United States household credit card debt reached $1.28 trillion in early 2026, yet Bank of America reported the biggest aggregate consumer spending gain since 2023. This jarring contradiction defines the macroeconomic landscape of the current quarter. Strong headline retail figures in April 2026 are masking a deeply fragile reality for the majority of citizens.

Consumers are actively depleting their personal financial reserves to sustain accustomed consumption levels. They are maintaining this spending pace despite severe energy inflation and rapidly rising essential costs. This data-driven analysis looks beneath the surface of the aggregate statistics to identify the underlying funding mechanisms supporting the current market.

The data reveals how inflation disproportionately impacts different demographics across the country. Understanding this structural divergence is essential for assessing the true economic outlook 2026 presents to market participants. Investors relying purely on headline metrics may severely misjudge the stability of the current economic expansion.

Understanding the K-Shaped Consumer Economy

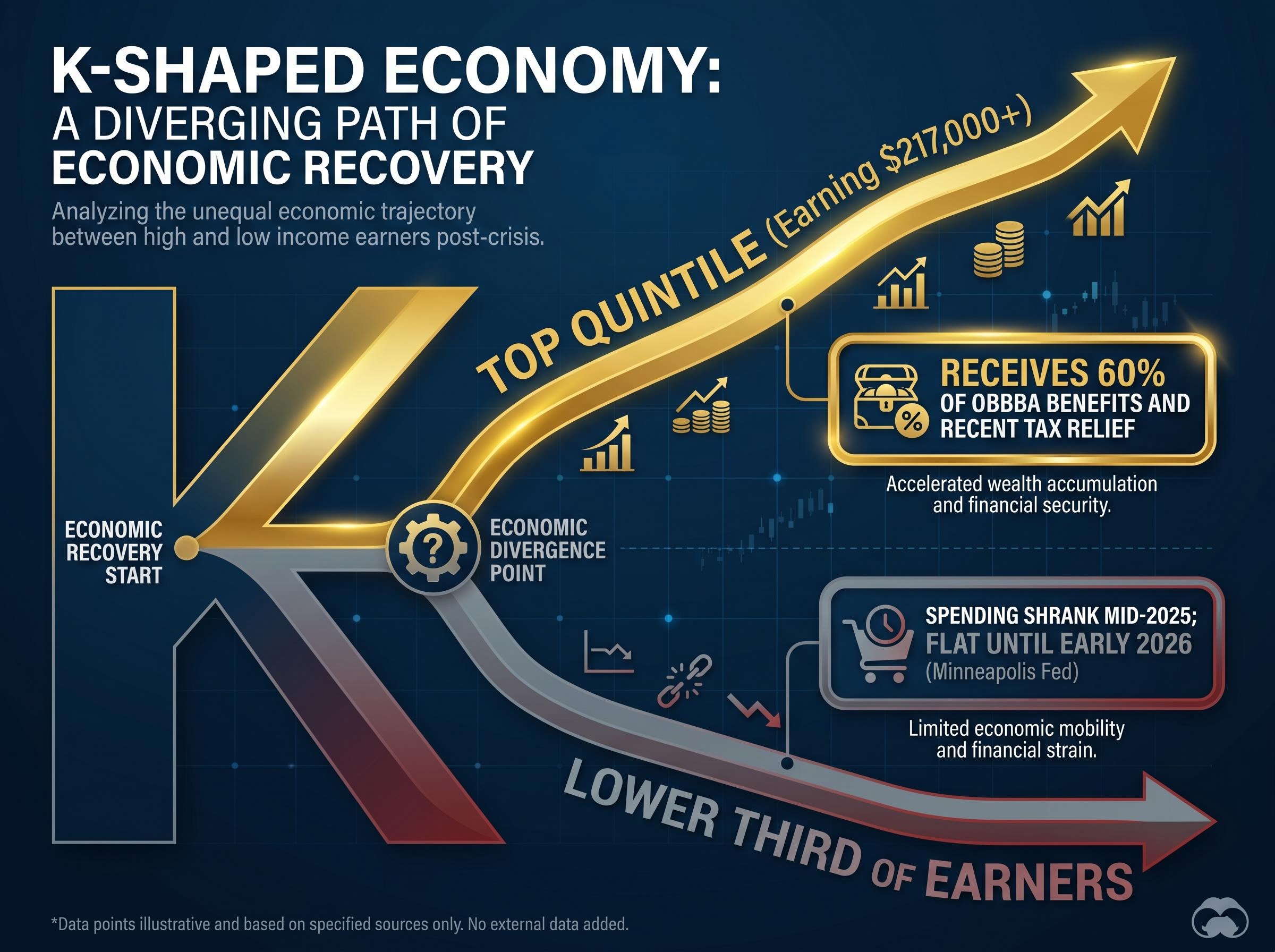

The discrepancy between robust retail sales and rising debt requires a detailed understanding of the K-shaped consumer economy. This economic model describes a scenario where different segments of the population experience diverging financial trajectories simultaneously. While top earners see their wealth accelerate upward, the bottom tiers face compounding financial pressure that erodes their purchasing power.

Aggregate economic metrics combine these two disparate groups into a single national average. When viewed as a whole, the national retail numbers look incredibly strong. Real Personal Consumption Expenditures, a primary measure of domestic spending, increased by 0.10%, or $17.28 billion, in February 2026.

The official Bureau of Economic Analysis consumption data demonstrates how modest top-line aggregate increases obscure the underlying reality of an increasingly strained middle class.

However, top earners are artificially floating these national averages due to structural financial advantages. These include recent tax cuts and exclusive programmatic benefits that largely bypass lower-income households. The divergence between these two demographic groups is stark and measurable:

- The top quintile of households, earning approximately $217,000 or more, receives an estimated 60% of OBBBA benefits and recent tax relief.

