Global oil prices surged from $72 per barrel in late February 2026 to nearly $120 by early March, creating an immediate cost burden across the global economy. The sheer velocity of this Middle East supply disruption has forced institutional investors to reassess their baseline economic assumptions for the year.

As of late April 2026, Brent crude remains elevated above $103, yet financial markets are paradoxically pricing in a temporary scenario where initial interest rate hikes will quickly give way to broader growth concerns.

Assessing the Australian inflation outlook requires looking beyond daily commodity fluctuations to understand the competing macroeconomic currents. The current energy shock will likely force a short-term rate spike from domestic central bankers. However, understanding the hidden structural forces working beneath the surface reveals why long-term economic damage may be firmly capped.

Decoding the April 2026 Oil Shock and the Backwardation Signal

The immediate reality of the energy crisis is visible in spot markets, where prices reflect a severe disruption in Middle East oil exports. As of 29 April 2026, the daily energy complex reflects acute near-term supply anxiety.

Beneath this immediate anxiety, shifting global energy dynamics are fundamentally altering long-term supply models; major developments like the impending departure of the United Arab Emirates from OPEC suggest that traditional cartel pricing power may eventually weaken.

Brent crude spot prices are trading at approximately $103.40 per barrel, recording a 4.84% daily increase. West Texas Intermediate (WTI) crude spot prices sit at approximately $91.06 per barrel, up 5.99% daily.

While headline prices suggest panic, the structure of the oil futures curve tells a different story. The market is currently in a state of deep backwardation, a condition where near-term futures contracts trade at substantial premiums to longer-dated delivery months. This pricing structure serves as Wall Street’s clearest signal that commercial traders expect the current crisis to normalise rather than deteriorate permanently.

“WTI prices for December 2026 delivery are trading as much as $40 below front-month May and June contracts, providing a definitive market signal that the supply crunch is viewed as temporary.”

Understanding the difference between current spot prices and future contract pricing prevents panic-driven decisions based solely on daily headlines. The massive discount in forward pricing indicates that while the immediate supply crunch is severe, institutional capital is betting heavily on supply stabilisation within six months.

When big ASX news breaks, our subscribers know first

How Supply Disruptions Dictate Central Bank Action

Central banks operate under specific mechanical mandates when facing severe supply disruptions. When core inputs like energy become scarce, the resulting price increases bleed across the broader economy, forcing monetary policymakers to act even if economic growth is already slowing.

The primary tool central banks use to regulate demand when supply cannot respond is the benchmark interest rate. By raising the cost of borrowing, policymakers intentionally cool consumer purchasing behaviour to bring aggregate demand back into balance with constrained supply.

- Policy committees raise benchmark interest rates, immediately increasing the cost of interbank lending.

- Commercial banks pass these costs to consumers through higher mortgage and commercial loan rates.

- Discretionary income contracts as debt servicing costs rise, destroying surplus consumer demand.

Historical precedent and institutional frameworks guide this defensive posturing. The Taylor Rule, a standard monetary policy benchmark, dictates an interest rate increase for surplus price growth.

The International Monetary Fund (IMF) has quantified the broader economic cost of this transmission mechanism. According to IMF analysis, true economic output typically decreases when price growth surpasses the baseline. This fundamental relationship explains why central bank announcements logically prioritise demand destruction over short-term economic expansion during commodity shocks.

Published IMF working paper analysis demonstrates how global commodity price shocks flow directly into core inflation metrics, forcing a sharp contractionary response from policymakers. The resulting reduction in broad money supply is intentionally designed to curb excessive consumer demand.

The Reserve Bank of Australia and May 2026 Rate Expectations

The global macroeconomic theory is rapidly translating into domestic borrowing costs across Australia. The persistent fuel crisis has introduced significant imported cost pressures, forcing the Reserve Bank of Australia (RBA) into a highly defensive monetary posture.

Immediate shifts in Australian interest rate expectations reflect this imported pressure. As of 24 April 2026, the ASX 30 Day Interbank Cash Rate Futures for May 2026 are trading at 95.745. This pricing implies a 74% market probability of an interest rate increase to 4.255%.

