Volatility is compressing returns across the exact investments designed to protect capital. The ongoing Middle Eastern conflict and severe energy supply constraints in April 2026 have created an environment where elevated borrowing costs are actively punishing government debt and precious metals. Investors holding traditional safe haven assets are watching these positions bleed value precisely when global tensions suggest they should be surging. This paradox demands a complete diagnostic of the current financial environment.

What follows is a comprehensive framework explaining why conventional defensive portfolios are struggling against persistent inflation. It provides a roadmap for capitalising on multi-year high yields and targeted, quality-focused Australian equity options. Diagnosing the most common portfolio errors of a rate-cut-starved environment requires understanding the new mechanics of capital preservation. This guide delivers actionable steps for restructuring fixed-income and equity allocations to withstand the current macroeconomic pressures.

Dismantling the Illusion of Automatic Portfolio Protection

Decades of financial theory have trained investors to expect a specific sequence during a global crisis. Stock markets fall, central banks lower interest rates, and protective investments surge in value. This historical pattern of crises triggering deflation and subsequent rate cuts has worked consistently over the past four decades.

Today, that automatic mechanism is completely broken. The current geopolitical tension represents a severe supply disruption rather than a demand destruction event. Central banks are unable to lower interest rates to rescue falling markets because they are battling persistent, structurally embedded inflation pressures.

Market Shock Comparison

“The current combination of disrupted supply chains and elevated inflation mirrors the initial 2022 market shock, proving that defensive allocations fail when central banks are forced to prioritise price stability over market support.”

Comparing the current environment to the combined pandemic and European conflict effects experienced previously reveals a harsh reality for passive investors. Rate cuts are no longer the default central bank response to geopolitical instability. During the 2008 financial crisis or the 2020 pandemic onset, deflationary fears allowed central banks to slash borrowing costs immediately.

The current market faces the opposite problem, rendering the traditional protective playbook ineffective. This explains why previously reliable defensive allocations are currently showing negative returns. Readers can avoid panic selling by understanding this macroeconomic context, recognising that waiting for an automatic defensive rally is a flawed strategy when inflation dictates monetary policy.

The mechanics of how inflation erodes purchasing power explain why central banks now prioritise price stability over supporting asset valuations, leaving passive investors completely exposed when the historical cycle of monetary easing fails to materialise.

When big ASX news breaks, our subscribers know first

Unpacking the Mechanics of the Bond and Gold Sell-Off

The destruction of defensive valuations begins with global energy transit routes. According to industry estimates, approximately one-fifth of worldwide petroleum and liquefied natural gas shipments normally pass through the Strait of Hormuz. Geopolitical tensions restricting these critical chokepoints create a massive petroleum supply constraint, filtering directly into global inflation metrics.

Official EIA global transit chokepoint data formalises this vulnerability, demonstrating how regional shipping constraints immediately force international energy prices higher.

This persistent inflation forces a severe repricing in the fixed-income market. According to market data, investors demand greater compensation for duration risk, driving yields on benchmark ten-year American government debt past the 4% threshold.

These elevated borrowing costs trigger several specific factors that depress government debt valuations:

Higher newly issued yields immediately discount the secondary market price of older, lower-yielding bonds. Persistent consumer price inflation erodes the real purchasing power of fixed future coupon payments. * Extended duration risk forces institutional capital to demand a higher risk premium before locking away funds.

The Precious Metals Pricing Dynamic

International precious metal demand faces a severe headwind from American currency strength. The inverse relationship between a strong US dollar and gold means international buyers face diminished global purchasing power when acquiring dollar-denominated commodities.

Gold prices are holding in the range of $4,700 to $4,828 per ounce, but they face intense pressure from US Treasury yields. The complete lack of dividend payments makes gold significantly less appealing in a high-rate environment where risk-free government debt offers substantial cash flow.

Precious metal valuations experienced an increase throughout the preceding twenty-four months before this current unwinding. This massive prior appreciation left the asset class highly vulnerable to a sharp correction once borrowing costs remained elevated for longer than the market anticipated. By understanding these exact macroeconomic levers, investors can better anticipate which economic signals might eventually trigger a market recovery.

Rethinking Traditional Defensive Fundamentals in a High-Rate World

Investors traditionally flock to defensive investments during periods of volatility because these instruments are designed to preserve capital. The core characteristic of these holdings is their historical negative correlation with risk assets. When growth stocks fall, these protective instruments are expected to hold steady or increase in value.

However, a fundamental difference exists between price volatility and yield generation in the fixed-income market. Bond yields and bond prices operate on a strict inverse relationship. When inflation drives central bank interest rates higher, the market price of existing bonds must fall to match the new, higher-yielding environment.