- Spending among the lower third of earners shrank in mid-2025 and remained completely flat until early 2026, according to Minneapolis Federal Reserve data.

This structural divide explains why the daily financial news broadcasts seem entirely detached from the reality many consumers experience. Aggregate data obscures the fundamental weakness in the lower and middle tiers of the economy. Investors must segment these household realities to accurately assess broader consumer health.

When big ASX news breaks, our subscribers know first

The Dangerous Disconnect in Household Balance Sheets

The optimistic retail transaction growth captured in recent metrics directly contradicts deteriorating household balance sheets. Bank of America reports that total credit and debit card spending per household increased 4.3% year-over-year in March 2026. On the surface, this transaction volume suggests a confident and expanding consumer base driving the economy forward.

The funding source for this spending tells a much different and highly concerning story. Consumers are executing an unsustainable drawdown of finite personal reserves rather than spending from true economic strength. The United States personal savings rate dropped to a precarious 4.00% in February 2026.

Simultaneously, total United States credit card debt sits at a record $1.28 trillion. The delinquency rate on these credit card loans climbed to 2.94% in late 2025, indicating that borrowers are struggling to service their mounting liabilities.

The New York Fed household debt data confirms that aggregate delinquency transitions are worsening across multiple lending categories, a trend that severely compromises long-term consumer resilience.

| Economic Metric | Current Figure | Macroeconomic Implication |

|---|---|---|

| Card Spending Growth | 4.3% YoY (March 2026) | Suggests robust consumption, but masks the dangerous underlying funding source. |

| Personal Savings Rate | 4.00% (February 2026) | Indicates households are depleting cash reserves rapidly to maintain lifestyles. |

| Credit Card Debt | $1.28 trillion (Early 2026) | Reveals a heavy reliance on high-interest debt to offset elevated inflation. |

Top economists warn that this illusion of financial resilience cannot continue indefinitely without structural consequences.

By revealing the debt funding the current spending spree, the unsustainability of the macroeconomic expansion becomes clear. This insight helps portfolio managers prepare for an inevitable contraction in aggregate demand as credit limits are reached.

