Crude oil breached the $100 threshold in April 2026, sending an immediate supply shock across equity and bond markets worldwide. The sudden geopolitical disruption in the Middle East has directly threatened the delicate pricing progress central banks achieved throughout late 2025, forcing a sudden reassessment of global inflation trajectories. Capital markets are currently suspended between the hard reality of immediate energy shortages and the longer-term structural shifts occurring in technology and international trade.

This analysis maps the underlying forces actively battling to dictate the pricing environment over the next 12 months. It moves beyond initial headline reactions to evaluate the specific mechanisms driving current price growth, central bank divergence, and institutional positioning. By weighing the immediate energy crisis against delayed disinflationary trends, investors can better identify how major institutions are hedging their exposures.

The tension between short-term cost spikes and long-term productivity gains will ultimately determine forward capital allocation strategies.

The Immediate Energy Shock and Baseline Pricing Pressures

The disruption within the Strait of Hormuz has translated directly into elevated petroleum valuations. Traders and analysts entered 2026 expecting a stabilisation in energy markets, but the conflict has forced sharp upward revisions in core economic forecasts. Energy costs are now disproportionately driving the consumer price index across major Western economies, replacing services as the primary engine of price acceleration.

Brent crude trading at approximately $109.85 per barrel as of late April 2026. West Texas Intermediate (WTI) crude tracking at approximately $102.66 per barrel.

The mathematical reality of these elevated input costs is already visible in recent data releases. March 2026 consumer price index metrics revealed unexpected stickiness in broad price levels across multiple jurisdictions. Fixed-income traders are pricing in higher terminal rates, reflecting the belief that central banks cannot ignore these persistent commodity spikes.

This shift in fixed-income expectations frequently exposes underlying equity pricing fragility, particularly when benchmark indices maintain near-record levels despite clear macroeconomic headwinds.