The shifting nature of global supply shocks has fundamentally altered market dynamics, with NBER asset class inflation research highlighting how persistent price pressures actively destroy the traditional hedging benefits of fixed income.

Inflation serves as the natural enemy of assets that do not produce growing cash flow. While gold offers theoretical inflation protection measured over multiple decades, it provides zero income to offset immediate purchasing power losses. Conversely, the concept of coupon payments provides portfolio stability regardless of underlying price changes prior to maturity.

| Asset Class | Traditional Crisis Behaviour | Inflation Crisis Behaviour | Income Generation Potential |

|---|---|---|---|

| Government Bonds | Prices rise as rates fall | Prices fall as rates rise | Fixed coupon payments |

| Physical Gold | Surges on safe-haven demand | Pressured by high yields | Zero yield generation |

| Cash Equivalents | Maintains nominal value | Loses real purchasing power | Floating rate returns |

| Quality Equities | Sells off with broad market | Passes costs to consumers | Growing dividend streams |

This educational framework separates the theoretical purpose of protective assets from their mechanical reality. Investors who grasp these underlying financial concepts are better equipped to implement advanced portfolio strategies.

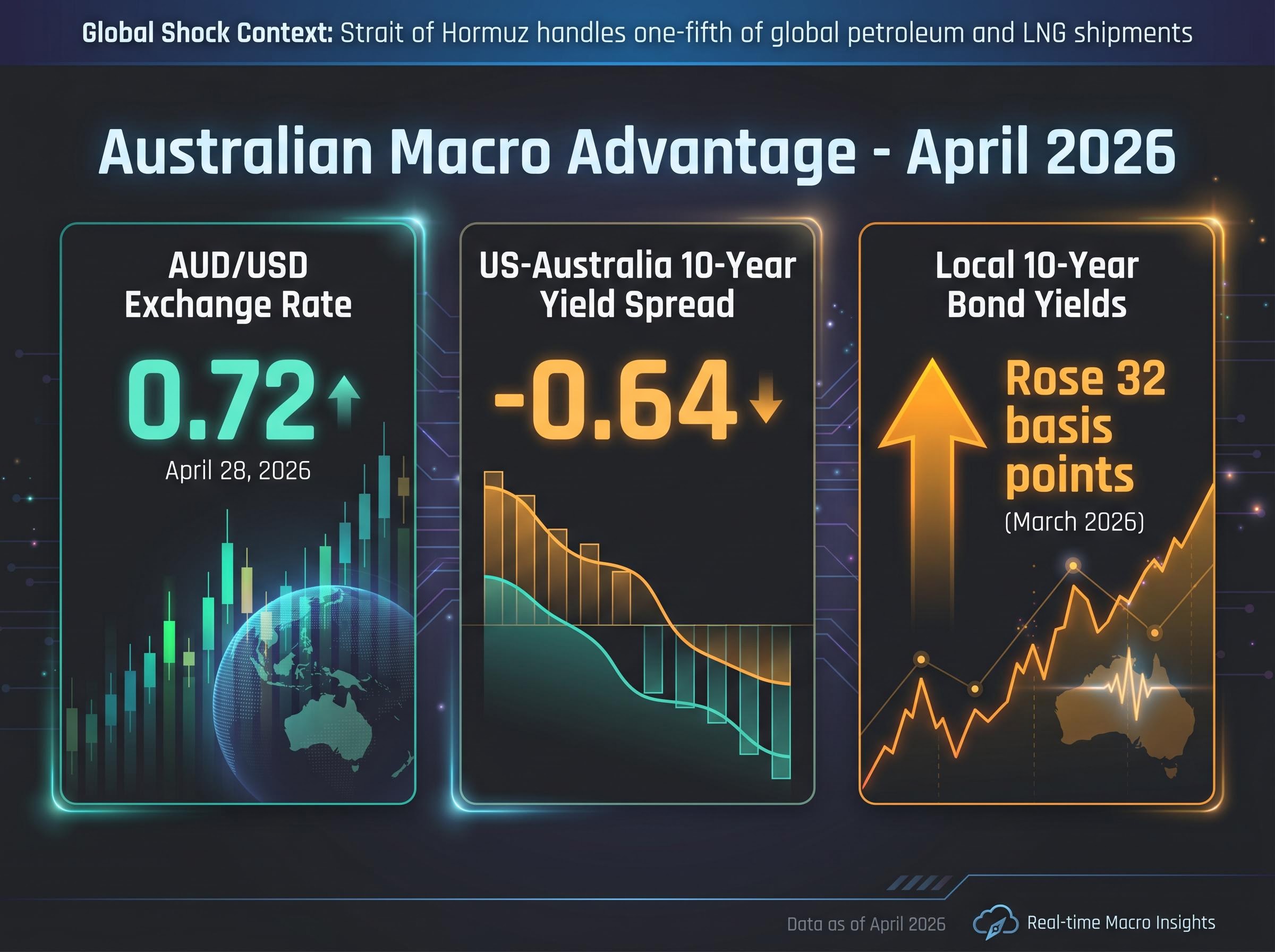

The Australian Currency Advantage Amid Energy Shocks

The global macroeconomic picture looks distinctly different from an Australian vantage point. While energy-dependent nations struggle with imported inflation, the Australian economy shows remarkable resilience as a net energy exporter. This structural advantage directly influences how local portfolios absorb global supply shocks.

The relationship between the Australian Dollar and global energy prices provides a natural buffer for domestic investors. As of April 28, 2026, the AUD/USD exchange rate sits at 0.72. This valuation is heavily dictated by the yield differential, with the US-Australia ten-year yield spread standing at -0.64.

Local ten-year bond yields rose by 32 basis points in March 2026, keeping pace with global movements while reflecting strong domestic economic fundamentals.

Global Currency Divergence

The American currency continues strengthening based on aggressive domestic energy production and elevated domestic interest rates. This dynamic creates a stark contrast with historically defensive currencies that lack domestic commodity backing.