The Invisible Squeeze of Energy and Essential Costs

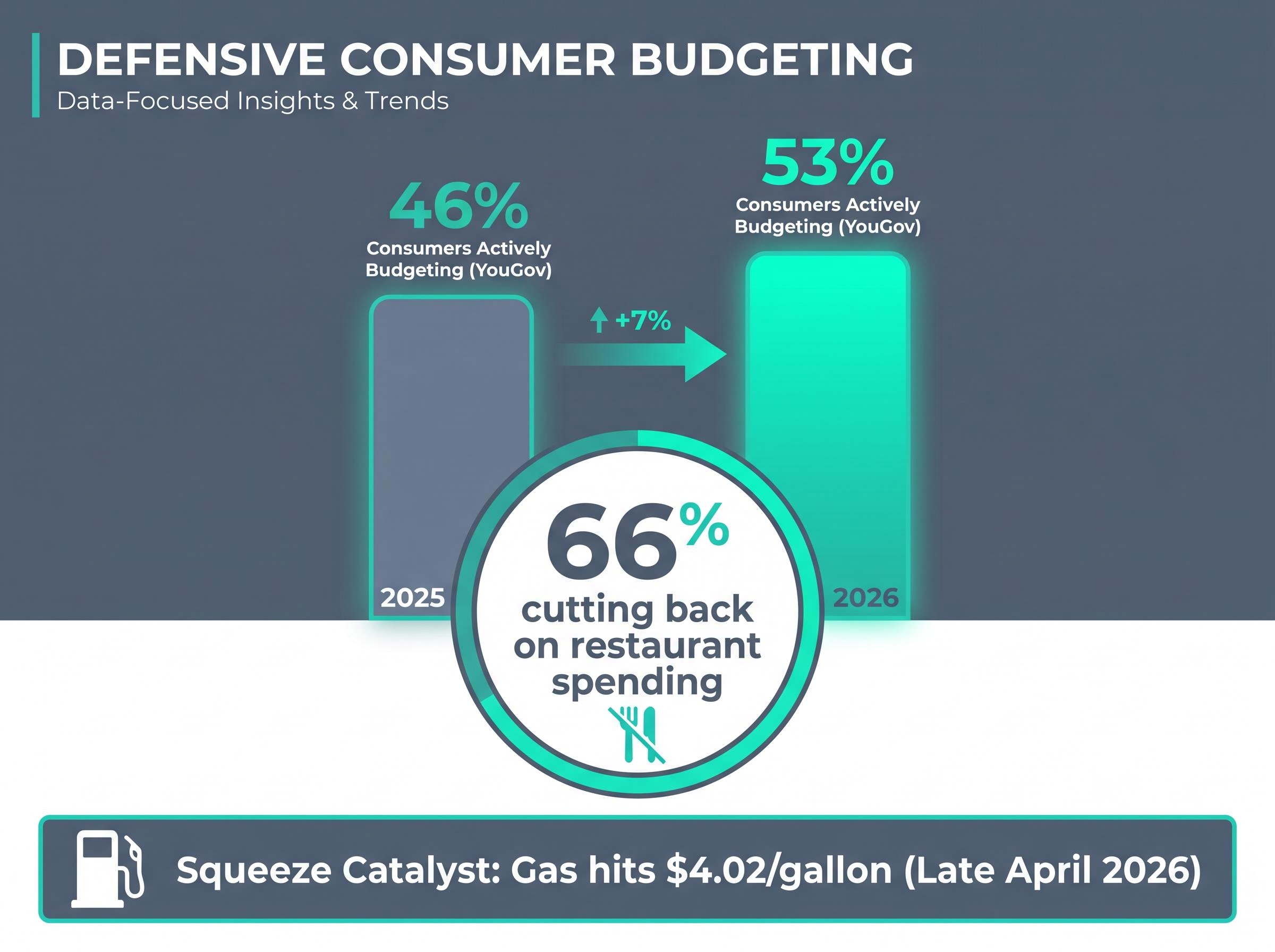

These abstract financial statistics translate into a daily struggle for lower-income earners facing high gasoline prices. The national average gasoline price reached $4.02 per gallon in late April 2026. Rising vehicle fuel operates as a highly regressive tax on the lower and middle classes, absorbing capital that would otherwise flow into discretionary retail sectors.