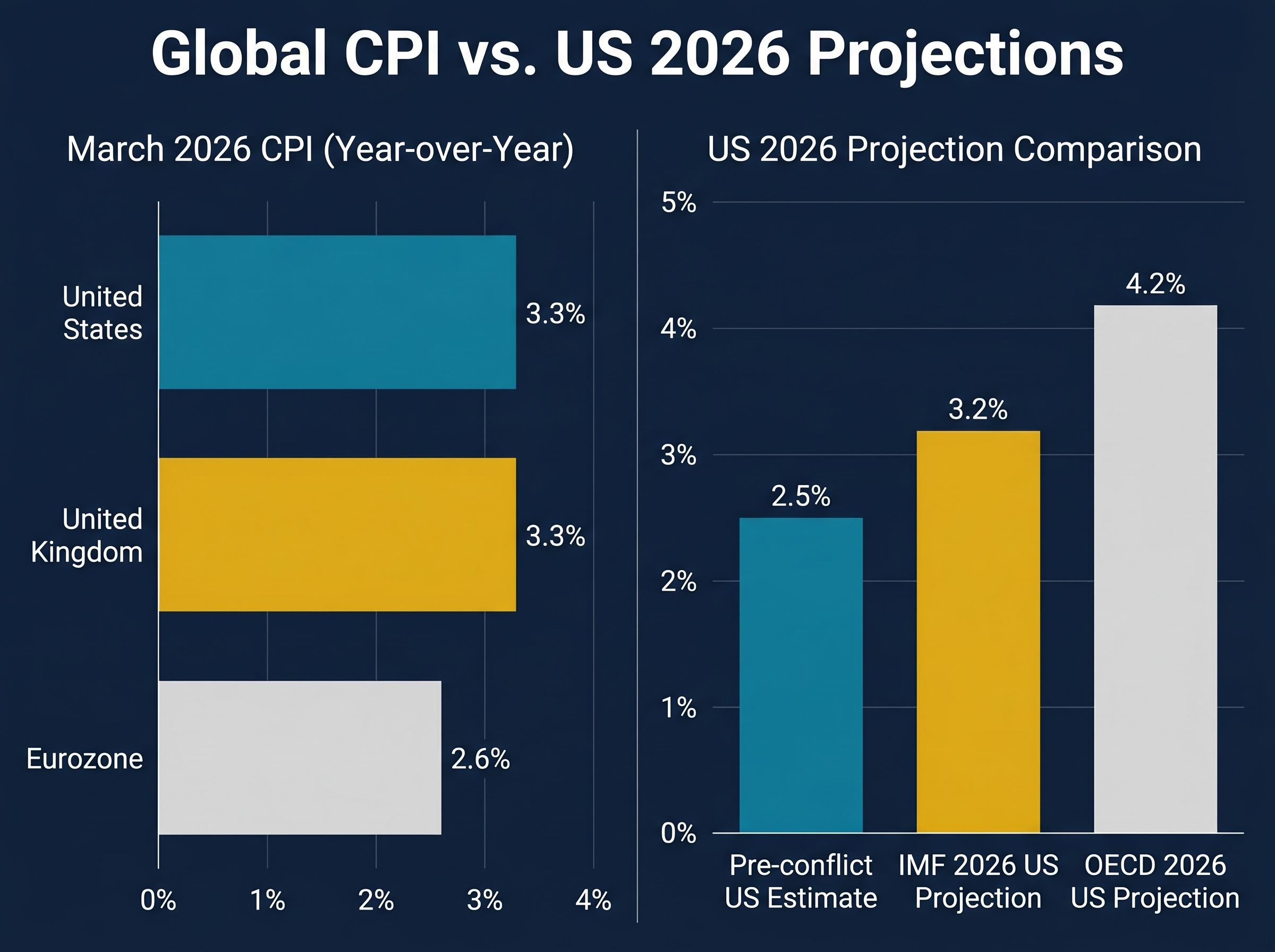

| Region | March 2026 CPI (Year-over-Year) | IMF 2026 Projection | OECD 2026 Projection |

|---|---|---|---|

| United States | 3.3% | 3.2% | 4.2% |

| United Kingdom | 3.3% | Not Specified | Not Specified |

| Eurozone | 2.6% | Not Specified | Not Specified |

This statistical divergence from early-year expectations provides a clear baseline for understanding the current market anxiety. The gap between the 2.5% pre-conflict US inflation estimate and current OECD projections illustrates how rapidly the macroeconomic environment has recalibrated.

When big ASX news breaks, our subscribers know first

The Mechanics of Cost-Push Price Growth and Policy Limits

A supply-side shock differs fundamentally from demand-driven price increases because it constrains economic output while simultaneously raising costs. When energy supplies are artificially restricted, manufacturing and transport expenses rise regardless of underlying consumer demand. Central banks face inherent limitations when deploying their traditional monetary policy toolkit against these external constraints.

Raising benchmark interest rates can cool an overheated economy by reducing consumer borrowing and spending. However, higher borrowing costs cannot resolve physical bottlenecks in the Strait of Hormuz or manufacture additional crude oil. Monetary authorities are therefore forced to choose between tolerating elevated prices or aggressively suppressing economic activity to balance the restricted supply.

“When a developed nation experiences price growth, every subsequent increase diminishes adjusted economic expansion,” according to recent analysis from the International Monetary Fund.

Policy responses are frequently guided by the Taylor Rule framework. This model suggests benchmark rates should rise for each percentage point that price growth exceeds target levels. Applying this strictly to supply shocks carries significant risk of severe recessionary outcomes.

Analysts have modeled how energy-driven recession risk develops during a supply shock, noting that reduced consumer spending and elevated business input costs operate simultaneously to constrict economic output.

Navigating the Historical Precedents

Historical parallels demonstrate the difficulty of achieving economic normalisation during prolonged petroleum constraints. The energy crises of the 1970s required aggressive monetary tightening by the Federal Reserve, eventually leading to the severe economic contractions of 1980 through 1982.

These historical interventions carried significant collateral damage. The relationship between compressed price acceleration and rising joblessness remains a primary concern for modern policymakers evaluating current intervention strategies.

Central Bank Divergence and Shifting Forward Guidance

The global monetary consensus is actively fracturing as regional authorities respond to the petroleum supply shock. Early 2026 optimism regarding coordinated interest rate reductions has dissolved into cautious rhetoric and renewed tightening warnings. The pass-through risks from elevated transport and input costs are forcing a rapid recalculation of mid-year timelines.

Geographical divergence in policy responses is becoming particularly pronounced across major economic zones.