The Japanese currency is rapidly losing its historical defensive position due to the nation’s heavy reliance on imported petroleum. Australian investors must understand how their local currency protects purchasing power differently than international counterparts. This divergence directly impacts strategic decisions regarding whether to hedge global equity investments, as holding unhedged international assets becomes a currency bet as much as an equity play.

Investors exploring geographic diversification as a defense mechanism will find our detailed coverage of international ETFs highly relevant; the guide examines how local capital is increasingly bypassing concentrated ASX sectors to use foreign technology allocations as a primary inflation hedge.

Capitalising on Fixed-Income Yields Despite Price Volatility

Current Australian wealth management guidance emphasises a shift away from fearing bond price drops. Instead, the focus moves toward active curve positioning to capture the long-term income-generating power of current yields.

Market pricing might currently overstate the severity of future monetary tightening. Institutional perspectives suggest that aggressive, sustained rate hikes could precipitate an economic contraction, eventually forcing central banks to pause. Furthermore, historical patterns show financial markets frequently recover from wartime disruptions once a clear trajectory toward resolution emerges.

A modern asset allocation strategy must systematically balance these attractive domestic fixed-income returns against international equity discounts, preparing the overall portfolio for the eventual normalisation of global supply chains.

Wealth managers are taking specific steps to adjust fixed-income allocations right now:

- Rotating capital into short-duration bonds to capture elevated yields while minimising interest rate risk.

- Holding existing high-quality bonds to maturity to guarantee the return of principal regardless of interim price fluctuations.

- Targeting floating-rate credit instruments that automatically adjust their coupon payments upward alongside central bank rates.

- Avoiding long-duration government debt until inflation metrics show three consecutive months of definitive cooling.

This approach turns a perceived market weakness into a strategic income advantage. Investors who shift their focus from daily price volatility to locked-in maturity yields can build highly predictable income streams. By ignoring the daily mark-to-market pricing of their bond holdings, investors can treat fixed income as a reliable cash flow engine rather than a speculative trading vehicle.