There is clear consensus among major Australian financial institutions regarding imminent monetary tightening. National Australia Bank (NAB) analysis indicates that the fuel crisis is directly pushing up prices, leaving the RBA with little choice but to support transient rate increases.

| Financial Institution | May 2026 Forecast | Projected Peak Cash Rate |

|---|---|---|

| Westpac | Increase of 25 basis points (4.35%) | 4.85% |

| Commonwealth Bank (CBA) | Increase Expected | Data Pending |

| National Australia Bank (NAB) | Increase Expected | Data Pending |

| ANZ | Increase Expected | Data Pending |

This alignment provides Australian homeowners and businesses with a clear expectation for their immediate debt obligations. While the RBA is reluctant to punish domestic consumers for international energy disruptions, the mechanics of inflation targeting mandate a strict response.

For local investors looking to restructure their capital against persistent imported cost pressures, our comprehensive walkthrough of ASX portfolio defense provides a systematic framework for prioritising companies with strong pricing power and low debt profiles.

The Hidden Structural Forces Capping the Crisis

While the immediate energy shock dominates headlines, the global economy is simultaneously experiencing massive deflationary pressures that counter the oil surge. These powerful global trends provide the critical context behind why bond markets expect the rate spike to be temporary.

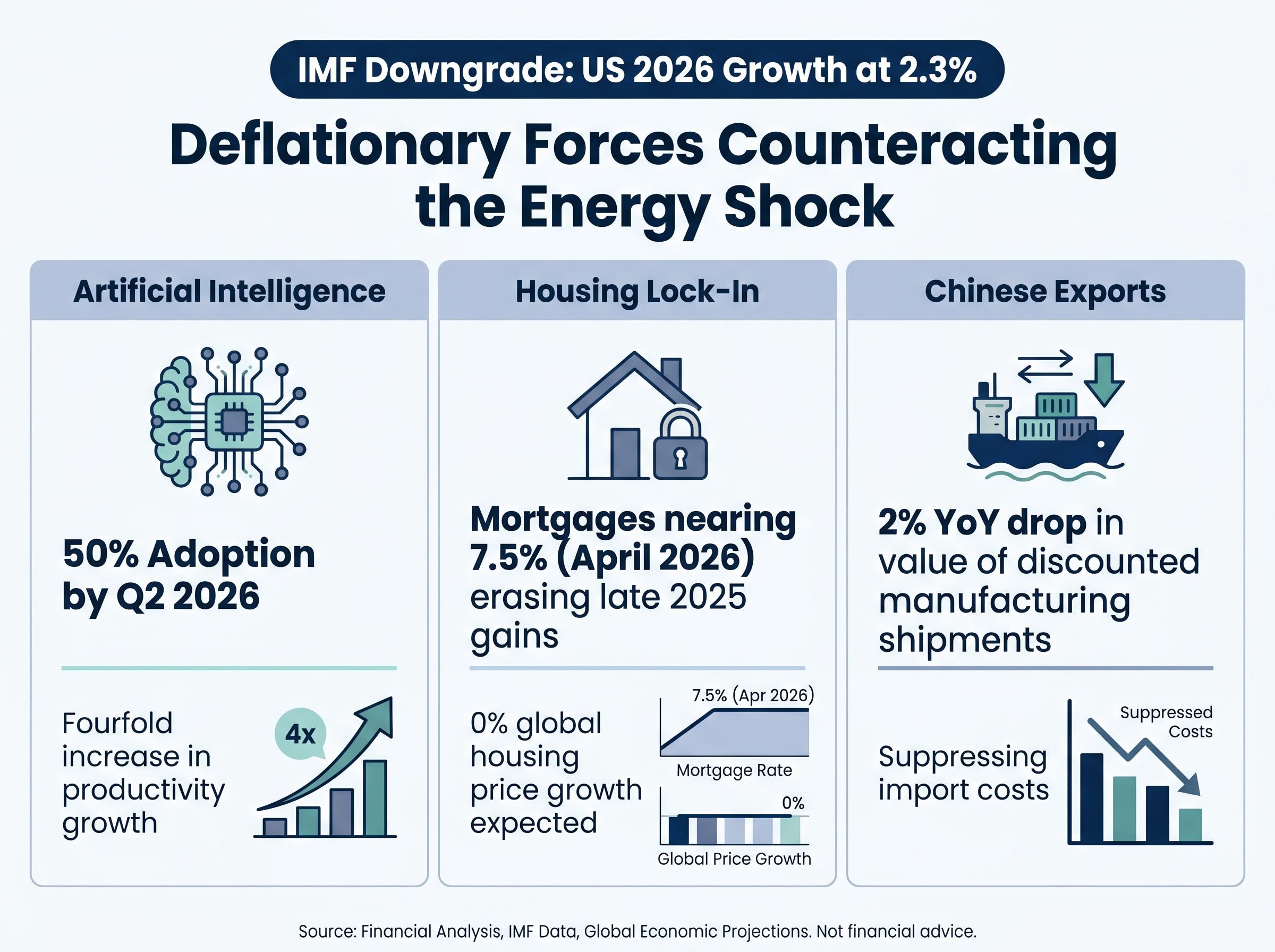

The International Monetary Fund has already downgraded US 2026 economic growth to 2.3% amid the energy crisis, signalling that aggregate demand is cooling.

Productivity Through Artificial Intelligence

Technological advancement is driving unprecedented operational efficiencies across the corporate sector. By the second quarter of 2026, artificial intelligence adoption has reached 50% across measured industries.

This integration has driven a fourfold increase in productivity growth, with enterprises reporting massive gains in operational efficiency and direct improvements in employee output. These technological dividends are actively absorbing higher input costs without requiring equivalent price hikes for end consumers.

Recent NBER economic growth research suggests transformative artificial intelligence can sustainably elevate output by multiples of the historical baseline. This structural shift allows companies to maintain profit margins despite rising energy input costs.

The Global Housing Lock-in Effect

Elevated borrowing costs have effectively frozen global property mobility, acting as a massive anchor on consumer spending. Mortgage rates spiking toward 7.5% in April 2026 have erased the affordability gains recorded in late 2025.

Consequently, global housing prices are expected to stagnate at 0% growth throughout the year. This severe inventory lock-in effect suppresses the broader consumer spending typically associated with property transactions and household formation.

Chinese Export Discounting in Australia