Elevated housing and utility costs are adding significant, unavoidable pressure to these constrained household budgets. This squeeze is forcing households to abandon nondiscretionary spending, including quality groceries and preventative healthcare. Deloitte research notes that spending on essentials is softening as consumer financial well-being metrics show a sharp pullback in overall purchasing intent.

A profound psychological shift in consumer behaviour is currently underway across the economy. Shoppers are moving away from confident purchasing and adopting defensive budgeting strategies to survive the inflationary environment. YouGov trend data for 2026 reveals that 53% of consumers are actively budgeting, up from 46% in 2025.

Dining out: 66% of cautious consumers are actively cutting back on restaurant spending. Wellness: Households are delaying elective health and personal care expenditures to preserve cash. * Discretionary retail: Apparel and electronics purchases are seeing delayed upgrade cycles as priorities shift.

This data grounds the macroeconomic theory in practical, daily realities. It demonstrates exactly where household budgets are breaking down under sustained inflationary pressure.

For investors analyzing the disconnect between retail figures and actual household stress, our deep-dive into US recession risk and consumer sentiment breaks down the dipping confidence metrics and the rapid depletion of financial buffers across the middle class.

Why Equities Ignore the Underlying Household Strain

Despite these fundamental economic weaknesses, equity markets remain largely detached from household realities. Stock valuations sit at unprecedented highs, driven by a collective dismissal of underlying inflation data and international conflicts. United States GDP growth is forecasted at a resilient 2.4% for 2026, providing surface-level justification for bullish institutional positioning.

Market psychology is currently dominated by the assumption of a soft landing and falling unemployment. American Association of Individual Investors survey statistics from mid-April 2026 show equity participants hold optimistic market outlooks. This bullishness is up significantly from levels documented before the Iran conflict escalated earlier in the year.

Market participants are actively ignoring imminent financial threats in favour of momentum trading. They are overlooking the fact that the projected growth heavily relies on perfect policy execution by central banks.

Geopolitical Blindspots in Current Valuations

Traders currently lack clear frameworks for pricing international instability into their equity models. The market’s inability to quantify these external shocks leaves valuations highly exposed to sudden downward revisions.

This reliance on rigid algorithmic pricing models creates substantial market correction risk, as automated trading systems typically treat structural supply shocks as standard market dips rather than fundamental disruptions.

If regional conflicts further disrupt global energy supply chains, the macroeconomic fallout could be severe. A sudden spike in oil prices would exacerbate the household budget squeeze, collapsing the consumer spending metrics that currently support the equity narrative. This disconnect between consumer strain and stock market risk warns of a potential sudden equity correction when reality catches up to market sentiment.

The Inevitable Reckoning for Consumer Resilience

The appearance of strong headline retail figures is an economic illusion heavily funded by debt and rapid savings depletion. While overall United States GDP growth forecasts appear stable at 2.4%, the unequal distribution of this growth leaves the broader economy deeply vulnerable. The K-shaped recovery has isolated the lower and middle classes from the benefits of the current expansion.

This accelerated economic bifurcation means that corporate earnings reliant on mass-market discretionary spending will inevitably collapse once lower-tier consumers exhaust their remaining credit facilities.

The gap between soaring equity valuations and deteriorating household balance sheets cannot expand indefinitely. As labour markets and credit cycles normalise in the second half of 2026, the mounting debt burden will likely force a sharp contraction in consumer spending. Investors and households alike must position themselves defensively to navigate this impending transition.

Past performance does not guarantee future results, and forward-looking financial projections are subject to volatile market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.