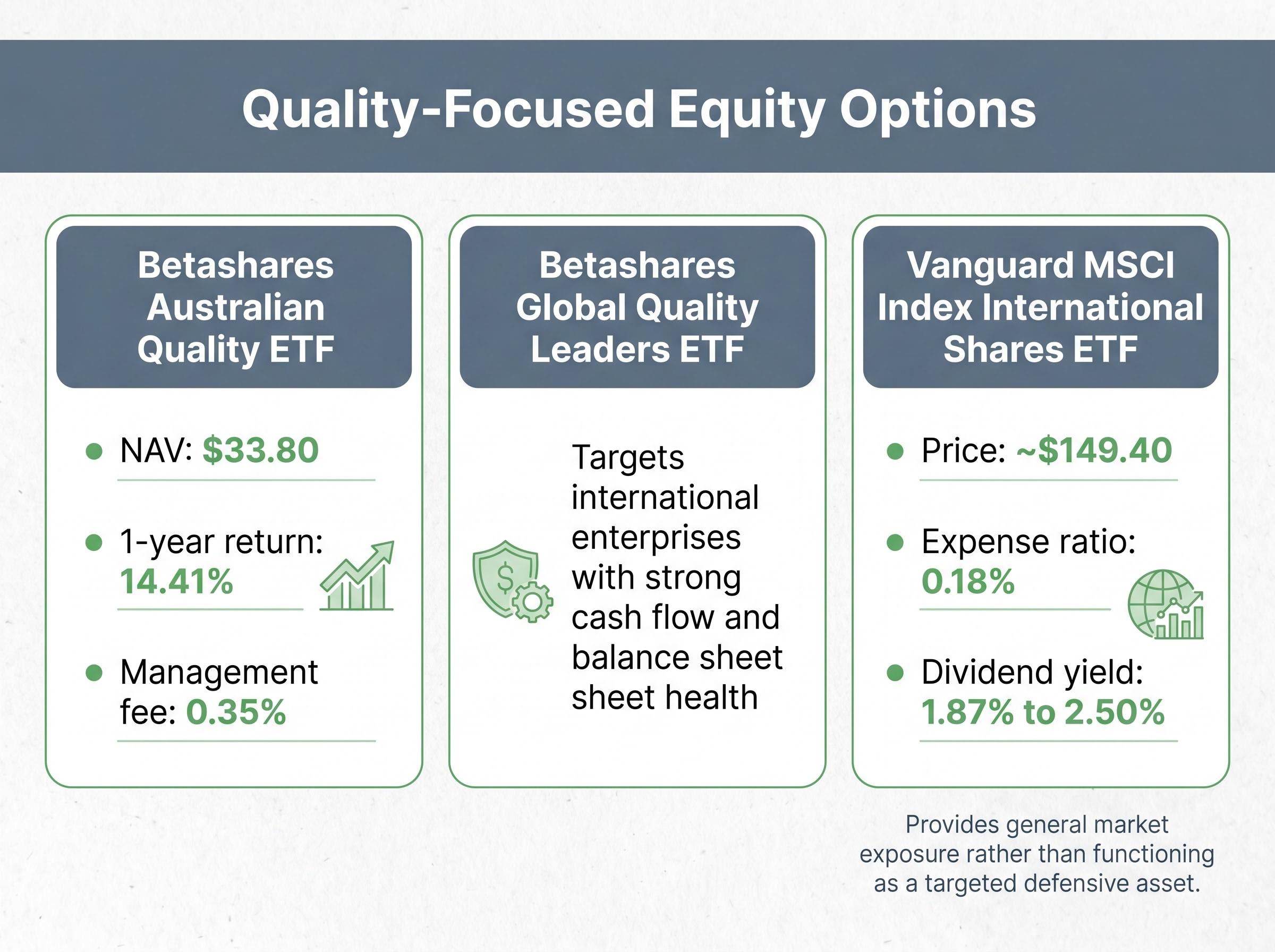

Quality-Focused Equity Strategies for Portfolio Stability

Careful equity allocations can provide the stability currently missing from the traditional bond market. Quality-focused Exchange Traded Funds offer a highly viable alternative for investors seeking capital preservation. These targeted funds select enterprises based on specific defensive characteristics, such as low debt levels, high return on equity, and consistent earnings generation.

A robust inflation investing strategy must now balance these immediate energy shocks against hidden disinflationary megatrends like artificial intelligence, ensuring the portfolio captures both defensive stability and future growth.

Investors must differentiate between targeted quality funds and broad global market exposure. The Australian market offers specific, research-backed financial instruments to build this resilient allocation immediately:

Betashares Australian Quality ETF metrics show a Net Asset Value of $33.80, a one-year return of 14.41%, and a management fee of 0.35%. Betashares Global Quality Leaders ETF methodology targets international enterprises selected specifically for strong cash flow and balance sheet health. * Vanguard MSCI Index International Shares ETF provides broad exposure with a current price around $149.40, a low expense ratio of 0.18%, and a dividend yield of 1.87% to 2.50%. Note that this provides general market exposure rather than functioning as a targeted defensive asset.

Equities with strong pricing power can pass inflationary costs directly to consumers, protecting their profit margins. This fundamental business strength makes quality-factor equities function as modern protective assets when traditional fixed-income instruments fail. Allocating capital to companies with minimal debt requirements effectively neutralises the threat of rising borrowing costs that currently plague the broader market.

Rebuilding a Resilient Portfolio for a Sustained High-Yield Era

The remainder of 2026 requires a definitive shift away from relying solely on traditional protective assets. The new macroeconomic strategy must focus entirely on yield capture and rigorous equity quality. The current environment heavily rewards active duration management and targeted stock selection over passive, set-and-forget defensive allocations.

Investors should position themselves to absorb continued volatility by balancing short-duration fixed income with high-margin, cash-producing equities. Adaptability is the ultimate hedge against persistent inflation and geopolitical uncertainty.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.