Shifting international trade balances are providing a direct deflationary counterweight for the local Australian economy. Australian import data shows a 2% year-on-year drop in the value of discounted Chinese manufacturing shipments.

With total export values from Australia to China declining, the influx of cheaper industrial goods is actively suppressing import costs. This dynamic helps neutralise the imported price pressures stemming from elevated crude oil prices.

Protecting Capital Through the Six to Twelve Month Window

Translating macroeconomic theory into portfolio strategy requires a clear framework for navigating current volatility. Historically, oil shocks act as a tax on corporate margins rather than operating solely through debt markets. Historical baseline data demonstrates that a 5% rise in oil prices links to a 2.2% drop in corporate earnings over a 12-month period.

Despite the immediate earnings pressure, historical patterns show that rate hikes driven by supply constraints typically begin to reverse within six to twelve months. Australian wealth platform Selfwealth, operated by Syfe, advises investors to prioritise broad diversification over concentrated sector bets during this window.

Alongside broad equity diversification, massive central bank accumulation has created a structural price floor for gold, prompting major institutions like Goldman Sachs to heavily raise their targets for safe-haven commodities heading into late 2026.

Reallocate capital toward resilient sectors that demonstrate strong operational efficiencies. Shift exposure away from highly rate-sensitive equities that rely heavily on short-term borrowing. Increase weighting in elevated fixed-income streams to capture peak yield. Focus on companies demonstrating proven margin protection and exposure to long-term secular themes like artificial intelligence.

These portfolio adjustments provide a defensive mechanism tailored specifically for a high-rate, supply-constrained environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Growth Concerns Will Ultimately Overpower Price Panics

The immediate energy shock of April 2026 is undeniably severe, but it remains structurally contained by broader economic shifts. While Australian borrowing costs will likely rise in the near term as the RBA defends against imported price pressures, historical patterns and forward futures pricing point to a swift reversal.

The deflationary weights of technological productivity, frozen housing markets, and discounted Chinese imports are actively absorbing the impact of $100-plus crude oil.

Maintaining investment discipline through the remainder of 2026 requires looking past the spot market panic. As the year progresses, central banks will inevitably pivot from managing supply-driven price spikes to addressing the broader economic slowdown, rewarding portfolios positioned for the eventual rate normalisation.

For readers interested in how institutional capital is adapting to these diverging crosscurrents, our full explainer on the global inflation rethink details how massive disinflationary counterweights are offsetting commodity price spikes across international markets.