The US Federal Reserve has pivoted away from expected June 2026 rate cuts, driven by average US gasoline prices tracking at $2.908 per gallon. The European Central Bank held rates steady in April 2026 but formally signalled the potential for 50 basis point hikes if current pressures persist. * The Reserve Bank of Australia explicitly cited fuel costs as the primary obstacle to reaching target levels.

These distinct regional challenges reflect varying exposures to energy imports and local currency valuations against the US dollar. The Federal Reserve’s delayed timeline places additional pressure on foreign central banks to maintain higher yields, preventing capital outflows to US debt markets. Investors are closely monitoring these specific policy triggers to gauge the trajectory of bond yields and borrowing costs over the coming quarter.

For readers wanting to explore how geopolitical tension specifically alters monetary policy, our full explainer on Fed interest rate projections details why financial markets have actively recalibrated their easing expectations toward late 2027.

The Structural Counter-Forces Masking Long-Term Trends

While immediate energy shocks dominate market headlines, powerful underlying disinflationary currents are actively developing beneath the surface. Market indicators in petroleum derivative markets are currently showing backwardation, a pricing structure where near-term contracts trade at premiums to longer-dated futures. This technical formation signals trader anticipation that current supply bottlenecks will resolve over the coming months, allowing inventory levels to normalise.

Beyond commodity markets, economists are actively debating the true near-term impact of artificial intelligence on productivity and pricing.

AI Productivity Versus Manufacturing Gluts

Economists from Bank of America maintain that long-term AI efficiency gains will eventually offset wartime pricing pressures. Conversely, analysts at RBC and The Economist caution that artificial intelligence is not yet providing a broad enough productivity boost in 2026 to counter the current energy spike effectively.

However, global trade dynamics are actively suppressing goods pricing despite elevated shipping costs. Inexpensive Chinese manufacturing exports continue to flood international markets as producers navigate changing tariff structures. Analysts from ING and The Economist project that this growing export volume will act as a massive structural deflationary force.

The latest macroeconomic analysis of Chinese deflation frames this industrial overcapacity as a direct export of lower prices to Western economies, effectively neutralizing localized inflation spikes.

This dynamic creates a complex macroeconomic environment where delayed technological efficiency gains contrast sharply with the immediate pricing impact of merchandise gluts. The structural shifts in supply chains are quietly working to offset the geopolitical premiums built into current commodity valuations.

Institutional Portfolio Adjustments and Asset Rotations

Institutional capital is actively repositioning to navigate these conflicting macroeconomic forces. Major wealth managers and institutional analysts are adopting increasingly defensive postures to protect against margin compression in equity markets. This shift translates macroeconomic theory into observable market realities.

