than weeks. Historically, non-institutional participants took extended periods to digest macroeconomic news before adjusting their portfolios.

This timeframe has collapsed entirely, replacing gradual portfolio adjustments with coordinated mass trading events. The baseline for this hypersensitivity became apparent during the April 2025 American trade duty declarations. Market data shows transaction quantities expanded across Australian platforms as the news broke, marking a clear departure from delayed consumer responses.

High-frequency reactions are no longer exclusive to institutional algorithms. The suddenness of the March drop confirms that consumer market momentum now moves in lockstep with breaking policy updates. Understanding this velocity helps analysts assess domestic liquidity during macro stress periods.

Official ASIC analysis of retail trading during periods of extreme volatility highlights a structural shift toward rapid-fire execution, noting that non-institutional participants frequently double their transaction frequency when macroeconomic conditions destabilize.

Market Sensitivity Shift Information that historically required extended periods to influence asset pricing now triggers almost immediate transactional reactions across consumer trading accounts.

When big ASX news breaks, our subscribers know first

Understanding the Mechanics of Zero-Delay Trading

Trade execution lag refers to the time delay between a market event occurring and a participant placing a corresponding trade. This delay historically served as a buffer for non-institutional market participants, preventing sudden mass capital flights based on single news events. It allowed time for secondary analysis and professional commentary to temper immediate emotional responses.

Modern infrastructure has removed this friction entirely. Mobile brokerage systems operated by CommSec, Stake, and nabtrade deliver institutional-grade news directly to user interfaces.

This connectivity relies heavily on the algorithmic mechanisms accelerating retail trading, which process macroeconomic signals and facilitate real-time portfolio recalibrations before human analysis concludes.

This constant connectivity means everyday Australians process and react to global events simultaneously alongside professional trading desks. This heightened behavioural sensitivity can lead to rapid market corrections and amplified local volatility.

When thousands of individual participants receive identical macroeconomic alerts, their collective instant reactions create severe intraday price swings. The structural reality of these platforms encourages immediate action over measured consideration.

Three main drivers facilitate this zero-delay trading environment: Platform accessibility via smartphone applications that keep trading accounts permanently logged in. Instant news alerts pushing policy decisions directly to mobile lock screens. * Simplified order execution mechanisms requiring minimal confirmation steps to deploy capital.

Managing Q1 2026 Volatility Through Global Diversification

The extreme macroeconomic events of early 2026 forced a structural migration toward overseas assets. The rapid trading mindset directed capital away from localised risks and toward broader international exposure.

Surging domestic electricity futures, which saw Q2 projections track higher at approximately $96.25/MWh, pushed retail participants to rethink their geographic concentration. Australian investors deliberately reduced their domestic weighting to seek stability in overseas sectors like healthcare and technology.

This capital rotation aligns with the desire to mitigate the domestic impacts of elevated operating costs. Overseas-focused funds surpassed domestic equivalents as the most frequently acquired fund category in Q1 2026. This flow of capital indicates a maturing retail sector capable of using global instruments to hedge local macroeconomic vulnerabilities.

Generational Approaches to Exchange-Traded Products

Different demographics approach these portfolio components with distinct strategies. Older generations still predominantly hold individual company shares while progressively integrating exchange-traded products into their wealth management plans.

Younger market participants treat these packaged funds as foundational portfolio building blocks rather than supplementary diversification tools. Generation Z account holders maintain an equal distribution of capital between single equities and packaged funds.

The official ASX investor demographic study confirms this structural generational shift, demonstrating that younger market participants now routinely utilize exchange-traded products to construct their foundational wealth bases rather than relying solely on individual equity selection.

According to platform data, Millennial demographic participants dedicate approximately 70% of their total investment capital toward exchange-traded products. These distinct adoption rates highlight how different age groups successfully restructure their holdings to handle macroeconomic shocks.

| Demographic Group | Single Equities Allocation | Packaged Funds Allocation |

|---|---|---|

| Generation Z | ||

| Millennials | 30% | 70% |

The Rapid Rotation from Defensive Bullion to Expansion Assets

A rapid departure from defensive investment postures dominated the transition from late 2025 into early 2026. Precious metal accumulation was previously stimulated by global political instability and served as the primary hedge for retail portfolios. The recent capital rotation into financial sector equities indicates rising market optimism despite underlying macro volatility.

Observing this broader retail investor capital rotation reveals that participants are intentionally moving away from cash reserves to capture cyclical growth opportunities.

Retail participants are looking past immediate energy shocks to position for broader economic recovery. According to platform data, purchasing transactions for the yellow metal declined to represent less than 70% of overall platform trading volume in Q1 2026. This decline provides evidence of a broader behavioural shift away from strict wealth preservation.

Investors appear willing to absorb higher near-term risks to capture growth opportunities outside traditional safety assets. Evaluating this pivot helps investors determine whether their own defensive holdings remain aligned with current retail momentum. Identifying where capital flows after leaving defensive positions reveals the market’s forward-looking risk appetite.

Key sectors currently attracting consumer capital outflows from previous precious metal allocations include: Financial equities benefiting from adjusted interest rate expectations. Global technology companies offering structural growth detached from local energy costs. * Healthcare providers demonstrating resilient pricing power.

The Long-Term Impact of High-Velocity Retail Markets

Instant execution capabilities and structural shifts toward global exchange-traded funds permanently alter Australian market stability. The psychological evolution of the modern retail participant has moved from delayed observation to immediate, aggressive participation. Investors no longer wait for institutional analysts to interpret macroeconomic data before adjusting their positions.

This structural shift means domestic liquidity can evaporate or surge in minutes based on global headlines. Future central bank announcements will likely trigger identical high-velocity reactions across domestic platforms.

Preparing for these dynamics requires holding diversified baseline portfolios that can withstand severe intraday swings without forcing reactive liquidations. The retail market has fundamentally changed, and investment strategies must account for this new era of zero-delay execution.

For readers wanting to understand the systemic implications of these rapid capital flows, our detailed coverage of the global ETF shift outlines how increased adoption of automated investment tools will further reshape domestic liquidity.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.