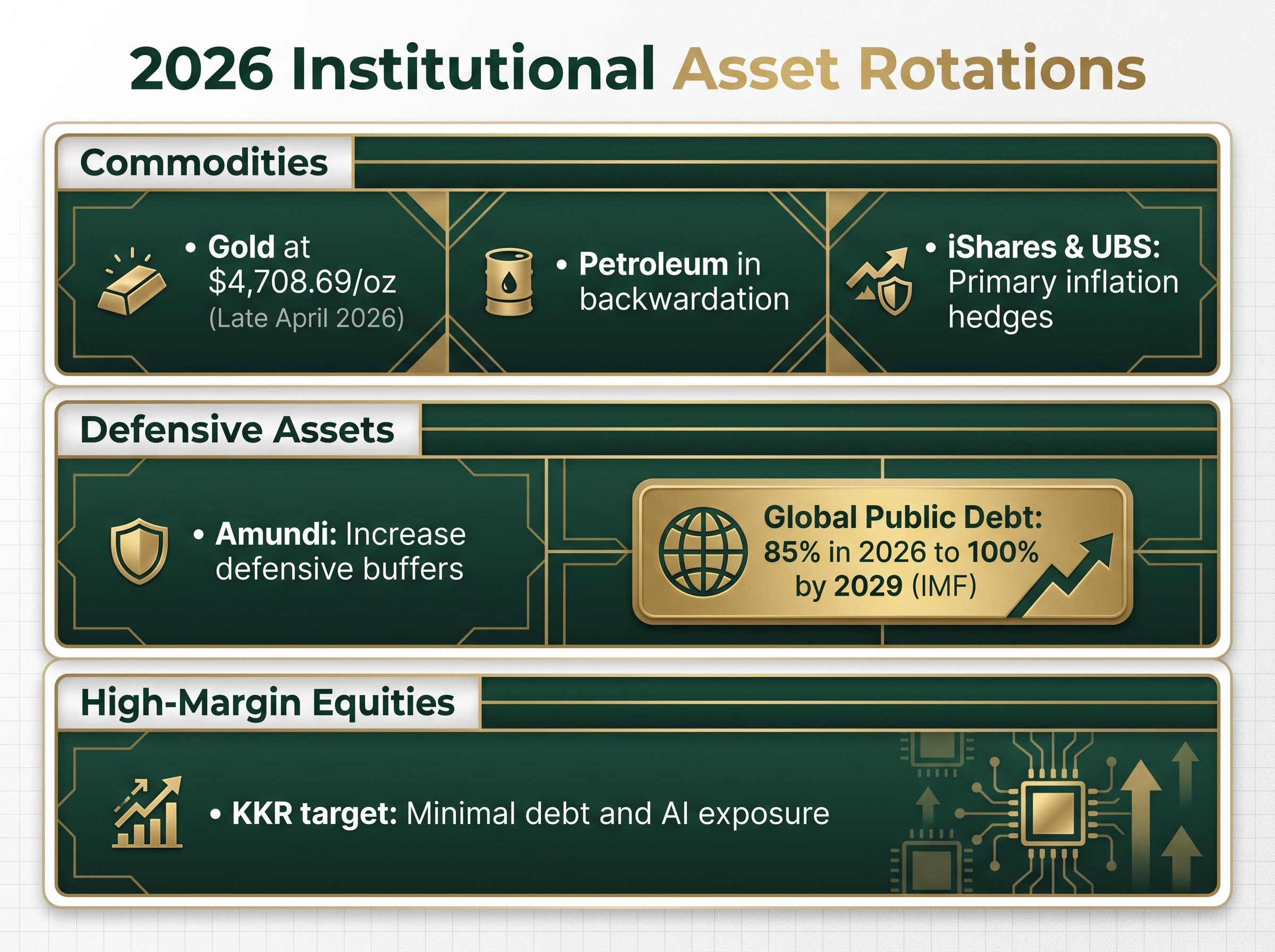

Traditional safe assets are demonstrating unexpected resilience against elevated interest rate expectations. Gold has maintained its established role amid geopolitical tension, trading at approximately $4,708.69 per ounce in late April 2026 with no recent declines. Meanwhile, sovereign debt markets face looming pressures, with global public debt projected by the IMF to hit 100% of GDP by 2029, up from the current OECD average of 85% for 2026.

The official IMF baseline macroeconomic projections underscore these fiscal vulnerabilities, indicating that higher borrowing costs will heavily restrict government spending capacities in the coming years.

Institutions are deploying specific strategies to generate cash flow while awaiting clarity on future borrowing costs. Recommendations from major firms highlight a defensive rotation.

| Asset Class | Current 2026 Status | Institutional Stance |

|---|---|---|

| Commodities | Petroleum in backwardation; Gold at $4,708.69 per ounce | iShares and UBS recommend allocations to serve as primary inflation hedges. |

| Defensive Assets | Sovereign debt yields remain elevated amid rising public deficits | Amundi advises increasing defensive buffers against heightened market volatility. |

| High-Margin Equities | Facing modest drawdowns from growing margin compression fears | KKR targets highly profitable enterprises with minimal debt burdens and AI exposure. |

These strategic rotations provide a blueprint for evaluating portfolio diversification. Asset managers are prioritising companies capable of absorbing higher input costs without destroying demand for their end products.

Mapping the Trajectory of 2026 Capital Markets

The current macroeconomic environment represents a distinct tension between immediate geopolitical energy shocks and the long-term structural forces of artificial intelligence and global manufacturing. Historical data suggests that supply-constrained petroleum crises typically resolve within six to twelve months. This historical precedent urges patience over panic as supply chains adapt to new regional realities.

While institutional managers continue hedging their duration risk, retail investor sentiment has remained surprisingly optimistic, highlighting a growing behavioral divide in how market participants weigh geopolitical threats.

Institutional positioning indicates a clear preference for capital preservation, strong liquidity, and disciplined automated purchasing strategies through this period of elevated volatility.

These statements are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.